ID : MRU_ 434118 | Date : Dec, 2025 | Pages : 251 | Region : Global | Publisher : MRU

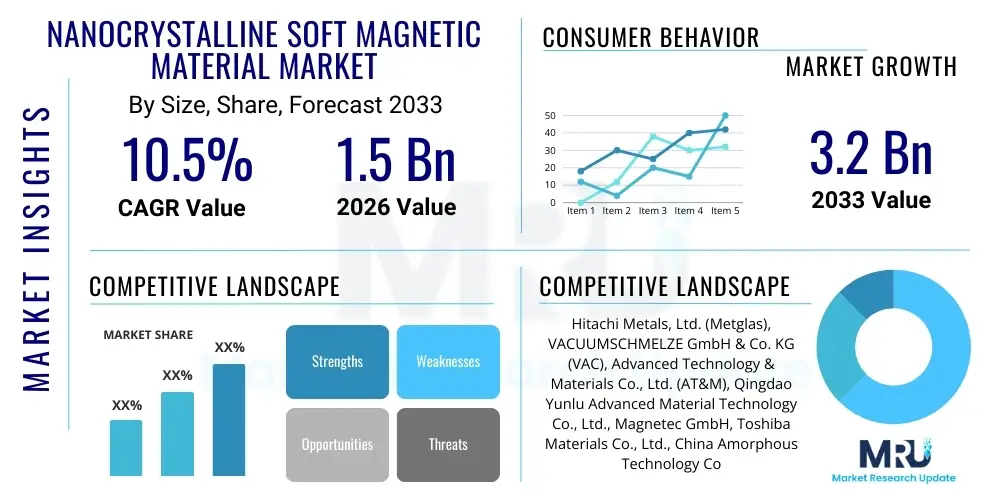

The Nanocrystalline Soft Magnetic Material Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2026 and 2033. The market is estimated at USD 1.5 Billion in 2026 and is projected to reach USD 3.2 Billion by the end of the forecast period in 2033. This substantial growth trajectory is primarily fueled by the accelerating global adoption of electric vehicles (EVs) and the increasing demand for highly efficient power conversion systems in renewable energy infrastructure. Nanocrystalline materials, characterized by their superior magnetic permeability, low core losses, and excellent thermal stability, are becoming indispensable in high-frequency applications, replacing traditional ferrite and amorphous materials where miniaturization and energy efficiency are paramount design requirements.

Market expansion is further supported by significant investments in smart grid technologies and data center infrastructure globally. These advanced sectors require robust, reliable, and energy-saving magnetic components such as inductors and transformers to manage high power density effectively. The inherent benefits of nanocrystalline alloys, specifically their ultrafine grain structure (typically below 100 nm), provide magnetic properties that are unattainable with conventional crystalline metals. This technological advantage positions them perfectly for demanding applications in aerospace, medical devices (MRI machines), and sophisticated communication systems where performance under extreme conditions is non-negotiable.

Geographically, the Asia-Pacific region is anticipated to dominate the market share, driven by rapid industrialization, large-scale electronics manufacturing bases, and supportive government policies promoting EV production in countries like China, Japan, and South Korea. However, North America and Europe are also experiencing robust growth, propelled by stringent energy efficiency regulations (e.g., EU Ecodesign directives) and continuous innovation in power electronics research and development. The commercialization of advanced production techniques, such as rapid solidification casting, is simultaneously driving down manufacturing costs and enhancing material quality, further democratizing the usage of these high-performance alloys across diverse industries, thus maintaining the high projected CAGR.

The Nanocrystalline Soft Magnetic Material Market encompasses the production, distribution, and utilization of alloys exhibiting excellent soft magnetic properties derived from a microstructure characterized by nanoscale crystalline grains. These materials, typically based on iron, silicon, boron, and often copper and niobium additions (e.g., Finemet-type alloys), offer a unique combination of high saturation magnetic flux density, ultra-low coercivity, and high electrical resistivity, making them significantly superior to traditional amorphous and ferrite materials in high-frequency applications. The core product description involves ribbons and cores manufactured through rapid quenching techniques, primarily planar flow casting, followed by carefully controlled annealing processes to achieve the desired nanocrystalline structure.

Major applications of these materials span across key industrial sectors, including power electronics (especially switch-mode power supplies, SMPS), renewable energy systems (solar inverters, wind turbine converters), electric vehicles (on-board chargers, inductive charging systems, DC-DC converters), electromagnetic compatibility (EMC) filters, and high-precision sensors. The paramount benefits driving their adoption include significant reduction in energy losses (enhancing overall system efficiency), miniaturization capabilities due to high flux density operation, and improved operating frequency limits compared to competing technologies. This operational efficiency translates directly into lower heat generation and reduced size and weight for critical components, which is a major advantage in space-constrained modern electronics.

Key driving factors accelerating market expansion include the global shift towards electrification and energy conservation, spurred by environmental regulations and rising energy costs. Specifically, the mandated adoption of higher energy efficiency standards (like those in power supply units) compels manufacturers to integrate materials with minimal core losses. Furthermore, the proliferation of high-frequency switching technology in consumer electronics and industrial automation demands materials that can sustain performance at elevated frequencies without severe thermal degradation. The intrinsic ability of nanocrystalline alloys to meet these rigorous demands securely cements their position as essential enabling technology for the next generation of power electronics infrastructure.

The Nanocrystalline Soft Magnetic Material Market is undergoing rapid transformation, propelled by several convergent business trends focused on energy transition and digital infrastructure build-out. Key business trends include the strong integration of these materials into Electric Vehicle (EV) components, particularly traction motors, high-power charging stations, and battery management systems, positioning the automotive sector as the primary demand catalyst. Additionally, strategic partnerships between material suppliers and Tier 1 electronics manufacturers are increasing, aiming to standardize performance specifications and optimize supply chain resilience. The market is also seeing heightened focus on automated, high-volume production techniques to scale manufacturing capacity and address the growing need for materials capable of operating efficiently in temperatures exceeding 150°C, necessitated by compact automotive and industrial designs. Innovation remains centered on optimizing annealing protocols to tailor magnetic properties precisely for specific application frequencies and power levels.

Regional trends indicate that the Asia Pacific (APAC) region, spearheaded by China, maintains the dominant position in both consumption and production, benefiting from extensive government support for renewable energy and EV manufacturing ecosystems. Europe is demonstrating significant acceleration, driven by ambitious Green Deal initiatives and strict energy efficiency mandates, particularly in Germany and Scandinavia, fostering demand for high-efficiency solar inverters and industrial power supplies. North America shows consistent growth, largely attributed to technological advancements in data center power infrastructure and aerospace applications, where high reliability and weight reduction are paramount. Regulatory environments favoring high-performance materials are consistently boosting adoption rates across all major economic zones, necessitating localized supply chain establishment to mitigate geopolitical risks and transport costs associated with these heavy, high-value components.

Segmentation trends highlight the dominance of the power electronics segment by application, capturing the largest market share due to widespread use in switched-mode power supplies (SMPS) and industrial automation equipment. By alloy type, Fe-based nanocrystalline materials, particularly those offering high saturation flux density, remain the most utilized due to their cost-effectiveness and superior performance characteristics suitable for mid-to-high frequency applications (10 kHz to 500 kHz range). Furthermore, there is an increasing trend in the development of materials specifically engineered for high-frequency common mode and differential mode chokes, addressing the complex electromagnetic interference (EMI) issues inherent in modern, high-speed power conversion circuits. The push for greater power density dictates that core manufacturers continuously refine material thickness and geometry to maximize performance within extremely compact component footprints.

User inquiries regarding AI's influence on the Nanocrystalline Soft Magnetic Material Market frequently center on themes of material discovery acceleration, quality control optimization, and predictive maintenance in manufacturing processes. Users are concerned about how AI-driven simulations can replace traditional trial-and-error methods in alloy composition and annealing parameter determination, speeding up the development cycle for new, specialized nanocrystalline grades. There is significant interest in AI's role in optimizing magnetizing and demagnetizing processes, ensuring precise control over core properties during mass production. Key expectations include leveraging machine learning algorithms to analyze vast datasets related to material performance under varying operating conditions (temperature, frequency, power), thereby facilitating the design of components that exhibit maximum efficiency and lifespan. This predictive modeling capability is anticipated to be critical for meeting the strict reliability requirements of high-stakes applications like aerospace and high-speed rail, reducing material waste and improving overall manufacturing throughput.

The Nanocrystalline Soft Magnetic Material Market is governed by a compelling mix of growth Drivers, significant Restraints, and transformative Opportunities, collectively shaping the market's Impact Forces. Primary drivers revolve around the non-negotiable global mandate for energy efficiency, specifically the exponential growth of the Electric Vehicle sector requiring high-performance, compact, and lightweight power magnetics, coupled with the rapid expansion of renewable energy infrastructure demanding low-loss components for optimal energy harvesting. These drivers are strongly supported by the inherent technical superiority of nanocrystalline materials over traditional ferrites in high-frequency power conversion applications. However, significant restraints challenge market expansion, notably the high initial manufacturing cost associated with rapid solidification and precise annealing processes, requiring substantial capital investment. Furthermore, the limited number of established, high-volume producers creates supply chain vulnerabilities, compounded by challenges in machining and handling these brittle amorphous ribbons into usable core geometries, necessitating specialized processing techniques that add to the overall component cost and complexity.

Opportunities for disruptive growth are substantial, particularly the continuous development of novel Fe-based alloys with enhanced saturation flux density, broadening the material's applicability into lower-frequency, high-power transformer markets traditionally dominated by silicon steel. The increasing penetration of Wireless Power Transfer (WPT) technologies, especially for EV charging, presents a vast new application area where the low losses and high frequency response of nanocrystalline materials are highly advantageous. Moreover, advancements in powder metallurgy and 3D printing techniques are starting to be explored for creating complex magnetic geometries, potentially overcoming current limitations in core shaping and accelerating the market's ability to customize solutions rapidly. Strategic vertical integration by material providers to offer not just the ribbon, but the finished core or even the complete power module, represents a key pathway for maximizing value capture and streamlining customer adoption.

The overall Impact Forces are significantly high and positive, driven by technological necessity. The societal push for decarbonization and energy independence is creating a structural demand floor for high-efficiency components that only nanocrystalline materials can reliably address at high frequencies. This demand strength outweighs the current cost and production complexity restraints, particularly as economies of scale are achieved through expanding production capacity in Asia and Europe. The market is therefore experiencing a strong shift towards performance-based procurement rather than pure cost-minimization, ensuring that materials offering measurable energy savings, reduced thermal management needs, and enhanced system longevity will continue to command premium pricing and market share, thus solidifying the long-term upward trajectory of the segment.

The Nanocrystalline Soft Magnetic Material Market is systematically segmented based on various technical and commercial parameters, including Alloy Type, Application, End-Use Industry, and Geographic Region. This segmentation allows for precise market sizing and strategic focus, reflecting the diverse material requirements across different user groups. The categorization by Alloy Type generally separates Fe-based alloys from Co-based and Ni-based alloys, with Fe-based types dominating due to their excellent balance of high saturation magnetic induction and cost-effectiveness, suitable for high-volume power applications. Segmentation by Application highlights critical functional areas like power conversion, electromagnetic interference (EMI) suppression, and specialized sensors, each demanding unique magnetic characteristics suchities in permeability and core loss profile.

The End-Use Industry segmentation is crucial, distinguishing between high-growth sectors such as Automotive (specifically Electric Vehicles and hybrid systems), Renewable Energy (solar and wind inverters), Telecommunications (5G infrastructure and data centers), and Industrial Automation (motors and drives). The growth rate within each segment is highly correlated with capital expenditure and regulatory shifts within that particular industry. For instance, the automotive segment is currently experiencing explosive demand due to the electrification trend, requiring standardized, reliable core materials for on-board charging and traction systems. Conversely, the sensor segment, while smaller in volume, demands extremely high precision and stability, often using specialized, high-permeability Co-based materials.

Understanding these segment dynamics is vital for market players seeking strategic positioning. Companies often specialize in developing material grades tailored for specific segments, such as ultra-thin ribbons for high-frequency telecommunications transformers or robust cores engineered for the high current demands of utility-scale solar inverters. The trend towards vertical integration, where material manufacturers offer customized core shapes and finished components, is a direct response to the need for simplified sourcing and optimized performance within these specialized industry segments, ensuring that the chosen magnetic solution perfectly aligns with the required operational parameters like operating temperature range and switching frequency.

The value chain for nanocrystalline soft magnetic materials is complex, involving highly specialized technological steps from raw material acquisition to final product integration. The upstream segment is dominated by the sourcing and refining of high-purity raw materials, primarily iron, silicon, boron, niobium, and copper. This stage requires rigorous quality control as trace impurities can drastically affect the final magnetic properties. Key upstream suppliers include major metal producers and chemical companies specializing in amorphous and metallic glass precursors. The midstream manufacturing stage is the most critical and technologically challenging, involving the energy-intensive process of rapid solidification (planar flow casting) to produce the amorphous ribbon, followed by precise, controlled heat treatment (annealing) to induce the nanoscale crystallization necessary for achieving optimal soft magnetic characteristics. Manufacturers must possess proprietary knowledge regarding cooling rates and thermal profiles to ensure uniformity across large production batches, maintaining consistent permeability and coercivity levels.

The distribution channel involves several layers, differentiating between direct sales and indirect channels. Direct sales are prevalent for large volume contracts, especially with Tier 1 automotive suppliers or major renewable energy system integrators, where technical consultation and customized material specifications are mandatory. Indirect channels utilize specialized distributors and representatives who manage smaller, fragmented customer bases, such as niche industrial control manufacturers or R&D laboratories. These distributors often provide cutting, winding, and housing services to transform the raw ribbon into finished cores (toroidal, rectangular, or C-cores). The efficiency of the distribution network is crucial for maintaining competitive lead times, especially given the global nature of electronics manufacturing and the typically high transport costs associated with these specialized magnetic components.

The downstream segment involves the integration of the finished nanocrystalline cores into final applications, such as high-frequency transformers, DC-DC converters, and EMI filters, utilized by end-users. The key players in the downstream sector are original equipment manufacturers (OEMs) in power electronics, automotive, and IT infrastructure. The trend shows a move towards greater vertical integration, where the core manufacturers increasingly provide integrated modules or encapsulated components rather than just the raw core, adding value and simplifying the assembly process for the OEM. Understanding the specific design constraints of the end application, such as operating temperature limits, required power density, and physical size constraints, dictates the specifications passed back up the value chain, emphasizing the necessity of close collaboration between material producers and end-product designers to optimize overall system performance and cost.

Potential customers for Nanocrystalline Soft Magnetic Materials represent a broad spectrum of high-technology industries requiring superior power management and electromagnetic compatibility. The primary end-users are original equipment manufacturers (OEMs) specializing in advanced power conversion electronics. In the automotive sector, this includes manufacturers of Electric Vehicles (EVs) and Hybrid Electric Vehicles (HEVs) who require high-performance materials for on-board chargers (OBCs), DC-DC converters, traction inverters, and wireless charging pads. These components demand materials that minimize losses at high switching frequencies (up to 500 kHz) while operating reliably under high temperatures, making nanocrystalline cores indispensable for achieving maximum driving range and battery efficiency, thereby appealing directly to EV manufacturers seeking performance advantages.

Another significant customer segment is the renewable energy sector, encompassing manufacturers of solar photovoltaic (PV) inverters and wind turbine converters. Inverters utilize nanocrystalline materials extensively in the construction of high-frequency transformers and output chokes, crucial for maximizing energy harvest efficiency and ensuring grid stability. Additionally, companies involved in building modern telecommunication infrastructure, particularly 5G networks and hyperscale data centers, represent a rapidly expanding customer base. These applications require ultra-efficient power supply units (PSUs) and robust EMI suppression components to manage the massive energy demands and complex signal integrity issues inherent in high-density computing environments. The reliability and low-loss characteristics of the materials directly translate into reduced operational expenditures for these energy-intensive facilities.

Furthermore, specialized industrial and medical equipment manufacturers constitute key niche customers. Industrial automation firms integrating high-efficiency motor drives and induction heating systems benefit from the material’s high saturation and low loss at varying frequencies. The medical sector, particularly companies producing Magnetic Resonance Imaging (MRI) machines, CT scanners, and advanced patient monitoring systems, relies on the exceptional magnetic shielding and precision of nanocrystalline materials for reliable sensor and signal processing components. Ultimately, any industry prioritizing power density, reduced component size and weight, and exceptional energy efficiency at elevated frequencies is a prime potential customer for these advanced soft magnetic alloys.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.5 Billion |

| Market Forecast in 2033 | USD 3.2 Billion |

| Growth Rate | 10.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Hitachi Metals, Ltd. (Metglas), VACUUMSCHMELZE GmbH & Co. KG (VAC), Advanced Technology & Materials Co., Ltd. (AT&M), Qingdao Yunlu Advanced Material Technology Co., Ltd., Magnetec GmbH, Toshiba Materials Co., Ltd., China Amorphous Technology Co., Ltd. (CATC), MK Magnetic, Delta Electronics, Inc., TDK Corporation, KEMET Corporation, Amotech Co., Ltd., Hengdian Group DMEGC Magnetics Co., Ltd., JFE Steel Corporation, Samhwa Electronics Co., Ltd., Sumitomo Metal Mining Co., Ltd., Fuji Electric Co., Ltd., Micrometals, Inc., Vitsuba Corp., Precision Technologies, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Nanocrystalline Soft Magnetic Material Market is defined by sophisticated metallurgy and advanced thermal processing. The foundational technology remains Rapid Solidification (Planar Flow Casting), which involves melting the raw alloy and ejecting it onto a high-speed, water-cooled rotating copper wheel. This process achieves cooling rates exceeding 1 million degrees Celsius per second, preventing the formation of conventional crystalline structures and instead yielding an amorphous metallic glass ribbon, which is the precursor material. The thickness of this ribbon, typically ranging from 18 to 30 micrometers, is critically controlled during casting as it directly influences high-frequency performance and eddy current losses. Continuous innovation in casting equipment focuses on improving ribbon uniformity, minimizing defects, and increasing the overall throughput and width of the manufactured ribbon to reduce production costs and enable larger core fabrication.

Following casting, the amorphous ribbons undergo a precise thermal treatment, known as Annealing, which is the key step in inducing the nanocrystalline phase. This involves heating the material just above the crystallization temperature for a defined time under controlled atmosphere conditions, facilitating the homogeneous nucleation and growth of extremely fine (5–20 nm) crystalline grains, primarily iron-rich phases, within the remaining amorphous matrix. The precise control over the annealing parameters (temperature profile, time, and applied magnetic field) is paramount, as it determines the final magnetic properties, including permeability, coercivity, and core losses. Advanced annealing technologies now employ inert gas furnaces and even vacuum furnaces to ensure minimal oxidation and highly uniform grain formation across the entire core, which is essential for high-performance applications in sensitive power electronics.

Furthermore, technology development extends to core processing and component integration. Specialized cutting and winding techniques are required to minimize stress induction in the brittle ribbons, as mechanical stress can severely degrade the soft magnetic properties. Techniques like laser cutting or water jet cutting are sometimes utilized for precise geometry definition, while advanced automated winding machines ensure uniform layer tension during core assembly. The industry is also seeing increased research into soft magnetic composites (SMCs) using nanocrystalline powder, aiming to combine the excellent magnetic properties of the alloy with the three-dimensional shaping flexibility of powder metallurgy. This emerging technology promises to revolutionize the construction of complex magnetic components needed for advanced motor designs and resonant inductive charging systems, overcoming the geometric limitations inherent in standard ribbon-wound cores.

Regional dynamics significantly influence the Nanocrystalline Soft Magnetic Material Market, driven by localized industrial policies, technological adoption rates, and manufacturing concentration. The Asia Pacific (APAC) region stands out as the primary market engine, holding the largest share globally. This dominance is attributed to the presence of large-scale electronics manufacturing hubs in China, Taiwan, and South Korea, coupled with aggressive government investments in renewable energy infrastructure and the burgeoning Electric Vehicle supply chain. China, in particular, leads in both the production capacity and consumption of nanocrystalline cores, utilizing them extensively in domestic solar inverters and the globally dominant EV battery charging ecosystem. The region's high urbanization rate and rapid industrial power consumption growth necessitate continuous upgrades in power conversion efficiency, thereby ensuring sustained high demand for these specialized materials.

Europe represents the second most significant market, characterized by stringent energy efficiency and environmental regulations, such as the EU Ecodesign directives. These mandates compel manufacturers of power supply units, industrial motor drives, and lighting systems to utilize materials that drastically minimize standby power losses and maximize operational efficiency. Countries like Germany, with its strong automotive and industrial machinery sectors, and Scandinavia, heavily invested in green energy, are major consumers. European demand is highly focused on quality, reliability, and specific certifications, often driving innovation towards tailor-made, high-reliability nanocrystalline solutions for complex industrial and high-speed rail applications, emphasizing performance over absolute cost minimization in many strategic segments.

North America maintains a strong position, driven primarily by technological innovation in specialized sectors. The region’s demand is fueled by significant investments in data center infrastructure (requiring ultra-efficient power supplies and EMI filtering), aerospace and defense (where weight reduction and high thermal stability are critical), and high-power applications for utility grids. While manufacturing volume is lower compared to APAC, the average selling price (ASP) of nanocrystalline components tends to be higher due to the premium placed on customized, high-specification products meeting demanding regulatory and operational standards. Growth here is closely tied to advancements in semiconductor technology and the deployment of advanced smart grid systems requiring resilient magnetic components.

Nanocrystalline materials offer significantly lower core losses at high frequencies (typically above 100 kHz) and higher saturation magnetic flux density compared to ferrites. Compared to amorphous metals, nanocrystalline materials achieve superior permeability and better thermal stability, enabling the design of smaller, more efficient magnetic components for high-power applications like EV chargers and solar inverters.

EVs drive demand for nanocrystalline materials due to their necessity in high-efficiency on-board chargers (OBCs), DC-DC converters, and specialized inductors for traction systems. These components must handle high power densities and high switching frequencies to maximize battery life and minimize the weight and volume of the power electronics module, requirements perfectly met by nanocrystalline cores.

The primary challenges involve the high initial capital investment required for the rapid solidification casting equipment, the complexity of precisely controlling the nanoscale crystallization during the annealing process, and the brittleness of the amorphous ribbon precursor, which complicates subsequent cutting, handling, and core winding operations, often leading to increased production costs and specialized process requirements.

The Asia Pacific (APAC) region, specifically countries such as China and Japan, leads the global market in both production capacity and consumption. This is fueled by extensive manufacturing ecosystems for electronics and automotive components, coupled with substantial governmental support for the renewable energy sector and high-power applications.

Nanocrystalline materials generally provide optimal performance, characterized by low core loss and high permeability, in the intermediate to high-frequency range, typically spanning from 10 kHz up to 500 kHz. This range is crucial for modern switched-mode power supplies (SMPS) and resonant converters used in high-efficiency power systems, effectively bridging the gap between high-flux silicon steel and very high-frequency ferrites.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.