ID : MRU_ 431403 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

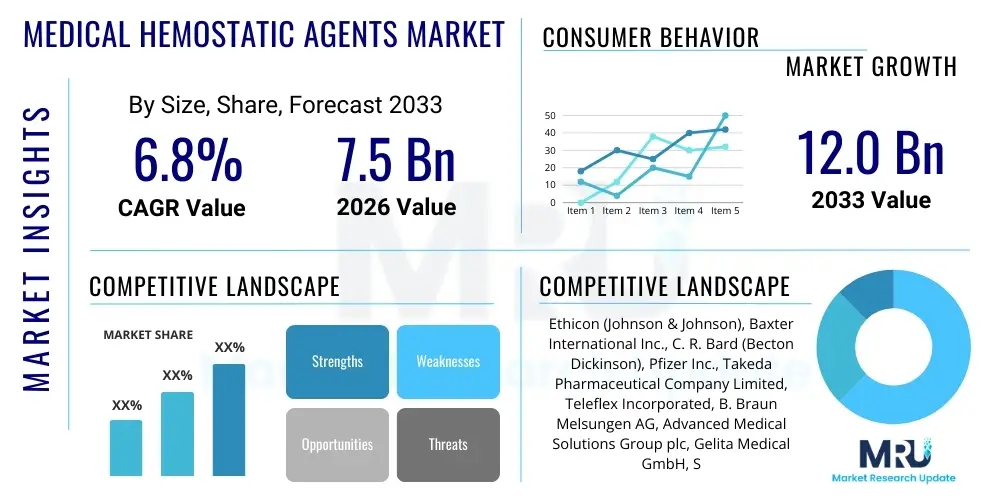

The Medical Hemostatic Agents Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at $7.5 Billion in 2026 and is projected to reach $12.0 Billion by the end of the forecast period in 2033.

Medical hemostatic agents are specialized therapeutic products designed to control bleeding during surgical procedures, trauma management, or in patients suffering from clotting disorders. These agents work by physically or biochemically accelerating the natural coagulation cascade, providing immediate and localized control over hemorrhage. The portfolio encompasses a wide range of products including mechanical hemostats, topical sealants, and bio-derived agents like fibrin sealants and thrombin-based formulations. The primary function is to achieve rapid and effective hemostasis, thereby reducing blood loss, minimizing the need for blood transfusions, shortening operation times, and ultimately improving patient outcomes, especially in complex or high-risk surgical settings.

Major applications of hemostatic agents span across cardiovascular surgery, general surgery (abdominal and thoracic), neurosurgery, orthopedic procedures, and trauma care. The increasing complexity of surgical interventions, coupled with the rising prevalence of chronic diseases requiring surgical management (such as cardiovascular disorders and cancer), are central drivers for market expansion. Furthermore, the global shift towards minimally invasive surgical techniques, where traditional mechanical hemostasis methods are challenging, increases the reliance on advanced topical agents that can be delivered efficiently through small incisions. The ongoing development of synthetic, highly biocompatible agents is enhancing product safety profiles and expanding their utility.

Key benefits driving the adoption of these products include their effectiveness in managing diffuse bleeding (oozing) and in patients with compromised coagulation pathways. They are essential tools in modern surgical environments where rapid return to functional status is prioritized. The market is witnessing robust innovation focused on combination products that offer dual mechanisms of action—combining physical barriers with biochemical stimulation—to address severe bleeding scenarios more comprehensively. The imperative to manage costs associated with post-operative complications and lengthy hospital stays further underpins the value proposition of effective hemostatic solutions.

The Medical Hemostatic Agents Market is characterized by steady technological advancements aimed at improving efficacy and ease of use, driven primarily by the global rise in surgical volumes and the need for enhanced bleeding control protocols in high-acuity settings. Business trends indicate a strong focus on strategic mergers and acquisitions among key players to consolidate product portfolios and gain access to specialized technologies, particularly in the realm of advanced biological and polymer-based sealants. The demand for synthetic and rapidly absorbable hemostats is growing, positioning companies that invest heavily in biomaterials research favorably. Furthermore, increasing regulatory scrutiny, while a challenge, is simultaneously driving market maturation by favoring high-quality, clinically proven products, establishing barriers to entry for smaller competitors and cementing the leadership of established manufacturers.

Regionally, North America maintains its dominance due to high healthcare expenditure, sophisticated surgical infrastructure, and quick adoption of premium products, especially fibrin sealants and topical thrombin formulations used in major cardiac and orthopedic surgeries. However, the Asia Pacific (APAC) region is projected to register the fastest growth rate, fueled by improving healthcare access, rising incidence of trauma, and the rapid expansion of medical tourism and surgical capacity in countries like China and India. European market growth remains stable, supported by stringent regulatory frameworks ensuring high product quality and continuous geriatric population growth driving surgical demand. Manufacturers are increasingly focusing on local manufacturing and distribution partnerships in emerging economies to capitalize on these growth trajectories.

Segment trends reveal that the topical hemostats segment, particularly the thrombin-based and combination agents, commands the largest market share due to their versatility and broad application across various surgical specialties. The growing preference for minimally invasive procedures is bolstering the segment of flowable hemostats, which can be easily delivered to internal sites. Furthermore, the application segment of cardiovascular and trauma surgery is experiencing rapid growth, reflecting the critical need for immediate, life-saving bleeding control in these specific high-risk scenarios. The market continues to shift towards highly specialized and expensive biological agents, offsetting the price pressure seen in commodity-based hemostatic products like oxidized regenerated cellulose.

User inquiries regarding the impact of Artificial Intelligence (AI) on the Medical Hemostatic Agents Market often revolve around optimizing surgical planning, predictive modeling for bleeding risk, and improving material design. Key themes emerging from these concerns include whether AI can personalize hemostat selection based on individual patient coagulation profiles, how machine learning might accelerate the discovery of novel bioactive agents, and the potential for real-time surgical assistance systems to dictate hemostat application during complex procedures. Users are also concerned about the integration challenges of AI-driven diagnostics (like viscoelastic testing analysis) with physical product application, and the resulting pressure on manufacturers to integrate AI-compatible data streams into product usage protocols. The overall expectation is that AI will primarily enhance precision, reduce material waste, and improve procedural efficiency related to hemorrhage management.

The Medical Hemostatic Agents Market is propelled by several strong drivers, counterbalanced by significant restraints, creating dynamic market opportunities that influence strategic decisions. The primary driving force is the global demographic shift, specifically the aging population, which necessitates an increasing number of complex surgical procedures prone to hemorrhage, such as joint replacements and cardiac interventions. Additionally, advancements in surgical complexity, including specialized cancer surgeries and transplantation procedures, mandate the use of highly effective and advanced hemostatic products. Opportunities are particularly rich in the development of combination agents that offer superior performance in controlling severe arterial and venous bleeding, and in expanding applications into fields like interventional radiology and military medicine. The overall impact force resulting from the interplay of these factors is high, indicating sustained market growth despite persistent pricing and regulatory challenges.

Key drivers include the rising global incidence of trauma, accidents, and cardiovascular diseases, all requiring immediate and effective bleeding management. Regulatory bodies are increasingly mandating stricter guidelines for surgical outcomes, pushing hospitals and surgeons toward products offering superior safety and efficacy profiles. Furthermore, the adoption of specialized hemostatic agents reduces complications and readmission rates, offering tangible economic benefits to healthcare systems, which further encourages their procurement and routine use. The shift towards proprietary, bio-absorbable synthetic agents over traditional, mechanical methods represents a substantial market transformation driven by clinical demands for less invasive and faster-healing solutions.

However, the market faces significant restraints, chiefly the high cost associated with advanced biological hemostatic agents, which limits their usage in cost-sensitive markets and smaller healthcare facilities. Regulatory pathways, especially for combination drug-device products, are often complex and time-consuming, delaying market entry for innovative products. Another substantial restraint is the persistent lack of comprehensive clinical evidence comparing the efficacy and cost-effectiveness of various specialized agents, making purchasing decisions difficult for hospital value analysis committees. Despite these hurdles, the substantial opportunity presented by unmet clinical needs in internal medicine (e.g., managing GI bleeds) and the rapid technological progress in biodegradable polymers ensure that the market remains highly attractive for sustained investment and innovation.

The Medical Hemostatic Agents Market is broadly segmented based on product type, application, and end-user, reflecting the diverse clinical needs addressed by these specialized products. Product segmentation distinguishes between topical hemostats, internal hemostats, and sealants, with topical agents commanding a substantial market share due to their versatility in handling generalized capillary and venous oozing across various surgical procedures. Segmentation by material type—including thrombin-based, fibrin-based, gelatin-based, and oxidized regenerated cellulose (ORC)—highlights the spectrum of efficacy and cost profiles available, catering to different surgical risk levels and healthcare budgets. The application segmentation demonstrates the critical reliance of high-acuity specialties such as cardiovascular, neurosurgery, and trauma care on premium hemostatic solutions.

The product landscape continues to evolve, driven by the shift towards bio-absorbable and combination products that offer mechanical barriers coupled with active biochemical coagulation promotion. Flowable hemostats, a subsegment of topical agents, are experiencing accelerated growth due to their effective deployment in hard-to-reach areas during minimally invasive and robotic surgeries, offering a significant advantage over rigid or patch-based products. This technological shift is directly influenced by end-user preferences, where hospitals and specialized surgical centers increasingly prioritize products that streamline procedures and reduce overall operating room time.

Analyzing the end-user segmentation shows that hospitals, particularly tertiary care centers and academic medical institutions, represent the largest consumers of hemostatic agents, especially the high-value biological products, owing to their high volume of complex surgeries. Ambulatory surgical centers (ASCs), while traditionally utilizing less complex hemostats, are rapidly adopting advanced products as the complexity of procedures performed in these settings increases. This detailed market segmentation provides manufacturers with critical insights into tailoring their distribution strategies and product development pipelines to target specific high-growth clinical areas and emerging geographical markets effectively.

The value chain for the Medical Hemostatic Agents Market is complex, starting with the procurement and refinement of highly specialized raw materials, spanning R&D, manufacturing, regulatory approval, and culminating in surgical application. Upstream activities involve sourcing high-purity biological components (like bovine or human thrombin and fibrinogen) or specialized synthetic polymers (like oxidized cellulose or gelatin). Strict quality control and compliance with Good Manufacturing Practices (GMP) are crucial at this stage due to the critical nature of these medical devices and biologics. Innovation here focuses on reducing immunogenicity risks associated with biological agents and enhancing the absorbability and efficacy of synthetic materials through novel cross-linking technologies.

The midstream section, dominated by manufacturing and assembly, involves significant capital investment in sterile processing facilities. This stage is characterized by intellectual property protections around formulation and delivery systems (e.g., flowable consistency or applicator design). Regulatory affairs play a pivotal role, as clearance from bodies like the FDA or EMA determines market access and claim validation. Distribution channels are highly controlled and segmented, utilizing both direct sales forces, particularly for high-volume hospital systems and specialized academic centers, and indirect distribution through established medical device wholesalers and distributors for broader geographical reach and inventory management efficiencies.

Downstream analysis focuses on the end-users—surgeons, nurses, and hospital procurement departments—who assess product performance, ease of use, and cost-effectiveness. Direct sales forces are vital for providing technical training and clinical support to ensure proper usage, which is critical for product efficacy and liability management. The purchasing decisions are often influenced by clinical protocols, established surgical preferences, and centralized hospital purchasing groups negotiating long-term supply contracts. Effective supply chain management is crucial to ensure that temperature-sensitive biological agents maintain their potency until the point of use, completing the value delivery loop efficiently and safely.

The primary consumers and end-users of medical hemostatic agents are institutions and personnel involved in acute medical intervention, surgical procedures, and trauma management. Hospitals, particularly those with high-volume surgery departments such as cardiovascular, orthopedic, and neurosurgery, constitute the largest segment of potential buyers. These centers require a constant supply of diverse agents—from economical ORC products for minor bleeding to premium, fast-acting fibrin sealants for complex cardiac bypass operations. Their purchasing is driven by clinical requirements for superior efficacy and the need to comply with surgical guidelines aimed at reducing blood transfusions and surgical site complications.

Beyond traditional hospitals, Ambulatory Surgical Centers (ASCs) represent a rapidly expanding customer base. As ASCs increasingly handle more complex outpatient procedures, including joint arthroscopies and certain plastic surgeries, their demand for intermediate-level hemostats and sealants is rising significantly. Furthermore, government organizations, including military medical corps and national disaster relief agencies, are key niche customers, requiring rugged, long-shelf-life hemostatic products for battlefield medicine and emergency response kits where immediate and effective hemorrhage control is paramount.

Specialty clinics focusing on dental surgery, aesthetics, and interventional radiology also form a crucial customer segment. Interventional procedures, which are minimally invasive but carry localized bleeding risks, necessitate the use of specialized agents that can be delivered percutaneously or through catheters. Overall, the buying behavior is highly centralized and influenced by clinical champions (surgeons) and value assessment committees, emphasizing the importance of robust clinical data and favorable health economic outcomes (HEOR) for successful market penetration.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $7.5 Billion |

| Market Forecast in 2033 | $12.0 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Ethicon (Johnson & Johnson), Baxter International Inc., C. R. Bard (Becton Dickinson), Pfizer Inc., Takeda Pharmaceutical Company Limited, Teleflex Incorporated, B. Braun Melsungen AG, Advanced Medical Solutions Group plc, Gelita Medical GmbH, Stryker Corporation, Integra LifeSciences, CryoLife Inc., Medtronic plc, 3M Company, Kiniksa Pharmaceuticals, Cohesion Medical, Hemostasis LLC, Meril Life Sciences, Shanghai RAAS Blood Products, Smith & Nephew plc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Medical Hemostatic Agents Market is rapidly evolving, driven by the need for agents that provide immediate, targeted, and safe hemorrhage control. The central technological push involves developing sophisticated bio-derived agents, such as highly purified, concentrated fibrinogen and thrombin formulations, often coupled with advanced delivery systems (e.g., dual-syringe applicators) for precise mixing and targeted application. Advances in material science are leading to next-generation synthetic hemostats, including specialized polymer scaffolds and micro-porous beads, engineered for rapid blood absorption and platelet concentration, offering alternatives to animal-derived products which sometimes carry immune risks. These innovations prioritize absorbability, eliminating the need for removal and reducing foreign body reactions, crucial for optimizing surgical recovery.

Another key area of technological development is the creation of combination agents—products that merge mechanical components (like oxidized cellulose or gelatin matrices) with active biological factors (like thrombin). These synergistic products offer dual mechanisms of action, providing both a physical scaffold for clot formation and biochemical activation of the coagulation cascade, resulting in superior efficacy in high-pressure or anticoagulated patient environments. Flowable hemostats represent a major technological breakthrough, specifically designed with rheological properties that allow them to conform to irregular tissue surfaces and be delivered easily through narrow laparoscopic ports, significantly enhancing their utility in minimally invasive and robotic procedures where manual application is restricted.

Furthermore, the integration of smart materials and nanotechnology holds promise for future hemostatic solutions. Research is underway on injectable hemostatic hydrogels that self-assemble at the injury site and nanoscale particles that specifically target and activate platelets, offering instantaneous systemic hemostasis for internal trauma. The continuous emphasis on enhancing the safety profile necessitates rigorous viral inactivation processes for all plasma-derived products, along with stringent quality control of synthetic material purity. Overall, the technology is moving toward personalized, highly responsive agents that can adapt their performance based on the specific bleeding characteristics and clinical setting, driving the displacement of older, less efficacious products.

Market growth is primarily driven by the increasing global geriatric population, leading to a higher volume of complex surgical procedures (cardiac, orthopedic, neurological), and the rising incidence of trauma cases worldwide requiring immediate bleeding control solutions. Technological advancements in product efficacy and minimally invasive surgery further boost adoption.

Biological hemostats (e.g., fibrin sealants, thrombin) actively participate in the biochemical coagulation cascade, rapidly accelerating clot formation, and are ideal for diffuse bleeding. Mechanical hemostats (e.g., gelatin sponges, ORC) function primarily by providing a scaffold or physical matrix to concentrate platelets and physically obstruct blood flow. Biological agents are typically higher cost and used in more critical surgical settings.

The Asia Pacific (APAC) region is projected to register the fastest Compound Annual Growth Rate (CAGR). This acceleration is attributed to rapidly improving healthcare infrastructure, substantial investment in trauma and specialty surgical centers, and increasing access to advanced medical devices across developing economies within the region.

Manufacturers face significant regulatory complexity, especially for combination products classified as drug-device mixtures. Challenges include demonstrating long-term clinical superiority over existing standards of care, navigating stringent approval processes (like FDA premarket approval), and meeting rigorous safety standards for biological source materials (e.g., viral inactivation protocols).

The shift necessitates the development of flowable and sprayable hemostatic agents that can be easily delivered and applied through narrow laparoscopic or robotic ports. Manufacturers are innovating delivery systems and formulations to ensure products conform to internal irregular tissue surfaces without requiring direct manual manipulation, enhancing efficacy in constrained surgical environments.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.