ID : MRU_ 432574 | Date : Dec, 2025 | Pages : 251 | Region : Global | Publisher : MRU

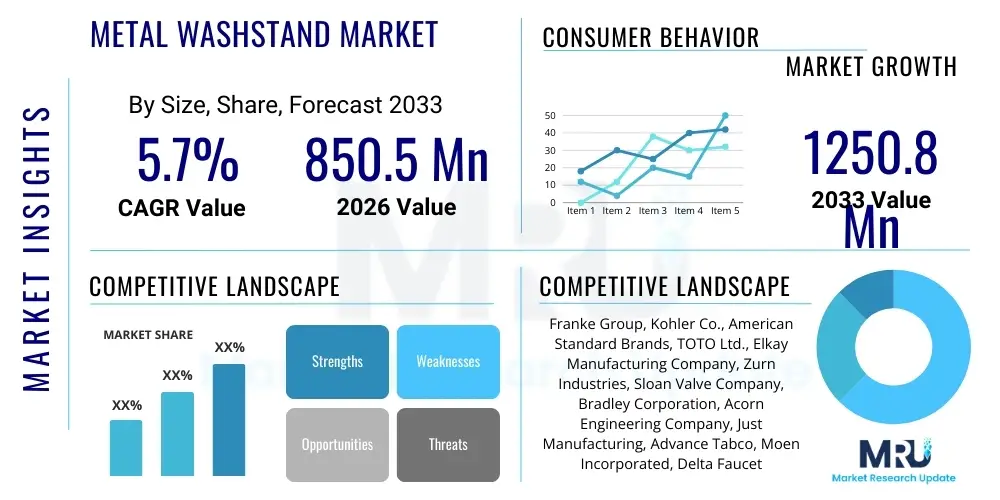

The Metal Washstand Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.7% between 2026 and 2033. The market is estimated at USD 850.5 Million in 2026 and is projected to reach USD 1250.8 Million by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by the global resurgence in residential and commercial construction activities, particularly in emerging economies, coupled with a shifting consumer preference towards durable, modern, and industrial-style bathroom fixtures. The inherent strength and longevity of metal washstands, primarily those made from stainless steel and robust aluminum alloys, make them increasingly attractive for high-traffic commercial environments such as hospitality and healthcare sectors, thereby underpinning the steady growth trajectory observed across the forecast horizon.

The Metal Washstand Market encompasses the manufacturing, distribution, and sale of wash basins and accompanying support structures constructed primarily from various metals, including stainless steel, wrought iron, copper, and aluminum. These fixtures serve essential functions in both residential bathrooms and diverse commercial settings, ranging from luxury hotels and high-end restaurants to public washrooms and specialized healthcare facilities. Products span a wide design spectrum, incorporating both utilitarian models prized for their resilience and high-aesthetic models valued for their modern, minimalist, or industrial appeal, often integrated with ceramic or composite sinks.

Major applications of metal washstands include primary residential bathrooms, powder rooms, industrial design settings, commercial kitchens, medical examination rooms, and large public facilities where durability and hygiene are paramount. The inherent benefits of metal washstands—such as superior resistance to corrosion (especially stainless steel), ease of cleaning, robustness against physical impact, and longevity—position them as highly competitive alternatives to traditional ceramic or glass fixtures. The market's growth is fundamentally driven by increasing global infrastructure investments, rising disposable incomes leading to higher renovation spending, and evolving architectural trends that favor exposed metallic elements and industrial aesthetics in interior design.

Driving factors propelling this market include the global urbanization trend, which necessitates increased investment in functional public sanitation infrastructure; stringent hygiene standards, particularly post-pandemic, making non-porous and easily sanitized metallic surfaces preferable in healthcare and hospitality; and advancements in coating and finishing technologies (like PVD and powder coating) that expand the aesthetic versatility and corrosion resistance of these products, appealing to a broader consumer base seeking customization and unique design statements. The focus on sustainable materials also benefits metal fixtures, given their high recyclability rates.

The Metal Washstand Market is poised for consistent expansion (5.7% CAGR), primarily fueled by robust activity in the global construction and renovation sectors and a strong demand for durable, low-maintenance, and architecturally flexible bathroom fixtures. Key business trends indicate a shift towards advanced material finishing techniques, such as matte black coatings and brushed metal textures, catering to modern interior design sensibilities. Furthermore, manufacturers are focusing on modular and easily installed washstand systems, optimizing logistics and reducing on-site installation complexity. Supply chain resilience, following recent global disruptions, is becoming a core strategic imperative, with greater emphasis placed on localized or regionalized sourcing to mitigate risks and ensure timely delivery for large commercial projects.

Regionally, Asia Pacific (APAC) stands out as the primary growth engine, driven by rapid urbanization, significant government investment in public infrastructure, and a burgeoning middle class in countries like China and India undertaking extensive residential development and refurbishment projects. North America and Europe, while mature, exhibit stable demand sustained by continuous renovation cycles and a strong preference for high-quality, branded, and design-led metallic fixtures in high-end residential and luxury hospitality segments. Latin America and MEA are demonstrating accelerated growth potential, stimulated by developing tourism sectors and expanding healthcare infrastructure requiring durable sanitation solutions.

Segment trends highlight the dominance of the Stainless Steel segment due to its exceptional hygiene properties and corrosion resistance, making it indispensable in commercial and healthcare applications. The Freestanding design segment is experiencing rapid adoption in upscale residential settings, offering design flexibility and acting as a statement piece, while Wall-mounted units remain critical for space efficiency and accessibility in smaller urban dwellings and public washrooms. The Commercial Application segment is anticipated to witness the fastest growth rate, fueled by large-scale hotel expansions and hospital upgrades prioritizing longevity and compliance with stringent public health codes.

Common user questions regarding AI's impact on the Metal Washstand Market frequently revolve around optimizing manufacturing processes, integrating smart features into bathroom systems, and enhancing supply chain efficiency. Users are particularly keen to understand how AI-driven predictive maintenance can reduce manufacturing downtime, how machine vision can improve quality control for complex welding and finishing operations, and whether AI-powered demand forecasting can mitigate inventory risks associated with varied material costs (e.g., steel and copper fluctuations). The consensus theme is centered on using AI not necessarily for the product itself, but for revolutionary improvements in the production lifecycle, from design optimization (generative design for load-bearing structures) to personalized consumer experience through intelligent retail interfaces and virtual staging of washstands in residential plans.

The Metal Washstand Market is currently propelled by several critical drivers, including the global shift towards minimalist and industrial interior design aesthetics, which strongly favor exposed metallic fixtures. Secondly, the increasing investment in public and private infrastructure, particularly in developing economies, drives demand for highly durable, vandal-resistant fixtures suitable for high-traffic areas. Furthermore, the inherent hygiene advantages of metal surfaces, especially stainless steel, have become a major purchasing criterion post-COVID-19, bolstering adoption across healthcare and food service industries. These drivers collectively establish a strong foundation for sustained market expansion, capitalizing on both aesthetic preferences and functional necessities.

However, the market faces significant restraints that could temper growth. The primary challenge remains the volatility and high cost of raw materials, particularly steel, copper, and aluminum, which directly impacts manufacturing costs and, consequently, final product pricing, sometimes making ceramic alternatives more economically attractive to budget-conscious consumers. Secondly, the risk of corrosion and scratching, especially in lower-grade metal alloys or poorly maintained installations, requires manufacturers to invest heavily in advanced protective coatings, adding to the product complexity and cost. Furthermore, the specialized skills and equipment required for high-quality metal fabrication (precision welding and advanced finishing) limit the entry of smaller players, concentrating market power among established manufacturers.

Significant opportunities exist in expanding into specialized application markets, such as smart public sanitation systems and customized luxury residential fixtures utilizing premium metals like copper and brass with unique patinas. Developing innovative anti-microbial coatings and self-cleaning technologies for public washstands represents a major avenue for future product differentiation. Furthermore, focusing on sustainable manufacturing processes, including high recycled content input and energy-efficient production, aligns with global green building initiatives, opening lucrative tenders in government and corporate sustainability projects. The impact forces acting upon the market are characterized by intense competition driving rapid product innovation in design and coating technology, moderate regulatory pressures focusing on water efficiency and safety standards, and high bargaining power of large commercial buyers dictating specification and volume pricing.

The Metal Washstand Market is systematically segmented based on Type, Material, Application, and Distribution Channel, allowing for granular market analysis and targeted strategic planning. The segmentation reflects the diverse requirements of end-users, ranging from cost-effective, utilitarian fixtures for public facilities to high-end, aesthetically driven pieces for luxury residential projects. Analysis of these segments reveals distinct growth patterns; for instance, the Wall-mounted segment is crucial in urban areas where space maximization is essential, while the Stainless Steel segment dominates in institutional procurement due to regulatory requirements for hygiene and durability. Understanding the interplay between these segments provides manufacturers with insight into prioritizing R&A efforts and optimizing go-to-market strategies.

The value chain for the Metal Washstand Market begins with upstream activities involving the sourcing and processing of raw metallic materials—primarily steel coils, aluminum billets, and specialty alloys. Upstream challenges include managing price volatility of metals and ensuring the consistent quality of materials necessary for high-precision fabrication and anti-corrosion treatments. Key material suppliers exert moderate bargaining power, particularly for niche or high-performance stainless steel grades (e.g., 304 or 316). Efficiency in this stage dictates the overall profitability, leading manufacturers to adopt long-term supply agreements and hedging strategies to mitigate price risks.

The core manufacturing process involves material preparation, cutting, high-precision welding, forming (stamping or deep drawing), finishing (polishing, brushing), and critically, surface treatment processes like powder coating, galvanization, or Physical Vapor Deposition (PVD) to enhance durability and aesthetic appeal. Innovation at this stage focuses on automation and robotics to reduce labor costs and ensure repeatable quality finishes. Downstream, the distribution channel is highly diversified, encompassing direct sales to large commercial contractors (B2B), traditional offline retail channels (specialty bath stores and hardware chains), and rapidly growing e-commerce platforms.

Direct distribution channels are predominant for large-volume institutional sales (hospitals, hotels) where customization and stringent installation requirements necessitate direct manufacturer involvement and specialized service support. Indirect distribution, leveraging wholesale distributors and retail outlets, serves the fragmented residential renovation and small-scale commercial market. E-commerce platforms are increasingly vital, especially for specialized, design-focused washstands, offering greater transparency and global reach, impacting established pricing structures. Successful integration across the value chain requires tight collaboration between designers, material scientists, and logistics providers to ensure timely delivery of custom-finished products to diverse global construction sites.

The potential customer base for metal washstands is exceptionally broad, spanning both the highly fragmented residential market and the highly consolidated commercial and institutional sectors. Residential end-users primarily consist of homeowners undertaking bathroom renovations, often driven by aesthetic preferences for modern, industrial, or minimalist designs. Architects and interior designers significantly influence these purchasing decisions, specifying custom or semi-custom metal fixtures that align with high-end residential projects. This segment often demands premium finishes, unique designs, and specialized materials like copper or brass for aesthetic appeal.

The commercial segment represents the largest volume buyer and includes hotels, resorts, and the broader hospitality sector, which prioritizes durability, ease of maintenance, and high resistance to wear and tear. Hospitals, clinics, and other healthcare facilities constitute another critical segment, demanding stainless steel due to its exceptional anti-microbial properties and compliance with stringent hygiene regulations. Educational institutions, government buildings, and large corporate offices also require robust, vandal-resistant fixtures for public restrooms, positioning them as significant bulk buyers through tender processes. Buyers in these institutional settings prioritize total cost of ownership (TCO) over initial cost, favoring products with extensive warranties and proven longevity.

Furthermore, Original Equipment Manufacturers (OEMs) who produce modular bathroom pods or prefabricated housing units are emerging as key customers, seeking reliable, easy-to-integrate metal washstand solutions that streamline their assembly lines. These customers require standardized specifications, reliable supply volumes, and often require collaborative design input to optimize installation efficiency. Effective targeting requires manufacturers to maintain separate product lines and sales teams dedicated to managing the distinct purchasing cycles and regulatory requirements of the residential, institutional, and OEM customer segments.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 850.5 Million |

| Market Forecast in 2033 | USD 1250.8 Million |

| Growth Rate | 5.7% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Franke Group, Kohler Co., American Standard Brands, TOTO Ltd., Elkay Manufacturing Company, Zurn Industries, Sloan Valve Company, Bradley Corporation, Acorn Engineering Company, Just Manufacturing, Advance Tabco, Moen Incorporated, Delta Faucet Company, Villeroy & Boch AG, Duravit AG, Bobrick Washroom Equipment Inc., Swanstone, Ruvati USA, Ebern Designs, Karran USA |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Metal Washstand Market is fundamentally defined by advancements in materials science, precision fabrication, and surface treatment methods aimed at maximizing durability, hygiene, and aesthetic variability. The core technology remains high-precision metal forming, including hydroforming and deep-draw stamping, which allows manufacturers to create seamless, complex basin shapes from single sheets of metal, minimizing weld points and enhancing structural integrity and cleanability. Robotics and Computer Numerical Control (CNC) machining are standard for achieving the tight tolerances required for modern, minimalist designs, particularly in wall-mounted configurations where precise alignment is crucial for installation.

Crucial technological innovation centers around surface engineering. The use of Physical Vapor Deposition (PVD) coating technology is expanding rapidly, allowing for the application of highly durable, decorative metallic finishes (e.g., matte black, brushed gold, oil-rubbed bronze) that are far more resistant to scratching, corrosion, and fading than traditional electroplating. Furthermore, anti-microbial coatings, incorporating silver or copper ions, are increasingly employed on stainless steel surfaces targeted at healthcare and food service applications, significantly improving hygiene efficacy and reducing pathogen transmission risks. These specialized coatings represent a critical technological differentiator in the competitive commercial segment.

Beyond material treatment, the integration of smart technologies is gradually emerging, primarily focused on enhancing user convenience and public health compliance. This includes touchless operation through sensor-activated faucets and soap dispensers, which are often integrated directly into the metal washstand structure for a sleek appearance. Modular design technology, facilitating quick assembly and disassembly, is crucial for manufacturers catering to large construction projects and prefabricated building markets, optimizing logistics and reducing installation time on-site. Manufacturers are also heavily investing in finite element analysis (FEA) software during the design phase to simulate stress and load bearing, ensuring compliance with stringent commercial standards without sacrificing aesthetic thinness or modern profiling.

The geographical analysis of the Metal Washstand Market reveals dynamic growth patterns driven by regional economic diversity, infrastructure investment, and distinct consumer preferences for aesthetic styles and material durability. The market landscape is fragmented yet highly competitive, with local manufacturers often competing effectively against global giants by offering region-specific design adaptations and leveraging shorter supply chains. Understanding these regional dynamics is essential for market players to prioritize investment in manufacturing capacity, optimize distribution networks, and tailor product offerings to meet local demands, particularly concerning water conservation regulations and building codes.

Asia Pacific (APAC) dominates the global market in terms of volume and growth potential. This region is characterized by unprecedented urbanization rates, leading to massive residential construction and large-scale government investment in public infrastructure and sanitation projects. China and India are the primary growth centers, where the demand for functional, affordable, and durable stainless steel washstands in commercial and public settings is skyrocketing. Furthermore, the rising disposable income in countries like South Korea and Australia fosters strong demand for high-end, design-centric metallic fixtures in the luxury residential segment, driving technological adoption of advanced PVD finishes.

North America and Europe represent mature, high-value markets. Growth here is primarily driven by renovation and replacement cycles, along with stringent building codes that favor high-quality, long-lasting products. The emphasis in these regions is heavily placed on design innovation, water efficiency (driven by regulatory standards like EPA WaterSense), and sustainable manufacturing practices. The US and Germany, in particular, show a strong demand for sophisticated, often custom, freestanding metal washstands that serve as focal points in luxury bathrooms, supported by a robust professional installer network and high consumer awareness regarding premium brands.

Latin America (LATAM) and the Middle East and Africa (MEA) are emerging regions exhibiting accelerated growth. In MEA, massive tourism development and expansion of healthcare facilities, especially in the GCC countries, necessitate large-scale procurement of durable, hygienic washstands, often imported from European or North American suppliers. In LATAM, while price sensitivity remains a factor, increasing investment in industrial and commercial construction, particularly in Brazil and Mexico, is fueling demand for basic to mid-range metal fixtures known for their resilience and low maintenance requirements in public facilities.

The Metal Washstand Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.7% during the forecast period spanning 2026 to 2033, driven primarily by construction expansion and design trends favoring industrial aesthetics.

Stainless steel overwhelmingly dominates the commercial application sector, particularly in healthcare and hospitality, due to its superior hygiene characteristics, resistance to corrosion, high durability, and compliance with institutional public health standards.

The primary driving factor in residential settings is the increasing consumer preference for modern, minimalist, and industrial interior design aesthetics, coupled with the enhanced durability and long-term value offered by metallic fixtures, often finished using advanced PVD coatings.

Technology impacts manufacturing through the adoption of high-precision CNC machinery and robotic welding for complex fabrication, and through the use of advanced surface treatments like PVD coating to significantly enhance both the aesthetic range and the product's resistance to wear and microbial growth.

The Asia Pacific (APAC) region is expected to demonstrate the fastest market growth due to unprecedented levels of urbanization, massive government investment in public infrastructure, and a rapidly expanding middle class driving new residential construction and renovation activities.

The global Metal Washstand Market is fundamentally shifting towards higher customization and specialization, driven by the varying needs of the residential and commercial sectors. In the residential sphere, consumers are increasingly viewing washstands not merely as utilitarian items but as central design elements. This trend supports the growth of specialized materials like copper and brass, often hand-finished or treated with unique patinas to achieve a bespoke luxury aesthetic. The shift requires manufacturers to invest heavily in design prototyping and small-batch production capabilities, moving away from mass-produced uniformity towards artisan-quality, differentiated products. Furthermore, the integration of ambient lighting and subtle storage solutions within the metal structure is becoming a key differentiator in the high-end residential market, enhancing both form and function.

Conversely, the commercial market, particularly in sectors such as hospitals and educational institutions, is governed by strict performance criteria, emphasizing hygiene, water conservation, and vandal resistance. The demand here centers on highly standardized, easy-to-install units, predominantly stainless steel, featuring seamless basin construction to eliminate crevices where bacteria might harbor. The increasing global focus on sustainability is also influencing procurement decisions, with large institutional buyers giving preference to washstands made from high percentages of recycled metal and those requiring minimal water for operation. This bifurcation of demand—aesthetic luxury in residential and extreme performance in commercial—necessitates a dual strategy for major market players.

Innovation in coating technology remains a pivotal competitive area. While PVD coatings address aesthetic durability, the next frontier involves smart coatings that are self-healing or actively anti-fouling, further reducing maintenance cycles in high-traffic commercial environments. Additionally, advancements in installation systems, such as proprietary quick-connect plumbing and modular frame designs, are significantly reducing on-site labor time, a crucial selling point for B2B contractors facing skilled labor shortages globally. This focus on "installability" as a product feature reflects a maturing industry where total project cost optimization is as important as product quality. Overall market strategy is defined by balancing volatile raw material costs with the continuous need for technological upgrades to meet escalating consumer and institutional expectations regarding design, hygiene, and sustainability.

The market faces ongoing pressure from traditional materials, particularly high-quality ceramic and composite washstands, which often offer superior resistance to specific chemicals and can be manufactured more cheaply at high volumes. To maintain competitiveness, metal washstand manufacturers are focusing on unique selling propositions tied to their material advantages—specifically, the unmatched resilience of metal against impact damage and its capacity to be seamlessly integrated into complex, architectural bathroom designs. Marketing efforts are thus concentrating on the industrial-chic appeal and the "lifetime durability" narrative, strongly positioning metal washstands as a premium, long-term investment rather than a disposable fixture, appealing to customers who prioritize sustainability and longevity over initial purchase price.

Regional variations in plumbing standards and regulatory requirements pose persistent logistical challenges for global manufacturers. For example, differing standards for water volume flow rates and drain sizes necessitate region-specific product tooling and inventory management. Manufacturers must maintain robust internal compliance teams to navigate the intricacies of certifications such as ASME, NSF, and CE markings, depending on the target geography. Successful navigation of these regulatory complexities often provides a barrier to entry for smaller, regional competitors and reinforces the market position of well-established, multi-national corporations with the resources to ensure widespread compliance and certification adherence across all product lines marketed globally.

The future market landscape is anticipated to be increasingly shaped by direct-to-consumer (D2C) sales models, facilitated by sophisticated e-commerce platforms utilizing augmented reality (AR) tools for virtual placement and customization. This channel allows niche metal fabrication companies specializing in specific aesthetics (e.g., handcrafted copper basins) to bypass traditional retail distribution, offering a wider variety of custom products to a global residential audience. However, managing the logistics of shipping heavy, high-value, and sometimes fragile metal fixtures globally remains a significant hurdle for purely online D2C models, requiring specialized packaging and reliable freight partnerships to minimize damage and customer dissatisfaction.

Further structural analysis highlights that the integration segment—integrated metal vanity systems that combine the washstand structure, countertop, and sometimes storage—is gaining substantial traction, particularly in luxury apartment complexes and boutique hotels. These systems offer streamlined installation and a high degree of aesthetic consistency, appealing to developers focused on premium finishes and efficiency. This integration necessitates strong collaboration between metal fabrication specialists and surface material providers (e.g., quartz or composite manufacturers) to ensure materials interface seamlessly, driving strategic partnerships and mergers across the value chain to offer complete, ready-to-install solutions that minimize on-site complexity and labor costs for major construction contractors globally.

In summary, the Metal Washstand Market is characterized by robust growth in emerging economies and persistent demand for high-value, design-led products in established markets. Key strategies for success involve continuous innovation in surface coatings (for both aesthetics and hygiene), achieving operational efficiency through AI and automation in fabrication, and developing highly customized distribution models that effectively serve the distinct needs of the commercial/institutional sector and the design-conscious residential consumer. Navigating raw material volatility and regulatory fragmentation remains central to long-term profitability and sustainable market leadership across all global territories.

The Metal Washstand Market is strategically important within the broader sanitation and architectural hardware industry due to its resilience to obsolescence and critical role in public health infrastructure. The inherent circularity of metal materials, particularly stainless steel, provides a competitive advantage in a world increasingly focused on reducing environmental impact. Manufacturers are leveraging this sustainability narrative by prominently featuring high recycled content percentages in their product specifications and achieving environmental product declarations (EPDs). This focus on circular economy principles is not only an ethical selling point but is rapidly becoming a mandatory requirement for large-scale governmental and corporate procurement contracts, fundamentally altering the competitive dynamics by favoring companies with established sustainable supply chains.

Technological refinement also extends into water conservation features, moving beyond simply integrating low-flow faucets. Modern metal washstands are being designed with subtly angled basins and specialized drainage systems that optimize water evacuation while minimizing splashing, thereby improving the overall user experience and reducing secondary maintenance associated with wet floors and surrounding surfaces in commercial washrooms. Furthermore, manufacturers are exploring lightweighting techniques using advanced aluminum alloys without compromising structural integrity, reducing transportation costs and the environmental footprint associated with logistics, appealing to globally distributed construction supply chains aiming for leaner operations.

The competitive landscape sees significant mergers and acquisitions (M&A) activity as larger plumbing fixture corporations seek to integrate niche metal fabrication expertise or acquire proprietary surface treatment technologies. This consolidation aims to create vertically integrated companies capable of controlling the entire production process from raw material input to final installation support, enhancing quality control and reducing reliance on third-party specialists for critical steps like PVD coating. Such strategic moves are particularly focused on bolstering capacity in the high-growth APAC region and strengthening market penetration in the mature, high-margin European luxury segments, ensuring a diversified global market presence.

Looking ahead, the market must prepare for potential disruptions from alternative, highly durable composite materials that are increasingly mimicking the industrial aesthetic of metal while potentially offering cost or weight advantages. Metal washstand manufacturers are countering this threat by focusing on features that composites cannot easily replicate, such as the seamless integration of heating elements (for towel warming features within integrated vanities) or the inherent anti-vandal properties that pure, thick-gauge metal provides. The strategic imperative is to ensure the functional and aesthetic superiority of metallic products remains clearly distinguishable from synthetic alternatives.

Finally, the growing trend of modular construction and prefabricated buildings mandates that metal washstand providers design products optimized for rapid, factory-based integration. This includes designing fixture attachments and plumbing connections that require minimal on-site adjustment, allowing entire bathroom pods to be shipped and installed with maximum efficiency. Manufacturers that successfully cater to the specific demands of the off-site construction industry—predictability, precision, and speed—will capture significant long-term contracts and establish themselves as preferred suppliers in the modern built environment.

***End of Report***

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.