ID : MRU_ 429664 | Date : Nov, 2025 | Pages : 241 | Region : Global | Publisher : MRU

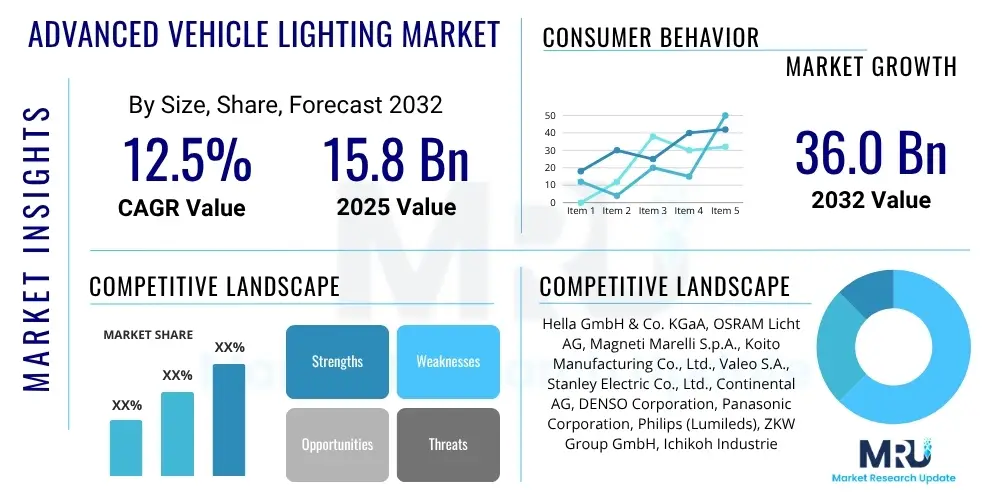

The Advanced Vehicle Lighting Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2025 and 2032. The market is estimated at USD 15.8 Billion in 2025 and is projected to reach USD 36.0 Billion by the end of the forecast period in 2032.

The Advanced Vehicle Lighting Market represents a significant evolution from traditional automotive illumination systems, encompassing sophisticated technologies designed to enhance safety, aesthetics, and driver comfort. These systems move beyond simple on/off functionality to offer dynamic, adaptive, and intelligent lighting solutions that respond to environmental conditions, vehicle speed, steering angle, and even other road users. This shift is driven by a confluence of stringent regulatory requirements for road safety, escalating consumer demand for premium features, and rapid advancements in light-emitting technologies and sensor integration. The market's scope includes a wide array of products, from high-performance LEDs and OLEDs to cutting-edge laser lighting and adaptive driving beam systems, all aimed at optimizing visibility and communication on the road.

Products within this market segment, such as Adaptive Driving Beam (ADB), Organic Light Emitting Diodes (OLED), Laser Headlights, and advanced LED Matrix systems, are distinguished by their ability to dynamically adjust light distribution. ADB systems, for instance, can selectively dim parts of the high beam to avoid dazzling oncoming drivers while maintaining maximum illumination of the road ahead. OLED technology offers unique design freedom with thin, uniform light panels, opening new possibilities for vehicle aesthetics and signaling. Laser lighting provides exceptional illumination range and efficiency, particularly beneficial for high-speed driving. These technologies not only improve night visibility but also contribute to vehicle personalization and energy efficiency, supporting the broader trend towards sustainable automotive solutions.

Major applications of advanced vehicle lighting extend across passenger vehicles, commercial vehicles, and increasingly, autonomous vehicles, where lighting plays a crucial role in sensor integration and vehicle-to-everything (V2X) communication. The benefits are multifaceted, including significantly enhanced road safety through improved visibility and reduced glare, distinctive vehicle aesthetics that contribute to brand identity, superior energy efficiency compared to conventional bulbs, and heightened driver comfort by reducing eye strain. Key driving factors propelling this market include global safety mandates, the rising production of premium and luxury vehicles, ongoing innovation in solid-state lighting, and the imperative to integrate lighting with advanced driver assistance systems (ADAS) for semi-autonomous and fully autonomous driving capabilities, making lighting an active safety component rather than merely a passive one.

The Advanced Vehicle Lighting Market is undergoing transformative growth, characterized by rapid technological adoption and increasing integration with broader automotive systems. Industry trends indicate a strong move towards intelligent, connected, and highly efficient lighting solutions, which are becoming pivotal for vehicle safety, design, and branding. The market is not merely about illumination but about sophisticated communication and perception enhancement, driven by advancements in LED, OLED, and laser technologies, alongside the integration of artificial intelligence and advanced sensors. This evolution is fostering a highly competitive landscape where innovation, cost-effectiveness, and compliance with evolving global standards are paramount for market players. Strategic partnerships between lighting manufacturers, component suppliers, and automotive OEMs are becoming more common to accelerate research and development and bring advanced systems to market more efficiently, ensuring seamless integration into next-generation vehicle architectures.

Regional trends significantly influence the market's trajectory, with Asia Pacific emerging as the largest and fastest-growing region, primarily fueled by robust automotive production, increasing disposable incomes, and the growing demand for advanced vehicle features in countries like China, India, Japan, and South Korea. Europe stands as a hub for innovation and early adoption of premium lighting technologies, driven by stringent regulatory frameworks for vehicle safety and a strong preference for high-end automotive features. North America is experiencing substantial growth propelled by the increasing penetration of ADAS and autonomous vehicle technologies, where advanced lighting plays a critical role in sensor fusion and environmental perception. These regional dynamics highlight diverse market priorities, from mass-market adoption in emerging economies to premium feature integration in mature markets, necessitating tailored product strategies.

Segment trends underscore the dominance of LED technology, which continues to evolve with innovations like matrix LED and Digital Light Processing (DLP) headlamps offering unparalleled control and versatility. The demand for smart lighting solutions, including adaptive high beams and intelligent ambient interior lighting, is experiencing significant growth, reflecting consumer desire for personalized and dynamic driving experiences. The premium segment is a key driver for advanced lighting, with luxury vehicles often debuting new technologies before they filter down to mass-market segments. Furthermore, the burgeoning electric vehicle (EV) market is creating new opportunities for energy-efficient lighting solutions, while autonomous vehicles are driving the need for lighting systems that can communicate with other vehicles and infrastructure. These segmentation shifts indicate a market moving towards more integrated, intelligent, and value-added lighting functionalities across all vehicle categories.

Common user questions regarding the impact of AI on Advanced Vehicle Lighting Market reveal a strong interest in how these technologies contribute to enhanced safety, improved driving experience, and the overall intelligence of vehicles. Users are particularly keen on understanding how AI enables more precise and predictive lighting functionalities, moving beyond simple reactive adjustments to anticipatory illumination. Queries often revolve around the practical benefits for drivers, such as reducing accident risks in adverse conditions, and the potential for greater personalization in interior and exterior lighting schemes. There is also significant curiosity about the integration of AI-driven lighting with autonomous driving systems, exploring how these systems perceive and respond to their environment to augment sensor capabilities and communicate intentions to other road users.

Furthermore, users frequently inquire about the technical implications and challenges of integrating AI into vehicle lighting. This includes questions about the computational power required, the reliability and robustness of AI algorithms in diverse real-world scenarios, and the associated cost increases. Concerns are also raised regarding the ethical considerations and regulatory hurdles for advanced AI-powered lighting features, especially those that dynamically interact with human drivers and pedestrians. The overarching theme is a desire for clarity on how AI can deliver tangible value, overcome current limitations of traditional lighting, and fit into the broader ecosystem of smart, connected, and autonomous vehicles without introducing undue complexity or cost.

The collective user sentiment points to high expectations for AI to revolutionize vehicle lighting, transforming it from a static safety feature into an active, intelligent, and integral part of the driving experience. Users expect AI to provide solutions for complex lighting challenges, such as glare management, precise object detection, and dynamic light patterns that adapt not only to external conditions but also to driver and passenger preferences. The focus is on intelligent systems that can learn, predict, and adapt, creating a safer, more intuitive, and highly personalized environment both inside and outside the vehicle, ultimately shaping the future of automotive illumination and its role in advanced mobility solutions.

The Advanced Vehicle Lighting Market is primarily driven by an confluence of stringent global safety regulations, which increasingly mandate advanced illumination features to improve road safety and reduce accident rates. Governments and regulatory bodies worldwide are pushing for technologies like Adaptive Driving Beam (ADB) and LED matrix headlamps, recognizing their potential to enhance visibility without causing glare to other drivers. This regulatory impetus is further complemented by the escalating consumer demand for luxury and comfort features in modern vehicles, where advanced lighting systems are perceived as a key differentiator, offering not only superior functionality but also contributing significantly to the vehicle's aesthetic appeal and premium feel. Moreover, the advent of autonomous vehicles is acting as a powerful catalyst, as sophisticated lighting becomes essential for sensor integration, environmental perception, and crucial vehicle-to-human (V2H) communication, allowing autonomous cars to signal their intentions to pedestrians and other road users effectively.

Despite the robust growth drivers, the market faces significant restraints that could impede its expansion. The high initial cost associated with research, development, and manufacturing of advanced lighting systems, such as laser headlights and complex LED matrix modules, remains a substantial barrier to widespread adoption, particularly in budget and mid-range vehicle segments. The inherent complexity of integrating these sophisticated lighting systems with other vehicle electronics, including ADAS and infotainment systems, presents considerable engineering challenges and demands specialized expertise. Furthermore, regulatory hurdles, particularly regarding the approval and standardization of cutting-edge technologies like fully active laser lighting or dynamic projection features, vary significantly across different regions, creating compliance complexities and slowing market entry for some innovations. These factors necessitate substantial investments and meticulous planning from manufacturers to overcome integration difficulties and navigate diverse regulatory landscapes effectively.

Opportunities for growth in the Advanced Vehicle Lighting Market are abundant, particularly in emerging automotive markets where vehicle penetration is increasing, and consumers are increasingly seeking advanced safety and comfort features. The trend towards customization and personalization of vehicle lighting, both interior and exterior, presents a lucrative avenue for manufacturers to offer tailored solutions that cater to individual preferences and brand identities. The seamless integration of advanced lighting with Vehicle-to-Everything (V2X) communication systems offers transformative potential for predictive lighting, where information from road infrastructure and other vehicles can inform dynamic light adjustments, anticipating road conditions and hazards. Continuous software updates and over-the-air (OTA) capabilities also open doors for feature upgrades and improvements post-purchase, enhancing vehicle longevity and value. The primary impact forces shaping this market include relentless technological innovation, fierce competition among key players, a constantly evolving regulatory environment, and shifting consumer preferences towards intelligent and connected vehicle experiences.

The Advanced Vehicle Lighting Market is comprehensively segmented to provide a detailed understanding of its diverse components and the dynamics influencing various sub-sectors. This segmentation allows for a granular analysis of market trends, identifying key areas of growth, technological shifts, and consumer preferences. The market is primarily categorized based on critical attributes such as the underlying technology employed, the specific type of vehicle in which these systems are installed, the distinct application areas within the vehicle, and the sales channel through which these products reach the end-user. Each segment reveals unique characteristics in terms of adoption rates, competitive landscapes, and technological maturity, contributing to the overall market complexity and strategic considerations for industry participants.

Understanding these segments is crucial for stakeholders to develop targeted strategies, from product innovation and manufacturing to marketing and distribution. For instance, the demand drivers and technological requirements for headlamps differ significantly from those for interior ambient lighting. Similarly, the uptake of advanced lighting in passenger vehicles will have different dynamics compared to commercial vehicles, influenced by factors like cost sensitivity, fleet management priorities, and regulatory compliance. The sales channel segmentation further differentiates between OEM installations, which are driven by vehicle production cycles and manufacturer specifications, and the aftermarket, which is influenced by consumer upgrades, repairs, and customization trends, providing a holistic view of the market's reach and penetration.

The value chain for the Advanced Vehicle Lighting Market is a complex and interconnected ecosystem, beginning with the upstream segment that forms the foundational components. This segment primarily consists of raw material suppliers, providing essential materials such as specialized plastics, optical-grade glass, sophisticated semiconductors, and various metals crucial for light sources and housing. Following this, component manufacturers play a pivotal role, specializing in producing highly intricate elements like LED chips, laser diodes, OLED panels, electronic control units (ECUs), sensors, and optical lenses. These suppliers are critical for innovation and quality, as the performance and longevity of advanced lighting systems heavily depend on the quality and precision of these base components, often requiring deep technological expertise and high capital investment in manufacturing processes.

Moving downstream in the value chain, the components converge at Tier 1 suppliers, which are typically large, specialized automotive lighting companies. These Tier 1 suppliers are responsible for the complex assembly of individual components into complete lighting modules or systems, such as entire headlamp units, rear lamp clusters, or interior lighting arrays. This stage involves significant research and development to integrate various technologies, ensure precise optical engineering, and comply with stringent automotive standards for safety, durability, and electromagnetic compatibility. Once assembled, these complete advanced lighting modules are then supplied directly to Original Equipment Manufacturers (OEMs), the automotive vehicle manufacturers, who integrate these sophisticated systems into their vehicle assembly lines. This direct collaboration between Tier 1 suppliers and OEMs is crucial for design, engineering, and seamless integration, often involving co-development projects to meet specific vehicle model requirements and aesthetic visions.

The distribution channel segment subsequently handles the delivery of the final product to the end-user. For new vehicles, this is primarily a direct channel from the OEM through authorized dealerships to the consumer. However, a significant portion of the market operates through indirect channels, particularly in the aftermarket segment. This involves a network of independent retailers, specialized automotive parts distributors, service centers, and online platforms that supply replacement parts, upgrade kits, and customization options for advanced vehicle lighting systems. This two-tiered distribution approach ensures broad market reach, catering to both the initial vehicle purchase and subsequent ownership needs. The entire value chain is characterized by a high degree of specialization, requiring extensive collaboration and robust logistics to manage the intricate supply and demand of technologically advanced automotive lighting solutions.

The primary customers for the Advanced Vehicle Lighting Market are automotive Original Equipment Manufacturers (OEMs). These include major global car manufacturers, luxury vehicle brands, and emerging electric vehicle (EV) startups. OEMs are the largest buyers, integrating advanced lighting systems directly into their vehicle designs and production lines. Their demand is driven by the need to differentiate vehicles through cutting-edge technology, enhance safety ratings, meet evolving regulatory standards for illumination, and provide distinctive brand aesthetics. OEMs seek robust, reliable, and innovative lighting solutions that can be seamlessly integrated with advanced driver-assistance systems (ADAS) and vehicle architectures, often requiring custom designs and long-term supply agreements with Tier 1 lighting suppliers. The emphasis for OEMs is on mass production capabilities, cost-efficiency at scale, and adherence to strict quality and performance specifications.

Another significant segment of potential customers comprises the aftermarket parts distributors, retailers, and independent repair shops. These entities cater to vehicle owners who seek to replace damaged lighting components, upgrade their existing vehicle's lighting systems, or customize their vehicles with advanced features that were not originally installed. This customer base is driven by factors such as vehicle aging, post-warranty repairs, a desire for enhanced safety features on older models, or personal aesthetic preferences. The aftermarket offers a diverse range of products, from direct OEM replacements to performance-enhancing upgrades and stylistic modifications, providing opportunities for both established brands and niche players to address specific consumer needs beyond the initial vehicle purchase.

Beyond traditional OEMs and the aftermarket, the Advanced Vehicle Lighting Market also serves specialized vehicle manufacturers and fleet operators. This includes producers of commercial vehicles such as trucks and buses, construction equipment, agricultural machinery, and emergency vehicles, all of which have unique lighting requirements for operational safety, durability, and compliance with industry-specific regulations. Fleet operators, managing large numbers of vehicles, are also key buyers, seeking durable, energy-efficient, and easily maintainable lighting solutions to minimize downtime and operational costs. The increasing demand for autonomous shuttles and delivery vehicles further expands the customer base, as these platforms require sophisticated, AI-integrated lighting for navigation, sensor performance, and effective communication with their surroundings, highlighting the broad and evolving spectrum of end-users for advanced vehicle lighting solutions.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 15.8 Billion |

| Market Forecast in 2032 | USD 36.0 Billion |

| Growth Rate | 12.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Hella GmbH & Co. KGaA, OSRAM Licht AG, Magneti Marelli S.p.A., Koito Manufacturing Co., Ltd., Valeo S.A., Stanley Electric Co., Ltd., Continental AG, DENSO Corporation, Panasonic Corporation, Philips (Lumileds), ZKW Group GmbH, Ichikoh Industries, Ltd., Samlip Industrial Co., Ltd., Gentex Corporation, Fiem Industries Ltd., SL Corporation, Varroc Lighting Systems, Grupo Antolin, Lear Corporation, Flex-N-Gate Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Advanced Vehicle Lighting Market is defined by a dynamic and continuously evolving technology landscape, with Light Emitting Diode (LED) technology at its core. LED matrix systems represent a significant advancement, allowing individual LEDs to be controlled independently, enabling highly precise light distribution. This capability facilitates glare-free high beams, dynamic turning lights, and projection of symbols or warnings onto the road. Organic Light Emitting Diodes (OLEDs) are another key technology, valued for their ultra-thin, flexible, and homogeneously illuminating surfaces, which offer unprecedented design freedom for rear lamps and interior ambient lighting, contributing significantly to vehicle aesthetics and signaling functions. These solid-state lighting solutions are not only energy-efficient but also offer enhanced durability and faster response times compared to conventional lighting.

Emerging at the high end of the spectrum is Laser Lighting, which delivers an illumination range far exceeding that of LEDs, providing exceptional visibility for high-speed driving and long-distance travel. Although currently limited to premium and luxury vehicles due to its complexity and cost, laser technology holds immense potential for future applications. Digital Light Processing (DLP) technology, adapted from projector systems, is gaining traction, allowing for millions of tiny mirrors to create ultra-precise light patterns. This enables highly sophisticated adaptive driving beams, sophisticated symbol projection for communication with pedestrians and drivers, and even personalized welcome scenarios, transforming the headlight into a versatile communication and safety tool.

Beyond the light sources themselves, the integration of intelligent sensors and artificial intelligence (AI) is transforming vehicle lighting into an active safety system. Advanced camera systems, radar, lidar, and GPS data feed into AI algorithms that predict road conditions, detect obstacles, and dynamically adjust light patterns in real-time. This includes predictive lighting, which anticipates curves or upcoming road features, and intelligent glare management, which selectively dims parts of the beam for other road users. Furthermore, connectivity features like Vehicle-to-Everything (V2X) communication enable lighting systems to exchange information with infrastructure and other vehicles, facilitating cooperative driving and enhancing overall road safety. Software-defined lighting, allowing over-the-air updates and personalized light profiles, signifies the convergence of lighting with the broader trend of software-centric vehicle architectures.

Advanced vehicle lighting systems significantly enhance road safety by improving visibility for drivers and reducing glare for oncoming traffic. They offer superior illumination precision, adapt dynamically to driving conditions, and contribute to unique vehicle aesthetics, enhancing brand identity. These systems also boast greater energy efficiency, reducing the load on the vehicle's electrical system and supporting fuel economy or extended range in electric vehicles. Their adaptive nature leads to reduced driver fatigue, improving overall driving comfort and safety.

Autonomous vehicles rely heavily on advanced lighting for several critical functions beyond simple illumination. These systems integrate with vehicle sensors (cameras, lidar, radar) to augment perception, illuminating specific areas of interest for improved object detection and classification in low-light conditions. Crucially, advanced lighting also enables effective vehicle-to-human (V2H) communication, allowing autonomous vehicles to signal their intentions, such as braking, turning, or recognizing pedestrians, through dynamic light patterns, thereby improving safety and predictability in shared road environments.

Artificial Intelligence (AI) transforms next-generation automotive lighting by enabling predictive, highly adaptive, and personalized illumination. AI algorithms analyze real-time data from various vehicle sensors and external sources (e.g., GPS, traffic data) to anticipate road conditions, identify hazards, and dynamically adjust light beams before the driver even perceives the need. This includes intelligent glare management, adaptive high beams that avoid blinding other drivers, and personalized interior ambient lighting. AI also optimizes energy consumption and facilitates seamless integration with ADAS and autonomous driving systems, making lighting an active, intelligent safety component.

Key regulatory trends significantly shape the advanced vehicle lighting market, primarily focusing on enhancing road safety and standardizing new technologies. Regulations in regions like Europe and North America increasingly mandate features such as Daytime Running Lights (DRL) and push for the adoption of glare-free high beam technologies like Adaptive Driving Beam (ADB). There is a continuous effort to update existing lighting standards to accommodate newer technologies like LED matrix and laser lighting, ensuring their safe and effective deployment while addressing concerns related to light pollution and energy consumption. Harmonization of global standards remains a challenge but is a key focus for market expansion.

The Asia Pacific (APAC) region currently leads in the adoption and growth of advanced vehicle lighting, primarily driven by high automotive production volumes in countries like China, Japan, and South Korea, coupled with rising consumer demand for premium features. Europe, particularly countries like Germany, is also a significant leader, known for its stringent safety regulations and early adoption of innovative lighting technologies. North America shows strong growth due to increasing integration of advanced lighting with ADAS and autonomous vehicle systems, reflecting a global trend towards intelligent and connected mobility solutions.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.