ID : MRU_ 428367 | Date : Oct, 2025 | Pages : 246 | Region : Global | Publisher : MRU

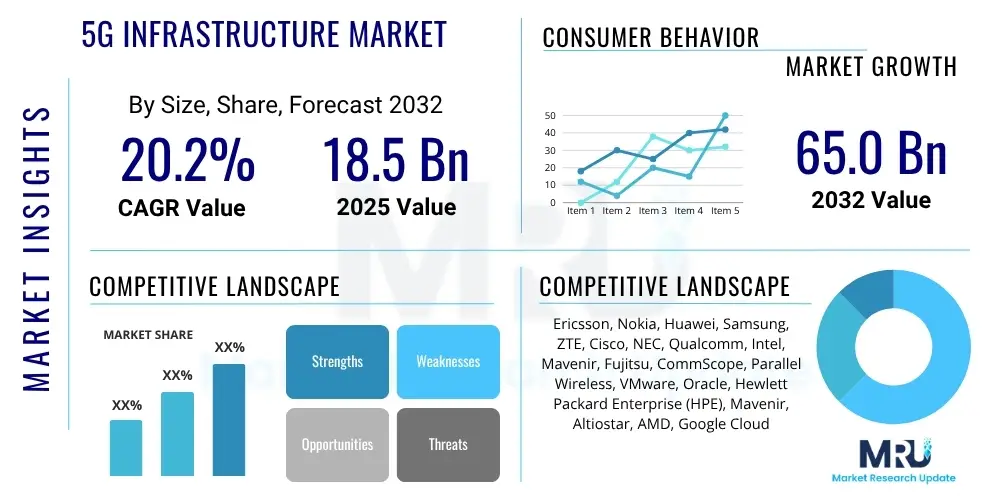

The 5G Infrastructure Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 20.2% between 2025 and 2032. The market is estimated at USD 18.5 Billion in 2025 and is projected to reach USD 65.0 Billion by the end of the forecast period in 2032.

The 5G infrastructure market encompasses the hardware, software, and services required to build and operate the fifth generation of cellular technology networks. This advanced technology promises significantly higher speeds, ultra-low latency, and massive connectivity compared to its predecessors, enabling a new era of digital transformation. Key components include Radio Access Network (RAN) equipment, core network elements, and transport network solutions that facilitate robust and efficient data flow.

Major applications of 5G infrastructure span across enhanced mobile broadband (eMBB), massive Internet of Things (mIoT), and ultra-reliable low-latency communications (URLLC). These applications support diverse sectors such as smart cities, autonomous vehicles, connected healthcare, industrial automation (Industry 4.0), and immersive entertainment. The inherent benefits of 5G infrastructure include improved network efficiency, reduced operational costs for service providers, and the enablement of innovative services that drive economic growth and societal advancements.

The primary driving factors behind the proliferation of 5G infrastructure include the exponential growth in mobile data traffic, the increasing adoption of IoT devices across industries, and the rising demand for high-speed, reliable connectivity in both urban and rural areas. Government initiatives worldwide to accelerate 5G deployment, coupled with significant investments from telecommunication operators and technology giants, further propel market expansion. The continuous evolution of wireless communication standards and the imperative for digital transformation across various enterprises also serve as critical catalysts for market growth.

The 5G Infrastructure market is currently experiencing robust growth, driven by aggressive network deployments globally and increasing demand for high-bandwidth, low-latency connectivity across diverse applications. Key business trends include the ongoing shift from Non-Standalone (NSA) to Standalone (SA) 5G architectures, which unlocks the full potential of 5G through advanced features like network slicing and ultra-reliable low-latency communication. There is also a significant surge in demand for private 5G networks, particularly within industrial and enterprise sectors, as organizations seek dedicated, secure, and customizable connectivity solutions for their specific operational needs. The Open RAN movement is gaining traction, fostering greater vendor diversity and innovation within the infrastructure ecosystem, which could potentially lower deployment costs and enhance network flexibility in the long run.

Regional trends indicate that Asia Pacific, particularly China, South Korea, and Japan, continues to lead in 5G deployments and subscriber penetration, fueled by government support and significant investments from major telecom operators. North America also demonstrates strong growth, characterized by rapid urban deployments and a growing emphasis on enterprise and industrial 5G applications. Europe is steadily progressing, with a focus on harmonizing regulatory frameworks and addressing spectrum availability challenges to accelerate infrastructure build-out. Emerging markets in Latin America, the Middle East, and Africa are showing nascent but promising growth, primarily driven by increasing smartphone adoption and the need for improved digital connectivity, often leapfrogging older technologies.

In terms of segment trends, the hardware component segment, including massive MIMO antennas, small cells, and base stations, remains a dominant contributor to market revenue due to the foundational requirements of 5G rollouts. However, the software and services segments are experiencing accelerated growth as network operators increasingly adopt virtualization technologies, cloud-native architectures, and managed services to optimize network operations and deploy new capabilities more flexibly. The enterprise end-use segment is poised for substantial expansion, driven by the increasing adoption of 5G for applications such as smart factories, logistics, and private networks, signaling a diversification beyond traditional consumer mobile broadband services. The deployment of millimeter-wave (mmWave) spectrum is also seeing increasing investment, especially in dense urban areas, for its capacity to deliver extremely high speeds, despite its shorter range.

Common user questions regarding the impact of AI on 5G infrastructure often revolve around how artificial intelligence can optimize network performance, enhance operational efficiency, manage the complexity of massive data flows, enable new services, and bolster network security. Users are keen to understand how AI will transition 5G networks towards greater autonomy, address the challenges of network slicing, and provide proactive insights for maintenance and resource allocation. There is significant expectation that AI will be a critical enabler for realizing the full potential of 5G, moving beyond basic connectivity to intelligent, self-optimizing, and highly adaptable networks. Concerns often include data privacy, the ethical implications of autonomous network decisions, and the skill gap required to implement and manage AI-driven 5G systems. The overarching theme is the pursuit of a more efficient, resilient, and intelligent network ecosystem through the symbiotic integration of AI with 5G infrastructure.

The 5G infrastructure market is propelled by a confluence of powerful drivers, including the insatiable demand for high-speed internet, the proliferation of IoT devices across industries, and the transformative potential of Industry 4.0 applications. Governments worldwide are actively promoting 5G deployment through supportive policies, spectrum auctions, and funding initiatives, recognizing its critical role in national digital economies. These factors create a robust environment for sustained investment and expansion in network build-out and technological innovation. Furthermore, the increasing adoption of cloud-based services and the necessity for real-time data processing for emerging applications like autonomous vehicles further underscore the importance of robust 5G infrastructure.

Despite significant growth, the market faces several restraints. High capital expenditure required for network deployment and upgrades presents a considerable barrier, especially for smaller operators. Spectrum availability and fragmentation across different regions pose regulatory and technical challenges, impacting network planning and efficiency. Security concerns related to data privacy and network vulnerabilities are also critical, demanding sophisticated solutions. Additionally, the complexity of deploying new infrastructure, particularly in dense urban environments and remote areas, alongside public apprehension regarding health concerns related to electromagnetic fields, can slow down rollout efforts.

Opportunities in the 5G infrastructure market are vast and evolving. The emergence of private 5G networks offers significant growth avenues, catering to specific enterprise needs in manufacturing, logistics, and healthcare, providing dedicated and secure connectivity. The development of network slicing capabilities opens up new revenue streams by enabling operators to offer customized network segments for different services with guaranteed Quality of Service (QoS). The integration of 5G with edge computing is another major opportunity, reducing latency and enabling real-time processing for bandwidth-intensive applications. Furthermore, the Open RAN movement holds the potential to diversify the vendor ecosystem, foster innovation, and reduce reliance on proprietary solutions, thereby driving competition and potentially lowering costs.

Impact forces on the 5G infrastructure market are multifaceted. Technological advancements, particularly in areas like massive MIMO, beamforming, and network virtualization, continuously reshape network capabilities and deployment strategies. Economic shifts, including global economic growth or downturns, directly influence investment levels by telecommunication companies and governments. Policy and regulatory frameworks, from spectrum allocation to national security guidelines, dictate the pace and nature of 5G expansion. The competitive landscape, characterized by intense rivalry among a few major equipment vendors and emerging players, drives innovation but also presents challenges related to market share and pricing. Societal acceptance and demand for new 5G-enabled services also play a crucial role in shaping market adoption and future growth trajectories.

The 5G infrastructure market is comprehensively segmented based on various technical and application-oriented factors, allowing for a detailed understanding of its diverse components and growth areas. This segmentation helps in analyzing market dynamics across different technologies, network architectures, and end-user applications, providing crucial insights into investment priorities and emerging opportunities. The market is primarily categorized by component, network architecture, spectrum type, and end-use application, each exhibiting unique growth trajectories and market characteristics driven by technological innovation and evolving consumer and enterprise demands.

The value chain for the 5G infrastructure market is complex and interconnected, starting from the foundational technology development and extending to the ultimate delivery of 5G services to end-users. At the upstream level, the chain involves research and development, design, and manufacturing of critical components such as semiconductors, chipsets, antennas, and specialized hardware. These are supplied by a relatively small number of specialized technology firms that possess deep expertise in advanced materials and radio frequency engineering. These component providers are essential for the quality and performance of the entire network, constantly innovating to meet the stringent requirements of 5G technology, including higher frequencies and massive connectivity. Their ability to deliver cutting-edge components directly influences the capabilities of downstream equipment vendors.

Further along the value chain, the midstream segment involves major network equipment vendors who integrate these components into complete 5G infrastructure solutions, including base stations, core network elements, and transport network systems. These vendors, such as Ericsson, Nokia, and Huawei, are responsible for designing, manufacturing, and assembling the entire network architecture. They also provide the necessary software for network management, orchestration, and virtualization. System integrators and deployment service providers then work closely with these vendors and operators to plan, install, and optimize the 5G networks. This phase is highly capital-intensive and requires significant technical expertise in network engineering and project management, ensuring seamless interoperability and adherence to global standards.

The downstream segment primarily consists of Communication Service Providers (CSPs) or Mobile Network Operators (MNOs) who acquire, deploy, and operate the 5G infrastructure to offer services to consumers and enterprises. They are the direct link to the end-users, responsible for marketing, billing, and customer support. The distribution channel for 5G infrastructure products and services is predominantly direct, with equipment vendors selling directly to large telecom operators or through long-term strategic partnerships. For enterprise and private 5G solutions, system integrators and value-added resellers (VARs) often play a crucial role, providing specialized deployment and managed services tailored to specific industry needs. Indirect channels might exist for smaller components or specialized software, but the core network infrastructure generally follows a direct sales model due to the complexity and scale of the projects.

The primary potential customers for 5G infrastructure are Communication Service Providers (CSPs), often referred to as Mobile Network Operators (MNOs), who are investing heavily in upgrading their existing networks to 5G to meet increasing consumer demand for faster and more reliable mobile broadband services. These operators aim to attract new subscribers, retain existing ones, and unlock new revenue streams by offering innovative 5G-enabled services such as fixed wireless access, enhanced mobile gaming, and virtual reality applications. Their extensive need for RAN equipment, core network upgrades, and transport solutions makes them the largest segment of buyers in the market. The competitive landscape among CSPs worldwide further fuels the rapid adoption and deployment of 5G infrastructure as they vie for market leadership and technological superiority.

Beyond traditional CSPs, the enterprise sector represents a rapidly expanding and significant customer segment for 5G infrastructure. Industries such as manufacturing, logistics, transportation, healthcare, and energy are increasingly seeking private 5G networks to enable mission-critical applications, improve operational efficiency, and enhance security. These enterprises leverage 5G for use cases like smart factories with automated guided vehicles (AGVs), real-time asset tracking, remote patient monitoring, and predictive maintenance. The demand for customized, dedicated, and secure connectivity solutions that 5G offers, often integrated with edge computing and AI, positions these enterprises as key drivers of future market growth, moving beyond public network deployments.

Additionally, governments and public sector organizations are emerging as significant buyers of 5G infrastructure, particularly for smart city initiatives, public safety, and critical national infrastructure. Smart city projects utilize 5G for intelligent traffic management, environmental monitoring, public surveillance, and connected streetlights, improving urban living and public services. Public safety agencies are adopting 5G for enhanced communication, real-time data sharing for emergency services, and drone operations. These entities are often interested in building robust, resilient, and secure networks that can support essential services and foster innovation within their jurisdictions. Their long-term investment cycles and focus on societal benefits ensure a stable demand for advanced 5G infrastructure solutions.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 18.5 Billion |

| Market Forecast in 2032 | USD 65.0 Billion |

| Growth Rate | 20.2% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Ericsson, Nokia, Huawei, Samsung, ZTE, Cisco, NEC, Qualcomm, Intel, Mavenir, Fujitsu, CommScope, Parallel Wireless, VMware, Oracle, Hewlett Packard Enterprise (HPE), Mavenir, Altiostar, AMD, Google Cloud |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The 5G infrastructure market is characterized by a dynamic and rapidly evolving technology landscape, foundational to achieving the ambitious goals of enhanced mobile broadband, ultra-reliable low-latency communications, and massive machine-type communications. Massive MIMO (Multiple-Input, Multiple-Output) technology is a cornerstone, significantly boosting spectral efficiency and capacity by utilizing a large number of antennas at the base station to serve multiple users simultaneously. This allows for improved coverage and higher data rates, particularly in dense urban areas. Complementary to Massive MIMO is Beamforming, which precisely directs radio signals towards individual user devices, minimizing interference and maximizing signal strength. These advanced antenna technologies are crucial for effectively utilizing higher frequency bands, including millimeter-wave (mmWave).

Network Slicing is another pivotal technology that enables operators to create multiple virtual, independent networks on a shared physical infrastructure, each tailored to specific service requirements such as low latency for autonomous vehicles or high bandwidth for video streaming. This capability is facilitated by Software-Defined Networking (SDN) and Network Functions Virtualization (NFV), which decouple network control from forwarding planes and virtualize network functions, respectively. SDN and NFV provide the agility and flexibility needed to manage the complex and diverse demands of 5G, allowing for rapid deployment of new services and efficient resource allocation. These virtualization technologies are transforming the operational models of telecom networks, shifting towards more software-centric and cloud-native architectures.

Edge Computing plays a critical role in the 5G ecosystem by bringing computing resources closer to the data source, significantly reducing latency and bandwidth usage at the core network. This distributed processing capability is vital for supporting real-time applications such as industrial automation, augmented reality (AR), and virtual reality (VR), which demand immediate responsiveness. Furthermore, the Open RAN (Open Radio Access Network) initiative is gaining considerable momentum, promoting open and disaggregated network architectures. Open RAN aims to foster innovation, increase vendor diversity, and reduce dependence on traditional monolithic equipment providers by standardizing interfaces between different network components, paving the way for more flexible and cost-effective 5G deployments.

5G infrastructure refers to the hardware, software, and services that build and operate the fifth generation of wireless communication networks, designed for higher speeds, lower latency, and greater connectivity.

The main components include the Radio Access Network (RAN), core network, and transport network (fronthaul, midhaul, backhaul) elements, alongside specialized software and services.

5G infrastructure offers significantly higher bandwidth, ultra-low latency, and the ability to connect a massive number of devices, supporting advanced applications like IoT, autonomous vehicles, and real-time AR/VR, which 4G cannot adequately handle.

Key industries benefiting from 5G infrastructure include telecommunications, manufacturing (Industry 4.0), transportation and logistics, healthcare, smart cities, and enhanced mobile broadband for consumers.

Major challenges include high capital expenditure, spectrum availability and fragmentation, security concerns, complex regulatory environments, and the need for extensive physical infrastructure build-out, especially for millimeter-wave deployments.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.