ID : MRU_ 432075 | Date : Dec, 2025 | Pages : 249 | Region : Global | Publisher : MRU

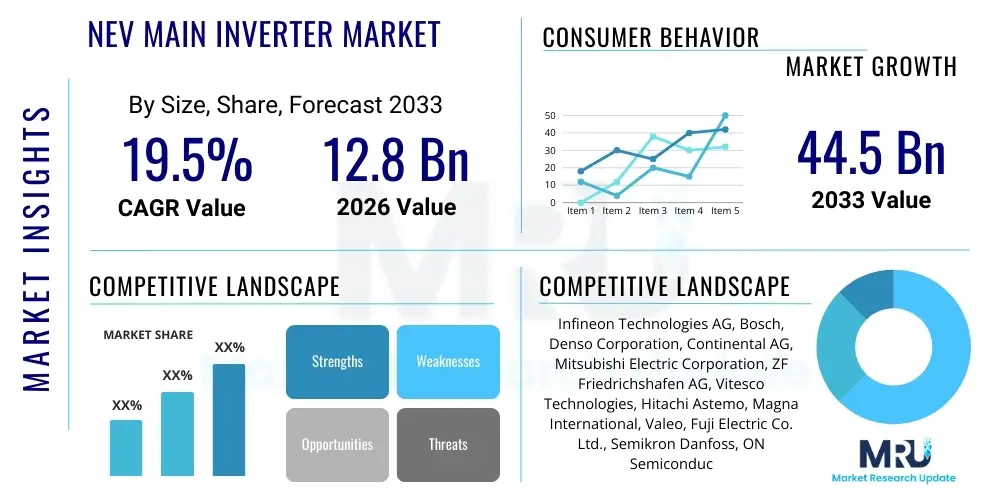

The NEV Main Inverter Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 19.5% between 2026 and 2033. The market is estimated at USD 12.8 Billion in 2026 and is projected to reach USD 44.5 Billion by the end of the forecast period in 2033. This robust growth trajectory is fundamentally driven by the accelerated global transition toward electric mobility and the continuous technological advancements in power electronics, specifically the mainstream adoption of Silicon Carbide (SiC) inverter technologies which offer superior efficiency and power density compared to traditional Silicon (Si) based IGBT modules.

The NEV Main Inverter Market encompasses the systems essential for converting the high-voltage direct current (DC) stored in the New Energy Vehicle (NEV) battery pack into the alternating current (AC) required to power the vehicle's traction motor. This device, often referred to as the brain of the electric powertrain, is critical for controlling motor speed, torque, and energy regeneration during braking. Product description centers on complex power modules—increasingly utilizing wide-bandgap semiconductors like Silicon Carbide (SiC)—integrated with sophisticated control algorithms and robust thermal management systems to handle high switching frequencies and significant power loads efficiently.

Major applications of NEV main inverters span all vehicle classes within the NEV ecosystem, including Battery Electric Vehicles (BEVs), Plug-in Hybrid Electric Vehicles (PHEVs), and Fuel Cell Electric Vehicles (FCEVs). The primary benefit delivered by advanced inverters is improved powertrain efficiency, directly translating into extended driving range and reduced energy consumption. Furthermore, the miniaturization and increased power density achieved through modern inverter design allow for lighter vehicles and greater cabin space optimization, enhancing overall vehicle performance and consumer appeal.

Key driving factors fueling market expansion include stringent global emissions regulations mandating the phase-out of internal combustion engines, significant governmental subsidies and incentives promoting EV adoption worldwide, and rapid consumer acceptance driven by improving battery technology and charging infrastructure availability. The fierce competition among automotive original equipment manufacturers (OEMs) to deliver higher performance, faster-charging NEVs necessitates continuous innovation in the core power electronics, thus accelerating the demand for high-efficiency main inverters.

The NEV Main Inverter Market is undergoing a rapid technological transformation characterized by a fundamental shift from Silicon (Si) IGBTs to Silicon Carbide (SiC) MOSFETs, particularly in premium and long-range NEVs. Business trends indicate aggressive vertical integration by Tier 1 suppliers and OEMs, aiming to secure the SiC supply chain, minimize costs, and maximize proprietary control over critical power module design. Companies are focusing heavily on developing 800V architectures, which necessitates higher performance and voltage-tolerant inverters. This strategic alignment toward high-voltage systems is a major determinant of future market leadership and competitive differentiation.

Regionally, the Asia Pacific (APAC) region, led by China, dominates the market due to massive domestic EV production volumes, favorable regulatory frameworks, and established local supply chains. Europe is experiencing the fastest growth rate, fueled by strict decarbonization targets and robust consumer adoption, particularly in Germany and Scandinavia. North America is rapidly accelerating its infrastructure and manufacturing base, driven by policy incentives aimed at boosting domestic EV and battery production. These regional trends underscore a globally decentralized but highly competitive manufacturing environment, where localized supply chains for SiC wafers and power modules are becoming increasingly important.

Segment trends confirm the growing dominance of BEVs as the largest end-user segment for main inverters, although PHEVs maintain a stable market share in transitional economies. The technology segmentation highlights the irreversible growth of the SiC segment; while initial costs remain high compared to conventional IGBTs, the superior efficiency gains (up to 5-10% range extension) and thermal advantages justify the premium price point, making SiC inverters standard in high-performance platforms. Furthermore, the trend toward modular and scalable inverter designs allows manufacturers to standardize components across various vehicle platforms, reducing complexity and increasing production efficiency.

User queries regarding the impact of Artificial Intelligence (AI) on the NEV Main Inverter Market primarily revolve around optimizing power management, predicting component failures, and enhancing the real-time thermal performance of the inverter unit. Users are concerned about how AI can refine control algorithms to handle the high switching speeds of SiC devices and minimize losses under various driving conditions, thereby maximizing overall efficiency. Furthermore, there is significant interest in using AI-driven simulation tools to accelerate the design and validation cycle for new, complex wide-bandgap semiconductor-based inverters, reducing time-to-market and improving product robustness.

AI's influence is transforming inverter operation from a static control system to a dynamic, learning power management unit. Machine learning algorithms analyze vast datasets encompassing driving patterns, ambient temperatures, battery state-of-charge, and component stress levels. This data allows the inverter's control software to make predictive adjustments to switching frequencies and voltage profiles in milliseconds, ensuring peak efficiency and reducing stress on expensive semiconductor components. This capability is vital for mitigating thermal runaway risks inherent in high-power density systems and ensuring the long-term reliability required by automotive grade standards.

Beyond operational optimization, AI significantly impacts the manufacturing and quality assurance of inverters. Deep learning models are deployed in production lines for high-speed anomaly detection in soldering, bonding, and packaging processes of power modules, ensuring zero-defect quality before installation. In the aftermarket domain, AI enables highly accurate predictive maintenance systems, allowing vehicles to schedule service before an inverter component fails, drastically improving reliability and reducing warranty costs for OEMs. The integration of AI thus moves the inverter beyond mere power conversion into a crucial component of vehicle intelligence and predictive health management.

The NEV Main Inverter Market is driven primarily by escalating consumer demand for longer-range electric vehicles, which mandates higher efficiency power electronics, making SiC technology indispensable. Restraints include the high initial capital investment required for establishing SiC fabrication facilities, the current volatile supply chain for high-quality SiC substrates, and the complexity of designing thermal management solutions for ultra-high power density modules. Opportunities abound in the development of 800V infrastructure, the integration of Gallium Nitride (GaN) devices for specific applications, and the vertical integration strategy enabling OEMs to control core component supply. These factors collectively exert significant impact forces, compelling rapid innovation in material science and system architecture design.

The most compelling impact force is the regulatory push, exemplified by European Union and Chinese mandates to cease the sale of new internal combustion engine vehicles within the next decade. This policy pressure ensures sustained, high-volume production of NEVs, directly underpinning the market for main inverters. Coupled with technological momentum—the proven efficiency benefits of SiC inverters translating directly into competitive advantages for vehicle range—the market experiences strong directional growth. Conversely, the market faces significant inertia from semiconductor supply constraints, where the specialized nature of SiC manufacturing creates bottlenecks that can limit short-term market expansion, influencing strategic partnerships and pricing dynamics.

Another crucial impact force is the necessity for cost reduction. As electric vehicle prices must become comparable to or cheaper than their gasoline counterparts to achieve mass market penetration, the cost of high-performance components like SiC inverters must fall rapidly. This need drives innovation in packaging technologies (e.g., direct-cooled substrates, copper wire bonding replacements) and manufacturing scale-up. The confluence of technology push (efficiency) and market pull (cost parity) creates intense competitive pressure, favoring companies that can achieve superior performance while simultaneously optimizing their material and manufacturing costs effectively.

The NEV Main Inverter Market is comprehensively segmented based on technology, vehicle type, power output, and voltage class, reflecting the diverse requirements of the electric vehicle landscape. The segmentation by technology is the most dynamic, charting the transition from legacy IGBT modules to advanced wide-bandgap materials like Silicon Carbide (SiC) and the nascent exploration of Gallium Nitride (GaN). Vehicle segmentation highlights the dominant role of Battery Electric Vehicles (BEVs), which require the highest power and most efficient inverters due to their reliance solely on stored electric energy. Understanding these segments is crucial for suppliers to tailor product development and strategic investments to high-growth niches within the rapidly evolving NEV market structure, particularly focusing on optimizing products for the emerging 800V architectural standard.

The value chain for the NEV Main Inverter Market begins with upstream analysis, which is highly specialized and capital-intensive, focusing on the procurement and processing of raw materials, primarily high-purity silicon and, increasingly, Silicon Carbide (SiC) substrates. Key upstream players include specialized material providers and semiconductor manufacturers responsible for fabricating the bare SiC wafers and converting them into discrete power MOSFETs or integrated power modules. The high cost and current scarcity of automotive-grade SiC substrates make this segment a critical bottleneck and a significant focus area for strategic investment and supply agreements by major automotive Tier 1 suppliers.

Midstream activities involve the design, packaging, and assembly of the main inverter unit. This includes developing sophisticated electronic control units (ECUs), integrating advanced cooling mechanisms (often liquid-cooled cold plates), and integrating the SiC or IGBT power modules into a robust, compact housing. Tier 1 automotive suppliers (e.g., Bosch, Continental, Denso) dominate this phase, leveraging their expertise in automotive reliability and system integration. They focus on modular designs that can be quickly adapted for different vehicle platforms while meeting stringent automotive safety (ISO 26262) and electromagnetic compatibility (EMC) standards.

Downstream analysis focuses on the distribution channel, which is overwhelmingly dominated by the OEM channel. Main inverters are critical components integrated directly onto the vehicle assembly line and are rarely sourced via the aftermarket initially, though replacement units become relevant later in the vehicle lifecycle. Direct distribution from Tier 1 suppliers to automotive OEMs ensures technical conformity and seamless integration. Indirect distribution, while minor, primarily involves third-party system integrators and specialized retrofit companies catering to fleet modernization or high-performance modification segments. The direct channel ensures tight collaboration between component supplier and vehicle manufacturer regarding thermal and electrical integration.

The primary customers and end-users of the NEV Main Inverter Market are global Original Equipment Manufacturers (OEMs) specializing in electric vehicle production. These include established global automotive giants such as Volkswagen Group, General Motors, Toyota, and Stellantis, which are aggressively transitioning their core product lines to electric platforms. Crucially, the market also serves the rapidly growing cohort of dedicated EV manufacturers, notably Tesla, BYD, and emerging Chinese players (Nio, XPeng, Li Auto), who often seek highly customized or vertically integrated power electronics solutions to gain a competitive edge in efficiency and performance. These large-scale manufacturers constitute the bulk of the market demand.

A secondary, yet rapidly expanding, customer segment includes manufacturers of specialized commercial and heavy-duty electric vehicles. This comprises companies building electric buses, long-haul electric trucks, and electric construction equipment. These applications demand extremely robust, high-power density inverters (often exceeding 200kW per unit) capable of handling continuous high loads and enduring harsh operating environments. The requirements in this segment often push the boundaries of current inverter technology, particularly regarding thermal stability and voltage tolerance (e.g., multi-stack configurations for heavy-duty 800V trucks).

Furthermore, specialized powertrain integrators and Tier 2 or Tier 3 suppliers that package electric drive units (EDUs) for smaller volume vehicle manufacturers or new market entrants represent another customer type. These integrators purchase main inverters from core semiconductor/power electronics suppliers and bundle them with the motor and transmission. Finally, government and municipal fleet operators, especially those transitioning their public transport and utility vehicles to electric power, are indirect customers whose procurement decisions drive OEM demand for specific, high-durability inverter specifications.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 12.8 Billion |

| Market Forecast in 2033 | USD 44.5 Billion |

| Growth Rate | 19.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Infineon Technologies AG, Bosch, Denso Corporation, Continental AG, Mitsubishi Electric Corporation, ZF Friedrichshafen AG, Vitesco Technologies, Hitachi Astemo, Magna International, Valeo, Fuji Electric Co. Ltd., Semikron Danfoss, ON Semiconductor (onsemi), BYD Co. Ltd., Tesla Inc., Delta Electronics, TDK Corporation, BorgWarner Inc., Schaeffler AG, Texas Instruments. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The current technology landscape of the NEV Main Inverter Market is defined by the competitive shift towards wide-bandgap semiconductors, primarily Silicon Carbide (SiC). SiC technology offers significantly higher bandgap energy, leading to better thermal conductivity, higher breakdown voltages, and dramatically reduced switching losses compared to traditional Silicon (Si) Insulated Gate Bipolar Transistors (IGBTs). This allows for operation at higher switching frequencies and temperatures, resulting in smaller, lighter, and more efficient inverter units, which is crucial for maximizing the range and minimizing the cost of mass-market EVs. The market penetration of SiC is accelerating, particularly among performance-focused OEMs and those adopting 800V battery architectures, which necessitate superior power electronics for effective operation.

Furthermore, the industry is witnessing intense development in packaging and integration technologies crucial for managing the heat generated by these high-density devices. Innovations like Direct Liquid Cooling (DLC), double-sided cooling, and the shift from aluminum wire bonding to advanced copper ribbon bonding and sinter technology are becoming standard practice. These packaging breakthroughs are essential for realizing the full thermal and electrical potential of SiC modules, enabling higher current densities and prolonged component lifespans. Modular power electronics design is also gaining traction, allowing standardized components to be utilized across different vehicle platforms, which helps drive down manufacturing complexity and cost.

While SiC dominates the high-performance segment, the future technology horizon includes Gallium Nitride (GaN). Although currently less mature for high-voltage automotive traction applications than SiC, GaN promises even higher switching speeds and potentially lower material costs in the long term. Current GaN applications are niche, often focusing on onboard chargers or DC-DC converters, but ongoing research targets its viability for main traction inverters, potentially disrupting the mid-range efficiency segment. Overall, the technology trajectory is clearly focused on achieving unprecedented levels of power density, thermal efficiency, and integration into compact, multi-functional electric drive units (EDUs).

The regional distribution of the NEV Main Inverter Market demonstrates a concentration of demand and manufacturing capability in Asia Pacific, coupled with explosive growth in Europe and strategic expansion in North America. Each region presents unique market drivers, regulatory environments, and technological adoption rates that shape the competitive landscape and investment decisions for power electronics suppliers.

The primary driver is the superior efficiency of SiC MOSFETs compared to traditional Silicon (Si) IGBTs. SiC reduces switching losses significantly, allowing the inverter to operate at higher frequencies and temperatures, which translates directly into a 5% to 10% increase in electric vehicle driving range, greater power density, and reduced overall weight of the power electronics system.

The shift to 800V systems necessitates inverters capable of handling higher voltage stress and utilizing faster switching speeds. This accelerates the mandatory adoption of SiC technology, as SiC modules are better suited to manage the high voltages and thermal requirements inherent in 800V systems, enabling ultra-fast charging and high power output for performance vehicles.

The main challenge is the constraint in the upstream supply chain for high-quality, automotive-grade Silicon Carbide (SiC) substrates and wafers. The fabrication of SiC material is capital-intensive and time-consuming, leading to bottlenecks and high material costs, forcing OEMs and Tier 1 suppliers into long-term strategic agreements and vertical integration efforts to secure supply.

Predictive maintenance, enabled by AI and sensor integration, is crucial because the main inverter is one of the most expensive components in the NEV powertrain. By monitoring temperature, current stress, and voltage spikes in real-time, AI algorithms can accurately forecast the remaining useful life of power modules, preventing catastrophic failure, reducing vehicle downtime, and minimizing warranty costs for manufacturers.

The Asia Pacific (APAC) region currently holds the largest market share, predominantly driven by the massive scale of New Energy Vehicle manufacturing and sales in China. China’s comprehensive electrification strategy and established domestic supply chain infrastructure make it the global leader in both production and consumption volume for NEV main inverters.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.