ID : MRU_ 433922 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

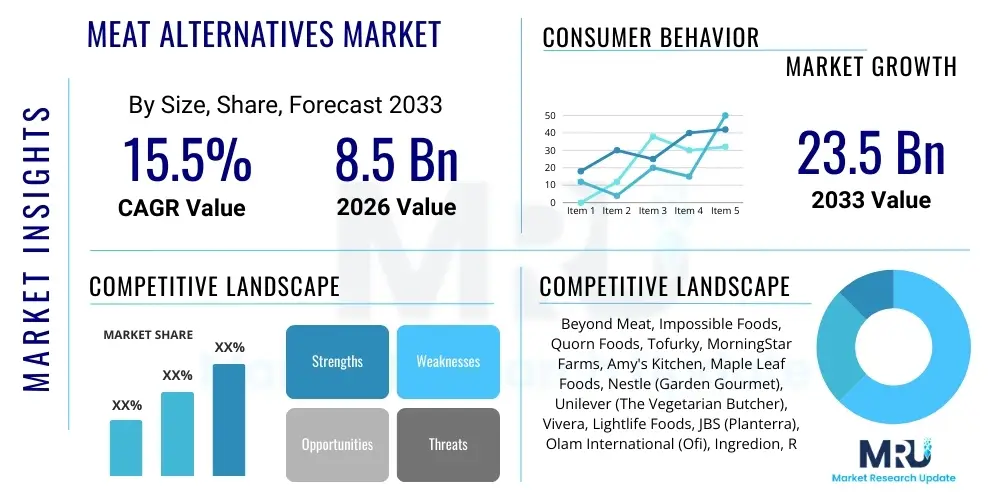

The Meat Alternatives Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.5% between 2026 and 2033. The market is estimated at USD 8.5 Billion in 2026 and is projected to reach USD 23.5 Billion by the end of the forecast period in 2033. This robust growth trajectory is primarily attributed to surging global consumer awareness regarding sustainability, ethical animal welfare concerns, and the perceived health benefits associated with plant-based diets, moving meat alternatives from a niche category to a mainstream dietary choice across developed and emerging economies. Continuous innovation in flavor technology, texture refinement, and the introduction of novel ingredient sources are key factors supporting this exponential market expansion.

The Meat Alternatives Market encompasses food products designed to mimic the aesthetic, chemical, and sensory attributes of conventional animal meat, serving as direct substitutes. These products utilize plant-based proteins, primarily derived from sources such as soy, wheat, peas, and various legumes, or increasingly, innovative fermentation and cell-culturing techniques. The primary applications span across the entire food sector, ranging from retail consumer packaged goods (CPG) to institutional foodservice providers, addressing growing demand for flexitarian, vegetarian, and vegan dietary preferences globally. Products include plant-based burgers, sausages, mince, nuggets, and deli slices, targeting staple dietary consumption patterns traditionally dominated by animal protein.

The core benefit proposition of meat alternatives revolves around environmental sustainability, requiring significantly less land, water, and energy compared to traditional livestock farming, thereby offering a reduced carbon footprint. Furthermore, from a nutritional standpoint, many meat alternative products offer lower saturated fat and cholesterol levels, often incorporating additional fiber, appealing directly to health-conscious consumers seeking proactive dietary management. Major applications include replacement ingredients in ready meals, restaurant menu items, and as direct home-cooking substitutes for beef, pork, and poultry. Market penetration is accelerating due to improved product quality and increasing price parity with conventional meats, especially in premium and specialized segments.

Driving factors for this market include rapid urbanization leading to increased access to diverse food options, proactive health regulations promoting reduced meat consumption in certain regions, and substantial venture capital investment fueling R&D and scaling up production capacity. The shift in consumer perception, treating meat alternatives not just as substitutes but as distinct, high-quality protein options, is critical. Government initiatives supporting sustainable agriculture and dietary diversification also play a pivotal role in accelerating adoption rates across both established markets like North America and Europe, and high-growth markets in Asia Pacific.

The Meat Alternatives Market is characterized by intense innovation and rapid consumer adoption, driven by global megatrends in sustainability and personalized nutrition. Business trends show a strategic movement towards vertical integration among key players, securing proprietary protein sources and enhancing supply chain resilience. Large, established food corporations are actively acquiring smaller, innovative startups or launching their own dedicated plant-based lines, consolidating market share and leveraging existing distribution networks to achieve mass market penetration. Furthermore, there is a pronounced trend toward ‘clean label’ formulations, focusing on fewer, recognizable ingredients to address consumer skepticism regarding highly processed substitutes. The foodservice sector is emerging as a critical growth engine, with major quick-service restaurants (QSRs) and institutional caterers incorporating plant-based options to meet diverse customer demands, moving the products beyond the specialty health food aisle.

Regional trends indicate North America and Europe currently dominate the market in terms of value, owing to high disposable incomes, robust vegan and flexitarian populations, and advanced regulatory frameworks facilitating new product introduction. However, the Asia Pacific (APAC) region is projected to register the highest CAGR, primarily fueled by traditional soy and wheat protein consumption (e.g., Tofu, Seitan) combined with burgeoning Western dietary influence. Specifically, countries like China and India, with historically high rates of vegetarianism and rapidly growing middle classes, present unparalleled long-term growth opportunities. Infrastructure development related to cold chain logistics and improved shelf-life technology are critical enablers for market expansion in these diverse geographic regions.

Segmentation trends highlight that the burger patty category remains the largest in terms of sales volume, benefiting from its high visibility in QSR partnerships. However, product types mimicking whole muscle cuts (e.g., chicken breasts or fish fillets) are demonstrating faster proportional growth, driven by advanced technological capabilities that allow for superior texture replication. Regarding protein sources, pea protein is experiencing significant momentum, challenging the traditional dominance of soy due to its non-allergen status and favorable nutritional profile. The shift towards hybrid products that combine plant proteins with cultured components represents a future segment trend, blurring the lines between current categories and aiming for ultimate sensory replication. Distribution analysis confirms that mainstream retail channels (supermarkets and hypermarkets) are crucial for volume sales, while online channels provide the necessary platform for niche, specialized, or direct-to-consumer (D2C) brands to establish loyalty and optimize logistics efficiency.

Common user inquiries concerning Artificial Intelligence (AI) in the Meat Alternatives Market frequently center on AI’s capacity to accelerate the R&D cycle, specifically regarding flavor and texture optimization, and its role in sustainable supply chain management. Consumers and industry analysts are keenly interested in how AI can solve the persistent sensory gap—the difference in taste, mouthfeel, and cooking performance between plant-based substitutes and their animal counterparts. Key concerns revolve around data privacy when AI models analyze proprietary ingredient mixes and the accessibility of complex AI tools to smaller, artisanal producers. Expectations are high regarding AI’s potential to dramatically reduce development costs and time, allowing for faster scaling and achieving price competitiveness necessary for mass market adoption.

AI’s influence spans the entire product lifecycle, starting from ingredient discovery and optimization. Machine learning algorithms are now being used to analyze thousands of protein structures and their interactions with fats and carbohydrates, predicting how specific plant protein combinations will hydrate, bind, and ultimately replicate the fibrous structure of meat. This predictive modeling drastically cuts down the need for costly, time-consuming wet lab experiments. Furthermore, AI-driven sensory panels and consumer preference mapping utilize large datasets of human feedback and chemical analysis to pinpoint the exact compound combinations required to achieve specific umami notes or textural springiness, enabling rapid iteration of product formulations until sensory perfection is attained.

Beyond product formulation, AI is revolutionizing operational efficiency and sustainability within the meat alternatives supply chain. Predictive analytics optimize sourcing by forecasting crop yields, managing ingredient quality variability, and ensuring ethical sourcing of inputs like pea or soy. In manufacturing, AI monitors fermentation processes and extrusion parameters in real-time, adjusting temperature, pressure, and moisture to maintain consistent texture and quality across vast production batches. This precision manufacturing is crucial for maintaining consumer trust and achieving the necessary economies of scale required to undercut the price point of conventional meat products in the long run. The integration of AI tools ensures cleaner, more efficient, and hyper-personalized product development pathways.

The Meat Alternatives Market is propelled by compelling drivers centered on macro-economic shifts, while simultaneously constrained by structural and sensory challenges. The dominant driver is the escalating global concern over climate change and the environmental impact of industrial animal agriculture; consumers, particularly Millennials and Generation Z, are consciously choosing alternatives with a lower carbon and water footprint. This is complemented by strong health and wellness trends, with consumers seeking to reduce intake of antibiotics, hormones, and saturated fats often associated with conventional meat products. The market benefits significantly from high levels of investment from both venture capital and major food conglomerates, ensuring continuous innovation in ingredients and process technologies (e.g., precision fermentation, biomass fermentation). The growing acceptance and availability in mainstream retail and foodservice channels act as strong market accelerators.

Restraints primarily revolve around sensory attributes and price competitiveness. Despite technological advancements, achieving perfect flavor, aroma, and especially the whole-cut texture replication remains a technical hurdle for many product formats, leading to consumer complaints of an ‘uncanny valley’ effect in comparison to real meat. Furthermore, many current plant-based alternatives are priced at a premium compared to conventional meat, particularly in developing economies, hindering mass adoption among price-sensitive consumers. Regulatory complexity poses another restraint; varying national regulations regarding labeling (e.g., use of terms like ‘meat’ or ‘burger’), food safety standards for novel ingredients (like cultured meat components), and approvals for genetic modification necessitate significant compliance costs, slowing down international market entry and product harmonization.

Opportunities are vast, centering on bridging the gap between current plant-based products and genuine meat sensory experience, primarily through emerging technologies. Precision fermentation and biomass fermentation (using microorganisms to produce specific proteins or ingredients like heme) offer pathways to cleaner labels and superior flavor components, opening up lucrative B2B ingredient markets. The development of hybrid products, combining animal cells (cultured meat) with plant structures, represents a major long-term opportunity aiming for ultimate sensory parity. Additionally, geographical expansion into underserved markets in APAC and Latin America, focusing on regionally relevant proteins and traditional dishes (e.g., plant-based seafood or alternatives for popular local cuisine), will unlock significant new revenue streams. The rising consumer demand for 'clean label' and minimally processed ingredients offers opportunities for companies focusing on whole-food plant-based alternatives with less reliance on complex texturization processes.

Segmentation analysis of the Meat Alternatives Market reveals a highly diverse landscape categorized by protein source, product type, distribution channel, and form. This granular breakdown is crucial for manufacturers to tailor product development and market entry strategies based on regional consumer preferences and regulatory environments. The market exhibits dynamic shifts, where traditional segments like soy and wheat proteins are facing increasing competition from next-generation sources like pea, rice, and fava bean proteins, driven by consumer demand for non-allergenic and sustainable inputs. Product innovation is focusing heavily on moving beyond minced formats (like burgers) toward more complex structures (like whole-cut steaks or seafood analogs) which command higher price points and offer greater differentiation.

The segmentation by distribution channel is vital, reflecting the market’s transition from specialty health food stores to mass-market retail and foodservice. The penetration into quick-service restaurants (QSRs) and casual dining establishments is a key indicator of mainstream acceptance and significantly boosts volume sales and consumer trial rates. Concurrently, the rise of e-commerce and specialized direct-to-consumer (D2C) platforms is optimizing supply chains for niche and premium offerings, providing better inventory control and immediate consumer feedback. Analyzing these segments helps stakeholders allocate resources efficiently, focusing investment on high-growth areas such as refrigerated ready-to-eat alternatives and high-quality B2B ingredients derived from precision fermentation.

The value chain for the Meat Alternatives Market begins with the upstream segment involving raw material sourcing, primarily focusing on cultivating high-yield, sustainable protein crops such as soy, peas, and wheat. Upstream activities also include primary processing steps like dehulling, fractionation, and isolation to extract concentrated protein powder. Key considerations at this stage are maintaining genetic purity, ensuring non-GMO status, and developing proprietary breeding programs to enhance the functional properties (e.g., solubility, emulsion capacity) of the plant proteins. Strong partnerships with agricultural suppliers are crucial for securing consistent, high-quality inputs and managing price volatility, which directly impacts the final product’s profitability and price parity goal.

The midstream processing stage is highly technology-intensive, involving the conversion of protein isolates into textures mimicking meat structure. This includes extrusion (high moisture and low moisture), fermentation, and complex ingredient blending utilizing binders, fats (often coconut or sunflower oil), and flavor systems (natural extracts, yeast, and heme analogs). Manufacturing requires specialized equipment and expertise in food chemistry and engineering to achieve optimal texture, mouthfeel, and cooking performance. Distribution channels, both direct and indirect, then handle the movement of finished products. Indirect channels dominate volume sales through extensive networks of third-party logistics (3PL) providers managing complex chilled and frozen supply chains to hypermarkets, supermarkets, and convenience stores, ensuring product integrity and shelf-life compliance.

The downstream analysis focuses on market penetration and consumer interaction. Direct distribution is crucial for emerging, niche brands utilizing e-commerce to build brand loyalty and collect valuable customer data, often bypassing traditional retail margins. The foodservice segment (QSRs, casual dining) acts as a high-volume indirect channel, crucial for mainstream consumer trial and awareness building. Direct consumer feedback, digital marketing, and strategic co-branding initiatives are essential downstream activities. Overall efficiency across the value chain hinges on mitigating energy usage during processing (especially extrusion and freezing) and minimizing waste, aligning the production process with the core environmental promises of the alternative protein industry.

The primary target demographic for the Meat Alternatives Market has expanded significantly beyond the traditional vegetarian and vegan base to include a vast and growing population of flexitarians. Flexitarians, defined as individuals actively reducing their meat consumption without eliminating it entirely, constitute the largest and fastest-growing segment. These consumers are motivated by a blend of health consciousness—seeking lower saturated fat intake—and environmental ethics, but demand products that offer convenience, versatility, and uncompromising flavor and texture parity with meat. They seek options that fit seamlessly into regular family meals and social dining experiences, driving demand for products like plant-based ground beef and chicken substitutes suitable for popular recipes.

Secondary high-value potential customers include the institutional and corporate catering sectors, encompassing schools, hospitals, corporate cafeterias, and airlines. These end-users are increasingly mandated by corporate social responsibility (CSR) goals or public health initiatives to offer sustainable and healthy menu choices, leading to large volume B2B purchases of meat alternatives. Furthermore, Millennial and Gen Z populations are statistically more likely to embrace plant-based diets, positioning them as critical long-term growth drivers, particularly those residing in urban centers with greater exposure to diverse, novel food trends and higher discretionary income allocated to specialty foods. The industry also targets individuals with specific dietary needs, such as those sensitive to red meat or those seeking kosher or halal certified protein sources, where plant-based substitutes offer inherent advantages.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 8.5 Billion |

| Market Forecast in 2033 | USD 23.5 Billion |

| Growth Rate | 15.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Beyond Meat, Impossible Foods, Quorn Foods, Tofurky, MorningStar Farms, Amy's Kitchen, Maple Leaf Foods, Nestle (Garden Gourmet), Unilever (The Vegetarian Butcher), Vivera, Lightlife Foods, JBS (Planterra), Olam International (Ofi), Ingredion, Roquette, Cargill, ADM, Eat Just, Mosa Meat, 3F Bio. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Meat Alternatives Market is characterized by innovation across three main pillars: plant protein processing, microbial fermentation, and cellular agriculture. Traditional processing relies heavily on High-Moisture Extrusion (HME) and Low-Moisture Extrusion (LME) techniques. HME is crucial for replicating the fibrous, anisotropic texture of whole muscle meats by subjecting plant protein dough to high heat, pressure, and shear, resulting in complex laminated structures. Ongoing R&D in extrusion technology focuses on developing larger, more scalable machines and optimizing the thermal and mechanical profiles to handle new, less processed protein sources, thereby reducing the reliance on chemical texturizing agents and achieving cleaner label status. Advancements in protein isolation chemistry, such as improved methods for removing off-flavors inherent in sources like pea protein, are also critical foundational technologies.

A rapidly expanding technological frontier is fermentation, segmented into biomass fermentation and precision fermentation. Biomass fermentation uses fast-growing microorganisms (like fungi or microalgae, exemplified by Mycoprotein) to produce large quantities of protein biomass efficiently, offering naturally fibrous textures and high nutritional density with fewer processing steps. Precision fermentation, conversely, involves programming microorganisms to produce specific functional ingredients, such as animal-identical proteins like whey, caseins, or heme (the iron-containing molecule responsible for the 'meaty' flavor and color), without involving any animals. These ingredients are incorporated into plant-based matrices to dramatically enhance sensory attributes, effectively closing the taste gap and offering unprecedented control over flavor and nutritional output.

While still nascent and highly regulated, cellular agriculture, often referred to as cultured or cultivated meat, represents the pinnacle of long-term technological evolution in this space. This involves growing animal cells (muscle and fat cells) in bioreactors, bypassing the need to raise and slaughter livestock. Though currently facing significant cost and scale challenges, cultured meat technology promises a product that is biologically identical to conventional meat, potentially offering the final solution to sensory limitations. The convergence of these technologies—combining plant scaffolding, precision fermentation-derived flavor components, and potentially cultured fat cells—forms the core technological strategy for next-generation products aimed at achieving true parity in taste, nutrition, and price.

The primary drivers include escalating consumer demand for environmentally sustainable food choices, heightened awareness regarding personal health and the reduction of saturated fats, robust venture capital investment in food technology, and the increasing availability and quality parity of plant-based products in mainstream retail and foodservice channels.

Precision fermentation is highly significant as a critical enabler. It allows for the bio-engineering of specific functional ingredients, such as animal-identical proteins (like heme or whey) or complex fats, providing superior flavor, texture, and nutritional profiles that conventional plant proteins alone cannot achieve, thus closing the sensory gap for next-generation products.

The Asia Pacific (APAC) region is projected to exhibit the highest Compound Annual Growth Rate (CAGR). This acceleration is driven by rapid urbanization, substantial population size, a growing flexitarian consumer base, and the localization of plant-based products designed to appeal to traditional Asian cuisines.

Key challenges include achieving consistent price parity with conventional meat, overcoming consumer skepticism regarding highly processed ingredient lists ('clean label' demands), and continuously refining product texture and flavor profiles to perfectly mimic whole-cut meat structures, which remains a substantial technological hurdle.

Soy protein historically dominates the market due to its versatility and cost efficiency. However, pea protein is currently the fastest-growing source, favored by manufacturers and consumers for its non-allergen status (unlike soy or wheat) and its improved functional properties in extrusion processes, driving significant market momentum.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.