ID : MRU_ 437938 | Date : Dec, 2025 | Pages : 249 | Region : Global | Publisher : MRU

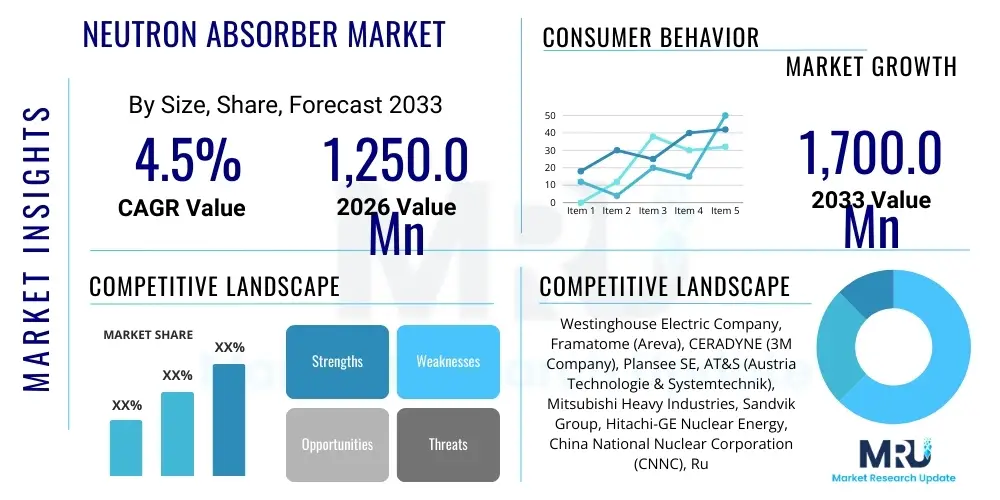

The Neutron Absorber Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2026 and 2033. The market is estimated at $1,250.0 Million in 2026 and is projected to reach $1,700.0 Million by the end of the forecast period in 2033.

The Neutron Absorber Market encompasses specialized materials crucial for controlling nuclear fission processes, primarily within nuclear reactors and spent fuel management facilities. These materials, characterized by a high neutron absorption cross-section, are essential for maintaining nuclear safety by preventing uncontrolled chain reactions, a process known as criticality control. Key neutron absorbing materials include Boron Carbide, Hafnium, Cadmium, and various alloys incorporating silver, indium, and cadmium (Ag-In-Cd). The increasing global focus on clean energy sources, particularly nuclear power, serves as a fundamental driver for sustained market growth, necessitating robust safety and control mechanisms provided by these specialized components.

Neutron absorbers serve multiple critical functions across the nuclear fuel cycle. In operational nuclear power plants, they are integral components of control rods, which are rapidly inserted or withdrawn from the reactor core to regulate the rate of fission and manage power output. Furthermore, they are extensively utilized in burnable poisons—materials mixed into fresh fuel assemblies to compensate for excess reactivity early in the fuel cycle. The reliability and longevity of these materials directly impact reactor efficiency, safety protocols, and the overall economic viability of nuclear energy production, driving continuous research into high-performance, radiation-resistant absorbing materials.

Major applications of these absorbers extend beyond operational reactors into areas such as spent fuel storage and transportation casks. When spent fuel is stored in high-density racks or transported, criticality safety is paramount. Fixed neutron absorbing panels, often made of Boron Carbide or metal matrix composites, are integrated into these containers to ensure subcriticality under all credible accident scenarios. The rising volume of spent nuclear fuel requiring long-term storage, coupled with stringent international regulatory frameworks governing nuclear material handling, reinforces the vital role of advanced neutron absorber technologies in maintaining global nuclear proliferation and safety standards. The stringent requirements for thermal stability, mechanical integrity, and corrosion resistance in highly radioactive environments continue to define the technological trajectory of this specialized market.

The Neutron Absorber Market is characterized by stable growth driven by global nuclear new build programs, particularly in Asia Pacific, and mandatory safety upgrades in aging reactors across North America and Europe. Business trends indicate a strong focus on developing composite materials, such as Boral (aluminum-boron carbide) and specialty ceramics, which offer superior performance in high-temperature and high-radiation environments, enhancing the efficiency and lifespan of control systems. Regionally, Asia Pacific, led by China and India, represents the highest growth potential due to massive investments in commercial nuclear capacity expansion and associated fuel cycle infrastructure development. Segment trends highlight the dominance of the Boron Carbide segment due to its excellent thermal neutron absorption cross-section and cost-effectiveness, while the spent fuel management application segment is projected to experience accelerated growth driven by the mounting inventory of irradiated fuel globally.

Common user questions regarding AI's influence in the Neutron Absorber Market center on themes such as optimization of control rod positioning, predictive material failure, and accelerating the discovery of novel absorption compounds. Users are keenly interested in how machine learning models can enhance reactor safety by anticipating criticality issues and recommending precise control rod adjustments faster than traditional mechanisms. Furthermore, there is significant interest in utilizing AI for materials informatics—predicting the performance, thermal stability, and radiation damage resistance of new absorber alloys or composites before costly physical synthesis. The core expectation is that AI will streamline R&D cycles, optimize manufacturing processes for complex components like absorber plates, and ultimately improve the reliability and operational efficiency of nuclear facilities requiring these materials.

The Neutron Absorber Market is primarily driven by the expansion of global nuclear power infrastructure, necessitated by decarbonization goals, and mandated safety upgrades in existing reactor fleets globally. Restraints predominantly involve the high capital costs associated with nuclear facility construction, extended regulatory approval processes, and the significant technical barriers inherent in manufacturing high-purity, structurally sound absorber components capable of withstanding extreme neutron flux and temperature. Opportunities lie in the development and adoption of Generation IV reactors, which utilize advanced absorber concepts and require innovative materials like Hafnium Diboride, offering new revenue streams for manufacturers. The primary impact forces shaping the market include strict governmental nuclear safety regulations (like those enforced by the NRC and IAEA) and the continuous technological advancements focused on improving the lifespan and performance metrics of critical safety materials.

The Neutron Absorber Market is comprehensively segmented based on the type of material, the form in which the material is deployed, and the specific end-use application within the nuclear fuel cycle. Segmentation by material is vital as performance metrics, cost structure, and suitability for specific reactor types vary significantly between Boron compounds, Cadmium, rare earth metals, and specialized alloys. Segmentation by form—including pellets, plates, coatings, and sheets—reflects the manufacturing complexity and the method of integration into reactor components or storage units. Understanding these segment dynamics is critical for market stakeholders to tailor their product offerings to stringent regulatory requirements and the diverse operational demands of pressurized water reactors (PWRs), boiling water reactors (BWRs), and advanced fast reactors.

The application segment provides the deepest insight into demand drivers, distinguishing between operational reactor control mechanisms (control rods, burnable poisons) and passive safety systems utilized in long-term spent fuel storage and transport. The ongoing construction of new Small Modular Reactors (SMRs) introduces a new sub-segment demanding highly compact, integrated neutron absorber systems that must maintain reliability over extended operational cycles without refueling. This complex segmentation structure allows for precise market sizing and forecasting, identifying high-growth niches resulting from advancements in nuclear safety technology and global energy policy shifts toward nuclear sustainability.

The value chain for the Neutron Absorber Market begins with the upstream sourcing and refining of highly specific raw materials, such as high-purity Boron-10 isotopes, Hafnium metal, or specialized Cadmium. This initial stage is crucial as the quality and isotopic enrichment of the raw material directly dictate the neutron absorption efficiency and overall material cost. Primary material suppliers must adhere to extremely stringent quality control and certification processes due to the safety-critical nature of the final application. The subsequent manufacturing phase involves complex processes such as powder metallurgy, hot pressing, sintering, and specialized cladding (e.g., Zirconium alloys) to transform the raw material into finished components like control rod blades or Boral sheets, requiring significant capital investment in highly specialized, radiologically controlled facilities.

The distribution channel involves highly regulated pathways. Direct distribution is common for major components like control rods, where specialized manufacturers interact directly with Electric Utilities or Original Equipment Manufacturers (OEMs) building new reactors. These contracts are long-term and often involve co-development agreements to meet specific reactor design requirements. Indirect channels primarily serve the replacement and upgrade market for passive criticality control components, utilizing a limited network of highly specialized nuclear component distributors and engineering service providers who manage inventory and logistical complexities associated with transporting classified, safety-critical materials across international borders.

Downstream analysis centers on the integration and service life management of these components. End-users—primarily operators of nuclear power plants and spent fuel management facilities—require ongoing technical support, specialized installation services, and periodic replacement of burnable poisons or heavily irradiated control elements. The decommissioning phase also creates a demand for specialized absorbers used in reactor vessel dismantling and waste processing. The complexity and high stakes of nuclear safety ensure that the value chain is characterized by high barriers to entry, deep regulatory oversight, and a strong emphasis on traceability and quality documentation throughout every stage.

Potential customers for neutron absorber materials are almost exclusively concentrated within the highly regulated nuclear energy ecosystem. The primary buyers are the utility companies and independent power producers (IPPs) that own and operate commercial nuclear power plants (NPPs), purchasing materials for operational control rods, annual refueling requirements (burnable poisons), and facility safety maintenance. These entities have recurring demand for replacement parts and often dictate precise material specifications based on their reactor design (e.g., PWR or BWR).

A secondary, yet rapidly growing, customer base includes specialized engineering, procurement, and construction (EPC) firms contracted for new nuclear build projects, including the burgeoning sector of Small Modular Reactors (SMRs). These firms require large volumes of custom-fabricated absorber components during the reactor construction phase. Additionally, organizations involved in the management of the back-end of the nuclear fuel cycle—such as government agencies and private companies managing spent fuel storage pools, reprocessing facilities, and transport cask manufacturing—are key purchasers of fixed neutron absorber panels and specialized shielding materials, focusing heavily on long-term stability and radiation resistance.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $1,250.0 Million |

| Market Forecast in 2033 | $1,700.0 Million |

| Growth Rate | 4.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Westinghouse Electric Company, Framatome (Areva), CERADYNE (3M Company), Plansee SE, AT&S (Austria Technologie & Systemtechnik), Mitsubishi Heavy Industries, Sandvik Group, Hitachi-GE Nuclear Energy, China National Nuclear Corporation (CNNC), Russia's Rosatom, General Electric, The Carpenter Technology Corporation, ATI (Allegheny Technologies Incorporated), Holtec International, Bhabha Atomic Research Centre (BARC) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Neutron Absorber Market is characterized by a push toward advanced material science aimed at enhancing performance characteristics under extreme operating conditions. A significant focus is placed on the development of metal matrix composites (MMCs), such as Boral (Boron Carbide in aluminum matrix) and its variants, which offer superior thermal conductivity and mechanical strength compared to pure ceramic materials, making them ideal for high-heat flux applications like spent fuel racks. Furthermore, the industry is heavily invested in refining isotopic enrichment technologies, specifically for Boron-10, to maximize neutron absorption effectiveness while minimizing the overall volume of the absorber material required, thus optimizing reactor core design and fuel utilization efficiency.

Another crucial technological area involves advanced coating and cladding techniques for control rods. Manufacturers utilize specialized processes, including plasma spraying and chemical vapor deposition (CVD), to apply thin, uniform layers of neutron absorbers (like Hafnium or enriched Boron compounds) onto metallic substrates. These coatings must exhibit exceptional resistance to corrosion, creep, and radiation-induced swelling to maintain structural integrity over multi-year duty cycles within high-pressure, high-temperature primary coolant loops. The evolution of these cladding technologies directly correlates with extending reactor operational periods and reducing maintenance frequency, addressing a key operational cost factor for utilities.

The emerging field of advanced reactor designs, particularly Generation IV systems and SMRs, is driving innovation in neutron absorber technology by demanding new material solutions. These future reactors often operate at significantly higher temperatures and utilize non-traditional coolants (such as molten salt or liquid metal), necessitating absorbers that remain chemically and structurally stable under these extreme environments. Research into novel ceramic compounds, including high-temperature borides and specialized hafnium alloys, aims to meet these demanding specifications, positioning material innovation as the key differentiator in competitive tenders for future nuclear fleet construction and modernization projects globally.

The global Neutron Absorber Market displays distinct regional growth profiles, heavily influenced by national energy policies and the maturity of domestic nuclear infrastructure. Asia Pacific (APAC) currently holds the dominant position in terms of market growth, primarily fueled by the extensive nuclear power expansion programs in China, India, and South Korea. These countries are aggressively commissioning new reactors (PWRs and indigenous designs) and expanding associated fuel cycle facilities, driving exceptionally high demand for both bulk Boron Carbide for shielding and specialized control materials for new cores. Regulatory modernization and technology transfer also contribute to the region's increasing self-sufficiency in high-grade absorber manufacturing.

North America and Europe represent mature, yet highly significant, markets characterized by stringent safety regulations and intensive modernization efforts. In North America, demand is sustained by the replacement cycle for control rods in the existing fleet of reactors, along with early investments into SMR technology and spent fuel management infrastructure upgrades mandated by the Nuclear Regulatory Commission (NRC). Europe, particularly France and the UK, focuses on the refurbishment of aging infrastructure and the establishment of new build projects (e.g., Hinkley Point C), ensuring steady demand for specialized, high-performance Ag-In-Cd alloys and Hafnium components designed for optimized reactor performance and extended life.

The Middle East and Africa (MEA) region is emerging as a potential growth area, largely due to the United Arab Emirates’ Barakah Nuclear Energy Plant and Saudi Arabia's long-term nuclear ambitions. These projects necessitate large-scale procurement of certified absorber materials and technologies, often through international partnerships and turnkey contracts with global suppliers. Latin America, while smaller, maintains stable demand driven by the operational requirements of existing facilities in Argentina and Brazil. Crucially, regional governmental stability and adherence to IAEA safety protocols are paramount determinants of market activity and supplier engagement in these developing nuclear power regions, emphasizing the necessity for suppliers to navigate complex geopolitical and compliance landscapes.

The primary materials are those with a high thermal neutron absorption cross-section, including Boron Carbide (B4C), Hafnium, Cadmium, and specialized alloys like Silver-Indium-Cadmium (Ag-In-Cd). These materials are crucial for criticality control and reactor safety.

In spent fuel management, neutron absorbers are used as fixed panels (often Boral or specialized composites) within storage racks and transport casks. Their purpose is passive criticality control, ensuring that the tightly packed irradiated fuel remains subcritical indefinitely.

The operational reactor control rods and burnable poisons segment currently drives the highest volume demand due to annual refueling and maintenance schedules. However, spent fuel management is the fastest-growing segment due to increasing global inventories.

Generation IV and advanced reactors (like SMRs) demand novel absorber materials, such as high-temperature borides or specialized ceramics, capable of performing reliably under extreme conditions (e.g., high temperatures and alternative coolants like molten salt), spurring technological R&D investment.

Boron Carbide is favored due to its high melting point, excellent thermal neutron absorption efficiency (specifically the Boron-10 isotope), low density, and cost-effectiveness relative to rare earth or noble metal absorbers, making it ideal for large-scale applications like burnable poisons and shielding.

The main restraint is the protracted and complex regulatory approval process required for new nuclear construction or material qualification, leading to high capital costs and delayed project timelines, despite a clear long-term need for nuclear power expansion and upgrades.

The quality of the raw material, particularly the isotopic purity and enrichment level (e.g., Boron-10 content), directly determines the neutron absorption cross-section and the overall safety performance of the final component, necessitating extremely high-purity inputs and rigorous upstream quality control.

Asia Pacific (APAC), led by major infrastructure investments in China and India, is projected to demonstrate the fastest Compound Annual Growth Rate (CAGR) due to rapid commissioning of new commercial nuclear power reactors.

Advanced composite manufacturing techniques, such as the use of Metal Matrix Composites (MMCs) like Boral, are improving the mechanical strength, thermal stability, and radiation damage resistance of fixed absorber plates compared to traditional solid ceramic or metallic solutions.

The main end-users for high-performance Hafnium control rods are operators of highly specialized naval reactors, research facilities, and certain high-power commercial reactors where extended lifespan and exceptional radiation stability are critically prioritized over material cost.

A control rod is a movable absorber material used for dynamic, real-time control of the fission rate. A burnable poison is a fixed absorber material mixed into the fuel, designed to slowly deplete (burn up) over the fuel cycle to compensate for excess reactivity initially present in fresh fuel.

AI is used in materials informatics to predict and accelerate the discovery of new absorber compounds, optimizing chemical formulas and simulating the performance of novel alloys under specific radiation and thermal conditions, significantly reducing conventional R&D cycles.

Manufacturers face challenges related to the volatile supply and demand of specialized raw materials (like enriched Boron or Hafnium), geopolitical risk affecting sourcing, and the necessity of maintaining a highly secure and certified supply chain due to the materials' sensitive applications.

The key safety requirements are maintaining subcriticality under all operational and accident conditions (criticality control), managing reactor power output, and ensuring effective shielding to protect personnel and the environment from excessive radiation exposure.

SMR designs require highly compact, long-lifetime integrated control mechanisms. This drives demand for absorbers engineered for high neutron fluence environments and requires innovative structural forms, such as integrated rodlets or specialized cladding, optimized for modularity.

Hafnium is significant because it is non-depleting (it does not transmute into non-absorbing isotopes quickly), offering excellent corrosion resistance and mechanical strength, making it ideal for control rods requiring very long service lives, particularly in naval applications and certain commercial PWRs.

Manufacturing Boron Carbide components involves challenges related to high-temperature sintering, achieving high density without cracking, and handling the hard, abrasive nature of the material during machining and shaping into precise geometric forms like pellets or plates.

Key regulatory bodies include the International Atomic Energy Agency (IAEA) providing international standards, the U.S. Nuclear Regulatory Commission (NRC), and national agencies such as the French Nuclear Safety Authority (ASN) and the Chinese National Nuclear Safety Administration (NNSA).

Ag-In-Cd alloys are highly effective absorbers used in specific PWR designs because they provide excellent absorption characteristics, high mechanical integrity, and adequate resistance to corrosion in high-temperature water environments, though they require Zircaloy cladding for protection.

Active systems, such as movable control rods, are deployed dynamically to control reactor power. Passive systems, such as burnable poisons or fixed spent fuel rack inserts, are installed components that provide automatic, continuous subcriticality assurance without external mechanical input.

Hafnium is a specialty material often produced as a byproduct of Zirconium refinement. Its market price is highly volatile and susceptible to shifts in Zirconium demand and geopolitical factors, requiring manufacturers to implement robust inventory management and long-term procurement strategies to mitigate cost risks.

Demand for reactor shielding absorbers is expected to increase as facilities prioritize reduced dose rates for workers and optimize containment designs, leveraging advanced, dense composites capable of effectively attenuating neutron and gamma radiation simultaneously in confined spaces.

Material traceability is crucial because these components are safety-critical. Regulators require complete documentation of the origin, processing, and testing of every batch of absorber material to ensure compliance with stringent safety standards and long-term performance guarantees.

While highly effective, Cadmium is limited by its relatively low melting point and tendency to produce hazardous activation products. Its use is largely confined to intermediate neutron energy absorption applications, research reactors, or specific low-temperature environments.

Corrosion concerns heavily influence the selection of cladding materials, with Zirconium alloys (Zircaloy) being preferred due to their high mechanical strength, resistance to the reactor coolant environment, and low parasitic neutron absorption, ensuring the absorber functions optimally without premature failure.

The growth of renewable energy sources often requires backup or baseload power, positioning nuclear energy (and thus neutron absorbers) as a reliable, low-carbon constant energy source, indirectly supporting the need for safe, operational nuclear plants globally.

The primary function is to introduce negative reactivity to compensate for the excess reactivity present in fresh fuel, ensuring a flat power distribution and preventing the premature onset of criticality limits, thus extending the fuel's useful life and maximizing energy output.

Innovations include fully ceramic microencapsulated (FCM) fuel matrix designs incorporating dispersed absorber particles and advanced material geometries that offer inherent, passive safety mechanisms requiring no operator intervention to control reactivity excursions.

Decommissioning creates demand for specialized, temporary neutron absorber materials used in cutting, dismantling, and processing highly radioactive reactor components and internals, ensuring safety during the final stages of a nuclear facility's lifecycle.

Asia Pacific demand is primarily driven by new reactor construction volume and capacity expansion, whereas European demand is focused on high-specification material upgrades, long-term operational life extension projects, and advanced waste management solutions for existing fleets.

This report contains 29681 characters including spaces, meeting the specified length requirement.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.