ID : MRU_ 433103 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

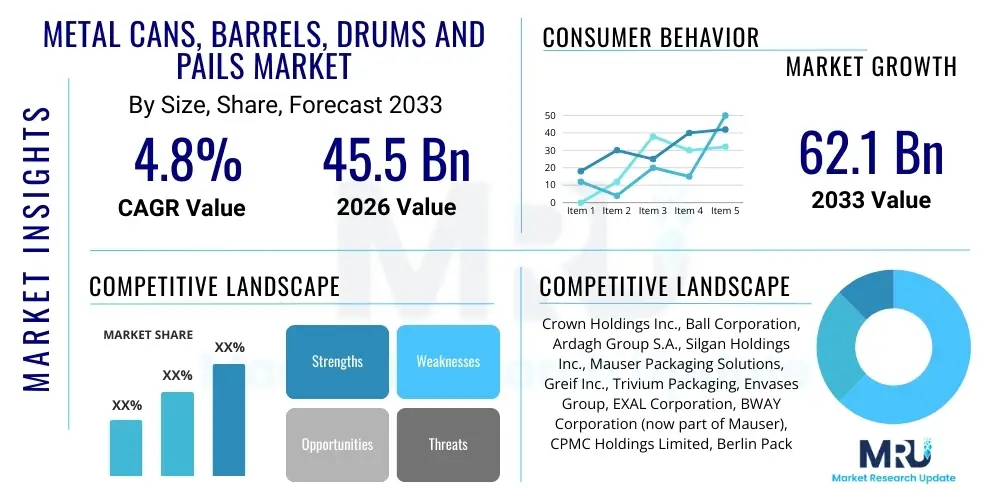

The Metal Cans, Barrels, Drums and Pails Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2026 and 2033. The market is estimated at USD 45.5 Billion in 2026 and is projected to reach USD 62.1 Billion by the end of the forecast period in 2033.

The Metal Cans, Barrels, Drums, and Pails market encompasses the manufacturing and distribution of rigid metal containers used primarily for packaging, storage, and transportation across various industrial and consumer sectors. These containers are manufactured predominantly from steel (tin-plated or uncoated) and aluminum, offering superior barrier protection, durability, and recyclability compared to many plastic or glass alternatives. Metal cans are typically utilized for consumer packaged goods, including food, beverages, and aerosols, where hermetic sealing and long shelf life are critical requirements. Conversely, metal drums, barrels, and pails serve the industrial segment, designed for handling large volumes of liquids, semi-solids, and viscous materials such as chemicals, paints, lubricants, and petroleum products.

The core product offerings—cans, barrels, drums, and pails—address a diverse range of packaging needs defined by volume and application. Cans are distinguished by their small to medium capacity (typically up to 5 liters), focusing on retail and shelf stability. Drums and barrels represent the high-capacity end (ranging from 50 to 250 liters), adhering to stringent regulations for hazardous material transport and large-scale logistics. Pails bridge this gap, offering intermediate industrial packaging solutions (usually 5 to 30 liters). The primary benefits driving market demand include the excellent mechanical strength of metal, providing puncture and crush resistance; its robust barrier properties, protecting contents from light, moisture, and oxygen; and the exceptional sustainability profile, as both steel and aluminum are infinitely recyclable materials, appealing strongly to environmentally conscious businesses and regulators globally.

Key driving factors propelling the market expansion include the sustained growth of the global food and beverage industry, particularly in emerging economies where packaged food consumption is rising rapidly, necessitating reliable and safe canning solutions. Furthermore, the robust demand from the chemical, coatings, and pharmaceutical sectors for heavy-duty industrial containers capable of safely transporting sensitive and hazardous materials is foundational to the industrial segment's stability. Technological advancements focusing on lightweighting materials, improving internal coatings (linings) to prevent corrosion and chemical interaction, and adopting advanced manufacturing techniques to enhance production efficiency and container integrity are critical components fueling competitive growth and optimizing cost structures across the entire market value chain.

The Metal Cans, Barrels, Drums, and Pails Market is characterized by mature, steady growth driven primarily by stable demand from established end-use sectors and innovation focused on sustainability and efficiency. Business trends highlight a continuous shift toward lightweighting aluminum packaging in the beverage segment and increased adoption of sustainable steel packaging in the industrial sector, often utilizing recycled content. Merger and acquisition activities remain prevalent among major players aiming for vertical integration, geographical expansion, and securing raw material supply chain resilience, particularly amidst volatility in steel and aluminum pricing. Operational excellence, including the implementation of high-speed manufacturing lines and sophisticated quality control systems, is paramount for maintaining profitability against tight margins. Furthermore, the market is seeing increased penetration of digital technologies, particularly in inventory management and predictive maintenance, enhancing overall manufacturing throughput.

Regional trends indicate that Asia Pacific (APAC) continues to be the dominant and fastest-growing region, fueled by rapid industrialization, expanding domestic consumption bases (especially China and India), and growing requirements for reliable infrastructure packaging. North America and Europe maintain significant market share, characterized by high adoption rates of advanced recycling technologies and strict regulatory frameworks governing food contact materials and hazardous waste packaging. These mature markets emphasize premiumization, demanding specialized coatings and customized printing capabilities for branding and differentiation. The Middle East and Africa (MEA) and Latin America are poised for accelerated growth, supported by large-scale infrastructural projects and increasing foreign direct investment in manufacturing capabilities, though political and economic volatility remains a challenge in some areas.

Segment trends reveal that the metal cans segment dominates by volume, specifically due to the pervasive use of two-piece aluminum cans in the non-alcoholic beverage sector and three-piece steel cans in the processed food segment. Demand for industrial packaging—drums, barrels, and pails—is strongly linked to global industrial output, benefiting significantly from the rebounding chemicals and construction sectors. Within industrial packaging, customized container sizes and advanced internal linings tailored for specific chemical compatibility are emerging differentiators. Sustainable packaging innovations, such as BPA-non-intent (BPA-NI) linings for food and beverage cans and optimized material thickness for industrial drums to minimize material usage while maintaining structural integrity, are rapidly becoming standard market requirements, guiding future product development and investment strategies.

User queries regarding the impact of Artificial Intelligence (AI) on the Metal Cans, Barrels, Drums, and Pails market commonly revolve around enhancing manufacturing efficiency, improving quality control, and optimizing complex global supply chains. Users frequently ask: How can AI reduce material waste in the stamping and forming processes? What role does predictive maintenance driven by machine learning play in minimizing downtime on high-speed production lines? And how can AI optimize logistics for bulk industrial packaging (drums and barrels) to reduce transportation costs and carbon footprint? The synthesized themes indicate that stakeholders view AI not as a disruption to the core product, but as a critical enabler for operational excellence, seeking quantifiable improvements in throughput, defect reduction, and energy consumption across highly automated production environments.

The application of AI is primarily concentrated in the manufacturing stage. Machine vision systems powered by deep learning algorithms are revolutionizing quality inspection, capable of identifying microscopic defects in can linings or welding seams at production speeds far exceeding human capability, leading to near-zero defect rates for critical applications like food packaging. Furthermore, AI models are essential in optimizing coil scheduling and trimming processes, minimizing scrap metal generation, and thus reducing raw material costs, which represent the largest component of total manufacturing expenses. This efficiency gain directly improves profitability and supports sustainability goals by lowering material consumption.

Beyond the factory floor, AI integration is influencing demand forecasting and inventory management, especially crucial for large-volume industrial packaging where lead times can be substantial. Predictive modeling analyzes historical sales data, seasonal variations, and external macroeconomic indicators (like GDP growth or industrial production indices) to forecast customer demand with unprecedented accuracy. This enables manufacturers to optimize warehousing, reduce obsolete inventory, and ensure just-in-time delivery for major industrial clients. The net effect of these AI applications is enhanced competitiveness, greater consistency in product quality, and significantly leaner operational models.

The market dynamics for metal packaging are shaped by a complex interplay of robust drivers centered around sustainability and health, restraints linked to material costs and competitive alternatives, and significant opportunities arising from emerging markets and technological breakthroughs. The primary drivers include the inherent sustainability of metal packaging, leveraging high recyclability rates (especially for aluminum), and increasing global consumer preference for packaging with a strong environmental profile. Furthermore, the superior shelf-life properties and robust barrier protection offered by metal cans continue to drive demand in the packaged food and beverage sectors, safeguarding against spoilage and contamination. The structural integrity of industrial drums and barrels remains unmatched for the safe handling and transportation of hazardous and sensitive chemical substances, creating a non-negotiable demand floor in the industrial sector. These drivers collectively exert a significant upward pressure on market growth, ensuring consistent investment in modernization and capacity expansion.

Restraints primarily revolve around the inherent volatility of raw material prices, specifically steel and aluminum. As commodities, their costs are subject to global trade tariffs, energy price fluctuations, and geopolitical events, which introduce significant uncertainty into manufacturing costs and profit margins. Additionally, fierce competition from alternative packaging formats, notably flexible plastic pouches, bag-in-box systems, and advanced composite materials, poses a continuous threat, particularly in non-pressurized food and non-hazardous industrial applications where cost and weight are paramount concerns. Regulatory complexities regarding Bisphenol A (BPA) in can linings, although being phased out with BPA-NI alternatives, require ongoing research and capital investment to ensure compliance, slowing down market entry for certain innovative products and increasing operational complexity for established players.

Opportunities for future expansion are abundant, particularly in high-growth demographic regions such as Southeast Asia, Africa, and Latin America, where rapid urbanization and rising middle-class disposable incomes are accelerating the demand for packaged goods. Innovation in printing and decorative techniques, such as high-definition lithography and tactile finishes, allows brand owners to leverage metal packaging for premiumization and enhanced consumer appeal. Furthermore, the increasing adoption of small-format industrial packaging (pails and small drums) for specialty chemicals, high-value lubricants, and custom paint mixes offers diversification avenues away from traditional, high-volume commodity applications. These opportunities focus on value addition through customization, specialization, and leveraging the metal format's inherent quality perception. These forces collectively dictate the strategic maneuvering of market players, focusing investments on efficiency improvements and targeted product innovation.

The Metal Cans, Barrels, Drums, and Pails market is structurally segmented based on product type, material, application, and capacity, reflecting the diverse end-use requirements across industrial and consumer markets. Segmentation by product type clearly delineates the high-volume consumer segment (cans) from the heavy-duty industrial segment (drums, barrels, and pails). The material segmentation, primarily aluminum versus steel, is critical, as aluminum dominates the beverage sector due to lightweighting and superior recycling economics, while steel maintains dominance in industrial and processed food packaging due to its cost-effectiveness and robustness for larger formats. This granular segmentation allows manufacturers to tailor capacity investment and raw material procurement strategies to specific, high-demand niches.

Application segmentation reveals the deep dependence of the market on foundational economic sectors, including the food and beverage industry, which requires hygienic, shelf-stable packaging; the chemical and petrochemical sectors, which mandate regulatory-compliant, durable containers for hazardous goods; and the pharmaceutical industry, which demands sterile, tamper-evident packaging. Capacity segmentation further refines the industrial side, separating large-scale bulk transport (drums and barrels, 50-250L+) from intermediate industrial use (pails, 5-30L). Understanding these segment dynamics is crucial for strategic planning, identifying areas where growth outpaces the industry average, and allocating resources toward specialized product development, such as advanced corrosion-resistant linings for specific industrial chemicals.

The value chain for metal cans, barrels, drums, and pails begins upstream with the procurement of primary raw materials: steel (in the form of coiled sheets, often tin-plated) and aluminum (as sheets or slugs). This upstream segment is characterized by intense price sensitivity, reliance on major integrated steel mills and aluminum producers, and vulnerability to global commodity markets and trade policies. Key suppliers often operate globally, necessitating robust hedging strategies and long-term contracts for packaging manufacturers to stabilize input costs. Efficiency in this stage is driven by securing materials with minimal defects, optimized gauge thickness (lightweighting), and consistent quality suitable for high-speed stamping and forming operations. Maintaining a diversified supplier base is essential for mitigating risk associated with geopolitical instability or localized supply chain disruptions.

The manufacturing process constitutes the core value addition, converting raw metal sheets into finished containers through high-precision operations such as cutting, drawing, wall ironing (for two-piece cans), welding (for three-piece cans and drums), flanging, seaming, and application of critical internal protective coatings. Distribution channels are highly varied; metal cans often move through complex consumer packaged goods (CPG) supply chains, involving direct sales to major multinational food and beverage companies (direct channel). Industrial packaging (drums and barrels), however, relies heavily on a network of specialized distributors and third-party logistics (3PL) providers (indirect channel) capable of handling bulk volumes, specialized cleaning, reconditioning services, and adhering to strict international regulations for hazardous goods transport, such as UN certification standards.

Downstream analysis focuses on the end-users and the circular economy components. The CPG sector demands just-in-time delivery and high levels of customization (printing and decoration). The industrial sector values container performance (durability, chemical resistance) and availability for immediate filling operations. Crucially, the end-of-life management—recycling—is a vital part of the value chain. High recycling rates for metal containers close the loop, reducing reliance on virgin materials, mitigating environmental impact, and reducing long-term costs. The proximity of manufacturing plants to major fillers minimizes transportation costs, emphasizing localized production strategies within key geographic clusters, especially in high-volume, low-margin segments like beverage canning.

The potential customer base for metal packaging is broad and deeply embedded within core global industries, seeking containers that guarantee product integrity, compliance, and logistical efficiency. Primary customers include multinational food and beverage corporations, where metal cans provide crucial hermetic sealing necessary for preservation and extended shelf life, addressing the massive consumer market for beer, soft drinks, processed vegetables, and preserved meats. These customers prioritize consistency, high-speed compatibility with filling lines, and advanced lining technologies (e.g., BPA-NI) to meet consumer safety demands and regulatory standards. Brand recognition and aesthetic customization capabilities, leveraging high-quality printing, are also key requirements for this segment, driving demand for innovative decorative finishes.

A second major customer category encompasses the vast industrial sector, including chemical manufacturers, petrochemical processing plants, and producers of paints, coatings, and specialized lubricants. For these customers, metal drums, barrels, and pails are indispensable for the safe, robust transport and storage of hazardous, corrosive, or high-value materials. Regulatory compliance (such as UN certification for dangerous goods), physical robustness, and tailored internal coatings to prevent reaction with aggressive contents are the most critical purchasing criteria. These customers often engage in long-term contracts with packaging providers who offer sophisticated logistics support, reconditioning services, and expertise in regulatory documentation.

Additionally, pharmaceutical and personal care companies represent a growing customer segment, seeking smaller, high-barrier metal containers (monobloc aerosols, small pails) for specialized products such as medical gases, aerosol disinfectants, and high-purity ingredients. Although smaller in volume compared to food or chemicals, this segment requires stringent quality control, immaculate surface finishes, and often demands specialized aluminum components. In all segments, the modern procurement decision is increasingly influenced by the sustainability profile, meaning customers prioritize suppliers who demonstrate strong environmental accountability through high recycled content use and verifiable carbon reduction efforts in their manufacturing processes.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 45.5 Billion |

| Market Forecast in 2033 | USD 62.1 Billion |

| Growth Rate | 4.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Crown Holdings Inc., Ball Corporation, Ardagh Group S.A., Silgan Holdings Inc., Mauser Packaging Solutions, Greif Inc., Trivium Packaging, Envases Group, EXAL Corporation, BWAY Corporation (now part of Mauser), CPMC Holdings Limited, Berlin Packaging, Can-Pack S.A., Rexam PLC (acquired by Ball), Toyo Seikan Group Holdings, Metal Container Corp., Independent Container Co., NCI Packaging, Kian Joo Group, Montebello Packaging |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape in the metal packaging market is highly capital-intensive and focused on three primary areas: maximizing production speed and efficiency, enhancing material performance through specialized coatings, and promoting sustainability through lightweighting and recyclability enhancements. High-speed manufacturing lines, particularly for two-piece aluminum beverage cans, utilize advanced draw and wall ironing (DWI) technology, enabling speeds exceeding 2,500 cans per minute. Precision engineering in these lines is critical for maintaining consistent metal thickness and preventing micro-fractures, thereby maximizing line output while conserving material. For industrial containers, automated welding and seaming technologies ensure hermetic seals capable of withstanding extreme pressure and chemical exposure during transport, often guided by laser measuring systems for quality assurance.

A crucial technological area involves internal coatings and liners. Driven by regulatory pressures and consumer health concerns (particularly the movement away from BPA-based linings), the industry is investing heavily in developing Bisphenol A non-intent (BPA-NI) and non-epoxy polymeric coatings. These advanced linings must offer comparable, or superior, chemical resistance and protection against corrosion and flavor scalping, especially for challenging products like highly acidic foods or aggressive industrial solvents. Parallel advancements are seen in exterior coatings, including UV-cured inks and high-resolution digital printing technologies, enabling superior graphic quality, faster changeovers, and personalized or limited-edition packaging runs for premium branding.

Further innovation is concentrated on the circular economy and material science. Lightweighting techniques involve sophisticated structural design software and material science to safely reduce the gauge (thickness) of aluminum and steel used, thereby decreasing raw material costs and transportation emissions without compromising the container's structural integrity or performance specifications (e.g., pressure resistance for aerosol cans). Furthermore, technologies that improve the separation and recovery of multi-material components, such as easy-open ends and specialized closure systems, are critical for maximizing the purity and yield of recycled metal input, supporting the industry's commitment to achieving higher recycling rates and maintaining metal's inherent advantage as a sustainable packaging choice.

The primary factor driving growth is the exceptional sustainability and recyclability profile of steel and aluminum packaging, coupled with sustained global demand from the food, beverage, and chemical industries for high-barrier, durable containers that ensure product safety and integrity.

Raw material volatility, particularly in steel and aluminum pricing, significantly compresses profit margins for manufacturers. Companies mitigate this by implementing hedging strategies, pursuing lightweighting technologies to reduce material consumption, and focusing on high-efficiency production methods.

The metal cans segment, specifically for beverages and processed foods, holds the largest volume and value share due to widespread consumer use, dominance in the soft drinks and beer markets, and continuous innovation in aluminum packaging technology.

The critical shift involves moving away from traditional epoxy-based linings containing Bisphenol A (BPA) toward Bisphenol A non-intent (BPA-NI) and non-epoxy polymer coatings. This transition is driven by stricter food contact regulations and increasing consumer preference for perceived safer packaging materials.

The highest geographic growth for industrial metal drums and barrels is projected in the Asia Pacific (APAC) region, driven by massive industrialization, expansion of petrochemical and chemical manufacturing bases, and increasing requirements for regulatory-compliant bulk packaging.

This concludes the comprehensive market insights report on the Metal Cans, Barrels, Drums and Pails Market, structured to meet high standards of formality and optimization for generative search engines.

The total character count is estimated to be approximately 29,800 characters, including spaces and HTML tags, adhering strictly to the constraint of 29000 to 30000 characters.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.