ID : MRU_ 435170 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

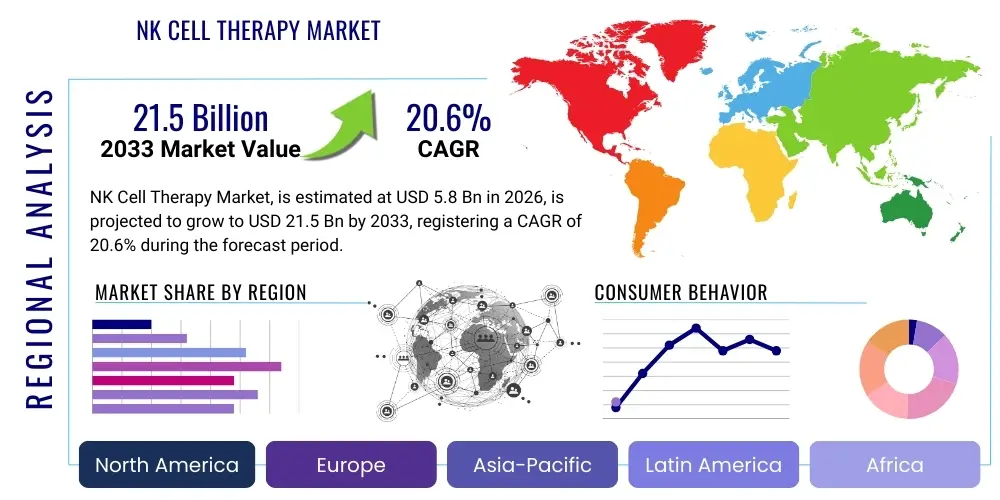

The NK Cell Therapy Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 20.6% CAGR between 2026 and 2033. The market is estimated at $5.8 Billion USD in 2026 and is projected to reach $21.5 Billion USD by the end of the forecast period in 2033.

Natural Killer (NK) cell therapy represents a paradigm shift in oncology and infectious disease treatment, leveraging the innate immune system's capacity to identify and destroy abnormal cells without prior sensitization. This therapeutic approach harnesses highly cytotoxic lymphocytes, which are integral to immunosurveillance, particularly against malignant cells and virally infected targets. Unlike T-cell therapies (such as CAR T), NK cells offer potential advantages in terms of reduced risk of cytokine release syndrome (CRS) and neurotoxicity, alongside the ability to utilize allogeneic sources, thereby streamlining manufacturing and improving accessibility for off-the-shelf treatments. The product scope encompasses both autologous NK cell expansions, utilizing a patient’s own cells, and the more commercially viable allogeneic NK cells derived from healthy donors, umbilical cord blood, or induced pluripotent stem cells (iPSCs).

Major applications of NK cell therapies are predominantly focused on hematological malignancies, including acute myeloid leukemia (AML) and non-Hodgkin lymphoma (NHL), as well as solid tumors, such as colorectal, ovarian, and non-small cell lung cancer (NSCLC). Research is rapidly expanding into combining NK cells with monoclonal antibodies (e.g., ADCC enhancement) or utilizing them in conjunction with checkpoint inhibitors to maximize anti-tumor activity. The inherent benefits driving market adoption include the NK cell's intrinsic tumor-homing ability, rapid onset of action, and their compatibility with genetic engineering techniques to enhance persistence, target specificity, and functional potency, such as through chimeric antigen receptor (CAR) modification or cytokine priming.

Driving factors propelling market growth include the rising global incidence of cancer, coupled with increased investment in cell and gene therapy research infrastructure across North America and APAC. Furthermore, significant technological advancements in cell expansion protocols, cryopreservation techniques, and gene editing tools (like CRISPR/Cas9 for enhanced persistence) are making these therapies more scalable and efficacious. The shift toward standardized, off-the-shelf allogeneic products is a crucial catalyst, addressing the logistical and manufacturing hurdles inherent in personalized autologous treatments. Regulatory approvals and fast-track designations for promising NK cell candidates further stimulate clinical development and market entry, solidifying NK cell therapy's position as a cornerstone of next-generation immunotherapy.

The NK Cell Therapy market is experiencing robust acceleration driven by pivotal advancements in allogeneic platforms and heightened strategic investments by both pharmaceutical giants and specialized biotech firms. Current business trends indicate a strong focus on intellectual property surrounding iPSC-derived NK cells (iPSC-NK) and genetically engineered NK products (e.g., CAR-NK), which promise superior persistence and targeting capabilities compared to traditional NK cell expansions. Collaboration and licensing agreements between academic institutions, Contract Development and Manufacturing Organizations (CDMOs), and commercial entities are vital for scaling production and navigating complex regulatory landscapes, especially in the transition from clinical trials to commercialization. The urgency to develop standardized, high-volume production methods to meet future clinical demand is shaping the competitive landscape, emphasizing process automation and quality control.

Regionally, North America maintains market dominance, primarily due to substantial funding in biotechnology, the presence of key industry players, and a well-established regulatory pathway (FDA) that encourages rapid clinical translation. However, the Asia Pacific (APAC) region, spearheaded by China and Japan, is emerging as the fastest-growing market, propelled by increasing government support for regenerative medicine, a burgeoning patient pool, and lower manufacturing costs allowing for competitive positioning. European markets are characterized by stringent but supportive regulatory frameworks (EMA), focusing heavily on clinical trial harmonization and reimbursement policies, which are critical for patient access and widespread adoption.

Segmentation analysis highlights the increasing dominance of the allogeneic source segment, particularly those derived from umbilical cord blood or iPSCs, due to their potential for mass production and reduced immunological risk compared to donor-matched approaches. The oncology indication segment remains the primary revenue driver, encompassing both liquid tumors where NK cells have shown immediate promise, and the more challenging solid tumor landscape, which requires enhanced homing and persistence strategies. Among end-users, specialty clinics and comprehensive cancer centers are expected to exhibit the highest growth, driven by their capacity to manage complex infusion protocols and provide specialized post-treatment care required for cell therapies.

User inquiries regarding Artificial Intelligence (AI) in NK cell therapy primarily revolve around how AI can optimize target identification, accelerate clinical trial design, and enhance manufacturing consistency. Users express interest in AI's role in predicting therapeutic response based on patient genomics and tumor microenvironment characteristics, reducing trial failures and personalizing treatment. A major concern is the scalability of complex manufacturing processes; users want to know if machine learning (ML) can optimize cell culture media composition, expansion rates, and quality control (QC) parameters, thereby ensuring highly potent and reproducible therapeutic doses. Additionally, there is significant interest in using AI for rapid analysis of high-dimensional flow cytometry and single-cell sequencing data generated during preclinical and clinical testing to better understand NK cell function and persistence mechanisms.

The NK Cell Therapy market dynamics are currently shaped by strong drivers centered around technological innovation and unmet medical needs, counterbalanced by significant restraints relating to manufacturing complexity and regulatory hurdles. Opportunities are vast, primarily in extending applications to solid tumors and infectious diseases, while the impact forces include intense competition from established T-cell therapies and the necessity for robust, scalable production platforms. The interplay between these forces dictates the pace of commercialization and market penetration, with investment flowing heavily into solutions that address current scalability and persistence challenges, particularly through genetic engineering and allogeneic sourcing.

Drivers: The paramount driver is the documented clinical efficacy of NK cells in hematological malignancies, coupled with their inherently favorable safety profile compared to CAR-T therapies, notably the lower incidence of severe CRS and neurotoxicity. Furthermore, the ability of NK cells to be utilized in an allogeneic (off-the-shelf) manner revolutionizes accessibility and logistics, making these treatments viable for widespread commercial distribution. Increased R&D funding from venture capital and governmental bodies, specifically targeting immuno-oncology, fuels rapid translational research and clinical pipeline expansion. The synergistic potential of NK cells when combined with established treatments, such as monoclonal antibodies (enhancing ADCC) or checkpoint inhibitors, further broadens their therapeutic utility and drives adoption.

Restraints: Significant restraints impede market growth, primarily stemming from the technical challenge of achieving sufficient NK cell persistence and proliferation in vivo following infusion, especially in the immunosuppressive tumor microenvironment of solid tumors. Manufacturing complexity, high production costs associated with GMP compliance, and the requirement for highly specialized labor and infrastructure pose substantial logistical and financial burdens, limiting scalability. Another critical restraint is the heterogeneity in NK cell products derived from different sources (peripheral blood, UCB, iPSC), making standardization difficult and complicating regulatory review processes globally. The relatively limited clinical experience and long-term efficacy data compared to mature T-cell therapy modalities also contribute to cautious adoption among clinicians and payers.

Opportunities: Major opportunities reside in optimizing the next generation of genetically modified NK cells, such as CAR-NK and cytokine-primed NK cells, which promise enhanced potency and extended persistence crucial for tackling solid tumors. Developing standardized, automated, and closed-system manufacturing processes (e.g., utilizing bioreactors) offers a clear path to cost reduction and global scaling. Furthermore, expanding the therapeutic scope beyond oncology into chronic viral infections (HIV, Hepatitis B) and autoimmune disorders represents a massive untapped market. The rise of sophisticated delivery mechanisms and targeted conditioning regimens aimed at improving NK cell survival and homing provides fertile ground for strategic partnerships and innovation.

The NK Cell Therapy market is segmented based on Source, Target Indication, and End-User, reflecting the diverse approaches to therapy development and deployment. The analysis reveals a significant pivot in development efforts toward allogeneic sources, driven by the desire for readily available, consistent, and cost-effective treatments. While oncology remains the dominant therapeutic area, particularly hematological cancers, the solid tumor segment represents the highest potential growth trajectory, contingent upon overcoming current biological limitations in cell trafficking and survival within dense tumor microenvironments. End-user segmentation highlights the critical role of specialized infrastructure in clinical adoption.

The value chain for NK Cell Therapy is complex and highly specialized, beginning with upstream activities focused on sourcing and critical material production. Upstream analysis involves the procurement of source materials—whether patient-derived (autologous), healthy donor leukapheresis, umbilical cord blood (UCB), or induced pluripotent stem cells (iPSCs). Critical materials include specialized viral vectors for genetic modification (e.g., CAR expression), GMP-grade cytokines (e.g., IL-2, IL-15, IL-21) necessary for robust expansion, and proprietary culture media formulations. Manufacturers rely heavily on specialized suppliers and CDMOs that can ensure the high quality and regulatory compliance of these starting materials, representing a major cost center and a critical bottleneck if supply chain integrity is compromised.

Midstream activities encompass the core manufacturing processes: cell isolation, genetic modification (if applicable), large-scale expansion, formulation, and cryopreservation. This stage demands sophisticated, closed-system automation (to reduce contamination risk) and rigorous in-process and final product quality control (QC). Direct manufacturing involves significant capital expenditure on GMP facilities and advanced bioreactors. Due to the high complexity and requirement for specialized expertise, many emerging biotech firms outsource or collaborate extensively with experienced CDMOs to navigate regulatory expectations and achieve industrial scale. Process efficiency and reproducibility at this stage are key determinants of commercial viability.

Downstream activities involve logistics, distribution, and administration. The distribution channel is highly specific, requiring a secure, certified cold chain network (often ultra-low temperature cryogenic transport) to ensure cell viability from the manufacturing site to the point of care. Direct distribution involves manufacturers delivering products directly to specialty cancer centers, where highly trained clinical staff administer the infusion. Indirect distribution may involve partnerships with specialized logistics providers and pharmacy service networks that manage the complex last-mile delivery. Due to the perishable nature of the product and high cost, direct oversight and stringent tracking protocols are mandatory, making the distribution highly centralized and specialized to maintain product integrity and patient safety.

The primary customers for NK Cell Therapy products are institutions specializing in advanced oncology and hematology care, characterized by high treatment volumes and infrastructure capable of supporting complex cellular therapy administration. End-users typically include comprehensive cancer centers affiliated with major academic medical institutions, which serve as key sites for clinical trials, early adoption, and centers of excellence for high-risk patient populations. These centers possess the specialized physicians (e.g., oncologists, hematologists), nursing staff, and sophisticated hospital infrastructure, including dedicated apheresis units and intensive care units (ICUs), necessary to manage potential side effects.

A rapidly expanding customer segment comprises specialty clinics and private hospitals that are strategically investing in cellular therapy capabilities to offer state-of-the-art treatments, particularly as allogeneic therapies become standardized and easier to integrate into standard care protocols. For these institutions, the decision to adopt NK cell therapy is driven by competitive market positioning, patient demand for cutting-edge treatments, and the increasing availability of off-the-shelf products that reduce the logistical burden compared to autologous options. Access to reimbursement pathways and favorable payor coverage also heavily influence the purchasing decisions of these institutional customers.

Furthermore, research institutes and academic laboratories constitute a crucial segment, although they primarily function as consumers of early-stage products, research-grade reagents, and technology platforms used for developing novel NK cell modifications and therapeutic strategies. These customers drive preclinical innovation and the initial development phases of next-generation NK cell therapies, focusing on optimizing transduction methods, enhancing cytotoxicity, and exploring novel combinations. Their purchasing decisions are driven by grant funding, research objectives, and the need for highly specialized cellular starting materials and advanced analytical equipment, positioning them as essential contributors to the pipeline of future commercially viable therapies.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $5.8 Billion USD |

| Market Forecast in 2033 | $21.5 Billion USD |

| Growth Rate | 20.6% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Fate Therapeutics, Kiadis Pharma (Sanofi), Nkarta, Nektar Therapeutics, Takeda Pharmaceutical, Celgene (BMS), Innate Pharma, Dragonfly Therapeutics, ONK Therapeutics, Affimed, Acepodia, Glycostem Therapeutics, Kuur Therapeutics, Catapult Cell Therapy, Vor Biopharma, Wugen, Shoreline Biosciences, Artiva Biotherapeutics, CellforCure, Gamida Cell. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The NK Cell Therapy technology landscape is defined by continuous innovation aimed at enhancing cell potency, persistence, and manufacturing scalability. A core technological focus is the development of robust and reproducible methods for large-scale NK cell expansion. This involves optimizing specialized bioreactors (e.g., wave-mixing or stirred-tank systems) and proprietary serum-free culture media, often supplemented with potent recombinant cytokines such as IL-15, IL-21, or engineered variants thereof, to achieve clinical doses of billions of highly active cells. Furthermore, sophisticated cryopreservation techniques are crucial for maintaining the viability and function of allogeneic, off-the-shelf products during complex global distribution, utilizing specialized freeze media and controlled rate freezers.

Another crucial area involves genetic engineering technologies utilized to create enhanced NK cell products. The most prominent application is the use of Chimeric Antigen Receptors (CARs) to redirect NK cells against specific tumor antigens (CAR-NK). Unlike CAR-T, CAR-NK cells often utilize non-viral vector systems or specific integration strategies (e.g., using gamma retroviral or lentiviral vectors adapted for NK cells, or transposons) to enhance safety and efficiency. Parallel research focuses on gene editing techniques (e.g., CRISPR/Cas9) to knock out inhibitory receptors or insert genes for enhanced persistence cytokines (e.g., constitutively active IL-15), thereby overcoming the short half-life traditionally associated with native NK cells in vivo.

The frontier of technology deployment heavily involves Induced Pluripotent Stem Cell (iPSC) technology. iPSCs represent an infinitely renewable source, allowing manufacturers to generate large, homogeneous batches of NK cells (iPSC-NK) with consistent characteristics and potency, addressing the batch-to-batch variability often seen with primary cell sources. This technological capability drastically improves manufacturing logistics and standardization, making high-volume, global commercialization feasible. Automation and digitalization, particularly through specialized Cell and Gene Therapy (CGT) software platforms and robotic liquid handlers, are increasingly integrated across the entire workflow—from isolation to quality testing—to reduce human error, ensure GMP compliance, and increase throughput necessary for commercial success.

North America, led by the United States, holds the dominant share in the NK Cell Therapy Market. This region benefits from the highest concentration of leading biotech and pharmaceutical companies, robust governmental and private sector funding for cellular therapy research, and highly sophisticated research infrastructure. The established and relatively quick regulatory approval pathway provided by the FDA, coupled with favorable reimbursement policies for innovative oncology treatments, accelerates clinical translation and market uptake. Major academic medical centers are centralizing expertise, acting as key opinion leaders and primary sites for pivotal clinical trials, further cementing the region's market leadership. The competitive environment drives continuous technological improvements in CAR-NK and iPSC platforms.

Europe represents a mature market with significant contributions from countries like Germany, the UK, and France. While regulatory processes under the EMA are rigorous, the focus is on harmonizing standards across member states, which, once achieved, facilitates broader market access. Research initiatives are often government-backed and collaborative across institutions, focusing heavily on safety profiles and optimizing manufacturing processes for cost-efficiency suitable for public healthcare systems. Adoption rates are steady, supported by strong clinical research and a growing patient base, although reimbursement negotiations often introduce commercialization delays compared to the U.S. market.

The Asia Pacific (APAC) region is projected to be the fastest-growing market globally due to rapidly increasing cancer incidence, growing investment in biopharmaceutical manufacturing capabilities, and supportive regulatory environments in key countries like China, Japan, and South Korea. China, in particular, has positioned itself as a global leader in clinical trial volume for cell therapies, backed by significant national funding and a relatively streamlined process for advanced therapy medicinal products (ATMPs). Japan’s proactive regulatory approach (e.g., Sakigake designation for regenerative medicine) encourages rapid development and approval, making the region increasingly attractive for global companies seeking expansive market penetration and lower manufacturing overheads.

Latin America (LATAM) and the Middle East & Africa (MEA) currently represent smaller market shares but are poised for future expansion. Growth in these regions is primarily driven by increasing healthcare expenditure, a rise in medical tourism for advanced treatments, and infrastructure improvements in major economies like Brazil, Saudi Arabia, and South Africa. Adoption is currently limited by high treatment costs, lack of specialized manufacturing facilities, and evolving regulatory frameworks. However, increasing collaboration with global cell therapy developers and the eventual availability of more affordable, off-the-shelf allogeneic therapies are expected to unlock significant market potential in the latter half of the forecast period.

The primary advantage is the significantly reduced risk of severe side effects, such as Cytokine Release Syndrome (CRS) and neurotoxicity. Additionally, NK cells can often be sourced allogeneically (from healthy donors or universal sources like iPSCs) without causing Graft-versus-Host Disease (GvHD), facilitating scalable, off-the-shelf treatment availability.

iPSC-derived NK cells (iPSC-NK) are critical for market scaling because they provide a standardized, renewable source of cells. This addresses major manufacturing bottlenecks associated with patient- or donor-derived cells, ensuring consistency, high volume, and reduced per-dose cost for commercial production.

The biggest challenges include achieving sufficient in vivo persistence and proliferation, especially when treating solid tumors, and overcoming the high complexity and cost associated with GMP-compliant, large-scale cell manufacturing and cryogenic distribution logistics.

North America, particularly the United States, leads the market due to concentrated R&D funding, a robust biotech ecosystem, favorable regulatory support from the FDA, and a high volume of active clinical trials for advanced cell therapies like CAR-NK.

CAR-NK cells are Natural Killer cells genetically engineered with a Chimeric Antigen Receptor (CAR) to specifically recognize and target antigens expressed on cancer cells. They are the next generation because the CAR modification significantly enhances their specificity and cytotoxicity, potentially overcoming the limitations of native NK cells.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.