ID : MRU_ 438486 | Date : Dec, 2025 | Pages : 242 | Region : Global | Publisher : MRU

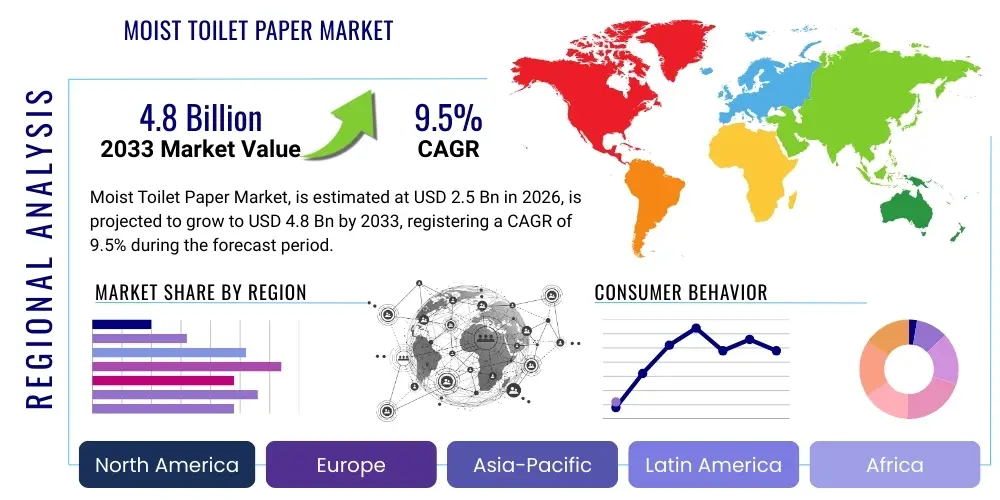

The Moist Toilet Paper Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2026 and 2033. The market is estimated at $2.5 Billion in 2026 and is projected to reach $4.8 Billion by the end of the forecast period in 2033. This robust growth trajectory is primarily fueled by increasing consumer awareness regarding personal hygiene, coupled with rising disposable incomes in emerging economies, leading to greater adoption of premium hygiene products. The perception of moist toilet paper shifting from a luxury item to a necessity in many developed regions further solidifies its market expansion, despite persistent challenges related to infrastructure compatibility and environmental sustainability.

The Moist Toilet Paper Market encompasses the production and distribution of pre-moistened, disposable wipes designed for post-defecation cleansing, offering superior hygiene compared to dry toilet paper alone. These products typically consist of non-woven material, saturated with a dermatologically tested cleansing solution that often includes moisturizing agents, mild preservatives, and fragrances. The primary application is personal care, targeting enhanced comfort, cleanliness, and addressing specific needs such as sensitive skin or hemorrhoidal conditions. Major applications also extend into institutional settings, healthcare facilities, and travel hygiene kits where convenient cleansing solutions are essential. Key benefits driving consumer adoption include improved cleansing efficacy, moisturizing properties that prevent irritation, and the overall perception of freshness and superior hygiene standards. Driving factors for market growth involve strong consumer interest in wellness and personal care, extensive marketing emphasizing flushability (despite ongoing debates), product innovation in biodegradable materials, and the convenience offered by these ready-to-use wipes. Furthermore, regulatory shifts standardizing flushability claims in certain regions are expected to mitigate consumer confusion and boost trust in product use, thereby accelerating market penetration across diverse demographic groups.

The product composition is critical to its performance and market acceptance, involving materials like wood pulp, cotton, or synthetic fibers like polyester, combined with water-based lotions. The complexity lies in achieving a balance between strength during use and rapid disintegration post-flush, a technical challenge that continuously shapes product development cycles. The global market is characterized by intense competition, with key players focusing heavily on developing sustainable product lines, particularly those using plant-derived and certified sustainable fibers to appeal to environmentally conscious consumers. The recent shifts in consumer behavior following global health events have magnified the importance of advanced personal hygiene routines, indirectly benefiting the moist toilet paper segment by normalizing supplementary cleansing products. This demand spike has prompted significant investment in manufacturing automation and efficiency, aimed at scaling production capabilities while adhering to stringent quality control and formulation standards essential for maintaining skin safety and product shelf life.

The global Moist Toilet Paper Market is experiencing dynamic business trends characterized by a decisive pivot towards sustainable and environmentally responsible products, driven primarily by consumer pressure and impending regulatory mandates regarding plastic content and marine biodegradability. Leading manufacturers are heavily investing in research and development to introduce 100% plant-based, plastic-free, and truly flushable wipes, redefining product standards and setting new competitive benchmarks. E-commerce platforms are emerging as the fastest-growing distribution channel, enabling brands to reach specialized consumer niches and offering subscription services that foster long-term loyalty and predictable revenue streams. Regional trends show that North America and Europe currently dominate the market value due to established hygiene norms and high consumer spending power, while the Asia Pacific region, particularly countries like China and India, represents the most significant growth opportunity, fueled by urbanization, improved sanitation infrastructure, and rapidly expanding middle-class populations prioritizing personal wellness. The shift in regional focus is compelling multinational corporations to tailor their product offerings to localized preferences regarding formulation, fragrance, and packaging size, ensuring market relevance across diverse cultural landscapes.

In terms of segmentation trends, the flushable category remains dominant, although its regulatory definition and consumer perception are under constant scrutiny, propelling the growth of robust third-party certifications. The residential end-user segment commands the largest market share, directly correlating with household adoption for everyday use, while the commercial and institutional segments show steady, specialized growth driven by heightened standards in hospitality and healthcare sectors. Ingredient-focused trends indicate a growing demand for hypoallergenic, alcohol-free, and naturally scented formulations, aligning with the broader consumer movement toward cleaner label products. Furthermore, the market structure reflects a consolidation trend where major fast-moving consumer goods (FMCG) companies are either acquiring smaller innovative sustainable brands or forming strategic partnerships to quickly integrate advanced material technology into their portfolios. This intense focus on material innovation and distribution efficiency is central to maximizing profitability and navigating the increasingly complex global supply chain for non-woven hygiene products. The confluence of sustainability goals and digital retail penetration defines the current competitive landscape and future market trajectory for moist toilet paper products globally.

Analysis of common user questions reveals strong interest concerning how Artificial Intelligence (AI) can revolutionize the supply chain, enhance personalized product marketing, and improve sustainability tracking within the Moist Toilet Paper Market. Users frequently inquire about AI's role in optimizing inventory levels to prevent stockouts, especially for subscription services, and its potential in predicting demand fluctuations based on seasonality or external public health events. Concerns center around the use of AI in formulating products, particularly regarding ingredient safety and transparency, and the deployment of predictive maintenance in manufacturing to reduce waste. Consumers expect AI to facilitate highly customized product recommendations, matching specific skin sensitivities or environmental preferences, thereby transitioning from mass market offerings to tailored hygiene solutions. Furthermore, questions arise about AI-driven quality control mechanisms ensuring the flushability consistency and material integrity across large batches, addressing a fundamental trust issue in the category. The consensus is that AI offers powerful tools for efficiency and personalization but must be implemented transparently, safeguarding consumer data while delivering tangible product improvements and operational cost reductions.

The adoption of sophisticated AI and Machine Learning (ML) algorithms is poised to transform manufacturing processes by enabling real-time monitoring of raw material characteristics, such as fiber moisture content and tensile strength, crucial for maintaining product quality and flushability standards. AI-driven predictive analytics allow manufacturers to anticipate equipment failures, minimizing downtime and significantly improving overall equipment effectiveness (OEE), thereby lowering the cost of goods sold. In the competitive retail environment, AI powers advanced dynamic pricing models and inventory optimization, particularly benefiting online retailers by ensuring optimal stock levels across geographically distributed fulfillment centers. This technological integration is not only optimizing internal operations but also creating new channels for consumer engagement, such as AI-powered chatbots providing immediate customer support regarding product usage, environmental disposal guidelines, and subscription management.

The market dynamics are defined by a complex interplay of Drivers, Restraints, and Opportunities, which together form the Impact Forces shaping the industry's evolution. The primary drivers include increasing consumer emphasis on superior personal hygiene, particularly post-pandemic, the convenience and comfort benefits over dry paper, and targeted product development addressing specific demographic needs like infant care and adult incontinence. These factors create strong underlying demand, particularly in regions where disposable income growth facilitates premium product purchases. Conversely, the market is significantly restrained by persistent consumer skepticism and infrastructure challenges related to flushability, leading to plumbing issues and municipal sewer blockages in some regions. Furthermore, environmental concerns regarding the volume of waste generated and the difficulty in composting or biodegrading some wipe materials impose regulatory and reputational pressures on manufacturers. This constant tension between convenience-driven demand and environmental responsibility defines a core constraint on global expansion and adoption.

Opportunities for growth are concentrated in the rapid innovation of truly sustainable materials, such as highly biodegradable wood-pulp alternatives and plastic-free fibers, which address the primary restraint of environmental impact. Emerging markets in Asia Pacific and Latin America offer untapped potential due to improving sanitation standards and increasing urbanization, providing new customer bases ready for initial adoption. The development of specialized products, including those infused with probiotics or specific dermatological agents, also opens niche market segments with high profit margins. The Impact Forces resulting from this interaction dictate that technological investment in sustainability is non-negotiable; manufacturers failing to secure validated third-party certifications for environmental claims risk significant loss of market share. The competitive force is high, compelling companies to focus simultaneously on cost efficiency via supply chain automation and premium branding achieved through verifiable sustainability and superior user experience, fundamentally transforming the competitive landscape from a commodity focus to a value-added personal health product.

The regulatory environment acts as a significant external force, particularly in mature markets like the EU and North America, where legislation increasingly restricts the use of misleading "flushable" labeling. This regulatory scrutiny forces companies to adopt higher standards for disintegration tests, minimizing negative public perception and infrastructural damage. The interplay between consumer demand for premiumization and the need for cost-effective manufacturing drives continuous process optimization. Companies that successfully navigate this nexus—delivering a high-quality, demonstrably sustainable, and affordable product—are positioned for long-term market leadership, while those reliant on older, non-biodegradable formulations face inevitable phase-out due to mounting regulatory and ethical pressures. The market thus requires agile responses to both consumer health trends and macro environmental policy shifts.

The Moist Toilet Paper Market is comprehensively segmented based on material type, end-user application, distribution channel, and flushability characteristics, reflecting the diverse preferences and infrastructure constraints globally. Segmentation by material type distinguishes between natural fibers (such as wood pulp and cotton) which generally align with sustainability demands, and synthetic fibers (like polyester blends) which often offer superior tensile strength and lower cost. The end-user analysis highlights residential users as the dominant segment, accounting for the largest consumption volume due to everyday household necessity, closely followed by commercial and institutional buyers, including hospitals and hotels, requiring bulk specialty products. Distribution channel segmentation is crucial, with traditional retail (supermarkets/hypermarkets) currently holding the volume lead, while online retail is rapidly gaining prominence due offering convenience, discretion, and subscription model benefits, particularly appealing to younger, digitally native consumers. Understanding these segments is paramount for strategic market entry and targeted product development.

Further granular analysis focuses on flushability, differentiating between products explicitly marketed as flushable, subject to rigorous testing standards, and non-flushable wipes, typically requiring disposal in waste bins. The regulatory landscape is driving innovation within the flushable segment, necessitating the use of specialized, dispersible substrates that break down quickly upon exposure to water turbulence. The growing importance of environmental attributes means segments focused on plant-based and plastic-free materials are experiencing above-average growth rates, even commanding a price premium, indicating a clear consumer willingness to pay more for sustainable options. Regional variations also dictate segmentation success; for instance, markets with underdeveloped sewer systems show higher resilience in the non-flushable category, while highly regulated regions prioritize verified flushable claims, influencing the dominant segments across continents.

The competitive strategy often involves targeting specific micro-segments based on skin condition or age group, such as sensitive skin variants that exclude common irritants like alcohol and parabens, or specialized wipes for baby and senior care. This vertical integration of product attributes allows manufacturers to capture high-value market share despite intense competition in the general-purpose categories. Successful market players meticulously analyze the intersectionality of these segments, for example, developing an organic, flushable wipe distributed primarily through online subscription models to target environmentally conscious, convenience-seeking urban households. This multifaceted segmentation approach ensures that product portfolios are optimized to maximize reach and profitability across the heterogeneous global consumer base, driving steady incremental growth and brand loyalty in specialized niches.

The Value Chain for the Moist Toilet Paper Market begins with the upstream sourcing of raw materials, primarily focused on non-woven fabrics and chemical inputs. Upstream analysis involves securing sustainable and cost-effective pulp and fiber sources, which often requires long-term contracts with certified forestry operations, given the industry's rapid shift towards biodegradable substrates like viscose and certified cellulosic fibers. The manufacturing phase involves converting these raw materials—non-woven fabric creation, impregnation with the cleansing solution, and final packaging—where precision engineering ensures consistent saturation levels and proper folding. Significant value is added during formulation development, requiring R&D expertise to balance skin safety, preservation efficacy, and environmental compatibility. Logistics, inventory management, and warehousing form a critical link, ensuring product freshness and efficient movement across global supply networks, which is essential given the product’s shelf-life sensitivity.

The downstream analysis focuses on market penetration and consumer reach through diverse distribution channels. Direct distribution involves sales through proprietary brand e-commerce sites and direct-to-consumer (D2C) subscription models, offering higher margin control and direct customer data collection. Indirect distribution relies heavily on established partnerships with large-scale retailers such as supermarkets and hypermarkets, which provide extensive physical reach and high volume sales visibility. The choice of distribution channel significantly impacts pricing strategy and promotional activities; direct channels facilitate personalized marketing, while indirect channels leverage retailer promotional clout. Retailers add value through merchandising, localized inventory management, and consumer convenience, although they often impose pressure on manufacturer margins. Successful market players optimize their value chain by leveraging technology, particularly AI and IoT, to monitor product quality throughout distribution and reduce waste from obsolescence.

Competition in the midstream and downstream components of the value chain is intense. Manufacturers strive for vertical integration, controlling material sourcing and production to maintain quality control and mitigate supply chain risks, especially concerning volatile fiber prices. Distribution channel management is increasingly complex due to the rise of specialized retailers and cross-border e-commerce, demanding robust logistics infrastructure capable of handling large volumes with rapid turnover. Furthermore, the push for environmentally friendly packaging requires investments in packaging machinery capable of handling recyclable or compostable films, adding complexity and cost to the final stage of manufacturing. Ultimately, profitability hinges on minimizing upstream raw material costs while maximizing downstream market presence and commanding a price premium through superior product quality, sustainable attributes, and effective branding and consumer education regarding proper disposal.

The Moist Toilet Paper Market serves a broad spectrum of end-users, with the primary target audience being residential consumers seeking enhanced personal hygiene and convenience in their daily routines. Within the residential segment, key buyer groups include families with young children, where the wipes offer easy cleanup, individuals focused on wellness and premium personal care products, and aging populations who benefit from the gentle cleansing action, particularly those managing incontinence issues. These residential buyers prioritize product attributes such as hypoallergenic formulations, reliable flushability, and favorable bulk pricing offered through subscription services or large-format retail. Their purchasing decisions are highly influenced by brand reputation, dermatological endorsements, and demonstrated commitment to environmental sustainability, particularly concerning plastic content and chemical ingredients.

Beyond the residential sector, significant potential lies in institutional and commercial end-users. Healthcare facilities, including hospitals and nursing homes, constitute a crucial customer base, relying on moist wipes for patient care, where hygiene standards are non-negotiable and product safety is paramount. The hospitality industry, encompassing high-end hotels and resorts, utilizes these products as part of their premium amenity offerings, enhancing guest experience and perceived value. Travel and leisure segments also represent substantial potential, with travelers seeking portable, convenient hygiene solutions. These commercial buyers typically prioritize bulk packaging, stringent quality control certifications, and dependable supply continuity, often negotiating long-term contracts directly with manufacturers or specialized institutional distributors to manage large volume requirements efficiently.

Emerging potential customer segments include specialized athletic facilities and public health initiatives promoting sanitation in developing regions. In the athletic context, wipes are valued for quick pre- and post-activity cleansing. For global health organizations, accessible and safe cleansing alternatives are critical in areas lacking robust infrastructure. Manufacturers targeting these varied potential customer groups must tailor their product size, packaging durability, and formulation complexity. For instance, institutional buyers require robust, often non-fragranced formulations, whereas residential consumers may prefer lighter scents and decorative, discreet packaging. Effective segmentation and targeted marketing based on these distinct usage contexts are essential to maximizing market penetration and securing long-term customer relationships across the entire spectrum of potential buyers.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $2.5 Billion |

| Market Forecast in 2033 | $4.8 Billion |

| Growth Rate | 9.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Procter & Gamble, Kimberly-Clark, Unicharm Corporation, Johnson & Johnson, Rockline Industries, SCA, Albaad Corporate, Nice-Pak Products, Hengan International Group, Vinda International Holdings, Essity AB, Georgia-Pacific, Resolute Forest Products, Lenzing AG, Godrej Consumer Products, Meridian Industries, Cottonelle, Charmin, Beiersdorf AG, Edgewell Personal Care. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Moist Toilet Paper Market is primarily centered around advanced non-woven manufacturing techniques, sophisticated liquid formulation sciences, and innovative packaging solutions that preserve product integrity and shelf life. In manufacturing, the hydroentanglement process (spunlacing) is crucial for producing non-woven substrates that offer a desirable balance of softness, strength, and controlled dispersibility, essential for achieving flushability. Recent technological advances focus on utilizing renewable raw materials, such as cellulosic fibers derived from sustainably managed forests, and integrating proprietary binding systems that break down rapidly upon hydration in wastewater environments. Furthermore, continuous process automation, utilizing sensors and robotics, is being implemented to ensure precise and uniform saturation of the substrate with the cleansing solution, reducing product variation and waste in high-speed production lines. This technological drive is essential for manufacturers to meet the stringent demands for both product performance and environmental compliance, optimizing resource usage while maintaining high output capacity across various global facilities.

Chemical formulation technology represents another critical area of innovation, particularly concerning preservation systems. As consumers increasingly demand "clean label" products free from harsh chemicals like parabens, phenoxyethanol, and formaldehyde releasers, manufacturers are developing novel preservative blends, including natural derivatives and organic acids, capable of maintaining microbial stability without compromising skin health. Emulsification techniques are also advancing to ensure the stable integration of moisturizing agents and mild cleansing surfactants within the water-based solution, maximizing efficacy and comfort. A major technological focus remains on developing solutions that are pH-balanced, hypoallergenic, and compatible with sensitive skin, achieved through extensive dermatological testing and optimization of ingredient ratios. This focus on bio-compatibility and safety is fundamental to premium branding and market acceptance in highly regulated regions such as the European Union.

Packaging technology is evolving rapidly, driven by the need for sustainability and enhanced user convenience. Innovations include the development of mono-material films for easy recycling, and highly effective resealable closure systems that prevent moisture loss and ensure the last wipe remains as fresh as the first, extending product utility over time. Furthermore, smart packaging solutions, such as embedded QR codes and near-field communication (NFC) tags, are being explored to provide consumers with instant access to product details, usage instructions, and disposal guidelines, aligning with transparency trends. These packaging advancements serve the dual purpose of minimizing the product's environmental footprint and significantly improving the overall consumer experience, which is a key differentiator in a crowded market. The combination of sustainable raw material science, refined liquid formulation, and intelligent packaging characterizes the technological front in the contemporary moist toilet paper industry, ensuring compliance, safety, and superior consumer value.

The global Moist Toilet Paper Market exhibits distinct regional consumption patterns and growth dynamics influenced by economic development, cultural hygiene practices, and local regulatory frameworks governing water infrastructure and waste disposal. North America, particularly the United States, represents a mature but high-value market characterized by high consumer awareness, widespread adoption, and a strong presence of leading international brands. The market here is driven by premiumization, where consumers seek specialty products focusing on sensitive skin, natural ingredients, and strong, although frequently debated, flushability claims. Ongoing infrastructural debates about sewer system capacity continue to influence local legislation and consumer choice, driving manufacturers to seek explicit certification from water utility groups. This maturity means growth is primarily incremental, relying heavily on product innovation and sophisticated marketing to stimulate repeat purchases and attract new users from niche demographics.

Europe stands out due to its stringent regulatory environment, particularly the focus on sustainability and plastic reduction mandated by the European Union. Countries like Germany and the UK are highly sensitive to environmental impact, favoring products certified as truly biodegradable and plastic-free, often relying on independent certification bodies to validate claims, thus forcing manufacturers to accelerate material science innovation. The European market shows a strong preference for naturally derived, mild formulations, reflecting a broader regional inclination towards organic and clean-label consumer goods. Asia Pacific (APAC) is positioned as the epicenter of future growth, propelled by rapid urbanization, expanding middle classes, and massive improvements in sanitation infrastructure, especially in populous nations like China and India. Although per capita consumption remains lower than in the West, the sheer scale of the population and the rapid adoption of Western hygiene standards forecast double-digit growth rates, requiring localized product adaptations (e.g., smaller package sizes, different fragrance profiles) to cater to diverse cultural preferences.

Latin America (LATAM) and the Middle East & Africa (MEA) represent emerging opportunities. LATAM’s growth is fueled by increasing disposable incomes and effective marketing campaigns linking moist wipes to superior family health and hygiene. In MEA, market penetration is accelerating, driven by tourism, expatriate populations, and governmental efforts to improve public health standards. However, these regions often face challenges related to product distribution logistics and infrastructure constraints, necessitating reliance on the non-flushable category in areas with less developed plumbing. Strategic investment in local manufacturing capabilities and tailored supply chains is essential for long-term success in these nascent but promising geographical markets, demanding a flexible approach that balances premium quality with price accessibility for the burgeoning consumer base.

The primary driver is the significantly heightened global focus on superior personal hygiene and wellness, especially in the wake of recent public health awareness initiatives. Consumers are increasingly adopting moist wipes as a standard part of their cleansing routine, recognizing the product’s capability to deliver enhanced cleanliness and comfort compared to dry paper alone. Furthermore, ongoing innovation in sustainable, skin-friendly formulations supports this trend by addressing health and environmental concerns, thereby broadening consumer acceptance and normalizing usage across diverse demographics.

The true flushability of moist toilet paper remains a significant point of contention, heavily dependent on the product's material composition and local wastewater infrastructure capacity. While many products are marketed as 'flushable,' only those conforming to stringent industry standards (like INDA/EDANA guidelines or specific regional certifications) designed for rapid disintegration are safe for most municipal sewer systems. Consumers should look for clear labeling and third-party verification, as non-dispersible wipes pose risks of causing expensive blockages in residential plumbing and public utility infrastructure, creating a major financial and environmental restraint for the industry.

The Asia Pacific (APAC) region, driven by economic powerhouses such as China and India, presents the most substantial future growth opportunity for the moist toilet paper market. This projection is based on rapid urbanization rates, consistent increases in middle-class disposable incomes, and widespread governmental investment in modernizing sanitation and wastewater treatment infrastructure. Although current per capita usage is lower than in Western nations, the enormous consumer base ensures that even modest increases in penetration will translate into exponential market value expansion over the forecast period of 2026 to 2033, making it a critical strategic focus area for global manufacturers.

The moist toilet paper industry is fundamentally shifting towards sustainability by investing heavily in raw material science to eliminate fossil-fuel derived plastics entirely. Key technological advancements include developing 100% plant-based, plastic-free cellulosic fibers (e.g., sustainable viscose, wood pulp, or bamboo) that are proven to be truly biodegradable and compostable. Manufacturers are also improving packaging materials by utilizing recyclable mono-films and reducing overall material weight, driven both by strict European Union regulations and increasing consumer demand for verifiable eco-friendly hygiene products, transforming environmental compliance into a crucial competitive advantage.

E-commerce and digital distribution have become paramount, evolving into the fastest-growing distribution channel for moist toilet paper products. Online retail provides consumers with unmatched convenience, discretion in purchasing personal care items, and access to subscription models that foster brand loyalty and ensure consistent revenue streams for manufacturers. Digital platforms also enable highly personalized marketing and direct-to-consumer sales, allowing brands to bypass traditional retail markups, gather valuable consumer data, and efficiently cater to niche demands such as specialized sensitive skin formulations or bulk sustainable product orders, fundamentally disrupting conventional retail dominance.

Future technological advancements will focus on integrating Artificial Intelligence (AI) and the Internet of Things (IoT) into manufacturing processes to achieve unprecedented operational efficiency and product consistency. This includes AI-driven predictive maintenance to minimize production downtime, sophisticated machine vision systems for real-time quality control checks on non-woven material integrity and saturation levels, and advanced chemical engineering for developing self-preserving, natural, and biologically safe cleansing solutions. These innovations are critical for scaling production capacity while simultaneously adhering to increasingly strict regulatory and environmental performance mandates globally.

Beyond the residential sector, two major commercial sectors are heavy consumers: healthcare and hospitality. Healthcare facilities, including hospitals, clinics, and long-term care homes, rely on these wipes for essential patient care, prioritizing hygienic, non-irritating, and often medical-grade formulations. The hospitality industry, particularly premium hotels and resorts, integrates moist wipes as a superior amenity offering to enhance guest experience and signify high standards of cleanliness and luxury. Both sectors prioritize bulk purchasing, dependable supply chains, and stringent product certifications to meet professional standards and operational demands.

Segmentation by material profoundly influences both price points and consumer purchasing decisions, directly linking material origin to sustainability perception. Products made primarily from natural fibers like wood pulp or certified sustainable bamboo often command a price premium due to the associated higher raw material costs and complex processing required to achieve flushability and biodegradability. Conversely, synthetic or blended fibers (such as polyester and rayon mixes) typically offer superior tensile strength and a lower production cost, resulting in more budget-friendly general-purpose options. The increasing consumer preference for environmentally responsible products means natural fiber segments are rapidly gaining market share, even at higher prices, reflecting a shift towards value-based consumption.

Key financial metrics highlighting the market's health include the Compound Annual Growth Rate (CAGR) of 9.5%, indicating robust, sustained expansion over the forecast period. The projected increase from an estimated market size of $2.5 Billion in 2026 to $4.8 Billion by 2033 confirms significant investor confidence and market penetration potential. Furthermore, high gross profit margins are observed in the premium and specialized product segments (e.g., sensitive skin, plastic-free), driven by consumer willingness to pay a premium for verified quality and sustainability. These metrics collectively signal a market undergoing successful transition towards high-value, differentiated product offerings, supported by positive consumer spending trends globally.

The most significant regulatory challenge is the lack of globally harmonized standards for flushability testing and labeling, compounded by increasing governmental scrutiny over 'greenwashing' claims related to biodegradability. Manufacturers are pressured to comply with diverse, often contradictory, municipal and regional water utility standards, particularly in North America and Europe. This necessitates substantial investment in external certification and transparent communication to avoid costly lawsuits, fines, and reputation damage, making regulatory adherence a complex and continuous operational priority for all major market participants.

Global supply chain fluctuations, especially regarding the sourcing of non-woven raw materials like wood pulp and specialized cellulosic fibers (viscose), impose significant cost volatility and logistical risks on the moist toilet paper market. Geopolitical factors, climate-related events affecting forestry, and global logistics bottlenecks can cause sudden price spikes and material shortages, directly impacting manufacturing costs and, consequently, retail prices. To mitigate these risks, leading manufacturers are diversifying their supplier base, focusing on certified sustainable sourcing, and investing in advanced inventory management systems to maintain consistent production flow and buffer against external market disruptions.

The highest value-add in the moist toilet paper value chain is generated primarily in two key areas: sophisticated liquid formulation R&D and downstream branding/marketing. Formulation expertise allows companies to create proprietary solutions offering superior skin care benefits, preservative efficacy, and unique sensorial experiences, justifying premium pricing. Downstream, effective branding, packaging innovation (like robust resealable mechanisms), and successful consumer education regarding flushability and sustainability transform a commodity item into a perceived necessity, capturing significant consumer surplus and securing long-term brand equity.

Beyond basic cleanliness, moist toilet paper addresses specialized consumer needs related to skin sensitivity, medical conditions, and enhanced comfort. The product is particularly effective for individuals managing sensitive skin, hemorrhoidal conditions, or dermatological issues, as the moist, often hypoallergenic formulations reduce friction and irritation associated with dry wiping. Furthermore, they meet the functional needs of caregivers in institutional settings for efficient, gentle cleaning of patients, thus providing therapeutic and comfort benefits well beyond standard hygiene.

Smaller, innovative startups are acting as powerful disruptive forces by focusing exclusively on niche markets, primarily sustainability and clean ingredients, which often challenges the incumbents' reliance on traditional, less eco-friendly materials. These startups are frequently pioneers in adopting 100% plastic-free, highly certified biodegradable substrates and novel preservation systems, utilizing direct-to-consumer (D2C) models and transparent supply chains to quickly gain consumer trust. Established players are responding either through accelerated internal R&D focused on sustainability or through strategic mergers and acquisitions to integrate the disruptive technology and brand credibility of these agile newcomers.

The long-term forecast suggests increasing market segmentation based on price sensitivity. While the general-purpose, commodity segments will remain highly price-competitive, dominated by large volume retailers and private labels, the premium and specialty segments are expected to maintain strong price inelasticity. Consumers in developed markets, particularly those seeking specific attributes like certified sustainability, dermatological safety, or unique dispensing mechanisms, are demonstrating a consistent willingness to pay a premium. Therefore, successful market navigation involves balancing cost efficiency for mass-market offerings with continuous innovation to justify higher prices in niche, value-added categories.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.