ID : MRU_ 433455 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

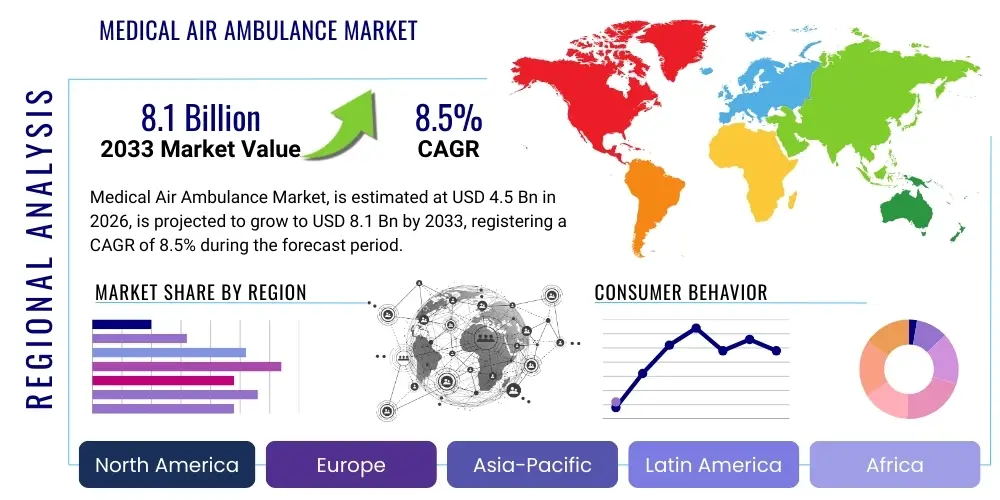

The Medical Air Ambulance Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD 4.5 Billion in 2026 and is projected to reach USD 8.1 Billion by the end of the forecast period in 2033.

The Medical Air Ambulance market encompasses specialized air transportation services designed for the urgent and rapid transfer of critically ill or injured patients between healthcare facilities or from accident sites to hospitals. This essential component of the emergency medical services (EMS) infrastructure utilizes highly customized aircraft, including helicopters (rotor-wing) and fixed-wing airplanes, equipped with intensive care unit (ICU) level medical equipment and staffed by specialized medical teams, such as flight nurses, paramedics, and physicians. The primary purpose is to significantly reduce transport time, which is crucial for improving patient outcomes, particularly in cases involving time-sensitive conditions like acute trauma, strokes, cardiac events, and the transportation of vital organs for transplantation. The rising incidence of chronic diseases, coupled with geographical disparities in access to advanced healthcare, particularly in remote and rural areas, solidifies the reliance on air ambulance services.

The core offerings of the medical air ambulance sector include both inter-facility transport (transfers between hospitals) and scene calls (retrieving patients directly from an incident location). Product specialization centers around the modification of aircraft cabins to meet stringent medical safety and operational standards, integrating life support systems such as ventilators, cardiac monitors, defibrillators, and complex medication delivery mechanisms. Major applications span comprehensive trauma care, specialized pediatric and neonatal transport, high-risk obstetrics transfers, and the critical logistical coordination required for international medical evacuations. These services offer unparalleled speed and the ability to bypass congested ground routes, making them indispensable for modern healthcare logistics.

Key driving factors accelerating market growth include advancements in avionics and satellite communication technologies, enabling safer operations in diverse weather conditions, and the increasing standardization of clinical protocols for flight crews. Furthermore, the expansion of global health tourism necessitates reliable international air medical services. Governments and private entities are increasingly investing in sophisticated air ambulance infrastructure to enhance disaster response capabilities and ensure comprehensive coverage across vast territories. The ability of air ambulances to bridge the gap between initial stabilization and definitive care remains the paramount benefit driving continuous demand and market expansion.

The Medical Air Ambulance Market is characterized by robust growth driven primarily by escalating global trauma rates and the persistent need for rapid patient transfer over long distances, positioning it as a critical sector within healthcare logistics. Business trends indicate a strong move toward consolidation among major providers, aiming for economies of scale and enhanced geographical coverage, complemented by significant investments in next-generation helicopter and fixed-wing fleets that offer greater range and operational efficiency. Furthermore, there is a distinct shift toward advanced specialized services, including ECMO transport and neonatal intensive care transport, demanding higher skill sets and specialized equipment, thereby driving up service complexity and pricing models. Partnerships between air ambulance operators and leading hospital systems are becoming central to service delivery optimization, ensuring seamless integration into the patient care continuum and facilitating faster deployment capabilities.

Regionally, North America maintains its dominance due to a highly developed EMS system, favorable reimbursement structures, and a high volume of complex trauma cases requiring immediate air transport. However, the Asia Pacific (APAC) region is emerging as the fastest-growing market, propelled by rapid urbanization, significant improvements in healthcare infrastructure investment, and increasing penetration of health insurance coverage in developing economies like China and India. European growth is steady, emphasizing cross-border medical transfers and standardization under EU-wide aviation and medical regulations, while the Middle East and Africa (MEA) see growth focused on oil and gas industry site emergencies and high-net-worth individual evacuations, driving demand for high-end fixed-wing capabilities.

Segment trends reveal that the Helicopter segment, particularly rotor-wing aircraft, holds the largest market share owing to its superior ability for point-to-scene retrieval and utility in urban environments, though the Fixed-Wing segment is experiencing accelerated growth driven by the rising demand for long-distance intercontinental patient transfers. By Application, Trauma and Cardiac emergencies represent the core revenue generators, given the time-critical nature of these conditions, while the Organ Transport segment demonstrates specialized, high-value growth tied directly to the expansion of global organ donation networks. End-User analysis confirms that Independent Service Providers, often operating under contract for hospitals or government agencies, are the primary revenue drivers, leveraging specialized operational knowledge and scale.

Common user questions regarding the impact of Artificial Intelligence (AI) on the Medical Air Ambulance Market center on how AI can enhance operational efficiency, improve patient outcomes through advanced triaging, and mitigate the high operational costs associated with air transport. Users are particularly interested in AI's role in optimizing flight path planning considering real-time weather, airspace restrictions, and ground traffic conditions, thereby minimizing mission duration and fuel consumption. Concerns frequently arise about the integration complexity of AI decision-support tools with existing avionics systems and the necessary regulatory clearances for AI-driven clinical protocols in flight. There is a high expectation that AI will automate administrative tasks, predict maintenance needs, and ultimately lead to a more responsive, reliable, and cost-effective air medical transport system.

The Medical Air Ambulance Market is primarily driven by the increasing global prevalence of trauma and cardiovascular emergencies, necessitating rapid specialized transport, combined with technological advancements in aircraft design and onboard medical equipment that enhance operational range and care capabilities. Significant growth is further propelled by rising consumer awareness regarding the golden hour principle in emergency care and the subsequent demand for high-speed transport, often supported by improving insurance penetration globally. However, the market faces stringent restraints, most notably the extremely high operating costs, including specialized crew salaries, fuel, and meticulous maintenance requirements, which often translate into high patient fees, limiting accessibility for some populations. Additionally, complex and varying aviation regulatory landscapes across different nations create operational hurdles for international providers.

Opportunities for expansion are substantial, particularly through the development of specialized niche services such as dedicated pediatric and neonatal transport teams and the integration of highly sophisticated life support systems like mobile ECMO units. Furthermore, expansion into emerging markets, where road infrastructure is often poor but economic development is increasing healthcare spending, presents lucrative long-term prospects. Strategic partnerships with governmental agencies for disaster relief and search-and-rescue (SAR) operations offer diversified revenue streams. The adoption of drone technology for transporting vital medical supplies or diagnostic samples to remote areas serves as a supplementary opportunity to enhance overall service efficiency.

The primary impact forces shaping the market involve intense pressure from insurance providers and governments to contain costs and standardize billing practices, balancing the need for rapid response with financial sustainability. Technological disruption, particularly the development of more fuel-efficient and quieter rotor-wing aircraft, influences fleet upgrade cycles. Socio-demographic changes, such as aging populations in developed countries and rising chronic disease burdens, constantly increase the baseline demand for critical care transport. The overall competitive intensity remains high, primarily focused on response time metrics, safety records, and the breadth of specialized medical accreditations held by the operators, driving continuous investment in quality assurance and specialized training protocols.

The Medical Air Ambulance Market is intricately segmented based on service type, aircraft platform, application specialization, and end-user base, reflecting the diverse operational and clinical requirements inherent in critical care transport. Analyzing these segments provides crucial insights into targeted investment areas and underlying demand drivers. Service type differentiation highlights the dichotomy between hospital-owned and independent providers, where independent operators often benefit from greater scalability and focus exclusively on logistics, while hospital-based units ensure seamless integration with specific facility standards. Aircraft type segmentation is pivotal, separating the capabilities of highly maneuverable helicopters, ideal for short-haul and scene operations, from the high-speed, long-range capabilities of fixed-wing aircraft crucial for international evacuations and intercontinental transfers. Understanding these segment dynamics is essential for market participants seeking to optimize fleet deployment and service offerings tailored to regional medical needs.

Application-based segmentation is perhaps the most medically significant, identifying high-demand clinical areas. Trauma and cardiac care consistently drive the largest share due to the irreversible damage caused by delays in these conditions, underpinning the necessity for rapid response times. Emerging segments, such as respiratory emergencies (especially relevant post-pandemic) and specialized organ transport, represent high-growth niches requiring specific, often bulky, support equipment and highly specialized clinical teams, driving capital expenditure in these areas. Finally, the End-User segmentation distinguishes between direct service consumption by hospitals and EMS agencies versus governmental contracts, which often involve large-scale agreements for public safety and military support, influencing the scale and stability of provider revenues. This detailed segmentation allows stakeholders to accurately gauge market penetration and tailor marketing strategies toward the most lucrative and demanding segments.

The value chain for the Medical Air Ambulance Market is complex and capital-intensive, starting with the upstream phase involving specialized aircraft manufacturing and modification, where key suppliers include major aerospace companies and highly specialized medical equipment providers who retrofit cabins to meet ICU standards. This phase is characterized by strict regulatory oversight, demanding compliance with aviation safety agencies (like FAA or EASA) and healthcare governing bodies. Procurement of high-quality, durable medical technology suitable for high-altitude operation and vibration resistance is crucial. The efficiency and cost structure established in the upstream phase significantly dictate the operational viability of the service providers, highlighting the importance of long-term maintenance contracts and reliable spare parts supply chains.

The midstream component is dominated by the air ambulance operators—the core service providers. These entities manage flight operations, employ highly specialized clinical and aviation personnel, coordinate logistics, secure necessary permits, and manage sophisticated dispatch centers, often integrating AI-driven systems for real-time mission optimization. Operational excellence in this stage relies heavily on maintaining rigorous safety standards, achieving rapid response times, and ensuring the continuous specialized training of clinical staff. This stage also encompasses critical relationships with airport and heliport managers, fuel suppliers, and ground transportation partners, ensuring a seamless patient transfer process from scene or facility to the final destination.

The downstream analysis focuses on the distribution channels and end-users. Services are distributed directly through contracts with hospitals (inter-facility transfers), direct emergency calls routed through EMS systems, and specialized agreements with insurance, travel assistance companies, and governmental bodies (military or public health contracts). Direct distribution through independent providers or hospital-owned services serves the immediate critical need. Indirect distribution involves brokering services through assistance companies that manage patient travel and payment logistics, especially for international evacuations. The ultimate buyers, or potential customers, are patients requiring critical care transfer, but the payment mechanism is typically handled by insurance payers, government healthcare schemes, or self-paying entities, influencing billing complexities and market access strategies.

The core potential customers and end-users of the Medical Air Ambulance Market span a variety of entities, reflecting the multifaceted nature of emergency and specialized critical care logistics. The primary and most frequent users are large regional hospitals and specialized medical centers, particularly those with trauma certifications or those acting as transplant centers, requiring rapid inter-facility transfers of critically unstable patients or time-sensitive organs. These hospitals rely on air ambulance services to expand their geographical reach, ensuring their specialized services are accessible across a wider region than ground transport allows. Furthermore, governmental bodies, including military organizations, federal emergency management agencies, and national health services, represent major customers through long-term contracts for search and rescue, disaster response, and transport of injured personnel.

Another significant customer segment includes private insurance providers and travel assistance companies. These entities contract air ambulance services on behalf of their policyholders, often involving complex medical repatriations from international locations or specialized coverage for high-risk employment sectors like oil, gas, and mining. These assistance companies focus on minimizing financial risk while ensuring policyholders receive high-quality, swift transport. Individual patients requiring immediate specialized medical attention, often facilitated by their insurance or paying out-of-pocket in critical, uninsured scenarios, also constitute a direct customer base. These diverse customer needs necessitate air ambulance providers to maintain a flexible fleet composition, capable of handling varying patient acuity levels, payload requirements, and operational distances.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 8.1 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Air Methods, Global Medical Response (GMR), PHI Air Medical, Apollo Hospitals, CHC Helicopter, IAS Medical, European Air Ambulance, lifeline Air Ambulance, Air Charter Service, Babcock International, REVA, Inc., FAI rent-a-jet, Gulf Helicopters, Summit Air Ambulance, Envision Healthcare, Air Ambulance Worldwide, Linetec, Metro Aviation, Bond Helicopters, Scandinavian Air Ambulance. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Medical Air Ambulance market is heavily reliant on technological sophistication across both the aviation and medical domains. Key advancements in rotor-wing technology, such as the increasing deployment of modern, twin-engine helicopters with enhanced payload capacity, reduced noise signature, and superior performance at altitude (e.g., Airbus H145, Leonardo AW169), are critical for improving safety and mission capability. Avionics technologies, including advanced Synthetic Vision Systems (SVS), Enhanced Vision Systems (EVS), and sophisticated weather radar, allow flight crews to operate more safely in degraded visual environments (DVE), significantly extending operational windows and reducing weather-related cancellations, a major restraint in the industry. Furthermore, the mandatory adoption of satellite-based tracking and communication systems ensures continuous operational oversight and seamless coordination with ground EMS and hospital teams.

On the medical front, the technology landscape is focused on miniaturization and ruggedization of critical care equipment. Portable, battery-operated life support devices—such as compact mechanical ventilators, high-fidelity cardiac monitors capable of transmitting data in real-time (telemedicine integration), and transport-capable defibrillators—are mandatory. Innovations in blood and plasma storage solutions designed to maintain optimal temperatures during flight, alongside specialized incubators for neonatal transport that mimic the stability of an NICU environment, are driving quality improvements. The capability to carry highly specialized therapeutic equipment, like miniaturized mobile Extracorporeal Membrane Oxygenation (ECMO) machines, represents the leading edge of medical air transport technology, enabling the transfer of the most critically ill patients over vast distances.

The convergence of Information Technology (IT) and operational logistics is another significant technological trend. Integrated Electronic Patient Care Records (EPCR) systems allow flight crews to access and update patient data instantly, linking seamlessly with the receiving hospital's electronic health records (EHR) system. This interoperability ensures a smooth handoff and minimizes the risk of information errors. Additionally, sophisticated Computer Aided Dispatch (CAD) systems utilize geospatial mapping and predictive analytics to optimize crew scheduling, aircraft positioning, and maintenance forecasting. These technologies collectively enhance operational efficiency, regulatory compliance, and the overall clinical quality of air ambulance services, transforming the market from purely transport-focused to a true extension of the hospital intensive care unit.

Market growth is predominantly driven by the increasing global incidence of time-sensitive medical conditions like severe trauma and cardiac events, coupled with expanding geriatric populations requiring rapid specialized care. Technological advancements in portable critical care equipment and increasing integration of air transport into comprehensive emergency medical systems also serve as key accelerators.

Rotor-wing (helicopters) are utilized for shorter distances, scene response, and urban environments due to their ability to land in confined spaces near accident sites or hospitals without runways. Fixed-wing aircraft are necessary for long-distance, high-speed transfers, including intercontinental medical repatriations, offering greater range and efficiency at high altitudes.

AI significantly enhances operational efficiency by optimizing dispatch logistics, predicting necessary aircraft maintenance, and dynamically selecting the safest and fastest flight paths based on real-time weather and airspace constraints. This leads to reduced response times, lowered operational costs, and improved overall mission safety records.

North America currently holds the largest market share, characterized by its highly developed Emergency Medical Services (EMS) infrastructure, extensive coverage by specialized trauma centers, and established reimbursement policies that support the high operational costs associated with air medical services.

The market is primarily constrained by extremely high operational costs, resulting in costly services that often necessitate robust insurance coverage, thereby limiting general public access. Additionally, strict and disparate aviation and medical regulations across different countries pose significant barriers to international operational standardization and scalability.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.