ID : MRU_ 432288 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

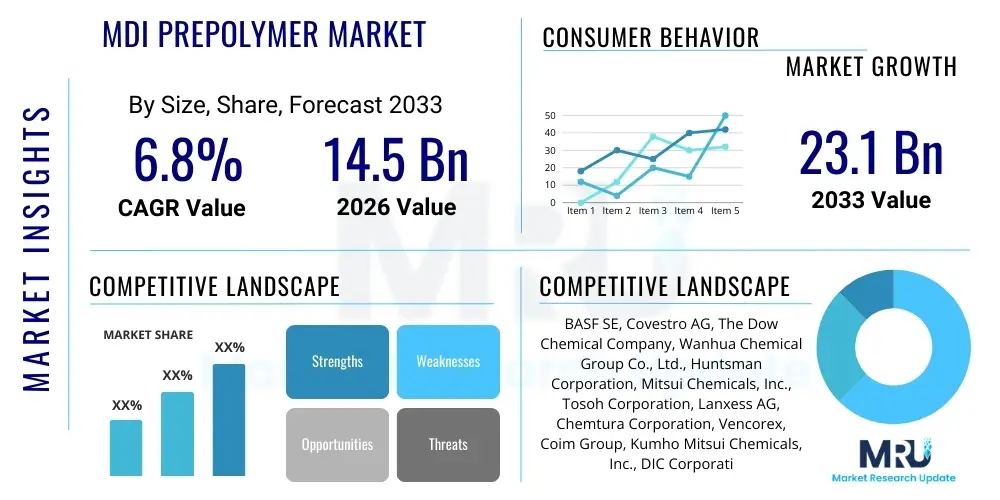

The MDI Prepolymer Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at $14.5 Billion in 2026 and is projected to reach $23.1 Billion by the end of the forecast period in 2033.

The MDI Prepolymer Market centers around specialized intermediate chemicals produced by reacting MDI (Methylene Diphenyl Diisocyanate) with a polyol (such as polyether polyols or polyester polyols) in a stoichiometric ratio where the NCO content is carefully controlled. These prepolymers are crucial components in the manufacture of high-performance polyurethanes, offering significant advantages over systems using raw MDI or mixtures, primarily through improved handling safety, enhanced material properties, and reduced volatility. The precise structure and molecular weight of the prepolymer dictate the final physical characteristics of the resultant polyurethane product, including hardness, flexibility, chemical resistance, and tensile strength, making them indispensable in demanding applications.

MDI prepolymers find major applications across diverse industries, notably in construction, automotive, footwear, and consumer goods. In construction, they are vital for producing high-efficiency insulation foams, sealants, and coatings known for their excellent thermal properties and durability. The automotive sector utilizes MDI prepolymers for manufacturing resilient seating foams, elastomeric components, and robust adhesives. Key benefits driving the market adoption include the ability to formulate polyurethanes with specific, tailored properties, excellent processability, and, crucially, reduced free monomer content, addressing growing regulatory concerns regarding workplace exposure to volatile isocyanates.

The primary driving factors sustaining market growth include the surging demand for energy-efficient building materials, especially high-R-value polyurethane insulation foams, spurred by global energy conservation mandates. Furthermore, the expansion of the electric vehicle (EV) sector, which requires specialized lightweight and durable polyurethane components for battery encapsulation and structural integrity, provides a significant impetus. The increasing preference for safer, lower-volatility systems compared to traditional pure MDI usage, coupled with innovation in bio-based and renewable polyols integrated into prepolymer formulations, continues to solidify MDI prepolymers' role as foundational components in advanced material science.

The MDI Prepolymer market is characterized by robust growth driven fundamentally by global infrastructure development and stringent energy efficiency regulations across industrialized nations. Key business trends include a strategic shift towards customizing prepolymer formulations to meet specific application demands in high-growth areas like specialized adhesives, advanced coatings (e.g., polyurea hybrid systems), and microcellular elastomers, moving beyond traditional rigid foam applications. The market structure features moderate consolidation among major integrated producers, who leverage feedstock backward integration to maintain competitive pricing and supply stability. Additionally, increasing investment in research focusing on low-monomer (< 0.1% free MDI) prepolymers is shaping product development and compliance strategies, particularly in regions with tight occupational health standards.

Regionally, Asia Pacific (APAC) stands out as the primary engine of growth, fueled by massive urbanization, infrastructure projects in China and India, and the rapid expansion of manufacturing capabilities, including footwear and automotive production, particularly in Southeast Asia. North America and Europe, while mature, demonstrate stable demand, driven primarily by replacement cycles, remodeling activities, and the strong adoption of high-performance, spray-applied polyurethanes for roofing and building envelopes. Regulatory pressures in Europe, especially concerning chemical safety and sustainability, are accelerating the adoption of innovative, solvent-free, and bio-based prepolymer derivatives.

Segmentation trends indicate that the rigid foam segment, critical for cold chain logistics and insulation, retains the largest market share, but flexible foams and coatings, adhesives, sealants, and elastomers (CASE) applications are exhibiting the highest growth trajectories. Polyether polyol-based prepolymers dominate due to their superior hydrolytic stability and versatility, though polyester-based prepolymers maintain relevance in applications requiring high mechanical strength and abrasion resistance. The trend is moving towards customized, specialty prepolymers that offer enhanced physical properties and processability for highly automated manufacturing environments.

Common user questions regarding the impact of AI on the MDI Prepolymer Market primarily revolve around operational efficiency, new product discovery, and supply chain resilience. Users frequently ask if AI can optimize complex polyol-MDI reaction processes, how machine learning might accelerate the development of novel prepolymer formulations (e.g., predicting properties based on reactant ratios), and whether AI tools can enhance predictive maintenance for continuous reactors. Key themes emerging from this analysis include the expectation that AI and advanced analytics will fundamentally transform manufacturing precision, drastically reduce formulation time for new custom products, and provide real-time optimization of raw material sourcing and inventory management, thereby improving profitability and consistency in production environments that require highly precise chemical synthesis.

The MDI Prepolymer market is significantly influenced by a dynamic interplay of market Drivers (D), Restraints (R), and Opportunities (O), which together dictate the Impact Forces shaping its trajectory. The dominant driver remains the increasing global emphasis on energy conservation, spurring demand for high-performance polyurethane insulation in residential and commercial construction, alongside rapid expansion in the automotive lightweighting sector. However, the market faces constraints primarily related to the fluctuating prices of key petrochemical feedstocks, especially MDI and crude oil derivatives, which impact manufacturing costs and pricing stability. Furthermore, regulatory scrutiny over isocyanate exposure, despite prepolymers being inherently safer, necessitates continuous investment in complex low-monomer production technologies.

Opportunities for growth are abundant, particularly in emerging application areas such as high-temperature resistant coatings, specialized medical devices requiring biocompatible polyurethane elastomers, and the burgeoning market for wind turbine blades, which utilize MDI-based structural adhesives and sealants. Technological innovation focused on developing bio-based or renewable polyol inputs offers a crucial pathway for differentiation and adherence to sustainability goals, attracting environmentally conscious end-users. These factors collectively create strong positive impact forces pushing the market forward, mitigating the headwinds posed by raw material volatility and regulatory compliance challenges.

The primary impact forces can be summarized as high initial investment requirements for specialized reactor technology versus high return on investment due to the premium nature of customized prepolymers. Geopolitical instability affecting feedstock supply chains constitutes a major external force, while the internal force of technological substitution (e.g., competition from alternative insulation materials) requires continuous product performance enhancement. The overall net impact is moderately positive, driven by irreplaceable functional benefits of polyurethane systems in key industries.

The MDI Prepolymer Market segmentation provides a detailed framework for understanding specific market dynamics based on product type, application, and end-use. Segmentation by NCO content or polyol type (polyether, polyester) allows market players to tailor production processes and marketing strategies to specific performance requirements—polyether-based systems are favored for water resistance and flexibility, while polyester systems are chosen for high tensile strength and abrasion resistance. The application spectrum is broad, encompassing rigid foams, flexible foams, and the lucrative CASE segment, each requiring unique prepolymer characteristics. Rigid foam remains foundational due to its extensive use in construction and refrigeration, but the rapid growth in specialized coatings and high-performance adhesives dictates substantial future opportunities.

The MDI Prepolymer market value chain commences with the upstream extraction and processing of crude oil, which yields benzene and propylene oxide, the fundamental building blocks for MDI (Isocyanates) and polyols (Polyethers/Polyesters), respectively. Key upstream activities involve complex chemical synthesis and distillation processes, often requiring high capital investment and advanced chemical engineering expertise. Major integrated chemical manufacturers, who control the production of both MDI and primary polyols, hold significant leverage in this stage, influencing cost structures and supply stability across the entire chain. Reliability in raw material supply and adherence to rigorous quality specifications are paramount at the upstream level, directly impacting the quality and consistency of the final prepolymer product.

The core manufacturing stage involves the reaction of MDI with polyols under specific temperature and pressure controls to create the prepolymer, characterized by precise NCO percentages and viscosity. This stage is followed by quality assurance testing to meet customer specifications. Distribution channels for MDI prepolymers are highly specialized due to the chemical nature of the product, requiring dedicated logistics compliant with chemical handling regulations. Direct sales are common for large-volume industrial customers (such as major automotive suppliers or foam manufacturers) where customization and technical support are essential. Indirect channels involve regional distributors and specialty chemical agents who manage smaller volumes and provide local technical services to niche application markets, particularly in fragmented geographical regions.

Downstream analysis focuses on the final application industries, primarily construction, automotive, and footwear. End-users process the delivered MDI prepolymers by reacting them with curative agents (e.g., amines, diamines, or specialized polyols) to form the finished polyurethane product (foam, coating, elastomer). The market efficiency is heavily influenced by the technical service and innovation provided by prepolymer manufacturers, helping downstream partners optimize their application processes. Successful value chain management requires robust coordination between material suppliers and application specialists to ensure optimal product performance and compliance with regional safety standards.

Potential customers for MDI prepolymers span a diverse range of manufacturing and construction entities that rely on high-performance polyurethane materials for functionality, durability, and insulation properties. The largest end-user group comprises rigid foam manufacturers supplying the construction and cold chain logistics sectors, requiring prepolymers optimized for high R-value insulation panels and spray foam applications. These customers are driven by stringent thermal efficiency standards and seek consistent, low-viscosity prepolymers that facilitate high production throughput and reliable on-site application.

Another critical customer segment includes manufacturers of automotive components and flexible foams, particularly those involved in producing seating, interior trim, and NVH (Noise, Vibration, and Harshness) dampening solutions. These buyers demand prepolymers that yield foams with excellent resilience, compression set, and specific densities. Furthermore, the burgeoning demand from the CASE sector—including producers of durable protective coatings (e.g., polyurea coatings for pipelines, flooring), industrial adhesives, and high-wear elastomers (e.g., rollers, seals, industrial tires)—represents a high-value customer base seeking custom-formulated prepolymers for superior mechanical and chemical resistance.

The footwear industry, especially manufacturers of high-performance athletic shoe soles and industrial safety boots, represents a significant consumer base for MDI prepolymers used in TPU and microcellular elastomer production. These customers prioritize prepolymers offering excellent abrasion resistance, flexibility, and lightweight characteristics. Additionally, specialized niche markets, such as manufacturers of medical devices (e.g., catheters, wound dressings) and electronic potting compounds, require ultra-low free monomer, medical-grade prepolymers meeting strict biocompatibility and cleanroom standards.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $14.5 Billion |

| Market Forecast in 2033 | $23.1 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | BASF SE, Covestro AG, The Dow Chemical Company, Wanhua Chemical Group Co., Ltd., Huntsman Corporation, Mitsui Chemicals, Inc., Tosoh Corporation, Lanxess AG, Chemtura Corporation, Vencorex, Coim Group, Kumho Mitsui Chemicals, Inc., DIC Corporation, Stepan Company, Carpenter Co., Repsol, FOSHAN SANHAO CHEMICAL CO., LTD., Sanyo Chemical Industries, Ltd., Suntoyo Chemical Co., Ltd., P.T. Polyurethane Technology. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape governing the MDI Prepolymer market is focused heavily on continuous reaction systems designed for precise stoichiometry control and thermal management, essential for achieving narrow NCO content distributions and low free monomer levels. Key technologies include advanced thin-film evaporators and specialized distillation columns utilized by leading producers to reduce the residual MDI monomer content far below regulatory thresholds (typically < 0.1% or < 0.05%), significantly enhancing product safety and handling characteristics. Continuous stir tank reactors (CSTRs) and plug flow reactors are employed, equipped with sophisticated sensor arrays and inline analytical tools (e.g., NCO titration systems) to ensure immediate quality adjustments and high-throughput production efficiency, moving away from less consistent batch processes.

Innovation is also highly concentrated in the development of tailor-made prepolymers that integrate novel polyol chemistries. This includes the use of renewable, bio-based polyols derived from vegetable oils or biomass waste, which directly address sustainability demands without compromising polyurethane performance. Furthermore, specialized compounding techniques are utilized to create hybrid prepolymer systems, often blending MDI with polymeric MDI (PMDI) or other isocyanates to fine-tune reactivity profiles for specific application methods, such as rapid-cure spray coating or reaction injection molding (RIM). The technological push is towards systems that allow for room-temperature processing and possess longer pot lives while maintaining fast demold times.

Digitalization and automation are increasingly crucial technologies, particularly the use of simulation software (e.g., Computational Fluid Dynamics) to model reaction kinetics and flow patterns within the reactors, minimizing unwanted side reactions and optimizing heat transfer. This digital integration allows for "smart manufacturing" environments where production parameters are continuously optimized based on raw material variability, ultimately leading to superior product consistency. The patent landscape shows intense activity surrounding prepolymer modification using catalysts and additives to control viscosity, improve compatibility with blowing agents, and enhance fire retardancy in the resulting polyurethane foams.

MDI prepolymers are reaction intermediates with significantly reduced levels of free, volatile MDI monomer compared to raw MDI or PMDI. This reduction minimizes inhalation risk and improves workplace safety, making them preferred materials in high-volume manufacturing settings where reduced volatility and tailored reactivity are required for precise processing.

The construction industry is the largest consumer due to the critical role of MDI-based rigid foams in thermal insulation, driven by global mandates for energy efficiency in residential, commercial, and cold storage applications. Secondary significant segments include the automotive sector for lightweighting and the Coatings, Adhesives, Sealants, and Elastomers (CASE) markets for durable protective materials.

Crude oil serves as the primary feedstock for the synthesis of benzene, which is essential for producing MDI, and for deriving polyether polyols. Therefore, volatility in crude oil pricing directly influences the cost of key raw materials, often leading to increased manufacturing expenses and subsequent price instability in the downstream MDI prepolymer market.

The dominant technological trend is the drive towards ultra-low free MDI monomer prepolymers, typically targeted below 0.1% or 0.05%. This is a direct response to tightening occupational health regulations, particularly in Europe and North America, ensuring safer handling and compliance for customers without sacrificing polyurethane performance characteristics.

The Asia Pacific (APAC) region is projected to register the fastest growth rate, propelled by rapid urbanization, massive government investment in infrastructure development, and the expansion of key manufacturing sectors like automotive and consumer goods across major economies such as China and India, creating immense demand for polyurethane systems.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.