ID : MRU_ 434795 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

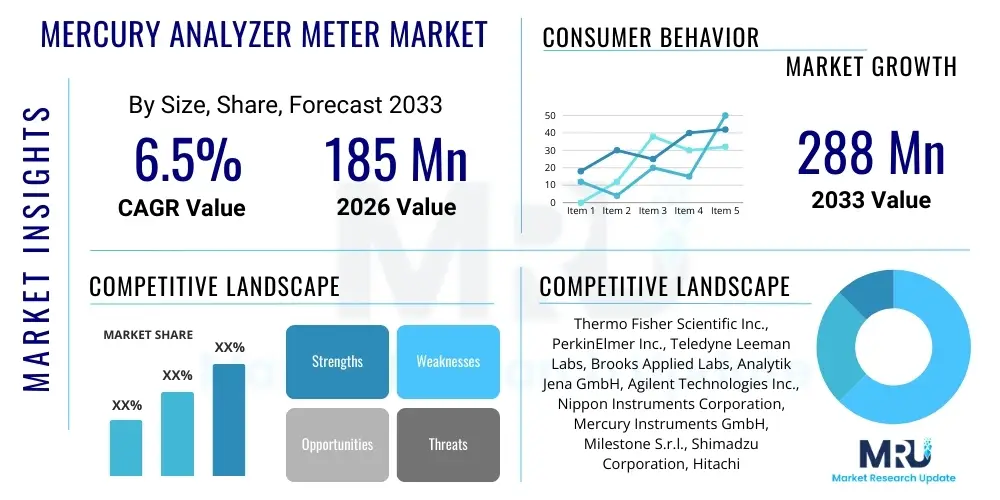

The Mercury Analyzer Meter Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at USD 185 Million in 2026 and is projected to reach USD 288 Million by the end of the forecast period in 2033.

The Mercury Analyzer Meter Market encompasses a range of sophisticated analytical instruments designed to accurately detect, measure, and quantify mercury concentrations in various matrices, including water, air, soil, gases, and biological samples. These instruments are crucial for environmental protection, industrial process control, and human health monitoring, driven primarily by increasing global awareness and stringent regulatory frameworks concerning mercury toxicity. The analyzers operate based on several core technologies, such as Cold Vapor Atomic Absorption Spectrometry (CVAAS), Cold Vapor Atomic Fluorescence Spectrometry (CVAFS), and Direct Combustion Analysis, each tailored for specific sample types and detection limits. The primary function of these meters is to ensure compliance with international treaties, most notably the Minamata Convention on Mercury, which aims to protect human health and the environment from anthropogenic emissions and releases of mercury and mercury compounds.

The product description spans from laboratory-based benchtop models offering high precision and ultra-low detection limits, suitable for certified testing facilities and research laboratories, to portable and online process analyzers required for real-time monitoring in industrial settings and field environmental surveys. Key applications include continuous emission monitoring systems (CEMS) in coal-fired power plants, quality control in the chlor-alkali industry, monitoring industrial wastewater discharge, and screening food and cosmetic products for safety compliance. The increasing industrialization, particularly in developing economies, coupled with growing environmental concerns related to coal combustion and mining activities, continually drives demand for robust and reliable mercury detection solutions.

Major benefits derived from utilizing advanced mercury analyzers include enhanced sensitivity, accuracy, and efficiency in testing procedures, often allowing for rapid, non-destructive analysis and minimizing sample preparation time. Driving factors for market expansion are multi-faceted, including mandatory regulatory enforcement, significant investments in environmental quality assurance programs by governments globally, and technological advancements leading to miniaturization and increased automation of testing equipment. Furthermore, public health initiatives focusing on monitoring mercury exposure pathways, especially through contaminated seafood, are creating specialized demand within the food safety testing segment, further solidifying the market's trajectory toward consistent growth throughout the forecast period.

The global Mercury Analyzer Meter Market is characterized by robust business trends driven by the pervasive need for environmental remediation and regulatory adherence. Key business trends include the shift towards fully automated and continuous mercury monitoring systems, particularly in large industrial sectors such as oil and gas, cement manufacturing, and energy generation. Furthermore, market competition is intensifying, focusing on developing highly sensitive CVAFS technology, which offers superior detection limits compared to traditional CVAAS, catering to ultra-trace analysis requirements in water and biological samples. Mergers and acquisitions remain a consistent strategy among established players seeking to integrate advanced software solutions, enhance regional distribution networks, and acquire specialized sensing technologies that improve instrument uptime and reduce overall cost of ownership for end-users.

Regionally, the market dynamics are highly differentiated, with North America and Europe maintaining dominance due to highly stringent regulatory enforcement, mature environmental monitoring infrastructure, and high levels of R&D investment supporting technological innovation. However, the Asia Pacific (APAC) region is projected to register the fastest growth rate, fueled by rapid industrial expansion, increasing government expenditure on mitigating severe pollution issues, and the proactive adoption of mercury reduction policies by major economies like China and India, particularly in response to Minamata Convention commitments. Latin America and the Middle East & Africa (MEA) represent emerging opportunities, where resource development projects and foundational environmental legislation are initiating the need for foundational monitoring capabilities, particularly in water and soil testing applications.

Segment trends reveal that the Cold Vapor Atomic Fluorescence Spectrometry (CVAFS) segment is anticipated to witness the highest growth, attributed to its unparalleled sensitivity, making it the preferred method for crucial applications like ultra-trace elemental analysis in regulatory compliance and research. Application-wise, the Environmental Monitoring sector dominates, encompassing air quality, water resource management, and soil contamination testing, reflecting the fundamental objective of mercury analysis. Within the product type category, portable mercury analyzers are gaining traction due to their utility in rapid screening, emergency response scenarios, and ease of use in diverse field locations, offering a cost-effective alternative for initial site assessments compared to complex laboratory instruments.

Common user inquiries regarding AI integration in the Mercury Analyzer Meter Market primarily center on how artificial intelligence can enhance analytical accuracy, automate calibration processes, and provide predictive maintenance for instruments. Users are keen to understand if AI-driven algorithms can effectively compensate for matrix effects, reduce false positives, and improve the speed of complex data interpretation, especially in real-time, continuous monitoring scenarios. Concerns often revolve around the security and validity of AI-processed environmental data and the initial cost of integrating sophisticated machine learning models into existing analyzer infrastructure. The summarized expectation is that AI will transform mercury analysis from a purely measurement-based task into a predictive and prescriptive monitoring discipline, optimizing resource allocation for pollution control and reporting.

The integration of artificial intelligence and machine learning (ML) holds significant potential to revolutionize the operational efficiency and analytical capability of mercury analyzer meters. AI algorithms can be employed to perform complex pattern recognition on continuous stream data generated by online analyzers, identifying subtle deviations indicative of potential instrument failure, contamination issues, or non-compliance events long before they escalate. This capability enables highly effective predictive maintenance scheduling, maximizing instrument uptime and ensuring data integrity, which is paramount for regulatory compliance reporting. Moreover, ML models can analyze vast datasets collected across multiple sites, improving the accuracy of environmental modeling and source apportionment studies related to atmospheric or aqueous mercury pollution.

Furthermore, AI is instrumental in streamlining the labor-intensive aspects of mercury analysis. Automated data processing systems utilizing AI can handle quality assurance/quality control (QA/QC) checks, flag outliers, and automate compliance reporting, thereby reducing human error and freeing up laboratory personnel for more complex tasks. In the field of sensor-based portable analyzers, AI can be used to dynamically adjust calibration curves based on ambient environmental conditions (e.g., temperature, humidity, pressure), ensuring robust and reliable measurements outside controlled laboratory environments. This advancement is particularly critical for enabling deployment in remote or harsh environments where access for manual calibration is limited, significantly enhancing the overall utility and reach of mercury monitoring programs.

The Mercury Analyzer Meter Market is powerfully shaped by a confluence of accelerating drivers (D), persistent restraints (R), emerging opportunities (O), and significant impact forces. The primary driving force is the global implementation of the Minamata Convention, which necessitates comprehensive monitoring across industrial emissions, product testing, and environmental matrices, compelling nations to invest heavily in appropriate instrumentation. This regulatory impetus is supported by technological advancements, such specifically the increasing sensitivity and portability of analytical instruments, allowing for monitoring in previously inaccessible locations. However, the market faces restraints centered around the high initial capital investment required for high-end laboratory analyzers and the necessity for highly trained technical personnel to operate and maintain these complex systems, which presents a significant barrier to adoption in smaller laboratories and developing countries.

Opportunities in the market are abundant, particularly in the development of low-cost, sensor-based analyzers tailored for continuous, wide-scale network monitoring, which opens up new revenue streams in smart city initiatives and decentralized environmental management systems. The growing focus on biological monitoring (hair, blood, urine samples) to assess human exposure levels provides a specialized niche for high-sensitivity medical and clinical analyzers. Impact forces are predominantly driven by the swift pace of technological change, pushing existing instrumentation towards obsolescence faster than traditional lifecycles, and the increasing societal pressure on corporations for environmental transparency, forcing industries to adopt robust, independently verifiable monitoring practices.

Furthermore, the competitive landscape is intensely focused on achieving lower detection limits, moving into the parts per trillion (ppt) and even sub-ppt range, especially crucial for ultrapure water testing in the semiconductor industry and oceanographic research. This drive for sensitivity is directly proportional to the stringency of proposed and existing environmental standards. The high cost of specialized reagents and consumables used in CVAFS and CVAAS techniques, coupled with challenges related to sample matrix complexity (which can interfere with measurements), acts as a continuous restraint on operational expenses. Overcoming these limitations through enhanced automation, simplified calibration protocols, and the integration of microfluidics represents the primary path for leveraging market opportunities and addressing persistent user challenges.

The Mercury Analyzer Meter Market is systematically segmented based on technology, application, and product type, providing a granular view of demand across various end-user industries and analytical requirements. The technology segmentation differentiates instruments based on their underlying analytical principles, ranging from traditional techniques like Cold Vapor Atomic Absorption to more advanced and sensitive methods such as Atomic Fluorescence and Direct Combustion. This segmentation is critical as it dictates the level of sensitivity, sample throughput, and application suitability of the instruments, catering to regulatory needs which often specify the required analytical methodology for compliance testing.

The segmentation by application highlights the diverse areas where mercury analysis is indispensable, primarily focusing on environmental testing (water, air, soil), industrial quality control (petrochemicals, cement, mining), and clinical/biological monitoring. The environmental segment remains the dominant consumer of mercury analyzers, driven by comprehensive government mandates and global treaties. Meanwhile, the product type segmentation categorizes instruments into benchtop (laboratory use), portable (field use), and continuous online analyzers (industrial process control), reflecting the user's need for high precision versus mobility and real-time data acquisition.

Understanding these segments is paramount for strategic market planning. For instance, the demand for continuous online analyzers is robust in large industrial facilities requiring uninterrupted monitoring of stack emissions, while benchtop models continue to be the standard for certified reference laboratories needing absolute accuracy. The ongoing trend toward miniaturization and enhanced battery life in portable units indicates significant future growth potential within regulatory inspection agencies and emergency response teams, ensuring market participants must continuously innovate across all three segmentation axes to maintain competitive relevance.

The value chain for the Mercury Analyzer Meter Market begins with upstream activities involving the sourcing of highly specialized components, including noble metals (like gold for amalgamation collectors), advanced optical components (detectors, lamps), and precision fluidic systems. Key upstream suppliers provide highly purified reagents, specialized materials for sensor manufacturing, and crucial electronic modules. The analytical instrument manufacturing stage is highly complex, requiring specialized engineering expertise to integrate fluidics, optics, and software, ensuring the instrument meets ultra-low detection limit specifications and regulatory standards. Successful manufacturers often invest heavily in R&D to optimize the detection method and improve system reliability and automation capabilities.

The distribution channel plays a critical role in reaching diverse end-users globally. Direct sales channels are often employed for major industrial clients and governmental laboratories, allowing manufacturers to provide specialized installation, training, and long-term maintenance contracts. Indirect distribution relies heavily on regional distributors, value-added resellers (VARs), and channel partners, particularly in fragmented or emerging markets, who handle logistics, local support, and regulatory compliance assistance. These intermediaries ensure market penetration for portable and benchtop units across various regional analytical laboratories and environmental consulting firms, acting as crucial links between high-tech producers and localized user needs.

Downstream activities involve the extensive after-sales support ecosystem, which includes instrument calibration, preventative maintenance services, provision of certified reference materials (CRMs), and software upgrades. This stage is crucial for customer retention and recurring revenue generation, as the instruments often require routine servicing to maintain certified performance levels. End-users span environmental agencies, petrochemical companies, universities, and clinical testing labs. The efficiency of the value chain is largely determined by the manufacturer's ability to minimize supply chain disruptions for specialized components and provide rapid, expert technical support, particularly as instruments are increasingly used for mission-critical environmental compliance monitoring.

Potential customers for Mercury Analyzer Meters are primarily driven by mandatory compliance requirements and the need for precision quality control in sensitive applications. The largest segment of end-users consists of governmental and regulatory bodies, including Environmental Protection Agencies (EPAs), public health departments, and international environmental organizations, who utilize these devices for broad environmental surveillance, regulatory enforcement, and public risk assessment across air, water, and soil matrices. Industrial end-users represent the second major group, encompassing sectors identified as significant sources of mercury emissions, such as coal-fired power plants, chlor-alkali producers, cement manufacturers, and waste incinerators, all of whom require continuous online monitoring systems (CEMS) to meet discharge and emission permits.

Beyond regulatory compliance, the research and academic sector forms a stable customer base, utilizing high-end benchtop and specialized ICP-MS systems for fundamental research into biogeochemical mercury cycling, toxicological studies, and the development of new remediation techniques. Furthermore, independent commercial testing laboratories that provide contract services to smaller industrial entities or perform certification testing for consumer products (e.g., food, cosmetics) are significant buyers, demanding reliable and validated instrumentation to maintain accreditation. The growing market for biological sample analysis positions hospitals and clinical toxicology labs as emerging, high-potential customers, requiring ultra-trace analysis capabilities for assessing human exposure burdens.

The purchasing decisions of these diverse end-users are influenced not only by price and performance metrics but increasingly by factors such as instrument ease of use, automation capabilities, long-term operational costs (consumables), and the vendor's ability to provide accredited training and traceable calibration standards. The transition toward stricter global standards means that purchasing agencies are increasingly prioritizing CVAFS technology due to its superior sensitivity, ensuring that manufacturers must continuously focus on optimizing this technology to satisfy the requirements of the most demanding end-user segments.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 185 Million |

| Market Forecast in 2033 | USD 288 Million |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Thermo Fisher Scientific Inc., PerkinElmer Inc., Teledyne Leeman Labs, Brooks Applied Labs, Analytik Jena GmbH, Agilent Technologies Inc., Nippon Instruments Corporation, Mercury Instruments GmbH, Milestone S.r.l., Shimadzu Corporation, Hitachi High-Tech Corporation, Buck Scientific, Lumex Instruments, Ecotech Pty Ltd., Lasec S.A., Beijing Titan Instruments Co., Ltd., PCE Instruments, AMETEK Inc., S-cubed Inc., Tekran Instruments Corporation. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Mercury Analyzer Meter Market is characterized by a continuous drive toward enhanced sensitivity, speed, and automation to meet increasingly stringent regulatory limits. The two foundational technologies are Cold Vapor Atomic Absorption Spectrometry (CVAAS) and Cold Vapor Atomic Fluorescence Spectrometry (CVAFS). CVAAS remains a robust, cost-effective standard for routine analysis, relying on measuring the absorption of specific wavelengths of light by gaseous mercury atoms. However, CVAFS represents the modern frontier, utilizing fluorescence measurement, which significantly reduces background noise and offers detection limits orders of magnitude lower than CVAAS, making it the preferred method for ultra-trace environmental and biological sample analysis required under new Minamata guidelines.

A crucial technological innovation is Direct Combustion Analysis, or Thermal Decomposition, which eliminates the need for extensive sample preparation through chemical digestion. This technique involves heating the sample in an oxygen stream to release mercury vapor, which is then measured, significantly reducing analysis time and minimizing the risk of contamination from reagents. Furthermore, advancements in sensor technology, particularly miniaturized electrochemical sensors and optical sensors utilizing microchip technology, are enabling the creation of compact, portable, and continuous online monitoring systems. These portable devices are essential for rapid field screening and monitoring applications where laboratory-grade precision is not required but quick, reliable data is crucial for initial assessments.

Integration of software and data connectivity is another dominant trend. Modern mercury analyzers feature sophisticated control software that automates calibration, manages complex sample sequences, and integrates with Laboratory Information Management Systems (LIMS). Cloud connectivity and IoT capabilities are becoming standard, facilitating remote diagnostics, secure data archiving, and real-time alerts for compliance breaches, particularly important for Continuous Emission Monitoring Systems (CEMS) installed in large industrial plants. Future technological development is heavily focused on improving selective preconcentration techniques, such as enhanced gold amalgamation traps, and developing reagent-free analysis methods to lower operational costs and environmental impact associated with chemical usage.

The global Mercury Analyzer Meter Market exhibits distinct regional consumption and growth patterns, heavily influenced by local regulatory maturity and industrial concentration. North America, specifically the United States and Canada, holds a substantial market share, primarily driven by long-standing, rigorous environmental policies, high public awareness regarding mercury toxicity, and mandated monitoring requirements across various sectors, including power generation and wastewater treatment. The Environmental Protection Agency (EPA) regulations necessitate the use of highly accurate and certified instruments, ensuring sustained demand for high-end benchtop and CEMS units. Innovation is robust in this region, with high adoption rates for advanced CVAFS technology and automated systems.

Europe represents another mature and technologically demanding market, underpinned by EU directives such as the Water Framework Directive and national implementation of the Minamata Convention goals. Western European countries demonstrate high demand for both environmental monitoring and clinical analysis due to comprehensive public health systems and well-established environmental surveillance networks. Regulatory consistency and the prioritization of sustainable development initiatives ensure a stable, albeit slower, growth rate than in developing regions. Furthermore, the European market is a key early adopter of advanced data processing and automation technologies integrated into analyzer platforms.

The Asia Pacific (APAC) region is forecasted to be the engine of market growth throughout the forecast period. Rapid industrialization, particularly in China, India, and Southeast Asia, has resulted in high levels of mercury release from coal power, artisanal mining, and industrial manufacturing, necessitating urgent action. Governments in these nations are increasingly dedicating large budgets toward environmental cleanup and monitoring infrastructure to meet international commitments, translating directly into high volume procurement of mercury analyzers, including both cost-effective portable units for wide deployment and high-end CEMS for industrial stack monitoring. This region's growth is predominantly volume-driven, coupled with significant foreign investment in analytical infrastructure development.

Latin America and the Middle East & Africa (MEA) currently represent smaller but rapidly expanding markets. In Latin America, the market is driven primarily by mining activities (especially gold mining, which uses mercury) and the need for water quality monitoring. Regulatory frameworks are developing, creating demand for robust, field-ready instruments. The MEA region's growth is linked to the expansion of the oil and gas sector and new infrastructure development projects, necessitating basic safety and environmental compliance monitoring, driving demand for reliable, albeit often entry-level, analyzer technology.

The primary driver is the global implementation of stringent environmental regulations, particularly the Minamata Convention on Mercury, which mandates ultra-low detection limits for mercury emissions and releases (often in the ppt range), necessitating the widespread adoption of highly sensitive technologies like Cold Vapor Atomic Fluorescence Spectrometry (CVAFS) for accurate compliance monitoring and human health assessment.

Benchtop units are laboratory instruments designed for maximal precision, high sample throughput, and certified regulatory compliance testing, typically utilizing CVAAS or CVAFS. Portable analyzers are designed for rapid, real-time screening in the field (e.g., soil surveys, hazardous material spills, initial site assessment), offering speed and mobility over absolute laboratory-grade precision.

The Asia Pacific (APAC) region is anticipated to exhibit the fastest growth. This is due to accelerated industrial development (power generation, manufacturing) leading to high pollution levels, combined with increasing governmental investments in environmental infrastructure and regulatory enforcement to meet international commitments like the Minamata Convention.

The shift towards integrated Continuous Emission Monitoring Systems (CEMS) incorporating direct combustion/thermal decomposition and automated data analysis (often supported by AI) is a major technological advancement. This allows industrial facilities to monitor mercury emissions in real time, minimize sample preparation, and ensure immediate compliance reporting with minimal human intervention.

The key restraints include the high initial capital investment required for purchasing high-end, complex instruments (CVAFS, CEMS), the substantial operational costs associated with specialized consumables and reagents, and the critical need for highly skilled technical personnel to operate, calibrate, and maintain these precise analytical systems.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.