ID : MRU_ 427548 | Date : Oct, 2025 | Pages : 241 | Region : Global | Publisher : MRU

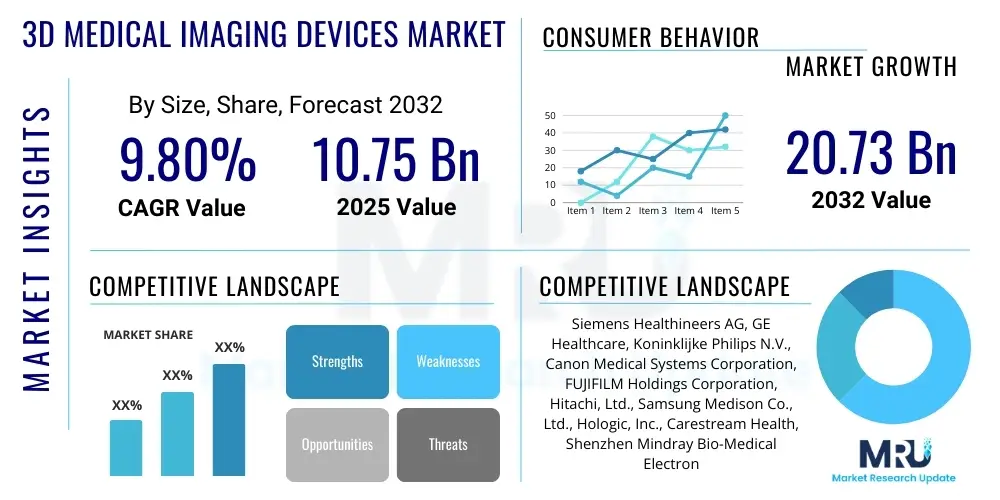

The 3D Medical Imaging Devices Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2032. The market is estimated at USD 10.75 billion in 2025 and is projected to reach USD 20.73 billion by the end of the forecast period in 2032.

The 3D Medical Imaging Devices Market encompasses advanced diagnostic and interventional tools that generate three-dimensional representations of anatomical structures and physiological processes. These devices leverage sophisticated technologies such as Computed Tomography (CT), Magnetic Resonance Imaging (MRI), Ultrasound, Positron Emission Tomography (PET), and advanced X-ray systems to provide detailed, multi-planar views of the human body. Unlike traditional 2D imaging, 3D imaging offers superior spatial resolution and depth perception, enabling clinicians to visualize complex structures, pathologies, and organ systems with unprecedented clarity. This enhanced visualization capability is crucial for accurate diagnosis, precise treatment planning, and effective monitoring of disease progression.

The primary applications of 3D medical imaging span a wide array of medical specialties, including cardiology, oncology, neurology, orthopedics, and gastroenterology. These devices are integral for diagnosing conditions such as tumors, vascular abnormalities, musculoskeletal injuries, and neurological disorders. Beyond diagnostics, 3D imaging plays a critical role in surgical planning, allowing surgeons to create detailed maps of surgical sites and rehearse complex procedures. They also facilitate image-guided interventions, improving precision and reducing invasiveness. The benefits extend to personalized medicine, where detailed 3D models can be used for custom implant design and patient-specific treatment strategies, ultimately leading to improved patient outcomes and reduced recovery times.

Key driving factors for the proliferation of 3D medical imaging devices include the increasing global prevalence of chronic diseases, a rapidly aging population, and continuous technological advancements. The rising demand for early and accurate disease diagnosis, coupled with a growing preference for minimally invasive procedures, further propels market expansion. Additionally, significant investments in healthcare infrastructure development, particularly in emerging economies, and supportive government initiatives promoting advanced diagnostic technologies contribute substantially to the markets robust growth trajectory. The integration of artificial intelligence and machine learning is also enhancing the capabilities and efficiency of these devices, making them indispensable in modern healthcare settings.

The 3D Medical Imaging Devices Market is currently experiencing dynamic shifts driven by a confluence of evolving business trends, distinct regional market dynamics, and significant advancements across various technological segments. Businesses are increasingly focused on strategic collaborations, mergers, and acquisitions to consolidate market share, expand product portfolios, and leverage synergistic capabilities in research and development. There is a palpable trend towards integrating artificial intelligence and machine learning into imaging software, aiming to enhance diagnostic accuracy, automate image analysis, and streamline clinical workflows. Furthermore, companies are investing heavily in cloud-based imaging solutions, enabling remote access, collaborative diagnostics, and efficient data management, which is particularly critical in expanding telehealth services.

Regionally, North America and Europe continue to dominate the market due to robust healthcare expenditures, established healthcare infrastructure, and high adoption rates of advanced medical technologies. These regions are characterized by a strong presence of key market players and a significant focus on research and development activities. However, the Asia Pacific region is rapidly emerging as a high-growth market, propelled by increasing disposable incomes, improving healthcare access, a large and aging patient population, and government initiatives aimed at modernizing healthcare facilities. Countries like China, India, and Japan are witnessing substantial investments in medical imaging infrastructure, attracting global players and fostering local innovation. This regional diversification indicates a broader global commitment to enhancing diagnostic capabilities.

Segmentation trends within the market highlight particular areas of accelerated growth and innovation. For instance, the ultrasound segment, especially in its 3D/4D variants, is seeing increased adoption due to its non-invasive nature, portability, and real-time imaging capabilities, making it valuable across numerous applications from obstetrics to point-of-care diagnostics. Similarly, the advanced CT and MRI segments are continually evolving with faster scanning times, higher resolution, and multi-parametric imaging techniques, enabling more comprehensive disease characterization. There is also a significant trend towards specialized imaging solutions tailored for specific clinical areas like oncology and neurology, driven by the imperative for highly accurate and precise diagnostic tools in managing complex diseases. The software and services components are also experiencing significant growth as AI-powered analytics and cloud solutions become integral to optimizing imaging workflows and delivering value-added services.

Artificial intelligence is profoundly transforming the 3D Medical Imaging Devices Market by revolutionizing every stage of the imaging workflow, from image acquisition and reconstruction to analysis, interpretation, and clinical decision-making. Users are keenly interested in how AI can enhance diagnostic precision, reduce diagnostic errors, and significantly improve operational efficiencies. There is a strong expectation that AI will lead to faster image processing, automated segmentation of complex anatomical structures, and the identification of subtle pathological features that might be missed by the human eye. Concerns often revolve around data privacy, the regulatory landscape for AI-driven diagnostics, and the need for rigorous validation to build trust in AI algorithms. Ultimately, the market anticipates AI will unlock new capabilities, leading to more personalized medicine and improved patient outcomes through predictive analytics.

The 3D Medical Imaging Devices Market is shaped by a robust interplay of driving forces, significant restraints, and promising opportunities, all contributing to its complex impact forces. Key drivers propelling market expansion include a global surge in the prevalence of chronic and lifestyle-related diseases, such as cardiovascular disorders, cancer, and neurological conditions, necessitating advanced diagnostic tools for early detection and precise management. The aging global population, particularly in developed nations, further fuels demand for sophisticated imaging solutions due to increased susceptibility to age-related ailments. Technological advancements, encompassing higher resolution imaging, faster acquisition times, reduced radiation exposure, and the integration of artificial intelligence, are continually enhancing the capabilities and appeal of these devices, making them indispensable in modern healthcare. Additionally, rising healthcare expenditures, particularly in emerging economies, and governmental support for medical research and infrastructure development provide substantial impetus for market growth.

Conversely, several restraints impede the markets full potential. The high initial capital cost associated with acquiring and maintaining advanced 3D medical imaging devices, alongside the expenses of specialized training for operating personnel, presents a significant barrier, particularly for smaller healthcare facilities or those in resource-constrained regions. Stringent and evolving regulatory approval processes, which vary across different geographies, can delay market entry for new technologies and increase compliance costs for manufacturers. Furthermore, a shortage of skilled radiologists, technicians, and specialists proficient in interpreting complex 3D images can limit the widespread adoption and effective utilization of these advanced systems. Data privacy and security concerns associated with handling vast amounts of sensitive patient imaging data also pose challenges, requiring robust cybersecurity measures and compliance with regulations like GDPR and HIPAA.

Despite these challenges, the market is brimming with opportunities. Emerging economies, with their rapidly expanding healthcare sectors and increasing patient awareness, represent vast untapped potential for market penetration. The burgeoning field of personalized medicine, which relies heavily on detailed anatomical and functional insights provided by 3D imaging, offers new avenues for device application and innovation. The ongoing integration of Artificial Intelligence and Machine Learning into imaging workflows promises to enhance diagnostic accuracy, automate routine tasks, and improve overall efficiency. Furthermore, the growing adoption of telehealth and remote diagnostic services, particularly post-pandemic, creates opportunities for cloud-based imaging solutions and remote image analysis. Research and development into novel imaging biomarkers and hybrid imaging techniques also present significant long-term growth prospects. These dynamic forces underscore a market poised for considerable transformation and expansion.

The 3D Medical Imaging Devices Market is extensively segmented to reflect the diverse landscape of technologies, applications, and end-users driving its growth. This detailed segmentation provides critical insights into market dynamics, enabling stakeholders to understand specific growth drivers, competitive landscapes, and emerging opportunities within various sub-sectors. The market is primarily broken down by product type, encompassing a range of sophisticated modalities, each offering unique capabilities and clinical advantages. Further segmentation by application highlights the specific medical fields where these technologies are most impactful, while end-user categorization illustrates the primary healthcare settings adopting these devices. Geographic segmentation reveals regional disparities in market maturity and growth potential, driven by varying healthcare infrastructures and regulatory environments.

The value chain for the 3D Medical Imaging Devices Market is an intricate network of specialized entities, spanning from raw material suppliers to the ultimate end-users in healthcare settings. At the upstream end, the process begins with the procurement of critical raw materials and highly specialized components. This includes suppliers of advanced sensors, detectors, high-performance computing units, sophisticated optics, and specialized materials like superconducting magnets for MRI systems or X-ray tubes for CT scanners. These component manufacturers are pivotal, often requiring deep expertise in materials science, electronics, and precision engineering. The quality and innovation at this initial stage directly influence the performance and capabilities of the final imaging devices. Strategic relationships with reliable, high-quality component providers are crucial for ensuring the supply chains integrity and enabling continuous technological advancement.

Midstream in the value chain are the original equipment manufacturers (OEMs) who design, assemble, and integrate these components into complete 3D medical imaging systems. This stage involves extensive research and development to incorporate cutting-edge imaging algorithms, AI-powered software for image processing and analysis, and user-friendly interfaces. Manufacturing facilities must adhere to stringent quality control standards and regulatory compliance to ensure product safety and efficacy. The downstream segment of the value chain focuses on the distribution and sales of these complex devices. This involves a mix of direct sales forces employed by major manufacturers, third-party distributors, and value-added resellers who often provide localized support, installation, and maintenance services. The distribution channels must navigate complex logistics due to the size, weight, and technological sensitivity of these devices, often requiring specialized transportation and handling.

The final stage involves the deployment and utilization of these devices by end-users, primarily hospitals, diagnostic centers, and research institutions. Here, the focus shifts to post-sales support, including installation, calibration, ongoing maintenance, and technical training for medical professionals. Direct distribution channels allow manufacturers to maintain greater control over brand representation, customer relationships, and direct feedback loops, fostering product improvement. Indirect channels, through distributors, offer broader market reach, particularly in geographically dispersed or emerging markets, leveraging local expertise and established networks. The efficiency and effectiveness of the entire value chain, from component innovation to after-sales service, are critical for competitive advantage and ensuring that advanced 3D medical imaging technologies are accessible and optimally utilized for patient care.

The primary consumers and beneficiaries of 3D medical imaging devices are diverse healthcare entities that require advanced diagnostic and interventional capabilities to deliver high-quality patient care. Hospitals, ranging from large university-affiliated medical centers to smaller community hospitals, represent the largest segment of end-users. These institutions require a comprehensive suite of imaging modalities to serve a broad patient base across various specialties, including emergency medicine, surgery, oncology, and cardiology. Their demand is driven by the need for accurate diagnosis, treatment planning, and monitoring, often dealing with complex cases that necessitate the superior visualization offered by 3D imaging. The scale of their operations often necessitates multiple imaging units and substantial investment in the latest technology.

Diagnostic imaging centers constitute another significant customer segment, specializing in providing advanced imaging services to patients referred by general practitioners and specialists. These centers focus on efficiency, patient throughput, and offering a wide range of state-of-the-art imaging options, often investing in the latest 3D CT, MRI, and ultrasound technologies to attract patients and referring physicians. Their business model heavily relies on providing accurate and timely diagnostic reports. Additionally, ambulatory surgical centers (ASCs) and specialized clinics, such as orthopedic, neurology, or cardiology clinics, increasingly adopt 3D imaging devices for pre-operative planning, intra-operative guidance, and post-operative assessment, particularly for minimally invasive procedures where precision is paramount.

Beyond direct patient care, academic and research institutions are crucial potential customers for 3D medical imaging devices. These organizations utilize these technologies for clinical trials, medical research, and training future healthcare professionals. Their demand is often for cutting-edge, high-resolution systems that can support advanced research protocols and contribute to the development of new diagnostic techniques and therapies. Government healthcare agencies and military hospitals also represent a segment of potential buyers, investing in these devices to ensure comprehensive healthcare services for their beneficiaries. The increasing complexity of medical conditions and the imperative for early, accurate diagnosis across all these segments underscore the continuous and growing demand for sophisticated 3D medical imaging solutions.

The 3D Medical Imaging Devices Market is characterized by a rapidly evolving technological landscape, driven by continuous innovation aimed at enhancing image quality, reducing scan times, improving patient safety, and expanding diagnostic capabilities. Core technologies include sophisticated multi-slice and multi-detector Computed Tomography (CT) systems that offer faster acquisition and higher spatial resolution, enabling detailed visualization of complex anatomical structures with reduced radiation doses through iterative reconstruction algorithms. Magnetic Resonance Imaging (MRI) systems leverage increasingly powerful magnetic fields (e.g., 3T, 7T, and ultra-high field systems) and advanced coil designs to provide unparalleled soft tissue contrast and functional information, including diffusion tensor imaging and functional MRI, crucial for neurology and oncology.

Ultrasound technology has undergone significant advancements, transitioning from conventional 2D to real-time 3D and 4D imaging (3D imaging in motion). These volumetric ultrasound systems provide dynamic views of organs and blood flow, particularly valuable in obstetrics, cardiology, and point-of-care applications, leveraging advanced transducer technology and beamforming techniques. Positron Emission Tomography (PET) is frequently combined with CT or MRI (PET/CT, PET/MRI) to offer hybrid imaging capabilities, fusing metabolic information with anatomical detail for comprehensive disease staging and treatment response assessment. This integration is facilitated by advanced detector materials, improved time-of-flight capabilities, and more efficient scintillators, enhancing image resolution and quantitative accuracy.

Furthermore, the technology landscape is being profoundly shaped by the integration of artificial intelligence (AI) and machine learning (ML). AI algorithms are employed for advanced image reconstruction, automated segmentation of organs and lesions, anomaly detection, and predictive analytics, significantly improving diagnostic accuracy and workflow efficiency. Cloud computing enables secure storage, sharing, and remote access to vast imaging datasets, facilitating collaborative diagnostics and supporting teleradiology services. Augmented Reality (AR) and Virtual Reality (VR) are also emerging as key technologies for surgical planning, intra-operative guidance, and medical education, offering immersive 3D visualization of patient-specific anatomy. These technological advancements collectively drive the market forward, pushing the boundaries of what is diagnostically possible and fostering more precise, personalized patient care.

The increasing global prevalence of chronic diseases, such as cardiovascular disorders and cancer, coupled with a rapidly aging population and the demand for early, precise diagnosis, is the primary driver. Additionally, continuous technological advancements, particularly in AI integration, significantly propel market expansion.

AI is transforming 3D medical imaging by enhancing image reconstruction, automating segmentation and quantification, improving diagnostic accuracy through computer-aided detection, and streamlining clinical workflows. It also contributes to predictive analytics and personalized medicine, leading to more efficient and precise patient care.

Applications in cardiology, oncology, neurology, and orthopedics benefit most significantly from 3D imaging. Its enhanced visualization is crucial for diagnosing complex pathologies, precise surgical planning, image-guided interventions, and comprehensive monitoring of disease progression in these specialties.

Key challenges include the high initial cost of acquiring and maintaining 3D medical imaging devices, stringent and complex regulatory approval processes, a shortage of skilled professionals to operate and interpret these systems, and ongoing concerns regarding data privacy and cybersecurity.

North America currently leads the global 3D medical imaging market, driven by its advanced healthcare infrastructure, substantial healthcare expenditures, high adoption rates of advanced medical technologies, and the strong presence of key market players engaged in continuous research and development.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.