ID : MRU_ 434007 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

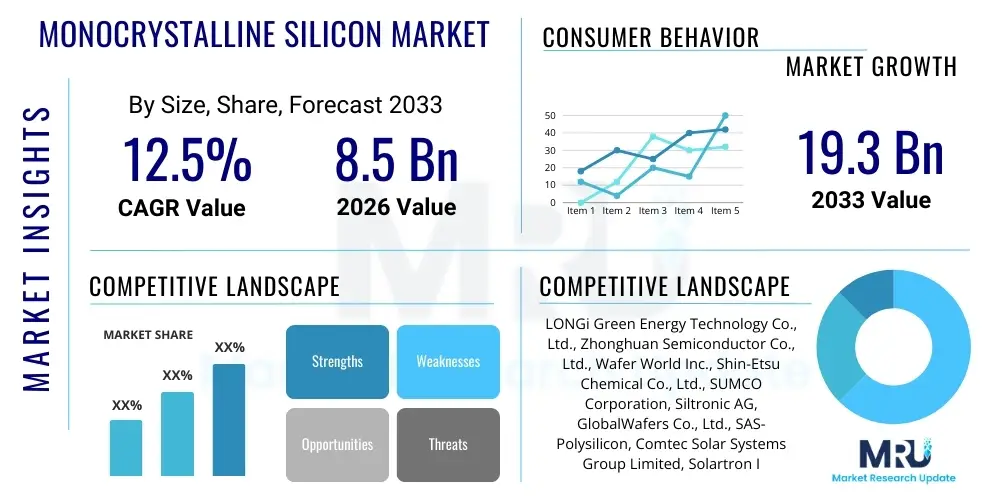

The Monocrystalline Silicon Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2026 and 2033. The market is estimated at USD 8.5 Billion in 2026 and is projected to reach USD 19.3 Billion by the end of the forecast period in 2033.

Monocrystalline silicon, often referred to as single-crystal silicon, is a critical foundational material characterized by a continuous, unbroken crystal lattice structure extending throughout the entire ingot. This uniformity eliminates the grain boundaries inherent in polycrystalline silicon, resulting in superior electronic properties, including higher electron mobility and reduced defect density. Its pristine crystalline structure makes it the preferred material for high-efficiency applications, particularly in the photovoltaic (PV) industry for producing premium solar cells and in the semiconductor sector for manufacturing integrated circuits (ICs) and microprocessors. The purity requirements for semiconductor-grade monocrystalline silicon are significantly higher than those for solar-grade silicon, driving distinct technological pathways in production, such as the Czochralski (CZ) method and Float Zone (FZ) technique.

The primary applications of monocrystalline silicon span across energy generation and advanced electronics. In the solar industry, mono-Si cells achieve higher energy conversion efficiencies compared to multi-crystalline cells, making them essential for utility-scale solar farms and residential installations where space constraints necessitate maximum power output per unit area. Beyond solar, the material is indispensable in modern computing. Every transistor within a high-performance chip is fabricated on a monocrystalline silicon wafer, which acts as the substrate. This widespread adoption is fueled by the material's stable electrical performance, reliability, and the long-established infrastructure for its mass production and processing.

Key driving factors accelerating the market growth include robust governmental support for renewable energy initiatives, rapidly declining costs of solar PV technology making it competitive with traditional energy sources, and the relentless demand for smaller, faster, and more powerful electronic devices. The transition to advanced packaging techniques and the emergence of specialized semiconductor applications like photonics and MEMS (Micro-Electro-Mechanical Systems) further solidify the material's market position. However, production is complex, involving high-temperature processes and stringent control over impurity levels, which dictates a high barrier to entry and continuous investment in advanced manufacturing techniques to meet ever-increasing purity and size demands.

The Monocrystalline Silicon Market exhibits dynamic growth primarily propelled by the exponential expansion of the global solar photovoltaic (PV) sector and sustained, high-volume demand from the semiconductor industry. Business trends indicate a significant shift towards larger wafer sizes, specifically 182mm (M10) and 210mm (G12) diameters in the solar segment, as manufacturers strive to reduce Balance of System (BoS) costs and improve module power output. Strategic consolidation among major ingot and wafer producers is optimizing the supply chain, enabling economies of scale and driving down material costs, which in turn fuels end-user affordability and market penetration. Furthermore, there is an increasing focus on developing advanced crystallization techniques to enhance material quality and minimize energy consumption during the production process, responding to industry pressure for sustainable manufacturing practices and stricter quality control standards necessary for next-generation electronic components.

Regional trends highlight the dominance of the Asia Pacific (APAC) region, specifically China, which accounts for the vast majority of global monocrystalline silicon production and consumption, driven by massive domestic solar installations and a robust, vertically integrated semiconductor supply chain. North America and Europe are experiencing accelerated demand, not primarily for material production, but for consumption in advanced technology sectors like high-performance computing, data centers, and specialized sensor manufacturing. Government policies, such as the European Green Deal and U.S. incentives for domestic solar manufacturing and semiconductor fabrication (CHIPS Act), are poised to diversify the supply chain geographically, reducing dependency on a single region and stimulating local capacity build-up, thus impacting regional competitive dynamics over the forecast period.

Segment trends underscore the criticality of the solar grade segment, which holds the largest market share by volume due to high adoption rates in utility-scale projects. However, the semiconductor grade segment is anticipated to witness the fastest growth in terms of value, driven by the increasing complexity of microprocessors (necessitating ultra-high purity silicon) and the rapid adoption of specialized applications like 5G infrastructure, electric vehicles (EVs), and artificial intelligence hardware. Technological advancements such as N-type silicon wafers, which offer superior performance and resistance to light-induced degradation (LID) compared to traditional P-type wafers, are reshaping segment preferences, pushing manufacturers to modernize their crystallization facilities and adjust doping strategies to capture premium market opportunities.

Common user questions regarding AI's impact on the Monocrystalline Silicon Market primarily revolve around two themes: optimization of manufacturing processes and AI-driven growth in demand for high-performance computing substrates. Users are keenly interested in how Artificial Intelligence and Machine Learning (ML) can improve the notoriously complex and energy-intensive Czochralski and Float Zone crystallization methods, seeking to understand if AI can reduce defect rates, optimize thermal gradients, and enhance crystal uniformity, thereby boosting yield and reducing operational costs. Simultaneously, there is significant inquiry into the indirect effect, recognizing that the rapid proliferation of generative AI models, large language models (LLMs), and deep learning requires immense processing power, leading to an explosive demand for advanced GPUs and specialized AI accelerators, all fundamentally built on high-purity monocrystalline silicon wafers. The overarching expectation is that AI will act both as a critical tool for operational efficiency and as a major catalyst for sustained end-market growth for the material.

The market for monocrystalline silicon is highly influenced by a critical balance of dynamic drivers, inherent restraints, and compelling opportunities that collectively determine its trajectory. The primary driver remains the overwhelming global shift towards renewable energy, supported by stringent climate policies and subsidies, which mandates the continued expansion of high-efficiency solar power generation. Concurrently, the unceasing demand for advanced computing power, fueled by digitization, 5G deployment, IoT, and AI, necessitates a constant supply of ultra-high purity silicon substrates for advanced semiconductor manufacturing. These powerful demand-side forces, coupled with manufacturing innovations that have consistently reduced the Levelized Cost of Energy (LCOE) for solar PV, create a robust environment for sustained market expansion and significant capital investment in capacity augmentation across Asia.

However, the market faces notable restraints, most prominently the extremely high capital expenditure and energy requirements associated with establishing and operating sophisticated crystal growth facilities. The production process, especially the Czochralski method, is energy-intensive, and fluctuations in energy prices directly impact operating margins and pricing strategies. Furthermore, the reliance on a few key regions for raw polysilicon supply introduces geopolitical risk and potential supply chain bottlenecks, contributing to price volatility. Environmental concerns related to the chemical waste generated during polysilicon purification and wafer processing also present a regulatory challenge, requiring continuous investment in green manufacturing technologies and waste remediation efforts to maintain regulatory compliance.

Opportunities for growth are concentrated in technological differentiation and market diversification. The shift towards N-type wafer technology (e.g., TOPCon and HJT cells) provides a significant growth avenue, as these architectures require monocrystalline silicon and offer superior performance margins. Additionally, the increasing demand for specialized silicon materials in non-traditional applications—such as Silicon Carbide (SiC) and Silicon on Insulator (SOI) wafers, which are processed using silicon as a base—for high-power electronics and automotive applications represents a high-value niche opportunity. The ongoing trend of regionalizing supply chains, spurred by government incentives in North America and Europe, also creates localized opportunities for new manufacturing entrants and technology providers focused on enhancing domestic resilience and reducing external supply dependencies.

The Monocrystalline Silicon Market is strategically segmented based on purity level (grade), production method, application, and end-user, reflecting the diverse and stringent requirements of its consumer base. Segmentation by grade, encompassing solar grade and semiconductor grade, is crucial as it dictates material cost, production complexity, and ultimate use case. Solar grade silicon, while dominant in volume, tolerates higher impurity levels compared to semiconductor grade, which mandates parts per trillion (ppt) purity for advanced chip manufacturing. The differentiation in production methods, primarily Czochralski (CZ) and Float Zone (FZ), further segments the market, with CZ being cost-effective and suitable for large-scale solar wafers, while FZ is preferred for ultra-high purity applications like power electronics and detectors due to its superior defect control.

Application-based segmentation provides insight into the primary consumption drivers, with Photovoltaic (PV) cells representing the largest segment, driven by global energy transitions. The Electronics & Semiconductor segment, although smaller by volume, commands a substantially higher market value due to the specialized nature and complex processing required for ICs, microprocessors, and memory chips. End-user segmentation mirrors this, focusing on large-scale solar panel manufacturers, semiconductor foundries (fabs), and specialized electronics component producers. Understanding these segments is vital for supply chain planning, investment prioritization, and technological specialization, as the needs of a solar cell producer for 210mm P-type wafers differ drastically from a foundry requiring 300mm N-type wafers for advanced CMOS fabrication.

The growing importance of specialized segments like Silicon on Insulator (SOI) and detector-grade silicon highlights a shift towards high-value, niche markets that offer superior margins. These advanced materials are essential for environments demanding high radiation tolerance or extreme temperature performance, finding applications in aerospace, defense, and high-frequency communication. The continuous miniaturization mandated by Moore's Law, combined with the push for higher efficiency in solar power, ensures that the demand for increasingly pure and precisely engineered monocrystalline silicon substrates will remain strong across all key segments, necessitating continuous innovation in crystal pulling and wafer slicing technologies to maintain market competitiveness and address stringent performance requirements.

The Monocrystalline Silicon value chain is characterized by capital intensity and a sequential transformation of raw materials into high-value components, beginning upstream with the mining of metallurgical-grade silicon (MGS) and culminating in the fabrication of end-user products. The upstream segment involves the energy-intensive process of refining MGS into ultra-high-purity electronic-grade polysilicon, typically through the Siemens process or fluid bed reactor technology. This purification step is highly concentrated geographically and represents a significant bottleneck and cost driver. The subsequent stage involves crystal pulling—the Czochralski or Float Zone process—to produce large monocrystalline ingots. The efficiency and quality achieved at this stage directly determine the value and applicability of the final wafer, demanding rigorous control over temperature, doping, and defect minimization.

Midstream activities involve the highly precise mechanical processing of these ingots into wafers, utilizing technologies such as wire sawing (diamond wire) for slicing and subsequent edge grinding, lapping, and polishing to achieve the required flatness, uniformity, and surface quality. For semiconductor applications, this polishing process is highly sophisticated (Chemical-Mechanical Planarization or CMP) to meet sub-nanometer surface roughness requirements. The distribution channel structure varies significantly by segment. Semiconductor wafers are typically sold directly from the wafer supplier to a limited number of high-volume, global semiconductor foundries (direct distribution), involving complex technical specifications and long-term contracts. In contrast, solar wafers may pass through distributors before reaching cell and module assemblers, although large, vertically integrated solar companies often handle the entire process internally (ingot-to-module).

Downstream activities are defined by the two major applications. In the solar sector, wafers are transformed into solar cells through doping and metallization, then assembled into modules for utility, commercial, or residential use. In the semiconductor sector, the wafer acts as the foundational substrate for complex lithography and fabrication processes conducted in foundries, resulting in integrated circuits, microprocessors, and memory chips. The indirect channels are primarily observed in the secondary market for specialized equipment, consumables (such as slicing wires, slurry, and chemicals), and the provision of technical services. The chain's high concentration in APAC, particularly in ingot and wafer manufacturing, underscores the geopolitical and competitive dynamics influencing global pricing and supply resilience for this foundational material.

The primary customer base for monocrystalline silicon is diversified across sectors requiring materials with superior electrical conductivity, high crystallinity, and thermal stability. The largest volume consumers are Solar Photovoltaic (PV) Cell Manufacturers. These companies, ranging from large, integrated global module suppliers to specialized cell fabricators, utilize solar-grade mono-Si wafers as the core component of high-efficiency solar panels. Their purchasing decisions are heavily influenced by wafer size (M10/G12 standardization), material cost per watt, and the ability of the wafer to support advanced cell architectures like TOPCon and Heterojunction Technology (HJT), demanding high-purity P-type or N-type material tailored for energy conversion performance.

The second major group of customers comprises Semiconductor Foundries and Integrated Device Manufacturers (IDMs). These entities, including major players in logic, memory, and specialized chip production, represent the highest-value market for monocrystalline silicon, requiring semiconductor-grade, ultra-pure wafers (200mm and 300mm) with near-zero crystal defects. Their stringent quality requirements necessitate long-term partnerships with wafer suppliers capable of providing precisely engineered substrates for advanced fabrication nodes (e.g., 7nm, 5nm, and below). The demand in this segment is dictated by global technology cycles, specifically the rapid adoption of AI, cloud computing infrastructure, data centers, and the expansion of the automotive electronics market, particularly electric and autonomous vehicles.

A burgeoning segment of potential customers includes specialized electronics manufacturers focused on niche applications. This encompasses producers of Power Electronics (e.g., IGBTs and MOSFETs for industrial motor drives and EV battery management systems), high-frequency Radio Frequency (RF) devices, and Micro-Electro-Mechanical Systems (MEMS) sensors used in consumer electronics and industrial automation. Furthermore, research institutions and defense contractors purchasing small volumes of specialized Float Zone silicon or Silicon-on-Insulator (SOI) wafers for specialized detectors, aerospace components, and advanced scientific instruments also form a valuable, albeit lower-volume, customer segment. These diverse end-users collectively drive the need for a range of silicon purity, doping types, and wafer specifications, requiring manufacturers to maintain highly flexible production capabilities.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 8.5 Billion |

| Market Forecast in 2033 | USD 19.3 Billion |

| Growth Rate | 12.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | LONGi Green Energy Technology Co., Ltd., Zhonghuan Semiconductor Co., Ltd., Wafer World Inc., Shin-Etsu Chemical Co., Ltd., SUMCO Corporation, Siltronic AG, GlobalWafers Co., Ltd., SAS-Polysilicon, Comtec Solar Systems Group Limited, Solartron Inc., Solar World AG, GCL Technology Holdings Limited, ReneSola Ltd., Crystal Solar, Norcink Inc., Addison Engineering Inc., Norsun AS, Hebei Jingye Group, PV Crystalox Solar PLC. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Monocrystalline Silicon Market is dominated by the continuous refinement of crystal growth and wafer processing techniques, driven by the dual goals of enhancing material purity for semiconductors and maximizing efficiency for solar applications. The Czochralski (CZ) method remains the bedrock of large-scale monocrystalline ingot production, accounting for the vast majority of volume due to its cost-effectiveness and capability to produce large-diameter crystals. Recent CZ advancements focus on magnetic field application (MCZ) to suppress convection within the molten silicon, thereby improving oxygen control and reducing micro-defect density, which is crucial for high-performance solar cells and power devices. Parallelly, the Float Zone (FZ) method, while lower in volume, continues to be the definitive technology for ultra-high purity silicon required for specialized applications like high-power rectifiers and radiation detectors, leveraging its ability to produce silicon with extremely low oxygen and carbon content.

Wafer slicing technology is undergoing a critical transformation, transitioning from traditional slurry wire saws to fixed abrasive diamond wire sawing (DWS). DWS significantly reduces kerf loss (material waste), increases slicing speed, and lowers overall production costs, directly impacting the competitiveness of monocrystalline silicon in the solar market. This technological shift enables the production of thinner wafers without compromising mechanical integrity, leading to reduced silicon consumption per watt of electricity generated. Furthermore, the push towards larger wafer formats, specifically 182mm (M10) and 210mm (G12) in the PV sector, necessitates optimization of crystal growth equipment and saw machines to handle the increased mechanical stress and thermal mass associated with these larger ingots, demanding continuous capital upgrades across the supply chain.

In the semiconductor arena, the focus is on achieving tighter specifications for surface quality and internal defect management. Techniques such as epitaxial growth are used to deposit a high-quality silicon layer onto a base substrate, often crucial for high-speed devices. Advanced metrology, including techniques like scanning electron microscopy (SEM) and atomic force microscopy (AFM), combined with sophisticated crystal defect detection systems (e.g., using light scattering), ensures that the produced wafers meet the extremely rigorous standards necessary for sub-10 nanometer fabrication processes. Furthermore, innovations in silicon recycling and reclaim processes are gaining traction, aiming to recover and re-polish used test wafers, contributing to resource efficiency and addressing sustainability concerns within the high-volume semiconductor industry, thus forming an important part of the broader technology ecosystem.

The geographical landscape of the Monocrystalline Silicon market is heavily skewed towards Asia Pacific (APAC), which serves as the global epicenter for both production capacity and consumption, particularly driven by the immense scale of China’s solar PV industry and its dominance in semiconductor manufacturing. However, regional market dynamics are increasingly being influenced by governmental policies in North America and Europe aimed at supply chain localization and resilience.

Monocrystalline silicon (mono-Si) has a single, continuous crystal structure, resulting in higher efficiency (typically 2-4% greater) and better aesthetic uniformity, making it preferred for premium solar panels. Polycrystalline silicon (poly-Si) consists of multiple crystals, making it cheaper to produce but resulting in lower electron mobility and overall efficiency due to grain boundaries.

The shift to N-type monocrystalline wafers (supporting technologies like TOPCon and HJT) is a major trend driving demand. N-type wafers offer superior performance, lower degradation rates (LID/LETID), and higher bifaciality compared to traditional P-type wafers, requiring monocrystalline manufacturers to upgrade production lines to handle the necessary phosphorus doping and crystallization precision.

The 300mm (12-inch) wafer is the current standard for mass-producing high-density integrated circuits (ICs), including microprocessors and memory chips. Utilizing larger wafers maximizes the number of chips (die) produced per wafer, significantly lowering manufacturing costs per chip, which is essential for advanced fabrication nodes (e.g., 7nm and 5nm technology).

The two main methods are the Czochralski (CZ) method, which is cost-effective and dominates solar and general semiconductor wafer production, and the Float Zone (FZ) method, which produces ultra-high purity, low-defect silicon used for specialized power electronics, high-voltage devices, and radiation detectors.

Geopolitical strategies, such as the U.S. CHIPS Act and European initiatives, aim to diversify and regionalize the supply chain away from the high concentration of manufacturing in China. This is creating new opportunities and investment for domestic production capacity in North America and Europe, specifically targeting high-purity semiconductor-grade silicon to reduce reliance on foreign imports.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.