ID : MRU_ 434269 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

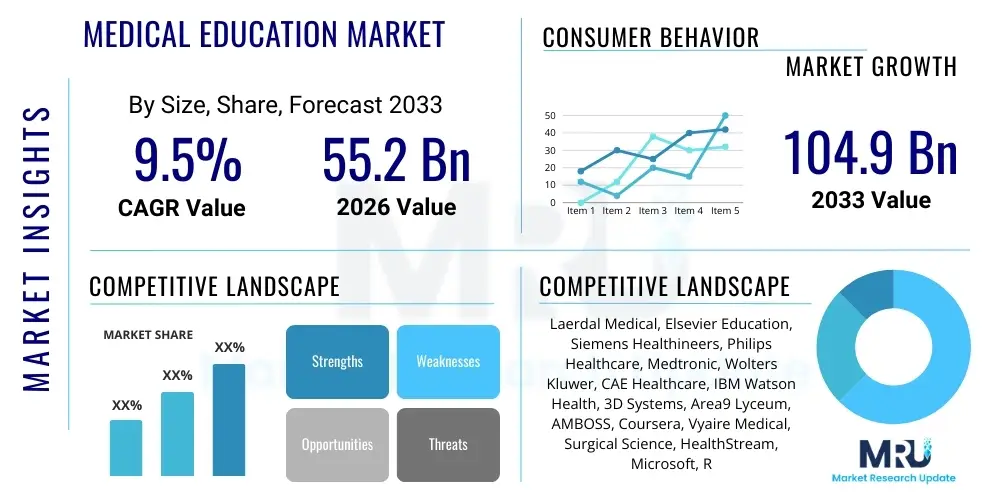

The Medical Education Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2026 and 2033. The market is estimated at USD 55.2 Billion in 2026 and is projected to reach USD 104.9 Billion by the end of the forecast period in 2033.

The Medical Education Market encompasses a vast ecosystem dedicated to training future healthcare professionals and ensuring the continuous competence of existing practitioners. This domain includes undergraduate medical training (MD, MBBS), graduate medical education (residency and fellowship programs), and continuing medical education (CME)/continuing professional development (CPD). The core product offerings within this market range from conventional lecture-based instruction and clinical rotations to advanced digital learning tools, simulation-based training platforms, immersive technologies suchologies (such as Virtual Reality and Augmented Reality), and specialized testing and assessment services. The paradigm shift toward competency-based medical education (CBME) and personalized learning pathways is fundamentally reshaping how medical knowledge is acquired and evaluated globally, requiring substantial investment in technology and innovative curriculum design to meet stringent accreditation standards and evolving patient care demands.

Major applications of modern medical education technologies extend beyond traditional academic institutions, finding significant traction in hospital networks, specialized training centers, pharmaceutical and medical device companies, and governmental health agencies responsible for public health workforce development. Key benefits derived from advancements in medical education include enhanced clinical decision-making capabilities, improved patient safety outcomes through high-fidelity simulation practice, faster dissemination of research findings and clinical guidelines, and increased efficiency in healthcare workforce training across diverse geographic settings. Furthermore, effective medical education systems are crucial for addressing global health disparities by rapidly scaling quality training programs in underserved regions, promoting interprofessional collaboration, and fostering ethical professionalism among trainees.

Driving factors propelling market expansion are numerous and deeply rooted in global demographic and technological changes. The primary driver is the pervasive worldwide shortage of healthcare professionals, necessitating the rapid and efficient scale-up of educational capacity, often through hybrid and distance learning models. Secondly, the accelerating pace of medical innovation, encompassing new diagnostics, therapeutics, and surgical techniques, mandates continuous professional learning to maintain clinical relevance. Regulatory pressures from accreditation bodies, which increasingly emphasize objective performance assessment and structured residency training, further compel institutions to adopt advanced tools for data collection and pedagogical analysis. Finally, the inherent advantages of digital transformation—such as accessibility, flexibility, and cost-effectiveness offered by e-learning platforms—are accelerating the adoption curve across all tiers of medical training, ensuring sustained market momentum throughout the forecast period.

The Medical Education Market is experiencing robust growth driven by the confluence of technological integration and critical global workforce demands. Business trends highlight a significant pivot towards digital learning solutions, specifically massive open online courses (MOOCs), microlearning modules, and sophisticated simulation platforms that offer practical, risk-free practice environments. Strategic partnerships between technology providers, medical schools, and large hospital systems are becoming central to developing and deploying comprehensive, accredited learning management systems (LMS) tailored for specialized medical domains. Key investment is focused on tools that facilitate personalized learning pathways, leveraging AI to track trainee performance and identify knowledge gaps, thereby enhancing the efficacy and efficiency of costly postgraduate training programs while simultaneously addressing the urgent need for continuous upskilling across the practicing professional base.

Regional trends indicate North America and Europe retaining dominant market shares due to high healthcare expenditure, established accreditation bodies, and early adoption of advanced simulation technology. However, the Asia Pacific (APAC) region is projected to exhibit the fastest Compound Annual Growth Rate (CAGR), fueled by rapidly expanding middle-class populations, increasing public and private investment in healthcare infrastructure, and government initiatives aimed at modernizing domestic medical training standards to meet escalating patient volumes. In developing economies within APAC and the Middle East & Africa (MEA), distance learning and mobile-based educational content are crucial for overcoming geographic limitations and scaling basic and specialty training efficiently. The adoption rates of AR/VR tools are rising globally, moving from experimental tools to core components of anatomy and procedural training curricula.

Segment trends confirm that the Continuing Medical Education (CME) segment holds a dominant position by revenue, reflecting the mandatory professional requirement for physicians to regularly update their knowledge base and maintain licensure across various jurisdictions. Methodologically, the market favors simulation and e-learning platforms over purely traditional didactic methods, given the proven ability of hands-on and interactive training to improve clinical outcomes and procedural competence. Device and consumables manufacturers play a crucial supporting role, particularly in high-fidelity simulation centers, driving revenue through the regular replacement and updating of training models and specialized equipment necessary for realistic practice scenarios. The shift toward evidence-based instructional design methodologies is forcing content providers to collaborate closely with clinical experts to ensure the relevance and accredited status of educational materials.

User inquiries regarding the impact of Artificial Intelligence (AI) on Medical Education primarily revolve around its capacity to personalize learning, automate assessment processes, and enhance clinical reasoning skills development. Common concerns center on whether AI will diminish the need for human faculty interaction, the accuracy and bias inherent in AI-driven diagnostic tutors, and the ethical implications of using patient data replicas for training purposes. Users anticipate AI will fundamentally reshape curriculum delivery by generating highly adaptive educational content, providing immediate, granular feedback on performance in simulated environments, and efficiently managing the enormous administrative burden associated with student tracking and compliance monitoring. Furthermore, there is significant interest in AI's role in future-proofing the medical curriculum, ensuring that trainees are prepared to work alongside AI tools in clinical settings, thereby embedding digital literacy and data interpretation skills into core competencies.

The market dynamics of Medical Education are profoundly shaped by a complex interplay of systemic drivers, structural restraints, and emerging opportunities, all magnified by critical impact forces. Primary drivers include the global mandate for standardized, high-quality medical training, fueled by increasing prevalence of complex chronic diseases and the imperative to improve global health outcomes. Technological advancements, particularly in extended reality (XR) and high-fidelity simulation, act as a powerful driving force by offering scalable and highly effective training methodologies that transcend geographical barriers. Restraints include the high initial investment required for sophisticated simulation equipment and technology infrastructure, alongside the significant challenge of gaining widespread faculty acceptance and training faculty members to effectively integrate new digital pedagogies into traditional curricula. Furthermore, stringent and often disparate regulatory frameworks across countries pose barriers to the standardization and international deployment of certain educational content and certification programs.

Opportunities for growth are abundant, notably in the rapidly expanding Continuous Medical Education (CME) segment, which presents a perpetual demand cycle driven by licensing requirements and the constant flow of new scientific discoveries. There is also a substantial opportunity in developing specialized training modules for emerging fields such as genomics, telemedicine, and health informatics, areas where current curricula often lag behind clinical necessity. The integration of robust data analytics into learning management systems offers a clear path toward personalized, outcome-focused education, which institutions can market as a superior training model. Strategic public-private partnerships aimed at subsidizing technology deployment in lower-resource settings represent a critical avenue for market expansion and achieving scale.

The impact forces currently restructuring the market include globalization, which facilitates the cross-border mobility of both students and educational resources, intensifying competition among institutions to offer globally recognized degrees. Demographic shifts, characterized by aging populations in many developed nations, place immense pressure on the system to rapidly train geriatric specialists and primary care physicians, demanding faster, more efficient educational throughput. Economic forces, such as the rising cost of traditional medical school education, incentivize the adoption of cost-effective digital alternatives. Regulatory forces, spearheaded by bodies like the Accreditation Council for Graduate Medical Education (ACGME) or the European Union of Medical Specialists (UEMS), continually raise the bar for instructional quality and assessment rigor, compelling consistent infrastructure upgrades and adherence to evidence-based educational standards.

The Medical Education Market is segmented comprehensively based on several critical dimensions, including educational level, type of training methodology, delivery method, and end-user engagement. This granular approach helps identify key growth pockets and strategic investment areas within the highly diversified ecosystem. The market structure reflects the entire professional life cycle of a healthcare provider, from foundational academic training through specialized residency and culminating in lifelong professional development. Dominant segmentation factors include the increasing reliance on technology-enabled solutions and the shift away from purely physical classrooms, particularly within the CME/CPD sector, where flexibility and accessibility are paramount.

The Medical Education value chain begins with the Upstream Analysis, which involves the content creators and foundational technology providers. This segment includes academic faculty who generate curriculum content and clinical knowledge, specialized medical publishers, software developers who build learning management systems (LMS) and assessment tools, and hardware manufacturers supplying simulation equipment, virtual reality headsets, and 3D printing services for anatomical models. The quality and intellectual rigor of the content, coupled with the reliability and interoperability of the underlying technology infrastructure, are critical determinants of value at this stage. Strong research partnerships between academic centers and technology firms ensure that educational tools remain clinically relevant and pedagogically effective, driving innovation in learning delivery.

The core of the value chain is the transformation and distribution segment. Transformation involves medical schools, residency program directors, and CME providers adapting raw clinical knowledge into structured, accredited educational programs, integrating simulation exercises, clinical rotations, and standardized testing. The Distribution Channel is bifurcated into Direct and Indirect methods. Direct channels include institutional delivery, where medical schools directly enroll and teach students, or major hospital systems managing their own residency programs. Indirect channels rely heavily on third-party digital platforms (MOOC providers, specialized e-learning firms) and global medical societies that disseminate educational materials and host international conferences. The efficiency of the LMS and the quality of the technical support are crucial factors influencing learner satisfaction and institutional return on investment in the indirect distribution model.

Downstream analysis focuses on the end-users and the realization of educational outcomes. End-users—including medical students, residents, practicing physicians, nurses, and allied health professionals—utilize the training to achieve specific goals such as passing board certification exams, obtaining licensure renewal (CME), or acquiring specialized procedural skills. The final measure of value is the measurable improvement in clinical competency and patient care outcomes. Feedback loops connecting clinical performance data back to curriculum developers are essential for continuous quality improvement. The entire chain is heavily regulated, meaning accreditation and compliance services also form a significant value-added component, ensuring that the delivered education meets the necessary professional and legal standards required for practice.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 55.2 Billion |

| Market Forecast in 2033 | USD 104.9 Billion |

| Growth Rate | 9.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Laerdal Medical, Elsevier Education, Siemens Healthineers, Philips Healthcare, Medtronic, Wolters Kluwer, CAE Healthcare, IBM Watson Health, 3D Systems, Area9 Lyceum, AMBOSS, Coursera, Vyaire Medical, Surgical Science, HealthStream, Microsoft, Remedy Education, Osso VR, SimuLab, Mentice. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

Potential customers in the Medical Education Market are highly diversified, encompassing institutions responsible for initial professional training and organizations dedicated to ongoing clinical competence. Academic Medical Centers (AMCs), including universities and affiliated teaching hospitals, constitute the foundational customer base, driving demand for robust Learning Management Systems, high-fidelity patient simulators, and specialized anatomical models necessary for foundational and advanced surgical training. These institutions are characterized by large student cohorts, complex regulatory compliance needs, and a persistent requirement for cutting-edge technology integration to maintain their competitive standing and accreditation status. The investment decisions within AMCs are often long-term and focus on scalable, multi-disciplinary solutions that can serve undergraduate, graduate, and faculty development needs simultaneously, ensuring a consistent revenue stream for technology providers.

The second major customer group consists of large Hospital Networks and Integrated Delivery Systems (IDSs). While they manage residency programs (GME), their primary driver for educational purchases is Continuing Medical Education (CME) and mandated institutional training related to patient safety, compliance, and new clinical guideline implementation. IDSs require flexible, modular e-learning content that can be deployed rapidly across dispersed geographical locations and consumed by practicing physicians and allied health staff with limited time constraints. Their purchasing decisions prioritize efficiency, regulatory adherence, and the ability to track completion rates accurately, making specialized CME providers and data analytics platforms highly valuable partners.

Finally, Pharmaceutical and Medical Device Companies represent a distinct and high-value customer segment. These entities invest heavily in proprietary medical education to train physicians and surgeons globally on the correct and safe usage of their specific products, whether novel therapeutics or complex surgical robots. This segment drives demand for specialized procedural simulation, often customized for their specific hardware, and utilizes accredited educational programs to support product adoption and market penetration. Their spending often focuses on high-end, specialized training solutions and global distribution platforms, where regulatory approval and scientific accuracy are paramount. Professional medical societies and specialized certification bodies also represent a critical niche, purchasing assessment tools and standardized curriculum materials to ensure consistency across their membership base.

The technology landscape of the Medical Education Market is rapidly evolving, moving beyond simple digitized textbooks to encompass sophisticated, immersive, and data-driven solutions. High-fidelity patient simulators remain foundational, integrating advanced physiological modeling with manikins that replicate human responses to treatments and complications, allowing trainees to practice crucial skills such as airway management, cardiac arrest protocols, and complex obstetric scenarios in a safe environment. Complementing this are Extended Reality (XR) tools, which include Virtual Reality (VR) for immersive anatomical study and surgical rehearsal, and Augmented Reality (AR) overlays that enhance real-world clinical training by providing on-the-spot guidance or visualizing underlying structures during procedures. These technologies drastically reduce the reliance on cadaver labs and operating room time, offering scalability and repeatable practice opportunities.

Digital platforms constitute the nervous system of modern medical education. Learning Management Systems (LMS) are essential for administering, documenting, tracking, and reporting educational courses and training outcomes. These systems are increasingly integrated with sophisticated assessment software that supports competency-based evaluations, including standardized patient encounters (using software to manage actors) and objective structured clinical examinations (OSCEs). Furthermore, the rise of specialized microlearning platforms and adaptive testing engines, often powered by machine learning algorithms, ensures that education is delivered in digestible formats tailored to the individual learner’s pace and professional needs, effectively tackling the challenge of information overload inherent in medical curricula.

The next frontier is the pervasive integration of Artificial Intelligence (AI) and Big Data Analytics. AI is utilized for performance benchmarking, identifying predictive indicators of clinical success or failure among trainees, and creating realistic, branching scenarios for diagnostic practice where the AI acts as a sophisticated, responsive patient or standardized examiner. Tele-education infrastructure, leveraging high-speed internet and secure video conferencing, is crucial for delivering specialist training to remote locations and for managing remote proctoring during certification exams. The convergence of these technologies—simulation, XR, personalized LMS, and AI analytics—is creating a cohesive, comprehensive educational environment aimed squarely at improving measurable clinical competence and addressing the variability traditionally found in medical training outcomes.

The dominant growth driver is the persistent global shortage of trained healthcare professionals, coupled with the mandatory requirement for Continuous Medical Education (CME) enforced by regulatory bodies worldwide. This necessity mandates the rapid scaling and modernization of training methodologies through technological adoption, specifically high-fidelity simulation and e-learning, to ensure consistent, high-quality competency development.

Technology is shifting curricula from traditional passive learning to active, competency-based medical education (CBME). Key technologies, including Virtual Reality (VR), Augmented Reality (AR), and AI-driven simulators, allow trainees to practice complex procedures safely, receive personalized feedback, and engage in high-risk scenarios repeatedly, thereby accelerating skill acquisition and minimizing the learning curve in clinical settings.

The Continuing Medical Education (CME) and Continuing Professional Development (CPD) segment currently commands the largest revenue share. This dominance is due to the perpetual demand cycle driven by licensing renewal requirements, the constant need for practicing clinicians to update knowledge on new research and guidelines, and the regulatory mandate for professional competency across all medical specialties.

The primary restraints include the substantial initial capital investment required to establish and maintain advanced simulation centers and technological infrastructure. Additionally, challenges exist in achieving widespread faculty acceptance and proficiency with new digital tools, coupled with the difficulty in standardizing regulatory compliance across diverse international markets, hindering global deployment.

AI significantly improves assessment rigor and objectivity by automating the evaluation of clinical performance, diagnostic reasoning, and procedural skills in simulated environments. AI-driven systems provide granular, unbiased feedback, track long-term competency progression, and help educators identify critical performance deficits that require targeted remediation, thus ensuring higher standards for certification.

This report provides a comprehensive overview and strategic insights into the current dynamics and future trajectory of the global Medical Education Market, highlighting key areas of technological influence, regional opportunities, and critical market structure elements necessary for strategic decision-making in this vital sector.

The development of interprofessional education (IPE) is a significant trend, pushing the market towards integrated training solutions that can accommodate diverse healthcare roles, including nurses, pharmacists, and allied health professionals, alongside physicians. This interdisciplinary approach necessitates specialized simulation and e-learning modules designed to foster teamwork, communication, and collaborative decision-making, which are crucial components of modern healthcare delivery systems. Institutions are increasingly looking for vendors that offer holistic platforms capable of managing IPE curricula and outcomes assessment under a single, unified system, simplifying administrative oversight and maximizing resource efficiency across various health professional programs. The success of these integrated platforms hinges on their ability to accurately simulate the complexities of real-world clinical teams operating under pressure, driving demand for high-end, networked simulation environments.

Furthermore, the focus on preventative care and public health necessitates educational content that goes beyond traditional disease management. The Medical Education Market is responding by incorporating modules on social determinants of health, population health management, and health policy into core curricula. This reflects a broader societal demand for physicians who are not only technically proficient but also adept at navigating complex healthcare systems and advocating for community well-level well-being. Providers of educational content are thus required to collaborate with public health experts and policymakers to ensure their offerings are relevant and up-to-date with emerging global health crises and priorities, fostering a more holistic approach to medical training.

The sustainability of the market is also tied to ethical considerations surrounding data privacy and the use of de-identified patient data in educational simulations and AI-driven tutors. Potential customers, particularly academic institutions and hospitals, demand that technology solutions adhere strictly to regional data protection regulations (like GDPR or HIPAA), ensuring secure handling of trainee performance data and any synthesized clinical information used for practice. Vendors who can provide robust, compliant, and transparent data security frameworks gain a competitive advantage, as institutional trust in educational technology platforms is paramount for long-term adoption and successful integration into mandated training pipelines. Investment in secure cloud infrastructure and blockchain technology for credential verification are becoming increasingly relevant technological requirements in this domain.

The globalization of accreditation standards is a silent, yet powerful, impact force. As medical schools seek international recognition and students desire portable degrees, adherence to global benchmarks set by organizations like the World Federation for Medical Education (WFME) becomes critical. This pressure standardizes the quality of education delivered, indirectly boosting demand for uniform, high-quality digital learning resources and assessment technologies that can be reliably deployed and audited worldwide. This phenomenon drives standardization in instructional design and pushes lower-tier institutions to upgrade their educational infrastructure to meet international quality thresholds, thereby expanding the overall potential customer base for advanced educational solutions and driving growth in emerging markets seeking international parity.

The competition within the technology provider segment is intense, characterized by both large, established medical device manufacturers (e.g., Siemens Healthineers, Medtronic, Philips) leveraging their existing clinical relationships to sell training solutions, and nimble, specialized EdTech startups (e.g., Osso VR, Mentice) focusing purely on highly specific simulation or adaptive learning software. This competitive landscape fosters rapid innovation, particularly in areas like haptics feedback for surgical simulation and cloud-based content delivery, pushing down the cost curve for certain basic educational modules while raising the performance threshold for high-end simulators. Strategic acquisitions of smaller, specialized technology firms by larger traditional publishers or simulation companies are frequent, consolidating market share and integrating niche capabilities into broader, more comprehensive platform offerings. The long-term success of vendors is increasingly reliant on their ability to offer integrated, end-to-end solutions covering UME, GME, and CME needs.

Furthermore, the rise of telehealth and remote patient monitoring requires medical education to rapidly evolve its focus on non-physical examination skills, communication protocols across digital mediums, and ethical use of technology in remote diagnosis. This demand fuels the growth of specialized modules within e-learning platforms that focus explicitly on virtual care delivery, prompting institutions to procure specialized software that mimics remote consultation environments. The integration of telemedicine training into core residency programs is no longer optional but a regulatory expectation, creating a new, substantial demand vertical within the training methodology segmentation, particularly for scenario-based training that assesses both clinical judgment and professional digital communication competence.

Investment patterns reflect a clear prioritization of experiential learning tools over purely didactic content. Capital expenditure by academic centers is moving from lecture hall renovations towards building advanced simulation centers and acquiring institutional licenses for virtual anatomy platforms. This shift is validated by strong educational research supporting the efficacy of simulation in achieving measurable competency milestones faster than traditional methods. Therefore, vendors specializing in realistic, anatomically accurate, and physiologically responsive training aids—ranging from full-body manikins to specific task trainers for procedures like central line insertion or ultrasound-guided biopsies—are experiencing the most robust growth and commanding premium pricing based on the fidelity and clinical relevance of their products.

The market also faces inherent challenges related to the longevity and maintenance of highly technical simulation equipment. The total cost of ownership (TCO) for high-fidelity simulators is substantial, encompassing not just the initial purchase price but also software licensing, dedicated technical staff for operation and repair, and continuous updates to simulation scenarios to reflect the latest clinical guidelines. This high TCO acts as a significant barrier to entry for smaller or less-funded institutions, particularly in developing regions. Consequently, service contracts, maintenance agreements, and technology-as-a-service (TaaS) models offered by major vendors are becoming crucial revenue streams, allowing institutions to manage costs through operational leasing rather than large upfront capital outlays, thereby stabilizing vendor revenues over the long term.

Finally, the growing specialization within medicine—giving rise to highly niche fields such as interventional oncology, structural heart disease, and palliative care—drives demand for hyper-specific CME modules. This micro-segmentation of the training market necessitates partnerships between content providers and professional specialty societies to ensure clinical accuracy and accreditation status. The educational resources developed for these niche areas are often highly technical, requiring specialized instructional design and leveraging advanced 3D visualization and simulation to convey complex anatomical and procedural details effectively. This demand for highly customized, specialized educational products represents a premium market segment with strong pricing power and limited provider competition, contributing disproportionately to revenue growth within the CME category.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.