ID : MRU_ 435677 | Date : Dec, 2025 | Pages : 251 | Region : Global | Publisher : MRU

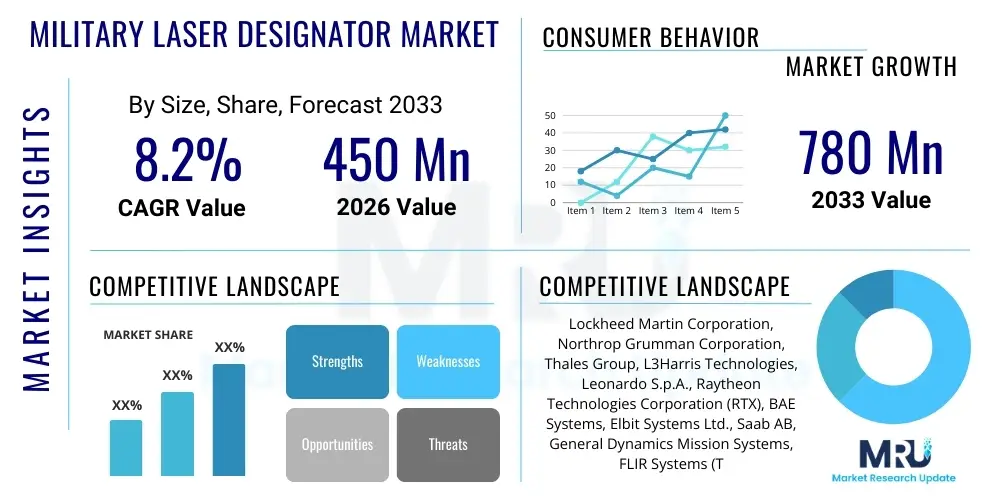

The Military Laser Designator Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.2% between 2026 and 2033. The market is estimated at USD 450 Million in 2026 and is projected to reach USD 780 Million by the end of the forecast period in 2033.

The Military Laser Designator Market encompasses highly specialized electro-optical systems designed to precisely illuminate targets for attack by laser-guided munitions, including bombs, missiles, and projectiles. These sophisticated devices, utilizing Diode-Pumped Solid-State (DPSS) laser technology, emit a coded laser beam that is reflected off the target, allowing a corresponding weapon sensor (seeker) to track the reflected energy and guide the munition to the designated impact point with exceptional accuracy. Critical applications span across joint terminal attack controller (JTAC) operations, special reconnaissance missions, and integrated weapon systems aboard military platforms such as fixed-wing aircraft, attack helicopters, and Unmanned Aerial Vehicles (UAVs). The core benefit of these designators is the significant reduction in collateral damage, enabling surgical precision strikes in complex operational environments.

The product portfolio within this market includes handheld and portable designators used by ground forces, vehicle-mounted systems, and highly integrated airborne designators housed in sophisticated targeting pods. Technological advancements focus heavily on miniaturization, increased effective range, improved battery life, and enhanced integration capabilities with modern Command, Control, Communications, Computers, Intelligence, Surveillance, and Reconnaissance (C4ISR) networks. The growing necessity for precision-guided munitions (PGMs) in modern warfare doctrines, coupled with increasing global geopolitical instability, acts as a pivotal factor driving the adoption and procurement of advanced laser designation systems by defense forces worldwide. Furthermore, the shift towards counter-insurgency (COIN) and urban warfare necessitates systems that provide accurate designation without requiring prolonged exposure to hostile fire.

Driving factors for sustained market expansion include the extensive modernization programs undertaken by major global militaries, particularly the replacement of legacy laser designation technologies with multi-spectral and ruggedized units. The rising deployment of UAVs across intelligence and attack roles inherently demands lightweight, high-performance laser designators optimized for unmanned platform integration. Moreover, continuous investment in R&D aimed at developing eyesafe laser designators—which maintain high performance while minimizing the risk to friendly forces—further stimulates market growth. The increasing emphasis on interoperability between allied forces also necessitates adherence to NATO Standardization Agreements (STANAGs) for laser codes, ensuring seamless cross-platform functionality.

The Military Laser Designator Market is characterized by robust technological advancements, driven primarily by the global shift towards network-centric warfare and the pervasive demand for high-precision strike capabilities. Current business trends indicate a strong move toward systems capable of integration across multiple domains—air, land, and sea—with a particular focus on minimizing size, weight, and power (SWaP) consumption for suitability on small tactical platforms. Defense contractors are increasingly engaging in strategic partnerships to develop advanced targeting pods that bundle laser designators with thermal imaging, high-definition cameras, and sophisticated tracking algorithms. Key market participants are prioritizing the development of robust systems that operate reliably under extreme environmental conditions, ensuring high reliability during critical mission phases. The commercial landscape is consolidating around key providers specializing in advanced photonics and systems integration, emphasizing proprietary cooling mechanisms and enhanced beam quality.

Regionally, North America maintains the dominant market share, fueled by massive defense budgets in the United States dedicated to platform modernization (e.g., F-35 targeting systems, ground JTAC equipment) and rapid technological insertion. However, the Asia Pacific (APAC) region is demonstrating the highest growth trajectory, primarily due to escalating military competition, border disputes, and extensive defense procurement by nations like China, India, and South Korea, who are actively seeking self-sufficiency or purchasing advanced Western and Russian technologies. European markets show stable growth, influenced heavily by NATO member obligations to upgrade precision strike capabilities and replace aging equipment fleets, particularly following renewed geopolitical tensions in Eastern Europe. The Middle East and Africa (MEA) continue to be critical consumers, driven by sustained conflicts and the urgent need for enhanced border security and counter-terrorism measures, often procuring integrated systems through Foreign Military Sales (FMS).

Segment trends reveal a rapid expansion in the Airborne segment, propelled by the widespread adoption of advanced targeting pods (ATPs) and the proliferation of attack and surveillance UAVs requiring integrated designators. Within the technology segment, DPSS lasers are replacing older lamp-pumped systems due to their superior efficiency and smaller footprint. Furthermore, the Portable/Handheld segment is experiencing significant innovation focused on ergonomics and multi-functionality, transforming traditional designators into comprehensive targeting and surveillance tools for ground troops. The continuous miniaturization efforts and cost reduction initiatives are broadening the accessibility of these high-tech systems to smaller military organizations and special operations forces, further diversifying the customer base beyond conventional air forces and armies.

Common user questions regarding AI's impact on Military Laser Designators center around concerns of autonomous targeting ethics, the reliability of automated recognition under combat stress, and the seamless integration of machine learning algorithms with legacy laser hardware. Users are primarily focused on how AI can enhance operational tempo and reduce cognitive load for human operators. The key expectations revolve around leveraging AI for rapid, precise, and consistent target identification and tracking, significantly beyond human capability in dynamic environments. Specifically, the integration of deep learning models into sensor fusion architectures is expected to automate the differentiation between combatants and non-combatants, addressing critical rules of engagement (ROE) concerns and further mitigating the risk of inadvertent collateral damage, thereby justifying substantial future defense investment in AI-enabled designation systems.

The integration of Artificial Intelligence transforms the laser designation process from a manually intensive task into a highly automated, data-driven operation. AI algorithms are instrumental in processing vast amounts of incoming sensor data from thermal, electro-optical, and synthetic aperture radar (SAR) sources in real-time, enabling Automated Target Recognition (ATR) far faster than human analysis. This capability allows the system to instantaneously classify potential targets, prioritize high-value assets, and maintain a lock even when environmental factors like smoke, fog, or dust temporarily obstruct the line of sight. Moreover, AI facilitates predictive tracking, optimizing the laser beam placement to compensate for high-speed target maneuvers or platform instability, thus improving the overall probability of a successful hit (Ph).

Furthermore, AI significantly enhances the interoperability and coordination aspects of precision strike missions. By using machine learning to analyze mission parameters, terrain data, and threat assessments, the system can recommend the optimal designator and PGM pairing for a given target, streamlining the decision-making process for Joint Terminal Attack Controllers (JTACs). This automation is critical in network-centric warfare environments where time is a critical factor. The long-term impact of AI will lead to the development of 'smart' designators that not only illuminate but also analyze the target's vulnerability, ensuring maximum lethality per strike while adhering strictly to ethical military standards and reducing the overall dependency on continuous, error-prone human intervention.

The Military Laser Designator Market dynamics are powerfully shaped by an interplay of increasing global defense spending and the ongoing demand for precision strike capabilities (Drivers), countered by stringent export controls and high procurement costs (Restraints). Opportunities lie predominantly in technological miniaturization for UAV integration and the growing utility in emerging threat sectors like Counter-UAS (C-UAS). The primary impact forces driving this market include geopolitical instability necessitating readiness, rapid technological obsolescence demanding continuous upgrades, and standardization efforts promoting interoperability among allied nations, creating a highly competitive environment focused on performance and reliability.

Drivers: Global geopolitical instability, particularly in Eastern Europe, the South China Sea, and the Middle East, necessitates that nations maintain high levels of military readiness and possess precision strike capabilities, leading directly to increased procurement of laser designators. Furthermore, military modernization programs across established and emerging economies are replacing older targeting systems with state-of-the-art, multi-function electro-optical targeting pods (EOTPs). The increasing adoption of unmanned aerial platforms (UAVs) across surveillance, reconnaissance, and strike roles dictates the need for lightweight, high-performance designation systems tailored for remote operation. Finally, the demonstrated success of precision-guided munitions guided by laser designators in recent conflicts strongly validates the investment in this technology, encouraging further expenditure.

Restraints: The market faces significant hurdles, notably the extremely high cost associated with research, development, and manufacturing of advanced military-grade photonics and cooling systems, which can limit adoption by smaller defense budgets. Strict international regulations governing the sale and transfer of military technology, primarily the International Traffic in Arms Regulations (ITAR) and similar export control regimes, restrict market reach and deployment, creating compliance overheads for manufacturers. Additionally, susceptibility to counter-measures such as laser blinding, jamming, or atmospheric interference (e.g., heavy dust or fog) necessitates constant technological resilience upgrades, adding to the complexity and cost of the systems.

Opportunities: Significant market opportunities exist in the continued miniaturization of laser designator components, specifically reducing the SWaP characteristics to enable seamless integration onto small, tactical, and low-cost UAVs and dismounted soldier systems. The expanding requirement for laser designation in non-traditional roles, such as guiding precision non-lethal weapons or providing accurate ranging for C-UAS kinetic systems, opens new revenue streams. Moreover, the shift towards eyesafe laser designation technology (utilizing wavelengths less damaging to human vision) creates a vital commercial avenue, especially for training and close-quarters operations where safety protocols are paramount. The long-term trend favors systems offering superior battery life and rapid charging capabilities for extended field operations.

The Military Laser Designator Market is comprehensively segmented based on its application platform, technology utilized, operating wavelength, and physical form factor. This segmentation reflects the diverse operational requirements of modern militaries, ranging from highly integrated airborne systems used by major air forces to rugged, portable units employed by ground special forces. The Platform segment is the most crucial, determining the size, power requirement, and cooling infrastructure necessary for the designator. Technological segmentation highlights the industry shift towards efficient DPSS lasers, offering superior beam quality and reliability compared to legacy lamp-pumped systems. Understanding these segments is critical for manufacturers aiming to align their product portfolios with specific defense procurement cycles and modernization objectives globally.

The value chain for Military Laser Designators is highly specialized, beginning with the upstream procurement of complex raw materials and highly refined optical components. This segment includes the sourcing of rare earth elements necessary for laser gain media (e.g., Neodymium-doped YAG crystals), high-purity semiconductors for laser diodes, and sophisticated optical glass for lenses and windows. Due to the precision requirements, suppliers must adhere to extremely tight military specifications, making this stage crucial for determining the final system performance. The manufacturing process involves highly intricate laser rod assembly, crystal growth, and precision optical coating application, demanding specialized cleanroom environments and expert engineering skills. This upstream phase is often concentrated among a few specialized vendors globally, resulting in potential supply chain fragility.

The midstream phase focuses on system integration and manufacturing, where major defense contractors assemble the laser source, beam steering mechanisms (gimbals), advanced cooling systems, and integrated sensor electronics (including thermal cameras and GPS/INS modules) into a single, ruggedized unit. Quality control and rigorous military qualification testing (MIL-STD compliance for shock, vibration, and temperature) are paramount during this stage. Integration into the specific platform, whether an aircraft targeting pod or a ground handheld unit, requires significant coordination with aircraft manufacturers or vehicle integrators. The distribution channel is heavily dominated by direct sales contracts with national defense ministries or, internationally, through government-to-government Foreign Military Sales (FMS) programs or Direct Commercial Sales (DCS) under strict export licenses. Indirect channels are minimal, primarily limited to small specialized distributors handling spare parts or maintenance services.

The downstream analysis involves the end-user deployment, training, maintenance, and eventual system upgrades. Potential customers (defense forces) prioritize long-term logistical support and system reliability, driving manufacturers to offer comprehensive service and upgrade packages over the system's lifecycle. Technological obsolescence in electro-optics is rapid, necessitating mid-life upgrades, often involving replacing sensor arrays and digital processing units. The critical nature of these systems ensures that the relationship between the original equipment manufacturer (OEM) and the end-user military force is a long-term partnership rather than a transactional sale, encompassing extensive training for JTACs, pilots, and maintenance crews. This structure ensures that manufacturers retain significant influence over the aftermarket and upgrade cycles, contributing substantially to recurring revenue streams.

The primary customers for Military Laser Designators are national Ministries of Defense (MoD) and their affiliated armed forces, specializing in units that conduct kinetic strike operations requiring extreme accuracy. High-priority buyers include Air Forces procuring advanced fighter and bomber aircraft, as these platforms are the primary users of high-powered targeting pods integrating laser designators for deploying precision-guided air-to-ground munitions. The procurement cycle is often lengthy, tied to major aircraft or platform refresh programs, and requires strict adherence to standardized interface protocols such as MIL-STD-1760 for weapons release and NATO STANAG 3733 for laser coding.

A second crucial customer segment comprises Special Operations Forces (SOF) and conventional Ground Forces, particularly Joint Terminal Attack Controllers (JTACs) and Forward Observers (FOs). These personnel rely on the smaller, lighter, and more rugged portable/handheld laser designators to rapidly and discreetly designate targets from the ground, coordinating close air support (CAS). Their procurement decisions are heavily influenced by SWaP metrics, battery life, operational range in diverse climates, and integration capability with soldier-worn digital communication systems. The shift towards network-centric warfare means these ground units require devices that can seamlessly transmit targeting data coordinates via secure networks.

Finally, emerging customer groups include governmental agencies involved in border security, maritime patrol organizations, and rapid-response counter-terrorism units that utilize Unmanned Aerial Systems (UAS). These customers seek cost-effective, medium-power designators optimized for drone payload constraints. The procurement in this segment is faster paced and focused on integrating commercial off-the-shelf (COTS) components that meet military ruggedness standards. Military research laboratories and defense prime contractors purchasing units for testing and integration purposes also constitute a smaller, yet technically demanding, customer base focused purely on cutting-edge features and customization options.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 450 Million |

| Market Forecast in 2033 | USD 780 Million |

| Growth Rate | 8.2% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Lockheed Martin Corporation, Northrop Grumman Corporation, Thales Group, L3Harris Technologies, Leonardo S.p.A., Raytheon Technologies Corporation (RTX), BAE Systems, Elbit Systems Ltd., Saab AB, General Dynamics Mission Systems, FLIR Systems (Teledyne FLIR), TRUMPF, Trijicon Inc., Qioptiq (Excelitas Technologies), Jenoptik AG, Kongsberg Gruppen, General Atomics Aeronautical Systems, Rafael Advanced Defense Systems, DRS Technologies (Leonardo DRS), Rheinmetall AG |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The current technology landscape of the Military Laser Designator market is defined by the migration from legacy flashlamp-pumped Nd:YAG lasers to highly efficient Diode-Pumped Solid-State (DPSS) laser architectures. DPSS technology offers substantial advantages, including greatly reduced thermal management complexity, increased pulse repetition frequency, superior beam divergence characteristics, and critically, a smaller and lighter footprint, making it ideal for integration into demanding aerial platforms and man-portable systems. Furthermore, modern designators incorporate sophisticated integrated cooling mechanisms, often utilizing micro-channel heat sinks or advanced thermoelectric coolers, which are essential for maintaining stable performance and extending the lifespan of the diode arrays under continuous high-power operation, a critical factor for maintaining mission effectiveness.

Integration technology represents another pivotal area of development. Advanced laser designators are no longer standalone devices but are deeply embedded within sophisticated multi-sensor targeting pods or ground surveillance systems. This integration involves utilizing high-resolution electro-optical (EO) and infrared (IR) sensors, advanced Inertial Navigation Systems (INS), and Global Positioning System (GPS) receivers to ensure precise geo-referencing of the designated target, even when the designator is mobile. Furthermore, the use of proprietary digital encryption and standardized pulse coding (STANAG 3733) ensures secure and interoperable communication between the designating unit and the seeking munition, preventing hostile interference or misidentification. The increasing computational power in these systems supports real-time image processing and complex trajectory prediction.

A key focus area for future R&D is the maturation of eyesafe laser designators operating around the 1.5 µm wavelength. While these systems offer crucial safety benefits for training and deployment near civilian areas, current limitations include lower atmospheric transmission and shorter effective range compared to the dominant 1064 nm wavelength systems. Overcoming these limitations through enhanced receiver sensitivity and high-power fiber laser technology remains a priority. Furthermore, the development of compact, stabilized gimbals capable of handling high angular rates is essential for airborne applications, ensuring the laser spot remains locked on target despite platform motion, turbulence, or long standoff distances, thereby maximizing the terminal accuracy of precision-guided munitions.

The primary function of a Military Laser Designator is to precisely illuminate a target with a coded, infrared laser beam, allowing laser-guided munitions (such as Paveway bombs or Hellfire missiles) to autonomously track the reflected energy and achieve a highly accurate terminal strike, significantly reducing collateral damage in precision warfare operations.

AI integration enhances efficiency by enabling Automated Target Recognition (ATR), predictive tracking, and rapid sensor fusion. This reduces the cognitive burden on human operators, minimizes the time from detection to strike, and ensures the laser spot remains locked on the target with high stability, even in cluttered or dynamic combat environments.

The key technological trends include the transition to high-efficiency Diode-Pumped Solid-State (DPSS) lasers, extreme miniaturization to meet Size, Weight, and Power (SWaP) constraints for UAV integration, the development of eyesafe (1550 nm) designators for safer training, and deep integration with C4ISR and multi-spectral targeting pods.

The Asia Pacific (APAC) region is projected to exhibit the highest Compound Annual Growth Rate (CAGR). This growth is primarily fueled by rising geopolitical tensions, massive military modernization programs in countries like China and India, and increasing procurement of advanced UAVs and associated precision strike capabilities throughout the region.

Non-eyesafe designators, typically operating at 1064 nm, offer superior power output and range but pose a risk of permanent eye damage upon direct exposure. Eyesafe designators (around 1550 nm) use wavelengths absorbed by the eye's media, dramatically reducing retinal damage risk, making them essential for training and operations in close proximity to friendly forces, though often at the cost of slightly reduced maximum range.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.