ID : MRU_ 434195 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

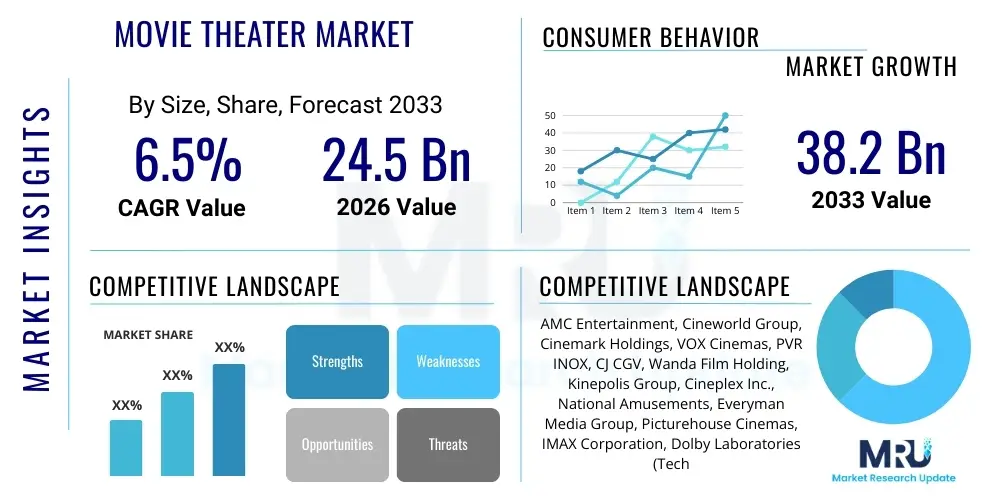

The Movie Theater Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at $24.5 Billion in 2026 and is projected to reach $38.2 Billion by the end of the forecast period in 2033.

The Movie Theater Market, encompassing the global exhibition industry, primarily generates revenue through ticket sales (admissions) and concessions (food and beverages). This sector serves as a crucial application for major film distribution, offering communal entertainment and an unparalleled cinematic experience that differentiates it from home viewing. Key benefits include superior technical presentation, immersive soundscapes, and the social aspect of viewing blockbusters. The market is fundamentally driven by the consistent supply of high-quality content from major studios, advancements in projection and audio technologies such as laser projection and Dolby Atmos, and the increasing consumer preference for premium, out-of-home entertainment experiences, especially in emerging economies. Product offerings continually evolve, incorporating premium formats like IMAX, 4DX, and other large-screen options to justify higher ticket prices and maintain competitiveness against sophisticated home entertainment systems. Furthermore, marketing strategies focused on experiential viewing are vital in driving foot traffic and overcoming the challenges posed by shorter theatrical windows.

The global Movie Theater Market is exhibiting resilience and strategic pivots, summarized by a strong focus on experiential cinema and operational efficiency. Business trends are defined by the proliferation of Premium Large Formats (PLFs) and variable pricing models, shifting the revenue mix towards higher Average Ticket Prices (ATPs). Exhibitors are heavily investing in reclining seats, dining options, and enhanced loyalty programs to maximize per-capita spending, thereby mitigating volume volatility. Regionally, Asia Pacific (APAC) stands out as the primary growth engine, fueled by rapid expansion in China and India, increased disposable incomes, and lower cinema density compared to established Western markets. Conversely, North America and Europe are focusing on modernization and consolidation, utilizing dynamic pricing and strategic venue closures to optimize real estate portfolios. Segment trends indicate a sustained preference for 3D and immersive formats, particularly for action and science fiction genres, alongside a notable resurgence in the importance of concessions revenue, which often boasts significantly higher margins than ticket sales, serving as a critical differentiator for overall market profitability.

Analysis of common user questions regarding AI's influence on the Movie Theater Market reveals significant concerns and expectations clustered around three main areas: personalized experience optimization, operational cost reduction, and the competitive threat posed by AI-driven content platforms. Users frequently inquire about how AI can personalize the entire customer journey, from predicting film preferences and optimizing seat selection to customizing concession promotions based on historical purchasing data and demographic profiles. Simultaneously, there is strong interest in AI's role in streamlining back-of-house operations, such as automated scheduling for staff, predictive maintenance for projectors and sound systems, and optimizing HVAC systems for energy efficiency. A core competitive theme revolves around whether studios will leverage AI for hyper-efficient content creation and distribution, potentially shortening theatrical windows or creating compelling, personalized home experiences that further erode the need for out-of-home viewing. These themes underscore a market seeking technological leverage to enhance margins and experience quality while simultaneously grappling with disruption.

AI’s deployment is fundamentally transforming the operational core of cinema exhibition, moving beyond simple data analytics to deep learning applications that drive profitability. Dynamic pricing algorithms, for instance, utilize real-time data on seat occupancy, weather conditions, local events, and competitor pricing to set optimal ticket prices for every showtime, maximizing yield management. Furthermore, AI is increasingly critical in managing content scheduling and inventory; machine learning models predict the long-tail performance of films, allowing exhibitors to allocate screens efficiently, ensuring that high-demand content receives maximum screen time while minimizing losses on underperforming features. This data-driven approach to scheduling minimizes waste and ensures optimal utilization of high-capital assets like PLF screens, which are central to modern cinema revenue strategy.

Beyond internal operations, AI is the key differentiator in enhancing the front-end customer experience, making the physical visit more seamless and personalized. AI-powered recommendation engines, integrated into mobile apps and ticketing kiosks, suggest not only films but also seating arrangements and premium upgrades based on individual viewing history and perceived willingness to pay. This personalization extends to concessions, where point-of-sale systems use facial recognition or loyalty data to trigger customized offers for snacks and beverages, boosting the high-margin secondary revenue stream. Moreover, AI-driven chatbots and virtual assistants are being deployed to handle routine customer service inquiries, such as ticket changes or directions, ensuring that human staff can focus on providing high-touch service during peak hours, thereby increasing overall customer satisfaction and loyalty in a highly competitive entertainment landscape.

The Movie Theater Market is influenced by a complex interplay of Drivers, Restraints, and Opportunities, shaping its trajectory and competitive intensity. A primary driver is the enduring success of global blockbuster franchises and the high-production value cinematic content that necessitates a big-screen presentation to be fully appreciated, maintaining the critical differentiation from smaller screens. Technological innovation, particularly the widespread adoption of laser projection and immersive sound technologies (like Dolby Atmos and DTS:X), continues to enhance the consumer value proposition, justifying premium ticket prices. Furthermore, demographic shifts in high-growth regions, characterized by increasing urbanization and a growing middle class with higher discretionary spending, significantly boost cinema attendance. These factors collectively push exhibitors toward continuous investment in capital improvements, transforming the standard movie outing into a diversified, high-value entertainment event.

Conversely, the market faces profound restraints, primarily driven by competitive forces and infrastructure costs. The most significant restraint is the acceleration of Direct-to-Consumer (D2C) streaming models and the resulting shorter theatrical exhibition windows, reducing the exclusivity period cinema relies upon. This compressed window diminishes the market’s control over content longevity and consumer urgency. High capital expenditure required for continuous technological upgrades (e.g., shifting from Xenon lamps to laser projectors, implementing PLF formats) presents a barrier, especially for smaller, independent cinema chains. Moreover, persistent challenges like widespread digital piracy, which is challenging to control globally, and fluctuations in the content supply chain due to production delays or labor issues, introduce volatility and uncertainty into year-over-year revenue forecasts, demanding proactive risk management strategies from market players.

Despite these challenges, substantial opportunities exist, centered on maximizing the physical space and diversifying revenue streams. The expansion of "Event Cinema," featuring live broadcasts of concerts, sports, theatrical performances, and gaming tournaments, effectively utilizes screen capacity during non-peak hours and attracts new demographic segments. The development of subscription and loyalty models (e.g., AMC Stubs A-List, Cineworld Unlimited) is crucial for securing recurring attendance and reducing the price sensitivity of frequent moviegoers, stabilizing core demand. Additionally, geographic expansion into underserved emerging markets, coupled with strategic consolidation in mature markets, provides avenues for efficiency gains and overall market penetration. The trend toward enhanced food and beverage offerings, including full-service dining concepts and premium alcohol sales, represents a high-margin opportunity to significantly increase per-capita spending and improve the overall profitability of the exhibition model.

The Movie Theater Market is comprehensively segmented based on key operational and revenue drivers, reflecting the diverse ways consumers experience cinematic content and how exhibitors monetize that experience. Primary segmentation includes the screen type (2D, 3D), which dictates technical requirements and ticket pricing; the revenue stream (admissions, concessions, advertising), defining the profitability structure of the business; the exhibition format (IMAX, Standard, 4DX), representing the level of technological immersion offered; and the geographical region, which influences market growth rates and content preferences. Understanding these segments is vital for exhibitors planning capital allocation and for studios determining distribution strategies, as consumer willingness to pay varies significantly based on the format and the overall perceived value of the viewing experience.

The Movie Theater Market value chain is a highly interconnected system that begins with content creation and culminates in the consumer experience. Upstream activities are dominated by production studios and distributors (e.g., Disney, Warner Bros., Universal), which finance, create, and market the films. This phase involves substantial risk and capital investment, with studios dictating the release schedule and negotiating the critical split of box office revenues with exhibitors. The midstream involves the distribution infrastructure—both physical prints (less common now) and digital cinema packages (DCPs)—that must be securely delivered and managed, often involving third-party mastering and encryption services. This upstream content supply dictates the viability and performance of the entire downstream market, making studio relations paramount for cinema operators.

The core of the value chain rests with the exhibitors—the movie theaters themselves. These entities handle the final delivery and presentation of the product, generating revenue primarily through admissions and high-margin concessions. Their activities include capital investment in projection and sound equipment, managing real estate assets, marketing local showtimes, and employing staff. The distribution channel is inherently dual: direct and indirect. Direct distribution involves the exhibitor selling tickets directly to the consumer via box offices or proprietary apps. Indirect distribution involves sales through third-party aggregators (e.g., Fandango, Atom Tickets) who charge a small commission but provide broader market reach. Maintaining efficient operations and high utilization rates of cinema assets is the key performance indicator at this stage.

Downstream analysis focuses on the end consumer, whose attendance provides the financial return necessary to sustain the entire chain. The profitability of the value chain is highly dependent on effective revenue-sharing agreements (typically a 50/50 or front-loaded split between studio and exhibitor) and the ability of the exhibitor to maximize secondary spending through premium offerings and concessions. The introduction of shorter theatrical windows has placed increasing pressure on the distribution mechanism, forcing studios and exhibitors to renegotiate terms continuously. Value is added at every stage, from the creative output of the studio to the technological immersion provided by the exhibitor, ensuring that the out-of-home viewing experience remains superior and compelling enough to drive consistent consumer spending.

The primary customers in the Movie Theater Market are diverse, ranging from high-frequency film enthusiasts (frequent moviegoers) to casual consumers seeking out-of-home entertainment. Frequent moviegoers, typically younger demographics (16-35 years old) or avid fans of specific genres (e.g., Marvel, DC), represent the segment with the highest revenue potential, often subscribing to loyalty programs and being willing to pay premiums for PLF experiences (IMAX, Dolby Cinema). These customers prioritize content quality, superior presentation, and the social experience. Exhibitors target this group with subscription models and exclusive early access screenings to secure reliable, recurring revenue streams, effectively turning ticket sales into a service revenue model.

The secondary customer segment includes families and occasional patrons who attend primarily during holiday periods or for major, globally advertised blockbusters. For this group, convenience, affordability, and the availability of family-friendly amenities (e.g., discounted tickets, spacious seating, kid-friendly concessions) are key buying factors. Marketing to this segment often focuses on the social gathering aspect and the event-like nature of major film releases. Additionally, emerging markets present a massive growth opportunity, targeting newly affluent middle-class consumers who view cinema attendance as an increasingly accessible form of modern, aspirational entertainment.

Corporate clients and educational institutions form a niche customer base, utilizing cinema venues for private screenings, corporate events, or educational field trips, particularly during off-peak weekdays. While smaller in volume than general admission, these rentals provide steady revenue utilization outside of prime viewing hours, diversifying the theaters’ income sources. Overall, successful market players must deploy highly sophisticated, AI-driven segmentation strategies to address the distinct price sensitivity, viewing preferences, and spending habits of these varied customer profiles, ensuring both high-margin premium sales and broad market volume.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $24.5 Billion |

| Market Forecast in 2033 | $38.2 Billion |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | AMC Entertainment, Cineworld Group, Cinemark Holdings, VOX Cinemas, PVR INOX, CJ CGV, Wanda Film Holding, Kinepolis Group, Cineplex Inc., National Amusements, Everyman Media Group, Picturehouse Cinemas, IMAX Corporation, Dolby Laboratories (Technology Partner), Barco NV (Technology Partner). |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Movie Theater Market is characterized by intense investment aimed at enhancing presentation quality and operational efficiency to create a powerful differentiation against in-home viewing. Laser projection technology, replacing traditional xenon lamps, is a critical development, offering superior brightness, contrast, and color fidelity while drastically reducing maintenance and energy costs. The proliferation of Premium Large Format (PLF) technologies, such as IMAX, Dolby Cinema, and proprietary in-house large screens, integrates these advanced projection systems with sophisticated sound technologies like Dolby Atmos and DTS:X, which utilize overhead speakers and complex mixing to create a three-dimensional, deeply immersive audio environment, substantially elevating the sensory experience of a theatrical visit.

Beyond the screen and sound, operational technology is undergoing a digital transformation. Seamless ticketing and customer journey technologies are increasingly important, relying on cloud-based systems for real-time inventory management, mobile ticketing integrated with loyalty programs, and automated, contactless entry solutions. This integration minimizes friction points for the customer, from the initial booking to entry into the auditorium. Furthermore, sophisticated software for energy management, coupled with AI-driven monitoring of equipment health, ensures operational longevity and sustainability, which is a growing concern for exhibitors operating large physical venues globally.

Future technological advancements are focused on personalized and interactive cinema. Technologies like 4DX, which incorporates motion seats, wind, water, and scent effects, transition the viewing experience from passive to active, further solidifying the 'event' status of a movie outing. Simultaneously, Virtual Reality (VR) and Augmented Reality (AR) experiences are being piloted in cinema lobbies and dedicated spaces, serving as complementary entertainment offerings that drive engagement before and after the main feature. The convergence of these presentation and operational technologies is crucial for exhibitors seeking to maintain relevance and competitive advantage in a media environment saturated with high-quality, convenient home alternatives.

Market growth is primarily driven by the expansion of Premium Large Formats (PLFs) like IMAX and Dolby Cinema, which offer a technically superior, immersive experience unattainable at home. Additionally, strong content pipelines featuring globally successful blockbuster franchises and rapid infrastructure expansion in high-growth regions like Asia Pacific are key growth drivers.

Concessions revenues are highly significant, often representing the most profitable segment of a cinema's business model. Due to very high margins compared to shared ticket revenue, optimizing food and beverage sales through premium offerings, full-service dining, and AI-driven personalized marketing is essential for overall exhibitor profitability.

Key technological trends include the transition to energy-efficient and high-fidelity laser projection systems, the integration of immersive sound formats (Dolby Atmos), and the adoption of seamless, contactless ticketing systems and AI-powered dynamic pricing models to enhance customer experience and operational yield.

The reduction in the exclusive theatrical exhibition window, driven by studio investments in Direct-to-Consumer (D2C) streaming, is a major restraint. It increases pressure on exhibitors to maximize box office returns quickly, necessitating higher-value offerings (PLFs, specialized events) and enhanced loyalty programs to secure rapid and repeat attendance.

Asia Pacific (APAC), particularly China and India, is projected to dominate market expansion in terms of volume and new screen count. This growth is fueled by increasing urbanization, rising disposable incomes, and lower pre-existing cinema density compared to mature Western markets, making it the primary target for future investment.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.