ID : MRU_ 438545 | Date : Dec, 2025 | Pages : 243 | Region : Global | Publisher : MRU

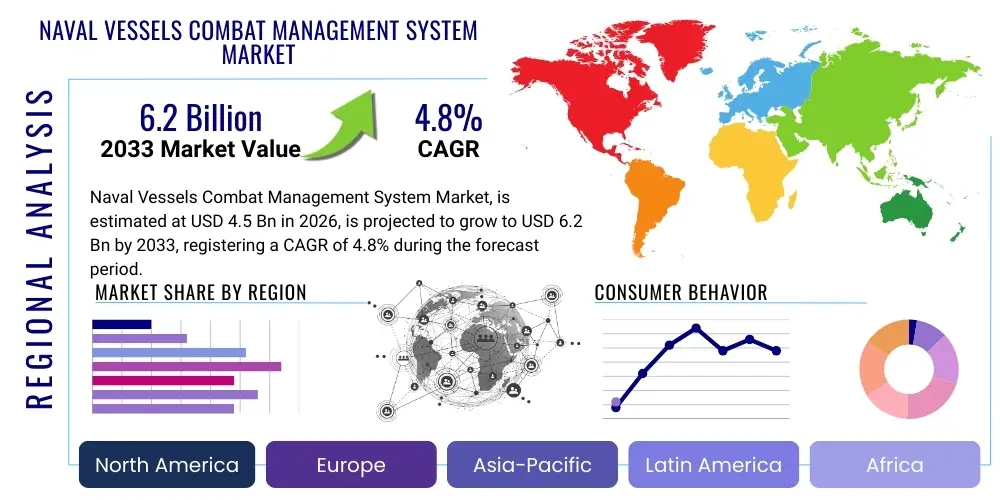

The Naval Vessels Combat Management System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2026 and 2033. The market is estimated at USD 4.5 Billion in 2026 and is projected to reach USD 6.2 Billion by the end of the forecast period in 2033.

The Naval Vessels Combat Management System (CMS) Market encompasses advanced integrated systems designed to enable naval platforms—ranging from frigates and destroyers to aircraft carriers and submarines—to effectively detect, track, classify, and engage threats across multi-domain environments (air, surface, subsurface, and cyber). A CMS acts as the central nervous system of a warship, fusing data from various onboard sensors, including radar, sonar, electronic warfare systems, and communications links, to present a unified tactical picture to the command team. The primary goal of these systems is to maximize the vessel's lethality and survivability by optimizing the deployment of weapons, countermeasures, and sensor assets in complex operational scenarios. Modern CMS solutions are characterized by their open architecture design, modularity, and high level of automation, facilitating rapid upgrades and integration of emerging technologies.

Product descriptions within this market focus on highly resilient, scalable software architectures that support sophisticated decision-making tools. Key components include tactical data link processing capabilities, electronic chart display and information systems (ECDIS), and advanced tracking algorithms utilizing machine learning for enhanced target classification in cluttered environments. These systems must comply with stringent military standards for environmental robustness and cybersecurity. Major applications span new vessel construction programs, mid-life upgrades (MLU) of existing fleets, and command, control, communications, computers, and intelligence (C4I) integration projects across allied navies, emphasizing interoperability and seamless data exchange between different platforms and national defense networks.

The driving factors propelling market growth are fundamentally rooted in global geopolitical instability and the persistent need for maritime domain awareness and protection of crucial sea lines of communication (SLOCs). Benefits derived from utilizing advanced CMS include shortened sensor-to-shooter timelines, improved situational awareness during high-intensity conflict, and reduced cognitive load on operators through automated processes. The shift toward network-centric warfare and the development of unmanned surface and underwater vehicles (USVs/UUVs) further necessitate highly sophisticated, distributed combat management capabilities capable of commanding and controlling these heterogeneous fleets effectively, cementing the role of CMS as critical national defense infrastructure.

The Naval Vessels Combat Management System Market is currently undergoing a transformative period, driven by accelerated naval modernization cycles across major global powers, particularly within the Asia Pacific region. Business trends emphasize the shift from proprietary, closed-architecture systems toward open-architecture, standardized solutions utilizing commercial off-the-shelf (COTS) components where permissible, which lowers long-term maintenance costs and speeds up technology refresh cycles. Key market players are increasingly focusing on strategic mergers, acquisitions, and defense partnerships to access niche technologies, such as advanced data fusion algorithms and artificial intelligence integration for threat identification. Furthermore, the rising demand for indigenous defense capabilities in emerging economies is fostering localized production and technology transfer agreements, altering the traditional competitive landscape dominated by established Western defense contractors.

Regional trends indicate that North America and Europe remain foundational markets due to substantial investment in next-generation platforms and ongoing fleet modernization; however, the Asia Pacific region is demonstrating the highest growth trajectory, fueled by China's aggressive naval expansion and the reactive recapitalization efforts of nations like India, Japan, South Korea, and Australia. The focus in APAC is heavily skewed toward integrated air and missile defense (IAMD) capabilities, requiring robust CMS capable of handling complex saturation attacks. Conversely, European markets prioritize systems emphasizing interoperability within NATO frameworks and anti-submarine warfare (ASW) capabilities tailored for complex coastal and deep-water operations. The Middle East is emerging as a critical customer segment, driven by investments in high-end surface combatants to secure strategic waterways.

Segment trends reveal that the Surface Vessels segment, particularly destroyers and frigates, commands the largest market share due to the sheer volume and complexity of their required operational capabilities. However, the Submarines segment is anticipated to exhibit robust growth, driven by the proliferation of advanced, quiet conventional and nuclear submarines requiring highly specialized combat systems for stealth and deep-sea operations. Technology-wise, software-intensive solutions are growing faster than pure hardware sales, reflecting the increasing importance of sophisticated command and control software, advanced mission planning tools, and data processing algorithms. The emphasis across all segments is on cyber resilience, ensuring that critical combat functions remain operational even under sustained electronic warfare attack or cyber penetration attempts.

Common user questions regarding AI's impact on Naval Vessels Combat Management Systems frequently center on automation reliability, ethical considerations in autonomous weapon deployment, and the ability of AI to accelerate the decision loop beyond human capacity (OODA Loop optimization). Key themes include how AI can manage sensor overload, the feasibility of predictive maintenance for complex systems, and the regulatory challenges associated with machine-speed warfare. Users express expectations that AI will significantly enhance threat classification accuracy, reduce personnel requirements, and enable robust command and control in denied or degraded communication environments. Conversely, major concerns revolve around data integrity, the risk of catastrophic failure due to algorithmic bias, and ensuring human-in-the-loop control for lethal engagements, demanding rigorous verification and validation standards for AI-integrated CMS components.

The Naval Vessels Combat Management System (CMS) market is subject to complex dynamics driven by global security imperatives (Drivers), stringent acquisition timelines and budget limitations (Restraints), and the rapid evolution of digital warfare capabilities (Opportunities). The core impact forces shaping this market include the perennial arms race among great powers, the imperative for maritime domain awareness against asymmetric threats, and the slow but inevitable transition towards highly automated, network-centric naval architectures. These factors collectively mandate continuous investment in system modernization and integration capabilities, ensuring naval forces maintain tactical superiority in contested environments.

Key drivers include escalating geopolitical tensions, particularly territorial disputes in the South China Sea and the Russian aggression in Eastern Europe, which necessitate robust naval deterrence capabilities. Furthermore, the global proliferation of sophisticated anti-ship missile technology and the increasing presence of quiet submarines demand CMS that offer integrated air and missile defense (IAMD) and advanced anti-submarine warfare (ASW) functionalities. Opportunities are abundant in the areas of digital transformation, including the adoption of open-architecture standards (like OpenVPX and HOST), enabling modular system design and faster integration of capabilities like quantum computing readiness and advanced electronic warfare suites. The transition to software-defined combat systems allows for capability upgrades via software patches rather than extensive, costly hardware overhauls, presenting long-term revenue streams for service providers.

However, significant restraints temper market growth. The extremely long procurement cycles for naval platforms—often spanning decades—delay the deployment of the latest CMS technologies, leading to potential capability gaps. Budgetary constraints in national defense budgets necessitate prioritizing certain capabilities over others, often limiting full-scale fleet upgrades. Moreover, the integration challenges associated with proprietary legacy systems and the scarcity of highly skilled system integrators and cybersecurity experts pose substantial barriers. The high entry cost and rigorous regulatory compliance required for naval defense technology also restrict the competitive field, focusing market power among a few large defense primes. The impact forces are thus characterized by a tension between technological innovation speed and the bureaucratic and logistical inertia inherent in major defense acquisition programs.

The Naval Vessels Combat Management System Market is systematically segmented based on Platform, Component, Application, and Operation. The Platform segmentation distinguishes between surface vessels (frigates, destroyers, carriers) and subsurface vessels (submarines), recognizing their distinct operational requirements and complexity levels. The Component segmentation separates hardware elements, such as consoles and processors, from the sophisticated software suite, which includes tactical decision aids and data fusion engines. Application segmentation focuses on whether the system is being deployed for new construction programs or for the critical mid-life upgrades (MLU) of existing naval fleets. Operation distinguishes between indigenous systems developed purely for domestic use and integrated systems designed for interoperability within allied fleets, particularly relevant for NATO and other multinational naval forces.

The value chain for the Naval Vessels Combat Management System market is intricate, starting with upstream activities dominated by specialized component suppliers and concluding with long-term maintenance and upgrade services. Upstream analysis involves the sourcing of critical COTS components, high-reliability embedded processors, ruggedized display technologies, and specialized sensor interfaces. Key defense primes often control the intellectual property related to the core software architecture and algorithms, acting as system integrators who procure hardware components from globally distributed suppliers. Managing supply chain resilience, especially concerning microelectronics and cybersecurity vetting of components, is paramount in the initial stages to ensure system integrity and performance compliance with military specifications.

The mid-stream process is centered on the core competencies of system integration, software development, and rigorous testing and validation. This stage is capital-intensive and requires deep expertise in physics, complex systems engineering, and military doctrine. Major defense contractors develop proprietary or semi-proprietary CMS software, which must seamlessly interface with dozens of disparate ship systems, including propulsion, navigation, radar, sonar, and weapon launchers. The development includes creating sophisticated human-machine interface (HMI) designs and extensive simulation environments to train operators and validate system performance against real-world threat scenarios before final delivery to the shipyard for installation.

Downstream analysis involves the final installation, integration onto the vessel (often during the new construction or MLU phase), and extensive sea trials. Distribution channels are predominantly direct, involving government-to-contractor agreements, as these are highly sensitive, strategic assets. Post-delivery, the value chain shifts focus to long-term lifecycle support, including maintenance, spare parts provision, software patching, and capability enhancements (via software upgrades). Indirect channels, such as strategic technology partnerships or joint ventures (JVs) between defense primes and national defense technology organizations, are often utilized to facilitate technology transfer and comply with national industrial participation requirements, particularly in large international sales contracts.

Potential customers for the Naval Vessels Combat Management System Market are almost exclusively national governmental entities, specifically the Ministries of Defence, the Navy departments, and Coast Guards requiring high-end combat capabilities. The procurement process is highly centralized, relying on competitive bidding processes (RFPs) overseen by national defense acquisition authorities. The primary buyers are large, technologically advanced naval forces engaged in blue-water operations, such as the US Navy, UK Royal Navy, French Navy, and the navies of China, Russia, Japan, and India. These navies demand the most sophisticated, network-centric systems capable of multi-domain warfare and interoperability with allied forces (e.g., NATO standards).

A second crucial segment of potential customers comprises navies undergoing rapid modernization programs or expanding their regional influence. Nations in Southeast Asia (e.g., South Korea, Indonesia, Vietnam) and the Middle East (e.g., Saudi Arabia, UAE) are investing heavily in new frigates and corvettes, often requiring off-the-shelf, proven CMS solutions adaptable to their specific regional threats, such as anti-piracy, coastal defense, and securing Exclusive Economic Zones (EEZs). These buyers often prefer systems that offer attractive technology transfer provisions to build local maintenance capabilities and defense industrial bases, favoring international suppliers who collaborate closely with domestic companies.

Furthermore, smaller navies and maritime security agencies, including some high-budget Coast Guards, represent a niche customer base, particularly for scaled-down, less complex CMS variants focusing primarily on surveillance, situational awareness, and light defensive capabilities for patrol vessels. These end-users are driven by the need to counter illicit activities, border incursions, and enforce maritime law. For all customer types, the long-term total cost of ownership (TCO), system reliability, and the security of the supply chain—specifically the absence of foreign hardware backdoors—are critical purchasing criteria that heavily influence contract awards and platform selection decisions.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 6.2 Billion |

| Growth Rate | CAGR 4.8% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Lockheed Martin Corporation, Raytheon Technologies Corporation (RTX), Northrop Grumman Corporation, BAE Systems plc, Thales Group, Leonardo S.p.A., Saab AB, General Dynamics Mission Systems, Hanwha Systems Co., Ltd., Elbit Systems Ltd., L3Harris Technologies, Inc., Terma A/S, Indra Sistemas S.A., Rheinmetall AG, Kongsberg Gruppen, Tata Advanced Systems, Russian United Shipbuilding Corporation, Mitsubishi Heavy Industries, Israel Aerospace Industries (IAI), Damen Naval. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Naval Vessels Combat Management System (CMS) market is characterized by a significant shift towards digitization, open standards, and high-speed data processing capabilities. A crucial technology is the adoption of modular, open system architectures (MOSA), often leveraging standards such as the Open Architecture Combat System (OACS) or the U.S. Navy's common processing systems. This open framework allows different subsystem components from various vendors to be integrated more easily, reducing vendor lock-in and allowing navies to quickly introduce new capabilities in response to evolving threats. Furthermore, virtualization and cloud-native principles are being applied to CMS software, allowing core processing functions to be run on commercial-grade, ruggedized servers rather than proprietary military hardware, thereby enhancing system scalability and reducing physical footprint.

Another fundamental technological development is the implementation of advanced sensor data fusion and tracking algorithms. Modern CMS must handle inputs from active and passive sensors across multiple spectral bands and domains, including electro-optical/infrared (EO/IR), acoustic, radar (AESA), and electronic support measures (ESM). Technologies like Kalman filtering, particle filtering, and now machine learning are essential for fusing this disparate data into a single, reliable, and latency-optimized tactical picture. The integration of advanced human-machine interfaces (HMI), incorporating augmented reality (AR) and sophisticated visualization techniques, is critical for reducing operator cognitive load during high-stress combat scenarios, facilitating quicker decision-making processes under high time pressure.

Cybersecurity technology is intrinsically linked to the combat management system itself, moving beyond simple network segregation to include embedded cyber resilience. This involves hardware-enforced root of trust, real-time intrusion detection systems (IDS) integrated into the core software, and secure virtualization techniques to isolate critical mission systems. Furthermore, the development and integration of robust tactical data link processors (e.g., Link 11, Link 16, Link 22) are paramount for achieving true network-centric capabilities, enabling seamless information exchange with joint forces and satellites. The future trajectory involves leveraging quantum resistance cryptographic measures to future-proof communication links and data storage against emerging computational threats.

Regional dynamics heavily influence the Naval Vessels Combat Management System market, reflecting varied defense budgets, specific regional threat landscapes, and national industrial policies. North America, dominated by the United States, represents the largest and most technologically advanced market segment. The US Navy's continuous modernization programs, focused on building next-generation frigates (FFG(X)), integrating advanced unmanned systems, and maintaining strategic superiority across global oceans, necessitate sustained high investment in complex, integrated CMS solutions. The focus here is on open-architecture systems, integration of AI for autonomous operations, and systems designed for multi-domain command and control (MDC2). The market is mature but highly specialized, with contracts often favoring the largest domestic defense primes who can meet stringent cybersecurity and performance requirements.

Europe constitutes a stable and growing market, driven largely by NATO requirements for interoperability and the ongoing need to replace aging Cold War-era fleets. Nations such as the UK, France, Germany, Italy, and Spain are prioritizing new construction programs for frigates and destroyers equipped with high-end anti-air warfare (AAW) and anti-submarine warfare (ASW) capabilities. European naval requirements place a strong emphasis on standardized tactical data link performance (especially Link 16 and Link 22) and the ability to operate within coalition forces. The competitive environment is robust, featuring strong domestic champions (e.g., BAE Systems, Thales, Leonardo, Saab) who often collaborate on large multinational defense projects like the European Patrol Corvette initiative. Eastern European navies, seeking to transition away from legacy Soviet-era equipment, are driving demand for flexible, COTS-based systems compatible with Western standards.

The Asia Pacific (APAC) region is indisputably the fastest-growing market globally, fueled by significant naval expansion and modernization efforts by China, and the corresponding necessity for counterbalance by regional players. China's rapid fleet expansion, particularly the production of Type 055 destroyers and aircraft carriers, mandates continuous development and deployment of highly sophisticated, indigenous combat management systems, often mirroring or attempting to surpass Western capabilities. Simultaneously, nations like India, Australia, South Korea, and Japan are heavily investing in high-capability surface combatants (such as the Indian Navy's Project 17A frigates and the Japanese Aegis-equipped destroyers) to maintain sea control and secure vital sea lines of communication against increasing regional assertiveness. This region sees intense competition between local vendors and international suppliers, with a strong emphasis on technology transfer and local manufacturing partnerships.

Latin America and the Middle East & Africa (MEA) represent emerging market segments characterized by selective, high-value procurement cycles. MEA, particularly the Gulf Cooperation Council (GCC) states, is investing in naval platforms for coastal security, protecting oil infrastructure, and strategic deterrence. These countries often procure complete, high-specification platforms from Western or Asian suppliers, requiring fully integrated CMS solutions optimized for operations in warm, shallow coastal waters and against asymmetric threats. Latin American navies are focused primarily on replacing aging vessels and upgrading existing patrol fleets, favoring cost-effective modernization packages that extend the operational life of their vessels, with CMS requirements centered on robust maritime surveillance and C4I integration.

The primary driver is the escalating geopolitical instability, particularly the rise of sophisticated anti-access/area denial (A2/AD) strategies and the rapid naval expansion undertaken by major powers in the Asia Pacific region. This necessitates continuous recapitalization and modernization of naval fleets with state-of-the-art CMS capable of integrated air and missile defense (IAMD) and complex multi-domain operations to maintain strategic deterrence and maritime security dominance.

Open Architecture Combat Systems (OACS) are fundamentally shifting the market by reducing reliance on proprietary hardware and software, promoting vendor diversity, and facilitating quicker technology insertion. By adopting standardized interfaces (e.g., MOSA), navies can reduce the long-term total cost of ownership (TCO) and significantly decrease the time required to upgrade capabilities, moving away from monolithic systems towards modular, software-defined solutions, which is critical for future naval agility.

AI is crucial for managing the exponential growth of sensor data (sensor fusion), accelerating the operational decision cycle (OODA Loop), and enhancing target classification accuracy in highly congested environments. Latest-generation CMS utilize AI for automated threat evaluation, optimal weapon assignment, predictive system maintenance, and, increasingly, for the autonomous command and control of integrated unmanned naval assets (USVs and UUVs), ensuring situational awareness remains reliable under information overload.

The Asia Pacific (APAC) region demonstrates the highest growth potential. This growth is directly attributable to the large-scale naval modernization efforts by countries responding to increased regional military activity, including China's blue-water aspirations. Major investors like India, Japan, South Korea, and Australia are prioritizing the acquisition of advanced surface combatants requiring high-end CMS for integrated threat management and robust territorial defense capabilities, driving high-volume contracts and rapid technology adoption cycles.

The most significant technical challenges involve physical space and power limitations within older hulls, complexity in interfacing new digital systems with legacy analog sensors and weapon launchers, and addressing the stringent cybersecurity requirements of integrating sophisticated network-centric hardware into platforms originally designed without adequate digital resilience. These upgrades require extensive and expensive systems engineering to mitigate integration risks and ensure operational compatibility without compromising hull integrity or mission effectiveness.

Cybersecurity is a paramount concern, as a CMS serves as the warship’s central brain. Successful cyberattacks could lead to mission kill by degrading sensor data integrity, corrupting weapon firing solutions, or disabling command and control functions entirely. Developers must integrate robust, hardware-enforced security measures, real-time intrusion detection systems, and secure boot processes from the foundational design stage. The shift to COTS components also necessitates rigorous supply chain vetting to prevent hardware and software backdoors.

An indigenous combat system is developed primarily by a nation's own defense industry for use exclusively within its national fleet, often built around unique operational doctrines and weapon systems, providing full sovereignty over the technology. An integrated/allied interoperable system is designed explicitly to meet the standards of multinational alliances (like NATO), ensuring seamless tactical data exchange (using Link 16/22) and coordinated operations with allied platforms, prioritizing connectivity and common operational picture generation across different naval forces.

Software growth outpaces hardware because modern CMS capabilities are increasingly defined by algorithmic complexity, data fusion effectiveness, and the sophistication of the human-machine interface (HMI). With the adoption of open, virtualized architectures, hardware refresh cycles are slowing, while the speed and frequency of software upgrades (for new threats, mission optimization, or AI integration) are increasing, meaning more value and investment is directed toward developing, testing, and maintaining software fidelity and performance.

Long procurement cycles (10-20 years) mean that by the time a vessel is commissioned, the originally specified technology may already be several generations behind commercial standards. This delay creates a risk of technological obsolescence, necessitating costly, pre-planned mid-life upgrades (MLU). Modern open architectures are the solution, allowing for more frequent, less disruptive 'plug-and-play' technology refresh cycles throughout the ship's service life, minimizing capability gaps caused by protracted acquisition timelines.

Defense firms mitigate international sales risks through strict adherence to export control regulations (such as ITAR and EAR), employing complex technology transfer agreements, and utilizing Foreign Military Sales (FMS) mechanisms supervised by their national governments. They often establish joint ventures (JVs) or local partnerships in buyer nations, agreeing to transfer maintenance, assembly, or less sensitive integration skills, while retaining strict control over the core proprietary software algorithms and critical source code to protect intellectual property and national security interests.

Beyond traditional conflict, enhanced CMS capabilities are increasingly driven by requirements for maritime domain awareness (MDA) against non-state actors, including counter-piracy operations, illegal fishing surveillance, and maritime drug interdiction. These operations require CMS optimized for asymmetric threat detection in cluttered littoral environments, high-resolution tracking of small, fast targets, and seamless integration with civilian law enforcement and border security databases, demanding highly reliable, non-lethal command options.

Lethality refers to the CMS’s ability to efficiently and accurately detect, track, and engage hostile targets using optimal weapon systems, maximizing the probability of mission success and neutralization of threats. Survivability refers to the system’s resilience, encompassing its ability to absorb damage, maintain functionality under sustained electronic warfare attack, resist cyber intrusion, and swiftly reconfigure operations (damage control) following a tactical strike, ensuring the vessel remains mission-capable under duress.

Environmental factors dictate rigorous ruggedization standards for CMS hardware. Operations in the Arctic demand systems resilient to extreme cold and optimized for low-visibility, high-latitude sensor performance, often integrating specialized ice-navigation data. Tropical operations require systems engineered for high heat, humidity, and resistance to corrosion and biofouling, necessitating robust cooling systems and sealed, military-specification components to ensure reliability during extended deployments in challenging climatic zones.

Surface vessel CMS require high-volume data processing for multi-layered defense (air, surface, land attack) and must manage numerous concurrent sensors and weapons (e.g., VLS cells). Subsurface vessel CMS prioritize stealth and operate in a data-scarce environment, relying heavily on passive acoustics and specialized non-hull penetrating sensors. Their systems focus on minimizing emissions, extremely precise navigation, and highly automated tactical decision support for anti-submarine and land-strike missions.

The shift to networked, or network-centric, warfare drastically increases demand for highly robust, redundant tactical data link processors (Link 16, Link 22, TTNT) and advanced cybersecurity hardware/software. It necessitates CMS components capable of managing and disseminating a single integrated air picture (SIAP) across a diverse network of ships, aircraft, and land-based commands, prioritizing high bandwidth, low latency, and secure data transmission over traditional point-to-point communication methods.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.