ID : MRU_ 434495 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

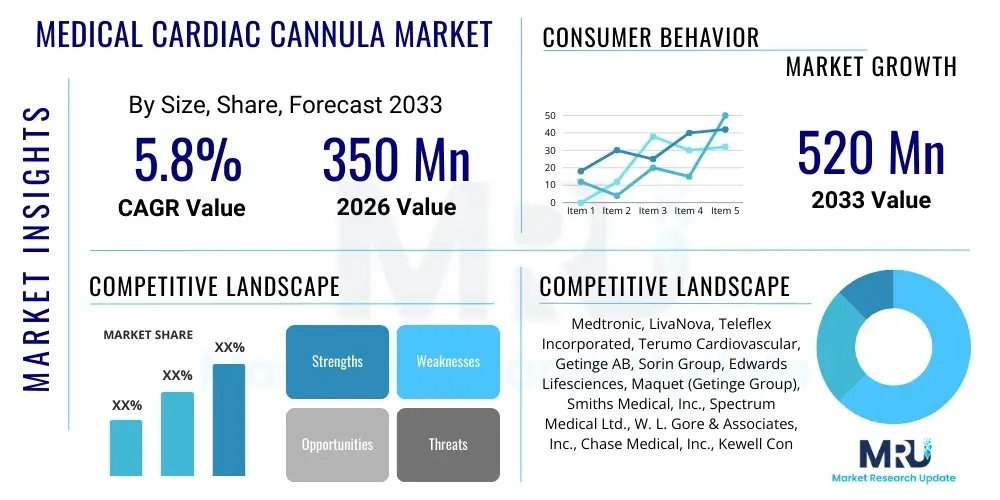

The Medical Cardiac Cannula Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 350 Million in 2026 and is projected to reach USD 520 Million by the end of the forecast period in 2033.

The Medical Cardiac Cannula Market encompasses the specialized medical devices used to establish vascular access and facilitate the circulation of blood or delivery of cardioplegia solutions during complex cardiac procedures, primarily open-heart surgery, and cardiopulmonary bypass (CPB). These essential components are critical in maintaining physiological stability when the heart is intentionally stopped or bypassed for surgical repair. The core product line includes arterial, venous, and cardioplegia cannulae, each designed with specific structural characteristics and material compositions, such as polyurethane and PVC, to optimize biocompatibility and flow dynamics, thereby minimizing trauma to the vascular tissue during insertion and operation.

Major applications of cardiac cannulae center around coronary artery bypass grafting (CABG), valve repair or replacement, and procedures involving the correction of congenital heart defects. The benefit derived from advanced cardiac cannulae includes improved surgical visualization, reduced incidence of hemolysis and air embolism, and enhanced safety profile during extended CPB runs. Key factors driving market expansion involve the globally rising prevalence of cardiovascular diseases (CVDs), increasing adoption of technologically advanced, minimally invasive cardiac surgical techniques, and the continuous development of novel cannula designs offering better maneuverability and reduced invasiveness.

The Medical Cardiac Cannula Market is characterized by steady, moderate growth, propelled significantly by the demographic shift toward an aging population and the corresponding increase in cardiac pathologies requiring surgical intervention. Business trends indicate a strong emphasis on product differentiation, particularly in developing smaller-profile, flexible cannulae suited for minimally invasive cardiac surgery (MICS), which lowers patient recovery time and hospital stays. Strategic acquisitions and collaborations among major medical device manufacturers and specialized cannula producers are consolidating market share and focusing innovation efforts on material science to improve hemocompatibility and reduce inflammatory responses associated with CPB.

Regionally, North America and Europe currently dominate the market due to established healthcare infrastructure, high procedural volumes, and rapid adoption of premium devices, alongside favorable reimbursement policies supporting complex cardiac interventions. However, the Asia Pacific (APAC) region is forecasted to exhibit the highest growth rate, driven by escalating healthcare expenditure, improving access to advanced surgical facilities, and a large, untapped patient pool suffering from preventable and treatable CVDs. Government initiatives in countries like China and India focused on enhancing cardiovascular care infrastructure are playing a pivotal role in this regional expansion.

Segment trends reveal that the venous cannulae segment holds the largest market share owing to their frequent use in standard CPB setups, while the minimally invasive procedure segment is experiencing the fastest growth, reflecting the broader surgical trend toward reduced invasiveness. Manufacturers are also focusing on material segments, prioritizing silicone and advanced polyurethane derivatives that offer superior kink resistance and flexibility. End-users, particularly large volume tertiary care hospitals, remain the primary consumers, but the demand from specialized cardiac centers and ambulatory surgical centers (ASCs) is rising due to the shifting paradigm of healthcare delivery.

Users frequently inquire about how Artificial Intelligence (AI) and machine learning (ML) integration could transform the precision and safety of CPB procedures involving cardiac cannulae. Common user questions revolve around AI’s role in optimizing flow dynamics, predicting potential complications during cannulation (such as vessel wall injury or malposition), and automating the monitoring of CPB parameters in real-time. There is significant interest in AI models that can analyze physiological data streams (blood gas, pressure, flow) to recommend dynamic adjustments to pump settings, ensuring optimal perfusion and minimizing shear stress on blood cells, which directly relates to the performance and design of the cannula used. Users expect AI to enhance procedural efficiency and personalize the CPB protocol based on individual patient characteristics, ultimately reducing morbidity and mortality associated with cardiac surgery requiring cannulation.

While cardiac cannulae are passive mechanical devices, AI significantly impacts their effective deployment and the surrounding ecosystem. AI algorithms are increasingly being applied in pre-operative planning, utilizing high-resolution imaging (CT/MRI) to create patient-specific vascular models. This advanced visualization helps surgeons precisely determine the optimal cannulation site, cannula size, and insertion trajectory, thus improving first-pass success rates and reducing procedural time. Furthermore, AI-driven predictive maintenance models are being developed for perfusion machines and associated tubing kits, including cannulae integrity checks, ensuring device reliability throughout the often lengthy duration of cardiopulmonary support.

The future convergence of cardiac cannulation and AI lies in the development of "smart cannulae." These hypothetical devices would integrate micro-sensors capable of transmitting real-time data regarding local flow velocity, pressure gradients, and even markers of tissue hypoxia near the insertion point back to an AI monitoring system. This feedback loop would allow the perfusionist or surgeon to make immediate, data-driven adjustments, fundamentally enhancing patient safety and potentially leading to customized cannulae designs optimized by machine learning algorithms for specific anatomical variations or disease states.

The Medical Cardiac Cannula Market is driven by the global surge in chronic cardiovascular diseases and the subsequent requirement for highly specialized surgical interventions, alongside technological advancements that promote less invasive surgical techniques. Restraints predominantly involve the inherent risks associated with cardiopulmonary bypass, strict regulatory hurdles surrounding Class II and Class III medical devices, and the significant cost of high-quality cannulae, especially in developing economies. Opportunities are abundant in emerging markets due to infrastructural growth and increasing access to complex cardiac care, coupled with the potential development of specialized cannulae for pediatric and neonatal applications, which represents a highly sensitive and underserved segment. These market dynamics—Drivers, Restraints, and Opportunities—collectively shape the Impact Forces, determining the overall pace and direction of market growth, prioritizing safety, efficiency, and material innovation.

The principal impact force is the undeniable demographic trend of aging populations worldwide, directly correlating with increased cardiovascular disease incidence, thereby providing a constant upward pressure on demand for cardiac surgical consumables. This force is counterbalanced by regulatory scrutiny, which acts as a restraint, forcing manufacturers to invest heavily in clinical trials and quality assurance, potentially slowing product launch cycles. Furthermore, the economic force of healthcare cost containment, particularly in saturated markets, pushes hospitals toward adopting reusable components or seeking out cost-effective single-use alternatives, challenging the profitability margins for premium cannula producers.

A significant ongoing force is the technological shift toward Minimally Invasive Cardiac Surgery (MICS). This requires cannulae that are smaller, more flexible, and easier to manipulate through restricted access points, fundamentally changing product design specifications. Companies that rapidly innovate in materials science to create anti-thrombogenic and highly flexible cannulae suitable for MICS procedures will capture the fastest-growing market segment. The ultimate impact force remains patient safety; the continuous demand for devices that reduce complications such as air embolism, shear stress, and tissue damage dictates the competitive strategy and product development roadmap across the industry.

The Medical Cardiac Cannula Market is comprehensively segmented based on product type, material, procedure, and end-user, providing a granular view of demand distribution and growth potential across various dimensions. Product segmentation, including arterial, venous, and cardioplegia cannulae, defines the primary functional categories, with venous cannulae commanding the largest share due to their necessity in almost all CPB procedures. The segmentation by material highlights the shift toward advanced polymers like polyurethane, which offers excellent flexibility and biocompatibility compared to traditional materials, while the procedure segment clearly indicates the exponential growth trajectory of minimally invasive techniques over traditional open-heart surgery.

The increasing complexity of cardiac interventions, particularly in structural heart disease management and complex congenital repairs, necessitates a diversified product portfolio. Arterial cannulae, crucial for returning oxygenated blood to the patient, are increasingly being optimized for peripheral cannulation sites (e.g., femoral or axillary), which aligns with MICS trends. Meanwhile, cardioplegia cannulae, designed for delivering the solution that temporarily arrests the heart, are seeing innovation aimed at better distribution and protection of the myocardium during ischemia.

End-user segmentation clearly identifies hospitals, particularly large tertiary and teaching hospitals with dedicated cardiothoracic units, as the dominant consumers due to high procedure volumes. However, specialized cardiac catheterization labs and ambulatory surgical centers (ASCs) are rapidly emerging segments. These centers are expanding their procedural scope to include less invasive hybrid procedures that still require specialized cannulation techniques, driving demand for single-use, high-precision products optimized for shorter, focused interventions.

The value chain for the Medical Cardiac Cannula Market begins with upstream activities focused on raw material procurement and highly specialized manufacturing. Upstream analysis involves sourcing high-grade, medical-quality polymers such as polyurethane and silicone, which must meet stringent biocompatibility and regulatory standards (e.g., ISO 10993). Key activities at this stage include precision extrusion, tip molding, and coating (such as heparin or hydrophilic coatings) to reduce thrombogenicity and insertion friction. Since material quality directly impacts patient safety and device performance, suppliers of raw materials and specialized components hold significant leverage, particularly those offering innovative, anti-thrombogenic polymer technologies.

Midstream activities encompass the core manufacturing, sterilization, and packaging processes. Cannulae production requires cleanroom environments and sophisticated quality control to ensure precise dimensions, consistent flow rates, and flawless assembly of wire reinforcement and connectors. Manufacturers invest heavily in automated assembly lines and validation studies to meet global quality standards (e.g., FDA, CE Mark). Efficient inventory management and large-scale manufacturing capabilities are critical for minimizing unit costs, as cannulae are predominantly single-use, disposable items in high-volume cardiac centers.

Downstream analysis focuses on distribution channels and end-user delivery. The channel structure relies heavily on indirect distribution through large medical device distributors and regional specialized distributors who manage inventory and logistics to hospitals. Direct sales forces are primarily utilized by major players for high-volume accounts and specialized product training for surgeons and perfusionists. The final interaction occurs at the point of use in the operating room or catheterization lab, where procurement departments prioritize vendors based on product reliability, clinical efficacy data, and competitive pricing, influenced heavily by Group Purchasing Organizations (GPOs) in mature markets like North America.

The primary end-users and buyers of medical cardiac cannulae are institutions performing complex cardiac interventions requiring temporary cardiopulmonary bypass (CPB) or extracorporeal membrane oxygenation (ECMO). These institutions include large, tertiary care hospitals and specialized teaching hospitals, which often house high-volume cardiothoracic surgery departments and pediatric cardiac centers. Due to the high criticality of the devices and the specialized nature of the procedures, purchasing decisions are typically influenced by a triumvirate of clinical effectiveness (validated by surgeons and perfusionists), cost-effectiveness (analyzed by hospital procurement), and standardization preferences across the institution's CPB protocols.

Secondary but rapidly growing customer segments include dedicated cardiac specialty centers and ambulatory surgical centers (ASCs) that are increasingly performing less complex, minimally invasive heart procedures, such as hybrid revascularization or certain valve repairs. These centers often prioritize ease of use, smaller-profile cannulae, and pre-packaged, comprehensive kits to streamline their operational efficiency. The purchasing cycle in these facilities tends to favor suppliers who can offer flexible ordering, reliable JIT (Just-In-Time) delivery, and competitive pricing for bulk, single-use items.

Furthermore, academic research institutions and centers specializing in advanced cardiovascular device development represent a niche but important customer base. They acquire specialized cannulae for preclinical testing, simulation models, and educational purposes related to perfusion technology and surgical training. Ultimately, the consistent requirement across all customer segments is for cannulae offering superior hemocompatibility, precise flow control, and maximum safety margins to minimize procedural complications and ensure optimal patient outcomes during critical life support procedures.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 350 Million |

| Market Forecast in 2033 | USD 520 Million |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Medtronic, LivaNova, Teleflex Incorporated, Terumo Cardiovascular, Getinge AB, Sorin Group, Edwards Lifesciences, Maquet (Getinge Group), Smiths Medical, Inc., Spectrum Medical Ltd., W. L. Gore & Associates, Inc., Chase Medical, Inc., Kewell Converters Ltd., Braile Biomédica, Biosensors International Group, Fresenius Medical Care AG & Co. KGaA, Nipro Corporation, Vygon SA, Cook Medical, Inc., Argon Medical Devices, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Medical Cardiac Cannula Market is primarily defined by material science innovation, design optimization for flow dynamics, and the integration of features supporting minimally invasive procedures. Current research and development efforts focus heavily on optimizing polymer coatings to minimize surface thrombogenicity and reduce the systemic inflammatory response syndrome (SIRS) often associated with prolonged cardiopulmonary bypass. Heparin-bonded surfaces and other bioactive coatings are standard, but the next generation of materials is focusing on proprietary surface chemistries that mimic the vascular endothelium, aiming for near-perfect hemocompatibility to reduce the need for high doses of systemic anticoagulants during CPB.

Design innovation centers around achieving high flow rates with smaller cannula profiles, a critical requirement for MICS. This involves advanced wire winding techniques for kink resistance, ensuring the cannula remains flexible yet structurally sound, even when navigated through tortuous or tight anatomical spaces. Multi-stage venous cannulae and complex tip geometries (e.g., dispersion tips, fluted designs) are key advancements, designed to improve venous drainage efficiency and minimize cavitation or vessel wall suction, thereby improving the safety and efficacy of the bypass circuit while requiring fewer access sites.

Furthermore, technology is adapting to the increasing use of specialized applications like Extracorporeal Membrane Oxygenation (ECMO). ECMO requires durable cannulae capable of supporting circulation and oxygenation for days or weeks, demanding different material robustness compared to short-term CPB cannulae. The introduction of integrated safety features, such as depth markers, integrated fixation wings, and clear guidance lumens for Seldinger techniques, reflects a commitment to improving insertion accuracy and reducing user error in critical care settings, showcasing a mature technological sector continually prioritizing patient outcomes and procedural predictability.

The global Medical Cardiac Cannula Market exhibits significant regional disparities in terms of maturity, growth trajectory, and technological adoption, reflecting varying healthcare spending, regulatory environments, and prevalence of cardiovascular diseases.

The Medical Cardiac Cannula Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033, driven by increasing cardiovascular disease prevalence and technological shifts toward minimally invasive procedures.

Based on product type, the Venous Cannulae segment currently holds the largest market share due to its necessity in virtually all cardiopulmonary bypass (CPB) procedures required for open-heart surgery, facilitating efficient drainage of deoxygenated blood.

The MICS trend necessitates the development of smaller-profile, highly flexible, and kink-resistant cannulae optimized for peripheral insertion sites (e.g., femoral, axillary). Manufacturers are focusing on thinner walls and advanced polymers to maintain high flow rates despite reduced outer diameters.

The Asia Pacific (APAC) region is projected to register the highest growth rate, primarily attributed to increasing healthcare investments, expanding medical infrastructure, and a large, aging population needing specialized cardiovascular surgical interventions.

Market growth is primarily restrained by the high cost associated with advanced, specialized cannulae, stringent and lengthy regulatory approval processes for Class II and III medical devices, and inherent risks and complications associated with prolonged cardiopulmonary bypass procedures.

Material science is crucial, focusing on developing advanced polymeric materials like specialized polyurethane and silicone. Key innovations include anti-thrombogenic surface coatings (e.g., heparin bonding) to improve hemocompatibility and reduce inflammatory responses during circulation.

The primary end-users are large tertiary and teaching hospitals with established cardiothoracic surgery departments. Demand is also rapidly growing from specialized cardiac centers and ambulatory surgical centers (ASCs) performing less invasive procedures.

AI influences the use of cannulae by optimizing pre-operative planning for precise insertion sites, providing real-time predictive monitoring of flow dynamics during bypass, and potentially leading to the development of 'smart cannulae' with integrated micro-sensors for enhanced safety feedback.

Arterial cannulae are used to return oxygenated blood from the bypass circuit back into the patient's arterial system, while venous cannulae are used to drain deoxygenated blood from the patient's venous system into the bypass circuit for oxygenation.

Cardioplegia is a solution used to temporarily stop the heart during surgery to protect the myocardium. Cardioplegia cannulae are specialized delivery devices used to infuse this solution directly into the coronary arteries or coronary sinus, ensuring myocardial arrest and protection.

GPOs significantly influence purchasing decisions in mature markets like North America by negotiating large volume contracts with manufacturers. This pressures manufacturers to offer competitive pricing, often standardizing product choices across numerous hospital systems based on cost and reliability.

Yes, pediatric and neonatal cannulae represent a highly specialized segment. These devices require extremely small profiles, unique geometries, and materials with zero tolerance for clotting or flow obstruction, presenting unique manufacturing challenges and high potential for specialized growth.

Manufacturers primarily aim to mitigate risks associated with hemolysis (blood cell damage), air embolism, tissue trauma during insertion, and the systemic inflammatory response syndrome (SIRS) caused by blood contact with foreign materials during cardiopulmonary bypass.

Throughout the value chain, quality control is maintained by sourcing only biocompatible, medical-grade raw materials (upstream) and utilizing strictly controlled cleanroom manufacturing processes, mandatory sterilization protocols, and comprehensive validation testing (midstream) to meet international standards like FDA and CE Mark requirements.

Procedures most reliant on cardiac cannulae include Coronary Artery Bypass Grafting (CABG), heart valve repair and replacement (aortic and mitral), congenital heart defect correction, and increasingly, specialized procedures supported by ECMO.

Depth markers are critical integrated safety features that provide surgeons and perfusionists with immediate visual confirmation of the precise distance the cannula has been inserted into the vessel, helping prevent deep insertion that could cause vascular trauma or malpositioning that compromises flow.

Kink resistance is typically ensured by incorporating internal wire reinforcement, often using fine stainless steel or nitinol wires embedded within the polymer walls. This allows the cannula to remain highly flexible while resisting collapse when bent or angled within the surgical field.

Demand in APAC is characterized by rapid volume growth and higher price sensitivity for standard products, whereas North America focuses on technological sophistication, premium pricing for specialized MICS devices, and stringent clinical data requirements for new product adoption.

The Medical Cardiac Cannula Market is projected to reach an estimated market value of USD 520 Million by the end of the forecast period in 2033, reflecting consistent demand acceleration driven by global cardiac disease rates.

The primary objective is to minimize blood clotting upon contact with the foreign material surface of the cannula, thereby preventing clot formation that could lead to air embolism or device failure, and reducing the patient's systemic inflammatory response to CPB.

Yes, regulatory hurdles, particularly securing approvals from bodies like the FDA and obtaining CE Mark certification under the stricter European Medical Device Regulation (MDR), act as a significant barrier due to the mandatory requirement for extensive clinical safety data and rigorous quality management systems for these life-sustaining devices.

Specialized distributors play a crucial role in the indirect distribution channel, managing complex inventory logistics, ensuring timely delivery of sterile, single-use products to hospitals, and often providing localized technical support and product education to clinical staff.

Advanced polyurethane offers superior benefits over older materials like PVC due to its excellent combination of biocompatibility, high tensile strength, and flexibility, allowing manufacturers to create thin-walled cannulae that resist kinking while maximizing internal lumen diameter for optimal flow.

The market employs a hybrid model; major established players utilize direct sales forces for high-volume teaching hospitals and complex product portfolios, while relying on indirect distribution (specialized distributors) to efficiently cover vast geographical territories and smaller procedural centers.

Upstream analysis focuses on the procurement and initial processing of specialized raw materials, including medical-grade polymers and wire reinforcements, ensuring these inputs meet stringent biocompatibility standards before they enter the core manufacturing and assembly processes.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.