ID : MRU_ 432384 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

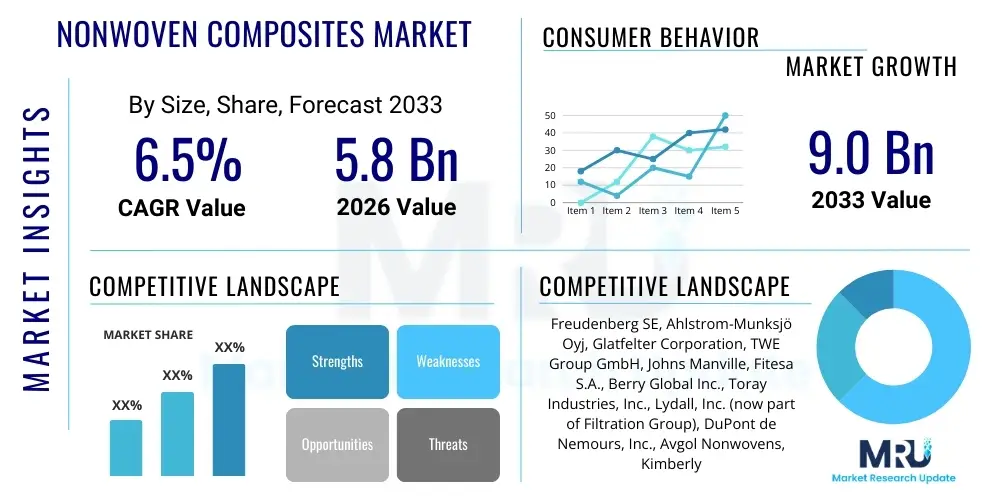

The Nonwoven Composites Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at USD 5.8 Billion in 2026 and is projected to reach USD 9.0 Billion by the end of the forecast period in 2033. This growth trajectory is fundamentally driven by the increasing demand for high-performance, lightweight materials across critical industrial sectors, particularly automotive, construction, and specialized filtration. Nonwoven composites offer a unique combination of flexibility, strength-to-weight ratio, and cost-effectiveness compared to traditional reinforced plastics or woven fabrics. The integration of various materials such as glass fiber, carbon fiber, and thermoplastic polymers within a nonwoven matrix allows for tailored properties essential for complex engineering applications. Furthermore, the global emphasis on enhancing energy efficiency and reducing material consumption in manufacturing processes positions nonwoven composites as an indispensable solution for modern material engineering challenges. The market valuation reflects sustained investment in new production technologies and the expansion of application scope in emerging economies.

Nonwoven composites are engineered materials formed by combining nonwoven fabrics, which are web structures bonded by mechanical, chemical, or thermal means, with other reinforcement materials or polymers to achieve synergistic functional properties. These materials transcend the limitations of conventional nonwovens by incorporating features like enhanced tensile strength, improved barrier properties, thermal resistance, or superior acoustic absorption, making them ideal for rigorous applications where multi-functionality is paramount. Common material systems involve a nonwoven base of polypropylene (PP), polyethylene terephthalate (PET), or rayon, which is then reinforced with fiberglass, carbon fiber matting, or laminated with films and breathable membranes. The resultant composites are integral to the automotive industry for interior components and lightweight structural parts, significantly contributing to vehicle weight reduction and fuel efficiency improvements. In the construction sector, nonwoven composites serve as durable roofing materials, geotextiles for soil stabilization, and advanced insulation barriers, providing long-term structural integrity and energy conservation benefits. The specialized nature of these materials means their adoption is highly correlated with innovation in end-user industries demanding higher performance standards and regulatory compliance regarding safety and sustainability. The intrinsic benefits, including their ability to be tailored precisely for specific end-use requirements, low production waste compared to woven materials, and relatively high processing speeds, solidify their critical role in the advanced materials landscape.

The Nonwoven Composites Market exhibits robust growth propelled by major business trends centered around sustainability, digitalization, and functional material innovation. Regionally, the Asia Pacific (APAC) dominates market share, primarily due to rapid industrialization, burgeoning construction activities, and substantial automotive manufacturing bases in countries like China and India, alongside increasing governmental focus on infrastructure development. North America and Europe, however, lead in technological advancement and the adoption of high-value, specialized composites driven by strict environmental regulations mandating lightweight and recyclable materials. Segment trends indicate a significant shift towards thermoplastic-based nonwoven composites due to their recyclability and ease of processing, positioning them favorably against thermoset alternatives in applications requiring lower cure cycles and reduced manufacturing complexity. Furthermore, the application segment is witnessing explosive growth in medical and hygiene products, where advanced nonwoven composites provide superior liquid barrier protection, breathability, and microbial resistance, a trend significantly accelerated by recent global health crises. The strategic focus of key market players involves forward integration into end-user markets and securing specialized raw material supply chains to mitigate volatility. These companies are heavily investing in proprietary bonding and lamination techniques to create composites with enhanced structural integrity and multi-layered functionality, ensuring sustained competitive advantage in this rapidly evolving market landscape.

User queries regarding the impact of Artificial Intelligence (AI) on the Nonwoven Composites Market frequently revolve around optimizing complex manufacturing parameters, achieving flawless quality control at high speeds, and accelerating the discovery of novel material formulations. Users are concerned with how AI can minimize waste, predict equipment failures (preventative maintenance), and integrate diverse sensor data from continuous production lines to maintain uniformity in the composite structure, especially concerning fiber orientation and bonding strength. The key themes underscore the expectation that AI and machine learning (ML) will revolutionize material formulation and process engineering by managing multivariate inputs—such as polymer melt temperature, fiber density, calendar pressure, and web speed—that traditionally require extensive trial-and-error. The consensus expectation is that AI will move the industry closer to 'zero-defect' manufacturing and significantly shorten the R&D cycle for next-generation, sustainable nonwoven composites. AI-driven simulation platforms are increasingly replacing physical prototyping, allowing manufacturers to test thousands of material combinations and structural architectures virtually, ensuring rapid commercialization of performance-optimized products tailored to specific application requirements while simultaneously reducing material cost and energy expenditure in the supply chain.

The Nonwoven Composites Market is shaped by a confluence of strong drivers (D), persistent restraints (R), emerging opportunities (O), and significant impact forces. Key drivers include the escalating global demand for lightweight materials in transportation to improve fuel economy and reduce emissions, alongside substantial governmental investments in public infrastructure projects that require durable and cost-effective geotextiles and construction reinforcements. Furthermore, the rapid expansion of the healthcare sector, particularly for high-quality disposable medical textiles and protective equipment, provides sustained impetus for specialized nonwoven composite growth. Restraints primarily involve the inherent volatility and increasing cost of key raw materials, particularly petroleum-based polymers (PP, PET) and specialized reinforcing fibers like glass and carbon, which directly affect manufacturing profitability and pricing stability. Additionally, the challenge of recycling multi-material composites presents a technical hurdle and a regulatory burden, hindering full lifecycle sustainability. Opportunities lie predominantly in developing bio-based and biodegradable nonwoven composites, appealing to eco-conscious consumers and meeting strict European environmental directives, and expanding specialized applications in renewable energy infrastructure, such as wind turbine blades and solar panel components. The major impact forces include stringent global regulatory standards (e.g., REACH in Europe, CAFE standards in the US) pushing for safer, lighter, and more environmentally compliant materials, alongside the disruptive impact of advanced bonding and lamination technologies that continuously redefine the functional possibilities of nonwoven structures, forcing manufacturers to rapidly innovate and adopt capital-intensive, high-tech production methodologies to remain competitive.

The Nonwoven Composites Market is comprehensively segmented based on material type, manufacturing process, application, and geography, reflecting the diversity and specialization within the industry. Understanding these segments is crucial for strategic planning, as market dynamics vary significantly between, for instance, meltblown-based composites used in filtration and needle-punched composites utilized in the automotive sector. The primary material segmentation includes thermoplastic polymers (polypropylene, polyester), natural fibers, and reinforcement materials (glass fiber, carbon fiber). Manufacturing process differentiation focuses on the bonding mechanism used to create the composite structure, such as thermal bonding, chemical bonding, and mechanical intertwining (needling). Application segments provide the most granular view of demand, spanning industries from infrastructure development and consumer electronics to sophisticated medical devices and high-end protective apparel. Each segment exhibits unique growth drivers and competitive landscapes, often dictated by specific regulatory requirements and end-user performance specifications, necessitating highly customized product offerings from manufacturers.

The value chain for the Nonwoven Composites Market begins at the upstream segment, dominated by petrochemical companies and specialized fiber producers supplying essential raw materials such as polypropylene pellets, PET chips, and high-performance fibers (glass and carbon). Price volatility in these raw materials significantly impacts downstream profitability, making long-term procurement contracts crucial. The middle segment comprises nonwoven fabric manufacturers who utilize processes like spunbonding, meltblowing, or carding to form the base web, followed by critical conversion steps where the nonwoven structure is combined with other materials (films, reinforcements, resins) through lamination, coating, or thermal bonding to create the composite. This manufacturing stage requires high capital investment in sophisticated machinery and precise process control. Downstream analysis involves the distribution channel, which utilizes both direct sales (for large volume contracts with major automotive OEMs or construction companies) and indirect channels (distributors and converters who supply smaller specialized markets). End-users typically purchase in bulk for integration into final products. Key to optimizing this chain is vertical integration, where major producers control both raw fiber production and final composite conversion, ensuring cost efficiency and quality control. The transition towards sustainable materials necessitates significant R&D collaboration between upstream suppliers and downstream converters to integrate bio-based polymers and facilitate efficient end-of-life recycling mechanisms, driving innovation across all stages of the value chain.

The primary consumers and end-users of nonwoven composites span several capital-intensive and consumer-focused industries, driven by the demand for enhanced durability, reduced weight, and multi-functionality. Major potential customers include global Automotive Original Equipment Manufacturers (OEMs) and their Tier 1 suppliers, who utilize these materials extensively for vehicle interior liners, sound absorption panels, trunk linings, and lightweight structural components aimed at meeting strict emissions and fuel efficiency standards. Another critical customer base is within the global Construction and Infrastructure Development sector, specifically firms specializing in geotechnical engineering and building insulation, where high-performance geotextiles and roofing underlayments are mandatory for long-term project viability and structural integrity. Furthermore, major players in the Hygiene and Personal Care industry, including manufacturers of disposable diapers, adult incontinence products, and high-end wipes, rely on specialized nonwoven composites for their superior barrier, fluid management, and softness properties. The Medical Device and Healthcare sector represents a rapidly expanding customer segment, demanding sterile, high-barrier composites for surgical drapes, gowns, and face masks. Finally, industrial filtration companies are core customers, utilizing composites tailored for high-efficiency particulate air (HEPA) filters and specialized liquid filtration media required in pharmaceutical, food and beverage, and semiconductor manufacturing processes. These customers seek materials that offer a superior performance-to-cost ratio and compliance with specific industry regulatory bodies.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 5.8 Billion |

| Market Forecast in 2033 | USD 9.0 Billion |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Freudenberg SE, Ahlstrom-Munksjö Oyj, Glatfelter Corporation, TWE Group GmbH, Johns Manville, Fitesa S.A., Berry Global Inc., Toray Industries, Inc., Lydall, Inc. (now part of Filtration Group), DuPont de Nemours, Inc., Avgol Nonwovens, Kimberly-Clark Corporation, Mitsui Chemicals, Inc., Asahi Kasei Corporation, P. H. Glatfelter Company, H.B. Fuller Company, ExxonMobil Chemical Company, Teijin Limited, Jofo Nonwovens, Suominen Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Nonwoven Composites Market is characterized by continuous innovation aimed at improving material functionality, structural integrity, and manufacturing efficiency, often focusing on blending different fiber types and bonding methods. Core technologies revolve around the primary web formation methods such as spunbond, where extruded polymers are spun into continuous filaments and laid into a web; meltblown, which uses high-velocity air to attenuate polymer streams into microfibers; and drylaid processes like carding and airlaying, which manipulate staple fibers. However, the 'composite' aspect relies heavily on secondary and tertiary processing techniques. Key advancements include sophisticated thermal bonding methods (e.g., ultrasonic welding and patterned calendering) that precisely fuse the nonwoven layers to reinforcing materials or functional membranes without the use of chemical adhesives, leading to lighter and potentially more recyclable structures. Furthermore, multi-layer lamination processes, particularly those involving extrusion coating and hot-melt adhesives, are crucial for creating high-barrier composites used in medical and construction applications, requiring precise control over layer thickness and uniformity to ensure optimal performance characteristics such as water vapor transmission rate (WVTR) and hydrostatic head pressure. Another critical technological development involves the integration of functional additives—such as antimicrobial agents, flame retardants, or UV stabilizers—directly into the polymer melt or applied via surface treatments, allowing the composite material to possess performance characteristics beyond simple structural reinforcement. This focus on functionalization, coupled with high-speed processing capabilities, defines the competitive edge in the advanced nonwoven composites manufacturing environment, ensuring rapid production of tailored materials compliant with demanding industry specifications and driving substantial capital expenditure in advanced machinery and robotics for handling delicate web materials.

The primary driver is the global regulatory push for vehicle lightweighting and improved fuel efficiency, which necessitates the use of high-strength, low-density nonwoven composites for interior components, filtration systems, and noise reduction applications.

High-performance composites often rely on combining specialized spunbond or meltblown webs with advanced lamination techniques and chemical or thermal bonding to integrate reinforcing layers like glass or carbon fibers, ensuring tailored multi-functionality and strength.

The main challenge is the inherent difficulty in efficiently recycling multi-material composites, which typically combine different polymer types, films, and reinforcements. Manufacturers are addressing this through the development of mono-material or bio-based composite structures.

The market is segmented into three primary material categories: thermoplastics (PP, PET), natural fibers (cotton, wood pulp), and high-performance reinforcement materials (glass fiber, carbon fiber), each catering to distinct industrial application requirements.

The Asia Pacific (APAC) region currently holds the largest market share, driven by rapid urbanization, significant infrastructure development, and substantial manufacturing bases in the hygiene, medical, and automotive sectors across countries like China and India.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.