ID : MRU_ 433196 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

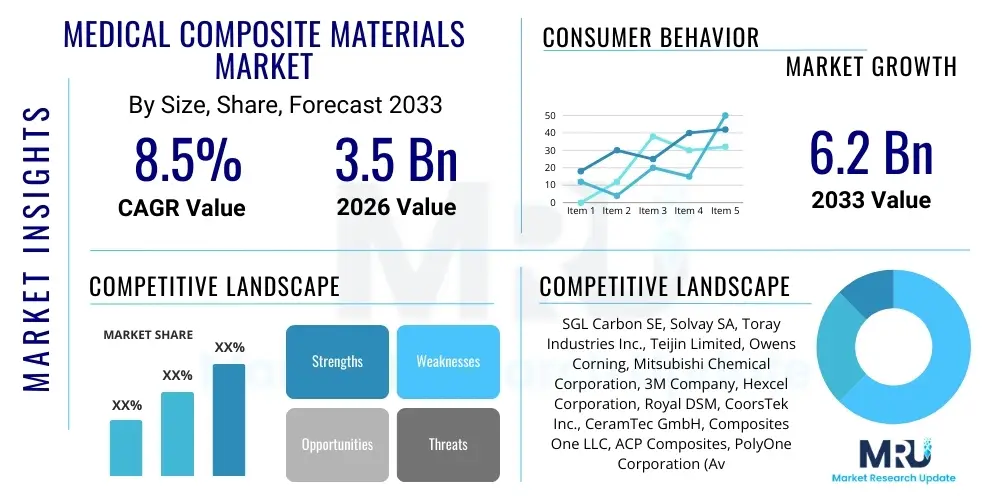

The Medical Composite Materials Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD 3.5 Billion in 2026 and is projected to reach USD 6.2 Billion by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by the increasing global prevalence of orthopedic and dental disorders, coupled with technological advancements in material science enabling the creation of biocompatible and high-performance composites suitable for complex medical applications.

The Medical Composite Materials Market encompasses advanced engineered materials characterized by superior strength-to-weight ratios, excellent biocompatibility, and customized mechanical properties, making them indispensable in modern healthcare. These materials are typically formed by combining two or more distinct components—a reinforcing agent (such as fibers or particles) and a matrix material (polymer, ceramic, or metal)—to achieve performance characteristics unattainable by monolithic materials alone. Key products include polymer matrix composites (PMCs), ceramic matrix composites (CMCs), and carbon-based composites, with specific attention given to fiber-reinforced polymers utilizing glass, carbon, or aramid fibers due to their application in load-bearing medical devices and implants.

Major applications of medical composites span across several critical medical disciplines, including orthopedics for bone plates and joint replacements, dentistry for fillings and prosthetics, and cardiovascular surgery for devices like heart valve components and specialized surgical instruments. The inherent benefits of these materials, such as radiolucency (allowing clear imaging without interference), corrosion resistance, and tunable elasticity mimicking natural tissue, position them as preferred substitutes for traditional metal alloys in critical implantology. The escalating demand for minimally invasive surgical procedures, which often require smaller, lighter, and more durable instruments, further solidifies the market position of these advanced composite solutions.

Driving factors for sustained market growth include the rapidly aging global population, which correlates directly with an increased incidence of age-related joint degradation and the subsequent need for orthopedic procedures. Furthermore, continuous innovation in 3D printing technologies and nanotechnology integration is enabling the fabrication of highly customized, patient-specific composite implants with improved osseointegration capabilities. Regulatory body support for advanced medical device adoption and the shift towards cost-effective, long-lasting treatment solutions also contribute significantly to the positive market trajectory observed across major geographical regions.

The Medical Composite Materials Market is currently characterized by robust business trends focusing heavily on material innovation, specifically the development of biodegradable and bioactive composites designed to minimize rejection rates and promote natural tissue healing. Companies are strategically investing in advanced manufacturing techniques, such as additive manufacturing (3D printing), which allows for the rapid prototyping and production of complex, porous composite structures tailored for bone scaffolding and drug delivery systems. The convergence of material science with personalized medicine represents a key area of competitive differentiation, leading to strategic partnerships between material suppliers and specialized medical device manufacturers aiming to control the entire value chain from raw material synthesis to final product commercialization.

Regionally, North America maintains the largest market share, driven by sophisticated healthcare infrastructure, high healthcare expenditure, and the early adoption of advanced medical technologies and complex surgical procedures. However, the Asia Pacific (APAC) region is projected to exhibit the highest growth rate (CAGR) due to expanding access to modern healthcare, rising medical tourism, and increasing government investment in domestic medical device manufacturing capabilities, particularly in countries like China, India, and South Korea. Europe remains a strong market, propelled by stringent regulatory frameworks ensuring high product quality and the presence of leading academic research institutions collaborating on next-generation composite formulations, especially within the dental and spinal treatment sectors.

Segment trends highlight the dominance of the application segment encompassing Implants, specifically orthopedic and dental implants, owing to the high mechanical demands and long-term necessity of these devices. By material type, Polymer Matrix Composites (PMCs), particularly PEEK-based composites, are leading due to their excellent wear resistance and chemical inertness. Further segmentation analysis reveals a significant uptake in the use of carbon fiber reinforced composites (CFRC) in surgical instruments and external fixation devices, capitalizing on the material's superior strength and radiolucency, which is crucial for monitoring healing progress without artifact interference during diagnostic imaging.

User queries regarding the intersection of Artificial Intelligence (AI) and the Medical Composite Materials Market predominantly center on how AI can accelerate materials discovery, optimize manufacturing processes, and enable truly personalized medicine through advanced composite design. Common questions address the speed at which AI models can screen potential composite formulations for biocompatibility and mechanical suitability, the role of machine learning in predicting the long-term performance and degradation of implanted materials, and the use of generative design algorithms to create complex lattice structures for orthopedic scaffolding. Concerns often revolve around data privacy when utilizing patient-specific biomechanical data for personalized composite creation and the validation requirements for AI-designed medical materials by regulatory bodies.

The integration of AI systems, particularly machine learning (ML) models, is fundamentally transforming the R&D landscape for medical composites. By analyzing vast datasets comprising material properties, clinical trial outcomes, and manufacturing parameters, AI drastically reduces the time and cost associated with synthesizing and testing novel composite formulations. This accelerates the identification of optimal reinforcement ratios and matrix combinations that meet specific biomechanical requirements for applications such as load-bearing joint replacements or customizable dental aligners. Furthermore, AI-driven process control enhances the consistency and quality of manufacturing, minimizing defects in complex structures created via methods like automated fiber placement or 3D printing.

In the context of personalized medicine, AI allows manufacturers to utilize patient MRI or CT scan data to generate optimized composite implant designs automatically. Generative design algorithms can tailor the mechanical stiffness and porous architecture of a composite scaffold to match the patient's existing bone density and desired loading conditions, potentially leading to faster healing and fewer revision surgeries. This capability, driven by sophisticated computational material science models integrated with AI, moves the industry closer to mass customization, ensuring that medical devices made from composites are not only high-performing but also perfectly matched to individual anatomical and physiological needs, thereby maximizing clinical efficacy and long-term success rates.

The Medical Composite Materials Market is significantly influenced by a dynamic interplay of Drivers, Restraints, and Opportunities (DRO), collectively forming crucial Impact Forces determining market direction and speed. The primary drivers include the global demographic shift towards an older population segment, substantially increasing the demand for complex orthopedic and dental restorative procedures where composites offer superior longevity and performance compared to traditional materials. Parallel to this, the rising patient preference for minimally invasive surgical techniques, necessitating smaller, highly precise, and radiolucent instruments, strongly favors composite solutions. The key restraint impacting market growth is the high initial cost associated with advanced material synthesis, processing, and the stringent regulatory approval pathways required for novel implantable medical devices, which can significantly protract commercialization timelines. This is compounded by existing manufacturing scale-up challenges for highly specialized, personalized composite structures.

Opportunities for growth are prominently situated within the development and commercialization of bioresorbable and smart composites that degrade harmlessly in the body after fulfilling their temporary structural role, eliminating the need for removal surgery. Furthermore, leveraging nanotechnology to incorporate therapeutic agents or sensing capabilities directly into the composite matrix (smart composites) opens new avenues in drug delivery and remote patient monitoring, offering value beyond just structural support. The integration of composite materials into advanced wound care management systems and surgical robotics represents further potential expansion domains. These opportunities encourage increased R&D investment and strategic collaboration between academic institutions and industry players aiming to capture future value.

The collective impact forces are currently pushing the market towards greater specialization and higher value-added products. The demand-side pull from geriatric care and advanced surgery is highly dominant, forcing manufacturers to overcome the cost barriers associated with production. Success in this market increasingly hinges on demonstrating clear clinical advantages, such as reduced patient recovery time and improved implant longevity, which justifies the premium pricing associated with cutting-edge composite solutions. Regulatory clarity and harmonization across major economic blocs could significantly accelerate market penetration for these innovative materials, turning localized opportunities into global standards of care, thus sustaining the strong projected CAGR throughout the forecast period.

The Medical Composite Materials Market is intricately segmented based on material type, fiber type, application, and geographical region, reflecting the diverse requirements and technological readiness across various medical disciplines. This segmentation provides a granular view of market dynamics, revealing specific areas of high growth and technological emphasis. The increasing sophistication in material science allows for tailored composite selection depending on whether the application requires high strength (like in orthopedic implants), excellent aesthetic properties (like in dentistry), or bioresorbability (like in tissue engineering scaffolds). Understanding these segments is crucial for stakeholders to align their R&D and market strategies effectively.

The material type segmentation highlights the maturity and widespread use of polymer matrix composites (PMCs), primarily thermoplastic and thermoset resins, due to their excellent processability and biocompatibility. Ceramic Matrix Composites (CMCs) and Carbon Composites also hold significant shares, particularly in applications requiring superior stiffness and radiolucency. The application segment drives the largest demand, with Orthopedics dominating, followed closely by Dentistry and Diagnostic Imaging components. The high capital investment and long life cycle required for orthopedic implants necessitate the use of premium, durable composite materials, reinforcing this segment's leading position and continuous innovation trajectory.

Future growth is expected to be pronounced in segments related to tissue engineering and customized prosthetic solutions, driven by breakthroughs in additive manufacturing technologies which facilitate the creation of complex composite geometries. Furthermore, the use of natural and biodegradable fibers, although currently niche, presents a critical opportunity aligned with sustainable healthcare practices. The strategic segmentation analysis confirms that market resilience is maintained through continuous innovation in both material synthesis and application engineering, ensuring that composites remain at the forefront of medical device advancement.

The value chain for the Medical Composite Materials Market is characterized by highly specialized stages, beginning with complex raw material sourcing and culminating in sophisticated clinical applications. The upstream segment involves the production of high-performance fibers (e.g., carbon fiber, high-purity glass fiber) and specialty polymer resins (e.g., PEEK, medical-grade epoxies). This stage requires rigorous quality control and material certification to meet stringent medical standards. Suppliers in this phase, often chemical or advanced materials companies, must ensure batch consistency and traceability, as the slightest variation can impact the final device's performance and biocompatibility. Pricing power is relatively high at this stage due to the technical barriers to entry and proprietary synthesis methods for medical-grade inputs.

The midstream phase involves the compounding and processing of these raw materials into semi-finished composite forms, such as prepregs, sheets, or specialized rods, followed by the actual manufacturing of the medical device components. This includes molding, pultrusion, filament winding, and increasingly, additive manufacturing (3D printing). Device manufacturers are the key players here, integrating material science expertise with engineering precision to fabricate components like bone plates, dental abutments, or MRI table tops. Direct involvement in R&D and robust quality management systems are crucial for maintaining regulatory compliance and product integrity before clinical deployment. Customization capabilities are essential for device manufacturers serving personalized medicine niches.

The downstream distribution channel involves specialized networks due to the high-value, critical nature of the products. Distribution often utilizes both direct and indirect channels. Direct sales channels are typically employed for high-volume, standard products sold directly to large hospital systems and specialized orthopedic clinics, ensuring close communication regarding inventory and technical support. Indirect channels involve authorized distributors and wholesalers who possess regional expertise and handle logistics for smaller clinics and international markets. End-users, including orthopedic surgeons, dentists, and radiologists, ultimately drive demand, making professional training and clinical support critical elements of the downstream value proposition to ensure safe and effective utilization of the advanced composite materials.

The primary end-users and buyers of medical composite materials span the entire spectrum of the healthcare ecosystem, from large multinational medical device original equipment manufacturers (OEMs) to specialized surgical clinics and research institutions. OEMs focusing on orthopedics and traumatology, such as companies producing hip and knee replacement components, internal fixation devices, and spinal fusion cages, represent the largest customer base. These entities require large volumes of highly consistent, high-strength composites like carbon fiber reinforced PEEK to integrate into their device platforms, driven by the necessity for radiolucency and mechanical properties that mimic bone.

Dental laboratories and dental product manufacturers constitute another significant customer segment, purchasing composites for restorative materials, orthodontic devices, and high-performance prosthetics. The demand in the dental sector is often driven by aesthetic requirements and the need for materials that are resistant to oral environments. Furthermore, hospitals and specialized surgical centers that directly procure customized patient-specific implants or require advanced imaging equipment components (like non-metallic surgical guides or MRI bore linings) are essential direct consumers, particularly as point-of-care manufacturing via 3D printing becomes more prevalent.

Finally, emerging customer segments include tissue engineering and regenerative medicine companies that utilize bioresorbable composites as temporary scaffolds for cell growth and regeneration. Academic research centers and government health organizations also function as key buyers, primarily for R&D purposes and for implementing new standards of care involving advanced material testing and clinical trials. These potential customers prioritize material traceability, certifications, long-term clinical data, and scalability of material supply, making robust material science support essential for supplier success.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 3.5 Billion |

| Market Forecast in 2033 | USD 6.2 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | SGL Carbon SE, Solvay SA, Toray Industries Inc., Teijin Limited, Owens Corning, Mitsubishi Chemical Corporation, 3M Company, Hexcel Corporation, Royal DSM, CoorsTek Inc., CeramTec GmbH, Composites One LLC, ACP Composites, PolyOne Corporation (Avient), Sekisui Chemical Co., Ltd., IsoTruss Inc., Pultrusion Composites Inc., Vistamax Composites, Tencate Advanced Composites, Barrday Corporation. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Medical Composite Materials Market is rapidly evolving, driven primarily by innovations in material science and advanced manufacturing processes aimed at enhancing biocompatibility, mechanical performance, and customization capabilities. A central technology is the advancement of high-performance polymer matrices, particularly the increasing utilization of Polyether ether ketone (PEEK) and its reinforced variants (e.g., carbon fiber reinforced PEEK). PEEK composites are highly valued for their elastic modulus closer to cortical bone, which reduces stress shielding effects common with metallic implants. Ongoing research focuses on incorporating surface modifications and bioactive coatings onto PEEK to promote rapid osseointegration and reduce the risk of implant failure, thereby significantly improving patient outcomes.

Additive manufacturing, specifically 3D printing technologies such as selective laser sintering (SLS) and fused deposition modeling (FDM) customized for medical-grade polymers and fibers, represents a pivotal technological advancement. 3D printing enables the production of patient-specific implants with complex internal geometries, such as porous lattice structures, which are essential for tissue ingrowth and vascularization in scaffolding applications. This technology drastically shortens the design-to-production cycle for customized orthopedic and craniofacial implants, making personalized medical devices scalable. Furthermore, continuous fiber additive manufacturing is emerging, offering the ability to print continuous carbon or glass fibers within a polymer matrix, maximizing the strength and load-bearing capacity of the printed composite parts, a critical requirement for high-stress applications.

Another significant area of technological focus is the development of bioresorbable composites, primarily based on polylactic acid (PLA), polyglycolic acid (PGA), or their co-polymers, often reinforced with ceramic nanoparticles or calcium phosphate fibers. These materials are engineered to maintain mechanical integrity long enough for the native tissue to heal, gradually degrading into non-toxic, naturally occurring metabolic byproducts. The incorporation of nanotechnology, using materials like carbon nanotubes or graphene derivatives, is being explored to enhance the structural performance, electrical conductivity, and potentially the antibacterial properties of medical composites. These continuous advancements in synthesis, processing, and functionality underscore the dynamic technical environment driving sustained market expansion and enabling increasingly complex medical interventions.

North America currently dominates the Medical Composite Materials Market, a position solidified by its well-established, sophisticated healthcare system and high expenditure on advanced medical devices. The region, particularly the United States, is a hub for leading medical device manufacturers and holds a commanding market share due to the early and aggressive adoption of technologies such as customized PEEK implants and advanced dental restoratives. High awareness among healthcare professionals regarding the benefits of composites—like radiolucency and reduced infection risk—further boosts demand. Moreover, robust regulatory frameworks, while stringent, provide a clear path for innovation, encouraging significant R&D investment into next-generation biomaterials and complex composite structures.

Europe represents the second-largest market, characterized by advanced research capabilities and a strong focus on quality and long-term device performance, particularly in countries like Germany, France, and the UK. The demand here is driven by an aging population and high standards of orthopedic and dental care. The European Medical Device Regulation (MDR) ensures that materials entering the market are subject to thorough clinical evaluation, favoring proven composite solutions in high-risk applications like spinal implants. Furthermore, collaborative research efforts between industry and academia in fields such as biodegradable composites and ceramic matrices contribute significantly to the continuous technological progress within the region.

Asia Pacific (APAC) is projected to be the fastest-growing region during the forecast period. This rapid growth is attributable to improving healthcare infrastructure, rising disposable incomes, and increasing awareness of advanced treatment options across developing economies like China and India. Government initiatives promoting domestic manufacturing and reducing reliance on imports are fueling local production of composite components. While market maturity is lower than in the West, the large patient pool, coupled with the rising prevalence of lifestyle diseases requiring orthopedic and cardiovascular interventions, ensures a rapidly expanding consumer base for medical composite materials, particularly those offering cost-effective performance advantages.

Medical composites, particularly carbon fiber reinforced materials, offer superior advantages over metals, primarily due to their reduced density, excellent fatigue resistance, and radiolucency, meaning they do not interfere with X-ray or MRI imaging. Crucially, their tunable elastic modulus can be matched closely to human bone, minimizing the stress shielding effect which can cause bone atrophy and implant loosening, leading to better long-term clinical outcomes for patients.

3D printing (additive manufacturing) is revolutionizing the production of medical composites by enabling the creation of patient-specific, geometrically complex implants and scaffolds quickly and accurately. This technology allows for precise control over internal porosity and external shape, crucial for maximizing tissue integration and reducing surgical time, making personalized orthopedic and dental devices highly scalable and cost-effective.

Polymer Matrix Composites (PMCs), particularly high-performance thermoplastics like PEEK and its variants, currently dominate the market share. PMCs are favored across applications, especially orthopedics and traumatology, due to their inherent biocompatibility, chemical inertness, and exceptional strength-to-weight ratio, which are critical requirements for long-term implant success and medical device durability.

Bioresorbable composites are advanced materials designed to safely degrade and be absorbed by the body after serving their temporary function, such as supporting a healing fracture. Materials based on PLA and PGA, often ceramic-reinforced, are strategically important because they eliminate the need for a second surgery to remove temporary fixation devices, reducing patient recovery time, hospital costs, and associated surgical risks.

New composite materials face significant regulatory hurdles due to the critical nature of their application, primarily focusing on long-term biocompatibility, extractables and leachables (E&L) testing, sterilization tolerance, and ensuring batch-to-batch consistency. Regulatory bodies, such as the FDA and European MDR agencies, require extensive clinical data and rigorous validation of both the material properties and the manufacturing process before granting market authorization.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.