ID : MRU_ 433587 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

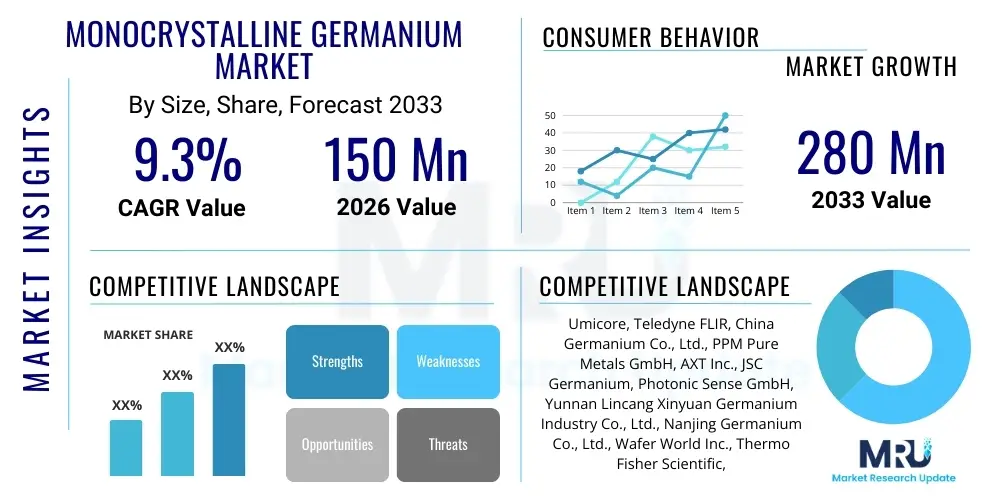

The Monocrystalline Germanium Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.3% between 2026 and 2033. The market is estimated at $150 Million USD in 2026 and is projected to reach $280 Million USD by the end of the forecast period in 2033. The market valuation reflects the high unit cost associated with ultra-high purity materials and the intricate, capital-intensive manufacturing processes required to produce defect-free single crystals. Although the market volume in tons might appear relatively small compared to bulk commodities, the specialized nature and high-performance requirements of the end-use applications—spanning defense, space, and advanced telecommunications—justify the high overall market value. This projected growth rate is slightly above the average for specialty materials, underpinned by continuous technological innovation in sensor technology and the non-satiable global appetite for enhanced surveillance and high-speed data transmission capabilities, solidifying Germanium's status as a critical strategic material.

The substantial growth anticipated between 2026 and 2033 is fundamentally driven by two macro trends: the proliferation of multi-junction solar cells in the rapidly expanding satellite and small-satellite (smallsat) constellation industry, and the mandated integration of long-wave infrared (LWIR) sensing into emerging platforms such as autonomous vehicles and drone technology. Furthermore, the push towards 6G infrastructure development, which heavily relies on specialized high-frequency semiconductor components often utilizing Silicon-Germanium (SiGe) alloys, ensures sustained, high-specification demand for the monocrystalline substrate. Market revenue projections are highly sensitive to geopolitical factors, particularly those affecting the raw Germanium supply chain, meaning the forecasted valuation relies on stable, albeit tightly managed, access to refined Germanium metal, which remains a key variable impacting the realized market size by 2033.

Monocrystalline Germanium (Mono-Ge) represents a strategic material at the confluence of advanced optics and cutting-edge semiconductor technology. Characterized by its unique lattice structure and exceptional purity, typically reaching five-nines (99.999%) or six-nines (99.9999%), Mono-Ge is manufactured using stringent crystal growth techniques like the Czochralski method, ensuring the uniformity and structural integrity required for high-performance devices. Its defining property is its transparency across the 2 to 14 micrometer infrared spectrum, making it unparalleled for critical applications such as thermal imaging lenses, defense targeting systems, and advanced meteorological satellites. The material's high refractive index and low optical dispersion in the IR band allow for the design of smaller, lighter, and more efficient optical systems compared to conventional materials. Moreover, Germanium's high electron mobility, superior to that of silicon, positions it as an essential foundation for compound semiconductors, specifically Silicon-Germanium (SiGe) heterostructures, which are crucial for high-speed, high-frequency radio frequency integrated circuits (RFICs) indispensable in modern communication infrastructure.

The applications driving the market expansion are diversified yet unified by the need for extreme performance and reliability. In the aerospace sector, Monocrystalline Germanium serves as the primary substrate for triple- and quadruple-junction solar cells, offering unmatched conversion efficiency and, crucially, high resistance to radiation damage encountered in Earth orbit and deep space missions, securing the power supply for critical satellite constellations. Simultaneously, the proliferation of infrared technology across commercial sectors—including industrial inspection, preventive maintenance in manufacturing, and sophisticated security surveillance—is creating new, high-volume opportunities for standard and mid-grade Germanium optics. The inherent benefits of using Mono-Ge, such as device miniaturization, enhanced signal integrity, and the capability to operate reliably in harsh thermal and mechanical environments, significantly enhance the competitive advantage for system builders, driving its increasing adoption in mission-critical systems where failure is unacceptable.

Key driving factors for the sustained market growth include escalating global military modernization efforts, particularly in the Middle East and Asia Pacific, which necessitate robust night vision and surveillance capabilities. Furthermore, the global shift towards advanced telecommunications, including the rapid rollout of 5G and research into 6G networks, places immense pressure on semiconductor manufacturers to deliver faster components, favoring SiGe-based RFICs built on Germanium substrates. While demand remains robust, the market faces structural challenges, primarily stemming from the complex supply chain of elemental Germanium, which is mined almost exclusively as a byproduct. This dependency on primary metal production output introduces inherent volatility and necessitates strategic industry focus on developing comprehensive recycling programs and diversifying primary sourcing regions to ensure long-term stability and continued technological development across all application segments.

The Monocrystalline Germanium market is experiencing a period of strategic transformation, characterized by aggressive technological refinement aimed at enhancing material purity and wafer size. Business trends reveal a pronounced focus on vertical integration, particularly among companies that possess both raw Germanium refining capabilities and advanced crystal growth expertise. This integration strategy is a direct response to the escalating geopolitical risk associated with raw material sourcing, allowing integrated firms to better control costs, maintain quality consistency, and ensure a dedicated supply stream for their high-value downstream products, notably large-diameter wafers (4-inch to 8-inch) crucial for high-volume semiconductor processing. Furthermore, there is a distinct business trend toward specialization, with certain manufacturers focusing exclusively on ultra-high purity (99.9999%+) substrates for aerospace applications, while others concentrate on cost-effective, high-volume production of IR optical blanks for commercial thermal cameras, segmenting the competitive landscape effectively based on quality and scale.

Regional trends distinctly highlight the Asia Pacific (APAC) region as the epicenter of future market growth, driven by massive domestic investments in semiconductor fabrication, particularly in compound semiconductors which leverage Germanium. The APAC region is rapidly expanding its consumer electronics and telecommunication infrastructure, necessitating high volumes of SiGe components. Concurrently, North America and Europe maintain their technological leadership, focusing strategically on advanced military procurement and sophisticated R&D into next-generation photonics and quantum technologies utilizing Germanium. Geopolitical factors, specifically tariffs and trade restrictions impacting Germanium exports from key producing nations, are driving policy changes in North America and Europe aimed at fostering domestic Germanium extraction and refining independence, potentially leading to the formation of protected regional supply ecosystems characterized by high regulatory compliance and stability, albeit at potentially increased material costs.

Segmentation analysis underscores the enduring dominance of the Infrared Optics application segment in terms of market volume and immediate revenue, sustained by ongoing global defense modernization cycles and the increasing industrial use of predictive thermal inspection tools. However, the highest growth velocity is observed within the Semiconductors/Electronics segment, largely fueled by the pervasive rollout of 5G/6G communication systems where SiGe outperforms conventional silicon, offering superior power efficiency and operational frequency. The purity grade trend emphasizes an irreversible shift towards six-nines purity (99.9999%) and above, as the sensitivity and resolution requirements of both IR sensors and advanced electronic substrates become increasingly demanding. This trend necessitates continuous investment in ultra-clean processing technologies and advanced metrology to certify material quality, directly impacting the operational expenditure and capital expenditure models of major Germanium manufacturers worldwide.

Analyzing user search queries reveals a pronounced interest in how Artificial Intelligence (AI) can mitigate the substantial manufacturing complexities inherent in Monocrystalline Germanium production. Users frequently ask about AI's potential to revolutionize the Czochralski growth process, a technique notorious for its sensitivity to minute environmental fluctuations. Key concerns center on whether AI-driven process control can reliably achieve uniform crystal structure, eliminate micro-defects, and increase the recoverable yield from each ingot, especially when attempting to grow larger, 8-inch diameter wafers. Furthermore, the role of AI in analyzing global Germanium supply chain data—including byproduct ore output, refining capacity, and geopolitical export policy shifts—is a major point of inquiry, as stable sourcing is paramount for consistent manufacturing. The core user expectation is that AI will introduce a level of precision and predictive capability previously unattainable, thereby addressing both manufacturing inefficiency and supply chain vulnerability simultaneously.

AI is strategically deployed across the manufacturing lifecycle of Monocrystalline Germanium, beginning with sophisticated computational modeling. Machine learning algorithms analyze vast historical data sets relating to crystal pulling dynamics, including heater temperatures, melt convection patterns, and rotation speeds. By creating precise digital twins of the growth environment, AI systems can predict and proactively counteract the formation of dislocations, twinning, and impurity segregation in real-time. This precise, automated adjustment leads to a substantial improvement in the homogeneity and purity of the resulting Germanium ingot, which is crucial for achieving the low defect density required for high-performance semiconductor substrates and diffraction-limited IR lenses. This technological enhancement reduces scrap rates, boosts overall production efficiency, and allows manufacturers to achieve more consistent quality metrics required by demanding defense and aerospace contracts, significantly lowering the effective production cost per qualified wafer.

Beyond manufacturing, AI profoundly impacts the downstream demand profile for Monocrystalline Germanium. The rapid expansion of AI infrastructure—including data centers, high-performance computing clusters, and specialized neuromorphic chips—necessitates components capable of extremely high-speed data processing and minimal latency. Germanium, through its incorporation into SiGe HBTs and optical interconnects, delivers the high electron mobility and speed necessary to meet these AI operational demands. Moreover, the integration of AI into advanced autonomous systems, such as self-driving cars, industrial robotics, and military reconnaissance platforms, relies on high-resolution thermal and visible light fusion imaging. These applications require robust, reliable Monocrystalline Germanium IR optics to provide the input data necessary for AI algorithms to function effectively in all weather and lighting conditions. Thus, AI simultaneously optimizes the supply side through enhanced manufacturing control and escalates the demand side through the fundamental hardware requirements of AI-enabled systems.

The overarching dynamics of the Monocrystalline Germanium market are shaped by compelling Drivers that ensure persistent demand, significant Restraints that impede growth realization, and strategic Opportunities that promise future expansion, creating complex Impact Forces. The primary Driver is the inexorable increase in global defense expenditure, particularly focused on tactical superiority which relies heavily on advanced thermal sensors and surveillance systems. Germanium's status as the preferred material for long-wave infrared (LWIR) transmission guarantees continuous high-specification demand from military end-users globally. A parallel critical driver is the technological advancement in telecommunications, where the move towards 5G advanced and future 6G standards demands semiconductor components—specifically SiGe Heterojunction Bipolar Transistors (HBTs)—capable of extremely high operating frequencies and superior power efficiency, capabilities uniquely enabled by Monocrystalline Germanium substrates.

Conversely, the market is severely restricted by its dependence on raw Germanium, a critical mineral that is recovered primarily as a byproduct of zinc smelting or coal fly ash processing, making its supply inherently inelastic and highly susceptible to the operational decisions of unrelated primary metal industries. This structural dependency is compounded by acute geopolitical risk, notably export quotas and restrictions imposed by major Germanium refiners, which can instantly trigger massive price spikes and acute shortages, destabilizing manufacturing schedules globally. Furthermore, the specialized manufacturing required to achieve five- and six-nines purity is extremely capital intensive, requiring highly specialized cleanroom environments and long cycle times (Czochralski pulling), resulting in high unit costs that limit adoption in broader, more cost-sensitive commercial applications, where cheaper alternatives like specialized glasses or zinc sulfide might suffice, particularly for lower-resolution systems.

The strategic Opportunities provide pathways to overcome these restraints and sustain long-term expansion. The burgeoning market for autonomous vehicle sensing, including sophisticated LiDAR and enhanced night vision systems, presents a massive new commercial demand vector for rugged, reliable Germanium optics, moving consumption beyond the defense sector. Similarly, the rapid deployment of thousands of LEO (Low Earth Orbit) satellites by private companies represents a sustained, high-value opportunity for Monocrystalline Germanium multi-junction solar cells, which are irreplaceable due to their high efficiency and radiation tolerance. Crucially, addressing the supply constraint through strategic investment in advanced Germanium recycling technologies—recovering the element from obsolete IR lenses and electronic scrap—offers a transformative opportunity to create a circular economy, reduce reliance on volatile primary sourcing, and secure long-term raw material stability for the entire high-tech value chain, fundamentally altering the market's risk profile.

The Monocrystalline Germanium market structure is defined by critical technical parameters, primarily Purity Grade, which acts as a gateway to specific high-tech applications, and by End-Use Application, which dictates volume requirements and technical specifications. Purity is paramount because even parts-per-million impurities can severely compromise the performance of advanced semiconductor devices or the transmission characteristics of IR optics, leading to stringent segregation into categories like five-nines and six-nines. Application segmentation clearly delineates the market drivers, with defense-related Infrared Optics representing the largest immediate revenue generator, while the complex, high-specification demands of the Semiconductor segment point towards the most dynamic future growth trajectory, emphasizing the market’s technological diversity.

The Monocrystalline Germanium value chain is intricate, commencing with the highly centralized upstream extraction phase. Germanium is predominantly sourced as a trace byproduct, mainly from the residues of zinc smelting or specific coal ash combustion. Key players involved in this initial phase focus on hydrometallurgical or pyrometallurgical refining processes to isolate Germanium from the host ore and then reduce the resulting Germanium dioxide (GeO2) to high-purity Germanium metal. This upstream activity is structurally characterized by high geographical concentration, making it extremely sensitive to trade policies and mining output fluctuations. Successful management of the upstream segment demands long-term contractual agreements with primary producers and substantial investment in proprietary purification technologies to guarantee the feedstock quality necessary for subsequent crystal growth, directly influencing the final cost and purity of the monocrystalline product.

The midstream transformation represents the most technologically demanding and value-additive stage. This involves using advanced techniques, primarily the Czochralski method, to melt the high-purity Germanium metal and slowly pull a single-crystal ingot. This process is meticulously controlled, often leveraging AI-driven systems, to ensure precise crystallographic orientation (e.g., [100] or [111]) and uniform doping, crucial for semiconductor applications. Once the ingot is grown, it undergoes precision cutting, lapping, and chemo-mechanical polishing (CMP) to produce highly planar, defect-free wafers, often 4 or 6 inches in diameter, though the industry is pushing towards 8-inch standards. The distribution of these specialized wafers is typically direct (Direct Channel), as the high unit value and custom technical specifications necessitate close collaboration between the wafer manufacturer and the component fabricator (e.g., semiconductor foundries or advanced optical coating houses), facilitating detailed technical support and non-disclosure agreements.

The downstream element centers on the integration of Monocrystalline Germanium components into complex final products. For the defense sector, Germanium optical blanks are shaped, polished, and coated to form mission-critical IR lenses and windows, often sold indirectly through large, multinational defense prime contractors (Indirect Channel) to government military agencies. In the semiconductor realm, Germanium wafers serve as the foundational substrate upon which epitaxial layers of SiGe or other III-V materials are grown, creating the finished integrated circuits. These ICs are then sold to telecommunication equipment providers, automotive electronics specialists, or consumer device manufacturers. The demand signals originating from these diverse end-users—ranging from the military's requirement for extreme resilience to the consumer electronics sector's demand for high-volume, low-cost components—determine the specifications and scale required at every preceding stage of the value chain, illustrating the critical pull effect of downstream technological advancements on upstream material processing innovation.

The customer landscape for Monocrystalline Germanium is dominated by entities operating at the forefront of high technology and national security, where material performance overrides cost considerations. The defense and aerospace sectors constitute the highest-value customer segment, encompassing government defense agencies, large prime contractors (like Lockheed Martin, Raytheon), and specialized manufacturers of missile guidance systems and space-borne sensors. These organizations require Monocrystalline Germanium for its superior performance in the thermal infrared band and its radiation tolerance, demanding ultra-high purity, certified six-nines grade material, and precise optical finishing. Their procurement cycles are characterized by long lead times, stringent qualification processes, and multi-year supply contracts, reflecting the strategic importance of ensuring a robust and reliable supply for mission-critical hardware that cannot tolerate material failure.

A rapidly expanding customer base is found within the global semiconductor and telecommunication industries. Major foundries and integrated device manufacturers (IDMs) specializing in high-speed connectivity chips (RFICs for 5G/6G base stations, high-performance computing, and automotive radar) are primary consumers of Germanium wafers. These customers leverage the high electron mobility of Germanium to overcome the frequency limitations of standard silicon, often utilizing Monocrystalline Germanium substrates to grow complex SiGe heterostructures. This segment is highly cost-sensitive to yield and wafer diameter but places immense value on crystal perfection and purity consistency, essential for maximizing integrated circuit performance and yield rates during mass production. The demand from this sector is closely correlated with global investment cycles in digital infrastructure modernization and consumer electronics saturation.

Emerging and specialized customer segments include manufacturers of advanced sensing technologies for autonomous systems and the rapidly evolving commercial space industry. Automotive suppliers developing sophisticated LiDAR and night vision cameras for Level 3 and Level 4 autonomous driving systems are increasing their uptake of Germanium optics due to the need for robust, all-weather performance. Concurrently, commercial satellite constellation operators (e.g., SpaceX Starlink, OneWeb) represent crucial customers for Monocrystalline Germanium solar cell substrates, demanding materials that offer superior power-to-weight ratios and resilience against solar flare damage. Furthermore, academic research groups and national laboratories conducting fundamental research in areas like quantum computing and advanced photonics often require smaller quantities of ultra-pure Monocrystalline Germanium for R&D purposes, testing novel device architectures and exploring new technological frontiers for materials integration.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $150 Million USD |

| Market Forecast in 2033 | $280 Million USD |

| Growth Rate | 9.3% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Umicore, Teledyne FLIR, China Germanium Co., Ltd., PPM Pure Metals GmbH, AXT Inc., JSC Germanium, Photonic Sense GmbH, Yunnan Lincang Xinyuan Germanium Industry Co., Ltd., Nanjing Germanium Co., Ltd., Wafer World Inc., Thermo Fisher Scientific, Materion Corporation, 5N Plus Inc., Albemarle Corporation, Alfa Aesar, IQE plc, II-VI Incorporated (Coherent), Sumitomo Electric Industries, Recycling Technologies International, Indium Corporation. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The core technological pillar of the Monocrystalline Germanium market is the rigorous refinement and crystallization process, headlined by the Czochralski (CZ) method, which must be continuously optimized to meet escalating purity and dimensional demands. Current technological advancements focus heavily on achieving larger crystal diameters, pushing from the standard 4-inch or 6-inch wafers toward 8-inch substrates, which significantly reduces the cost per chip area and improves throughput for semiconductor manufacturers. This requires sophisticated engineering solutions, including the implementation of magnetic fields (Magnetic Czochralski, or MCZ) during growth to suppress turbulent melt convection, thereby reducing the incorporation of harmful defects, specifically dislocations and swirl defects, and ensuring a uniform resistivity profile across the entire wafer surface, essential for high-yield device fabrication in advanced semiconductor fabs.

In the domain of applications, two critical technological trends stand out: advanced epitaxial growth and precision optical processing. For the semiconductor segment, Metal-Organic Chemical Vapor Deposition (MOCVD) and Molecular Beam Epitaxy (MBE) are the prevailing techniques used to deposit highly controlled, thin layers of SiGe or III-V materials onto the Germanium substrate. Technological innovation here focuses on reducing lattice mismatch stress, which directly impacts the performance and longevity of the resulting transistors and optical emitters. For infrared optics, the development of sophisticated anti-reflection (AR) coatings, often multilayered thin-film structures, is vital to minimize surface reflections and maximize transmission efficiency in the crucial 8-12 µm atmospheric window. Furthermore, diamond turning and ultra-precision grinding technologies are continually being refined to produce highly accurate aspheric and diffractive lens elements from Monocrystalline Germanium, enabling performance optimization and lens miniaturization for next-generation thermal systems.

Looking forward, critical technologies are emerging to address supply chain resilience and material integration. Germanium recycling technology, specifically high-purity chemical separation techniques designed to recover Germanium from end-of-life IR equipment and electronic waste, is gaining strategic investment as a crucial method for supply stabilization. Simultaneously, the exploration of Germanium integration into silicon photonics via specialized bonding or selective growth techniques is a key technological frontier. Leveraging Germanium's quasi-direct bandgap property for integrated photodetectors and light sources on silicon chips promises to revolutionize optical data transmission within microprocessors and data centers, driving new, high-volume technological demand. The rigorous implementation of advanced metrology, including high-resolution electron microscopy and sophisticated elemental analysis (e.g., ICP-MS), remains foundational to certifying that the monocrystalline material adheres to the extremely tight specifications required by space and defense customers.

Regional consumption patterns for Monocrystalline Germanium are deeply entrenched in the distribution of global high-tech manufacturing and defense industrial bases, creating highly differentiated market dynamics across geographical areas. Asia Pacific (APAC) represents both the primary manufacturing powerhouse and the fastest-growing consumer market. Driven by massive national strategic investments in semiconductor self-sufficiency, particularly in China, South Korea, and Taiwan, the demand for Germanium substrates for SiGe and III-V compound semiconductors is exploding. Furthermore, the region’s increasing defense budgets, coupled with indigenous development of advanced satellite and surveillance technologies, ensures a relentless, escalating need for high-quality IR optics. China’s dual role as a major raw material supplier and a burgeoning high-tech manufacturer gives the region immense leverage, though this also introduces significant regulatory complexity for international buyers.

North America, led by the United States, stands as the most mature and technologically demanding market, characterized by unparalleled investment in defense, aerospace, and advanced R&D. Demand here is dominated by the military industrial complex, requiring the absolute highest purity and specification materials for high-value programs like missile defense and advanced fighter jet sensors. The regulatory environment strongly favors domestic production or sourcing from stable, allied nations to mitigate geopolitical risk, translating into higher investment in advanced domestic refining and crystal growth facilities. Europe maintains a strong, stable demand profile, particularly in specialized industrial automation, high-end automotive safety systems (using thermal vision), and key defense R&D centers. European manufacturers focus on high-precision products and are actively pursuing supply diversification strategies in response to critical raw material mandates from the European Union, stabilizing their supply chain through strategic partnerships outside of traditional sources.

The emerging markets of the Middle East and Africa (MEA) and Latin America (LATAM) show promising, albeit smaller-scale, growth trajectories. In the MEA region, market expansion is primarily fueled by extensive national security modernizations, border surveillance initiatives, and critical infrastructure monitoring (e.g., oil and gas pipelines), all relying on robust thermal imaging systems. LATAM's growth is tied mainly to military modernization programs and limited adoption of commercial IR technology in mining and environmental monitoring. These regions largely depend on imported, finished Germanium components and systems from North America, Europe, and APAC. The growth in these areas is highly contingent upon local economic stability and governmental capital investment in security and infrastructure projects, positioning them as key future importers of Monocrystalline Germanium-enabled systems.

Monocrystalline Germanium is primarily used as the material for high-performance infrared (IR) optics, including lenses and windows for thermal imaging cameras, and as a substrate for high-efficiency multi-junction solar cells used in space applications and advanced Silicon-Germanium (SiGe) electronic devices for 5G/6G communication systems. Its core utility is its transparency to long-wave infrared radiation and its high electron mobility.

The Monocrystalline Germanium supply chain is highly sensitive because Germanium is mainly a byproduct of zinc refining. Geopolitical actions, such as export restrictions imposed by major producing countries, directly lead to reduced material availability, extreme price volatility, and increased sourcing risk, compelling end-users to secure long-term contracts and prompting increased investment in domestic and recycling capabilities.

The Semiconductors/Electronics segment is projected to exhibit the highest Compound Annual Growth Rate (CAGR). This acceleration is driven by the rapid adoption of Silicon-Germanium (SiGe) technology for high-frequency RF integrated circuits and specialized components necessary for next-generation telecommunications (5G and 6G) and high-speed radar systems, where Germanium offers superior operational parameters.

Monocrystalline Germanium offers significantly higher electron mobility compared to pure silicon. This superior characteristic allows for the fabrication of faster, more energy-efficient transistors (HBTs) that operate effectively at higher frequencies and temperatures, making it essential for advanced military radar, satellite communication, and high-performance computing components where speed and thermal resilience are critical design constraints.

Key technological advancements include improving the Czochralski crystal growth method to yield larger, defect-free wafers (e.g., 8-inch substrates) to enhance manufacturing economics, developing effective Germanium recycling processes to ensure sustainable supply, and refining anti-reflective coatings for enhanced infrared optical performance in extreme environments such as aerospace and defense.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.