ID : MRU_ 431491 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

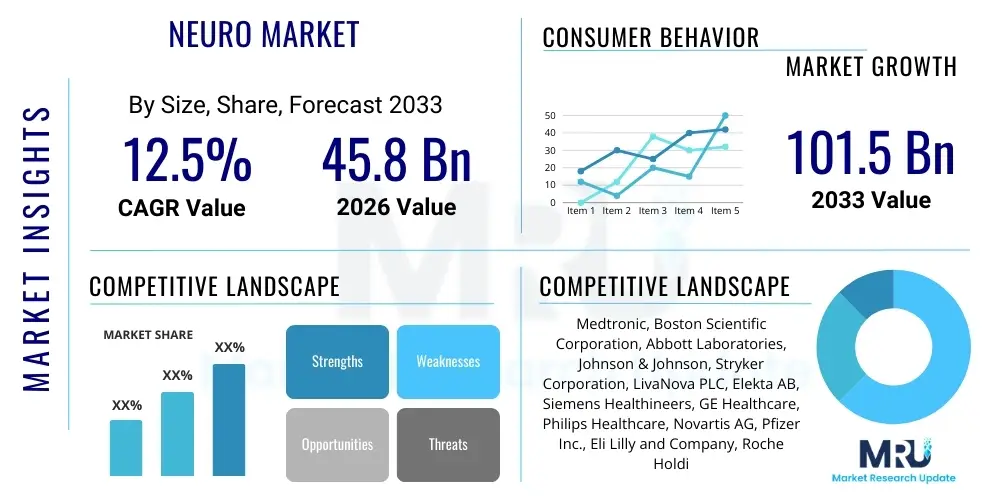

The Neuro Market, encompassing neurological diagnostics, therapeutics, research tools, and neurotechnology devices, is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2026 and 2033. The market is estimated at USD 45.8 Billion in 2026 and is projected to reach USD 101.5 Billion by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by the escalating global burden of neurological disorders, including Alzheimer’s disease, Parkinson’s disease, epilepsy, and stroke, coupled with significant advancements in neuroimaging and personalized medicine approaches.

The Neuro Market represents a sophisticated and rapidly evolving sector focused on the understanding, diagnosis, and treatment of conditions affecting the central and peripheral nervous systems. This broad market includes specialized pharmaceuticals for chronic neurodegenerative diseases, advanced surgical devices like neurostimulation implants, sophisticated neuroimaging modalities such as functional MRI (fMRI) and magnetoencephalography (MEG), and increasingly, digital neurological health solutions and remote patient monitoring systems. The rapid incorporation of artificial intelligence into diagnostics and drug discovery platforms is redefining capabilities, allowing for earlier and more accurate disease detection and the development of highly targeted therapies. Furthermore, increased public health awareness and significant governmental and private funding initiatives aimed at combating neurodegenerative diseases worldwide are bolstering market expansion.

Major applications of Neuro Market products span clinical neurosciences, academic research, and, increasingly, consumer wellness (e.g., brain training and cognitive enhancement tools). Key benefits derived from this market include improved quality of life for patients suffering from chronic neurological conditions, enhanced surgical precision through advanced robotics, and a deeper mechanistic understanding of complex brain functions. Driving factors include demographic shifts leading to an aging population, which is highly susceptible to neurodegenerative illnesses, breakthroughs in genomic sequencing linked to neurological disorders, and the continuous development of less invasive treatment options, shifting the paradigm from symptom management to disease modification.

The Neuro Market is experiencing robust growth fueled by several interlocking business, regional, and segmental trends. Business trends are characterized by substantial merger and acquisition activity focused on integrating small, specialized biotechnology firms with larger pharmaceutical and medtech companies, aiming to consolidate pipeline assets, particularly in areas like gene therapies and neurostimulation devices. Furthermore, significant capital investment is flowing into startups specializing in neuroinformatics and AI-driven clinical trial optimization, reflecting a shift toward data-centric approaches. Regional trends highlight North America’s dominance, driven by superior healthcare infrastructure, high reimbursement rates, and a concentration of leading research institutions. However, the Asia Pacific region is demonstrating the highest growth trajectory, primarily due to expanding access to advanced healthcare, rising awareness, and increasing government investment in public health infrastructure and neurological disorder management programs.

Segment trends indicate that the therapeutics segment, particularly biologics and specialized pharmaceuticals for rare neurological diseases, holds the largest market share but faces significant pricing and regulatory hurdles. Concurrently, the neurodiagnostic devices segment is witnessing rapid technological evolution, with demand surging for portable and non-invasive monitoring solutions (e.g., wearable EEG devices). Within the application segment, neurodegenerative diseases remain the largest contributor, although mood disorders and chronic pain management utilizing neurostimulation are rapidly increasing their market presence. Overall, the market trajectory is highly positive, driven by unmet clinical needs and technological convergence, particularly where hardware innovation meets sophisticated software algorithms.

User queries regarding the impact of Artificial Intelligence (AI) on the Neuro Market primarily center on three core themes: the potential for accelerated drug discovery, the reliability and ethics of AI-driven diagnostics, and the integration of machine learning into clinical practice for enhanced patient outcomes. Users frequently ask how AI can handle the immense complexity and heterogeneity of neurodegenerative diseases compared to traditional research methods, focusing on whether AI can accurately predict disease progression or therapeutic efficacy at an individual level. A key concern revolves around data privacy and the algorithmic transparency necessary to trust AI-s decision-making in high-stakes neurological interventions, such as surgical planning or seizure prediction. Expectations are high, anticipating that AI will significantly reduce the time and cost associated with bringing new neurological treatments to market and democratize access to high-quality diagnostic interpretations globally.

The application of AI and Machine Learning (ML) is fundamentally transforming the landscape of neuro research and clinical care. In diagnostics, deep learning algorithms are proving exceptionally adept at analyzing large volumes of neuroimaging data (MRI, PET scans), identifying subtle biomarkers predictive of Alzheimer’s or MS years before conventional diagnosis. This capability is enhancing both preclinical research and early intervention strategies. Furthermore, AI is crucial in processing electrophysiological data (EEG/ECG) to identify patterns related to seizure activity or sleep disorders, providing clinicians with more granular, actionable insights than ever before. This digital transformation improves throughput and significantly minimizes the rate of human error associated with subjective interpretation of complex medical images and signals, thereby raising the standard of care globally.

In drug development, AI models are being utilized for target identification, virtual screening of potential compounds, and predicting toxicity profiles, drastically cutting down the lead optimization phase for neurological therapeutics. This computational efficiency is particularly vital given the high failure rate traditionally associated with neuroscience drug development. Ethical considerations, however, remain central to the discourse, necessitating stringent regulatory frameworks to govern the deployment of autonomous AI systems in patient care. The future trajectory involves integrating personalized medicine data—including genomics, proteomics, and environmental factors—into comprehensive AI models to create truly individualized treatment plans for highly heterogeneous conditions like depression and schizophrenia.

The Neuro Market is profoundly shaped by a confluence of accelerating drivers, inherent restraints, strategic opportunities, and powerful external impact forces. A primary driver is the undeniable demographic shift, specifically the global aging population, which naturally experiences a higher incidence of age-related neurological disorders such as dementia and stroke. This is coupled with significant private and public sector investment aimed at addressing currently untreatable diseases, spurring innovation in gene therapy and advanced biotechnologies specifically targeting neuronal repair. Restraints often include the extremely complex nature of the blood-brain barrier (BBB), which severely limits drug delivery efficiency, leading to high clinical trial failure rates. Furthermore, the high cost of advanced neurotechnologies and lengthy regulatory approval processes for novel devices and therapeutics pose significant hurdles to market entry and widespread adoption in lower-income regions.

Opportunities within the Neuro Market are largely centered on technological breakthroughs and underserved segments. The proliferation of wearable and portable neuro-monitoring devices represents a massive opportunity for remote patient care and continuous data collection, transforming disease management from episodic to preventative. The rise of non-invasive brain stimulation techniques (e.g., TMS, tDCS) offers less burdensome treatment alternatives, expanding patient compliance and market penetration. Impact forces, such as changing healthcare policy emphasis toward preventative and personalized medicine, are influencing R&D directions. Global pandemic experiences have also highlighted the need for resilient neuro-telehealth infrastructure, accelerating digital health integration. Regulatory harmonization efforts across different jurisdictions could potentially streamline approvals, significantly impacting speed-to-market for innovative solutions.

The intricate structure of the nervous system and the inherent heterogeneity of neurological disorders mandate a cautious, yet highly innovative, approach to market development. The market is propelled by the promise of precision psychiatry and neurology, leveraging genomic data to tailor treatments. However, market growth is often tempered by reimbursement complexities, especially in emerging economies where advanced procedures remain prohibitively expensive. Navigating the ethical landscape concerning neuro-enhancement and direct neural interfaces also constitutes a substantial impact force, requiring industry stakeholders to proactively engage in policy development and public discourse to ensure responsible technological deployment.

The Neuro Market is highly diversified, segmented primarily by product type (devices, pharmaceuticals, services), application (disease type), technology, and end-user. This intricate segmentation allows market players to focus their R&D and commercial strategies on specific high-growth areas, such as advanced neuroimaging systems or specialized orphan drugs for rare neurological conditions. The pharmaceutical segment, despite facing patent cliffs and high development costs, maintains dominance due to the chronic nature of many neurological diseases requiring long-term medication. Conversely, the device segment, covering neurosurgery devices and monitoring tools, is driven by continuous innovation in miniaturization and less invasive surgical techniques. Analysis of the segments reveals a trend towards convergence, where therapeutic devices often incorporate drug delivery systems or sophisticated connectivity features, creating hybrid product offerings that redefine treatment modalities across the spectrum of neurological care.

The Neuro Market value chain is characterized by intensive upstream R&D and complex downstream distribution networks, reflecting the high-value, specialized nature of neurological products. Upstream activities are dominated by pharmaceutical and biotech companies engaged in basic neuroscience research, biomarker discovery, clinical trials, and intellectual property development. This stage requires significant financial capital and specialized scientific expertise, often involving collaborations between academia, government labs, and private enterprises. Key inputs include proprietary biological materials, advanced computational modeling tools, and specialized chemical synthesis capabilities. Successful navigation of the highly stringent regulatory environment (FDA, EMA) is a major checkpoint in transitioning from research to manufacturing, particularly for novel neuropharmacological agents or implantable devices.

The midstream involves the high-precision manufacturing of neurodevices, drug formulation, and quality control. Device manufacturing requires adherence to strict ISO standards and specialized cleanroom environments, particularly for sensitive implantable electronics. Downstream logistics focus on the distribution channels, which are typically bifurcated into direct sales models for high-cost, specialized surgical equipment (requiring manufacturer-employed clinical specialists) and indirect channels utilizing large medical distributors for pharmaceuticals and consumable diagnostic supplies. Hospitals, specialized neurology clinics, and academic centers serve as the primary points of consumption, where highly trained physicians and surgeons manage product integration and utilization.

The efficiency of the distribution channel is critical, especially for neuro-biologics that require cold chain logistics, and for cutting-edge devices that necessitate rapid, specialized technical support and clinician training. The market sees a growing emphasis on digital integration throughout the value chain, utilizing cloud platforms for managing patient data collected by diagnostic devices and employing direct-to-patient pharmacy services for chronic medication management. Optimized inventory management and streamlined regulatory compliance across international borders are continuously sought after to maximize profitability and reduce supply chain vulnerabilities inherent in high-tech medical markets.

Potential customers within the Neuro Market span a wide array of specialized healthcare providers, research entities, and regulatory bodies, all focused on acquiring advanced solutions for diagnosing and treating nervous system disorders. The largest segment of end-users comprises hospitals and specialized neurology clinics, which purchase high-volume pharmaceuticals, expensive neurodiagnostic imaging equipment, and complex neurosurgical systems. These institutional buyers prioritize product efficacy, long-term reliability, comprehensive technical support, and favorable reimbursement codes, making purchasing decisions lengthy and highly consultative, involving both procurement officers and key opinion leaders (KOLs) among the medical staff.

Another critical customer segment includes academic research institutions and government-funded laboratories dedicated to basic and translational neuroscience. These entities are primary consumers of research reagents, specialized in vitro and in vivo models, sophisticated microscopy systems, and advanced neuroinformatics platforms necessary for genetic and protein analysis related to neural function. Their purchasing decisions are often budget-constrained and grant-dependent, favoring high-throughput, modular equipment that can integrate seamlessly with existing lab infrastructure. Additionally, growing interest from the military and sports medicine sectors in brain injury assessment (concussions, TBI) creates emerging customer bases for portable diagnostic tools and advanced rehabilitation technologies.

Finally, the rise of specialized diagnostic centers and independent outpatient neurological rehabilitation facilities represents a rapidly expanding customer base. These organizations require cost-effective, user-friendly diagnostic systems and therapeutic devices that facilitate patient throughput and efficient billing. The direct-to-consumer segment, while smaller and highly regulated, is also emerging, driven by demand for wellness-focused neurotech products, such as cognitive enhancement apps and personal EEG trackers, though regulatory clarity in this space remains a prerequisite for mass adoption.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 45.8 Billion |

| Market Forecast in 2033 | USD 101.5 Billion |

| Growth Rate | 12.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Medtronic, Boston Scientific Corporation, Abbott Laboratories, Johnson & Johnson, Stryker Corporation, LivaNova PLC, Elekta AB, Siemens Healthineers, GE Healthcare, Philips Healthcare, Novartis AG, Pfizer Inc., Eli Lilly and Company, Roche Holding AG, Biogen Inc., UCB S.A., Takeda Pharmaceutical Company, Brainlab AG, Nihon Kohden Corporation, MindMaze. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Neuro Market technology landscape is characterized by high levels of innovation across diagnostic imaging, neuromodulation, and bioinformatics. Key technological advancements include the maturation of high-field MRI systems and the implementation of advanced computational neuroimaging techniques that allow for functional connectivity mapping, offering unprecedented insight into brain networks affected by conditions like epilepsy and psychiatric disorders. The transition toward non-invasive and minimally invasive surgical tools, such as focused ultrasound systems for targeted drug delivery and ablative procedures, is reducing patient morbidity and expanding the treatable population. Furthermore, the development of sophisticated neurostimulation devices, including Deep Brain Stimulation (DBS) systems with sensing capabilities and closed-loop functionality, allows for precise, responsive therapy adjustments tailored to real-time neural activity, significantly improving outcomes for Parkinson’s and essential tremor patients.

Another rapidly growing area is the utilization of Brain-Computer Interfaces (BCIs) and neuroprosthetics, moving beyond academic curiosity into therapeutic application for paralysis, motor function restoration, and severe mood disorders. These technologies rely heavily on micro-electrode arrays and advanced signal processing algorithms, making the confluence of hardware engineering and machine learning critical for success. In the pharmaceutical sector, targeted delivery systems, particularly those designed to temporarily open the blood-brain barrier or utilize nanoparticles, are becoming essential technologies, overcoming the historic constraint of inadequate central nervous system (CNS) drug penetration. Gene therapy and antisense oligonucleotide technology are also gaining traction, offering the potential to modify disease progression at the genetic level for previously intractable monogenic neurological diseases.

Digital biomarkers and remote patient monitoring represent foundational technologies shaping future care delivery. Wearable sensors capable of passively monitoring physiological and movement data provide longitudinal data streams that inform diagnosis, treatment response, and disease progression tracking outside of clinical settings. This technological shift is underpinned by robust data security frameworks (e.g., compliant with HIPAA and GDPR) and cloud-based data analytics. The continuous advancement and fusion of these technologies—from molecular biology tools to complex robotic surgery systems—ensure that the Neuro Market remains at the forefront of medical technology, constantly driving towards more precise, personalized, and patient-centric care models globally.

North America maintains its dominant position in the global Neuro Market, primarily driven by the United States. This dominance is attributed to a confluence of factors, including the presence of major neurotechnology manufacturers, extensive public and private research funding (notably from the National Institutes of Health, NIH), and a highly developed, well-reimbursed healthcare system. The U.S. leads in the adoption of expensive, cutting-edge neurodiagnostic devices and complex neurosurgical procedures, such as advanced deep brain stimulation and spinal cord neuromodulation. High prevalence of chronic conditions, aggressive R&D spending by pharmaceutical giants, and a regulatory environment that, while stringent, supports rapid innovation for breakthrough devices contribute significantly to the region's market value. Canada also contributes substantially, particularly in neuroscience research and clinical trials, benefiting from strong academic-industry linkages, though the U.S. market scale dictates regional growth metrics.

Europe represents the second-largest market, characterized by stringent regulatory standards (via the European Medicines Agency, EMA, and MDR/IVDR requirements) and a healthcare system focused on widespread public accessibility. Countries like Germany, the United Kingdom, and France are hubs for medical device manufacturing and pharmaceutical development, often specializing in fields such as neuro-rehabilitation and neuroimaging informatics. Market growth in Europe is steady, supported by aging demographics and robust governmental initiatives targeting neurodegenerative disease management. However, pricing pressures and heterogeneous reimbursement policies across different member states can sometimes fragment market penetration for premium products compared to the unified purchasing power seen in the US market. Scandinavia, particularly, is known for advanced neurological epidemiology studies and early adoption of digital health solutions in neurological care, fostering localized pockets of intense technological integration.

The Asia Pacific (APAC) region is projected to exhibit the highest Compound Annual Growth Rate (CAGR) throughout the forecast period. This rapid expansion is fundamentally driven by massive underserved patient populations, improving healthcare infrastructure investments in countries like China and India, and increasing disposable incomes leading to greater accessibility of advanced treatments. Government focus on modernizing public health systems and controlling the rapid rise in non-communicable neurological diseases, such as stroke and epilepsy, fuels demand for cost-effective diagnostic tools and established generic neurological pharmaceuticals. While technological sophistication may lag slightly behind North America and Europe, localized manufacturing capabilities and favorable economic policies aimed at attracting foreign direct investment (FDI) are rapidly closing the gap, positioning APAC as the critical growth engine for the next decade.

Latin America (LATAM) and the Middle East and Africa (MEA) present evolving yet challenging markets. LATAM growth is geographically concentrated in Brazil and Mexico, where urbanization and increasing private healthcare spending drive demand for diagnostic imaging and basic neurological medications. However, significant economic instability and disparities in healthcare access across the continent restrain overall market size. The MEA region is characterized by high-value, niche markets in the Gulf Cooperation Council (GCC) states, which possess advanced, heavily funded health systems capable of adopting premium neurosurgical technologies. Conversely, vast areas of Africa face significant infrastructural barriers, relying heavily on philanthropic and public health initiatives for access to basic neurological care, focusing primarily on infectious diseases with neurological manifestations, like meningitis. Future growth in these regions is contingent upon economic stabilization, infrastructure development, and substantial improvements in neurological professional training.

The primary growth drivers are the escalating global prevalence of chronic neurological disorders (especially due to the aging population), significant technological advances in neuroimaging and neurostimulation devices, and substantial public and private funding directed toward neuroscience research and treatment development.

The Neurotherapeutic Drugs segment currently commands the largest market share, driven by the persistent need for long-term pharmacological management of common conditions such as epilepsy, depression, stroke recovery, and pain management, despite ongoing challenges in developing disease-modifying therapies.

AI is revolutionizing neurological diagnosis by enabling faster, more accurate analysis of complex data, including MRI and EEG scans. AI algorithms identify subtle biomarkers predictive of disease onset or progression, drastically improving early detection and supporting personalized treatment planning.

Major challenges include the physiological barrier presented by the Blood-Brain Barrier (BBB), which restricts drug entry into the central nervous system, and the inherent complexity and heterogeneity of neurodegenerative diseases, resulting in historically high clinical trial failure rates and significant R&D costs.

The Asia Pacific (APAC) region is anticipated to exhibit the fastest Compound Annual Growth Rate (CAGR), propelled by rapidly expanding healthcare access, increasing governmental focus on neurological disease management, and growing awareness among large, underserved patient populations, particularly in emerging economies like China and India.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.