ID : MRU_ 429058 | Date : Oct, 2025 | Pages : 253 | Region : Global | Publisher : MRU

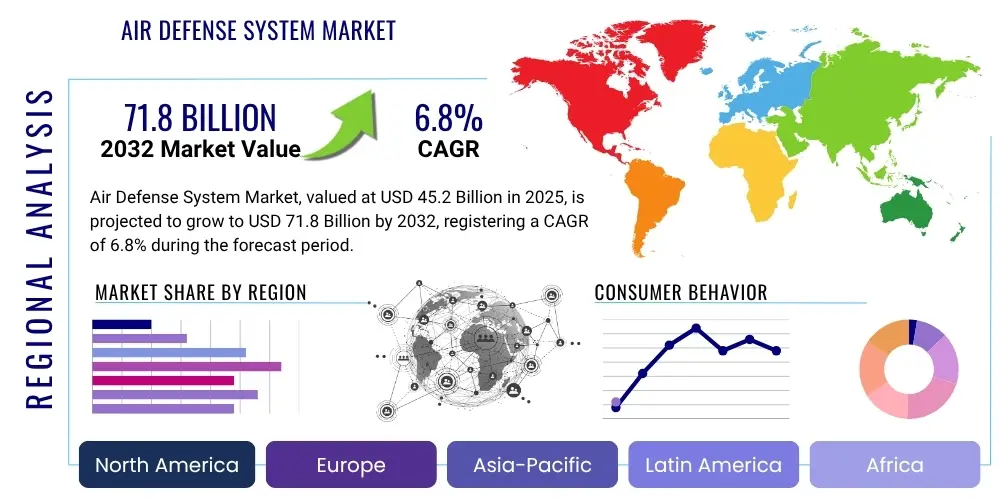

The Air Defense System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2032. The market is estimated at USD 45.2 Billion in 2025 and is projected to reach USD 71.8 Billion by the end of the forecast period in 2032.

The global Air Defense System market is undergoing significant transformation, driven by an evolving threat landscape and persistent geopolitical instabilities worldwide. Air defense systems encompass a sophisticated array of technologies designed to detect, track, intercept, and neutralize various airborne threats, including ballistic missiles, cruise missiles, hostile aircraft, and an increasingly prevalent array of unmanned aerial vehicles (UAVs) or drones. These systems are critical for national security, safeguarding critical infrastructure, military assets, and civilian populations.

The primary applications of air defense systems are predominantly military, serving the ground forces, naval fleets, and air forces of nations globally. They provide layered protection, ranging from short-range point defense to wide-area missile defense capabilities. Key benefits include deterrence against potential adversaries, strategic protection of sovereign airspace, and the operational advantage in conflict zones. The market's growth is largely propelled by escalating defense budgets, the modernization of existing military capabilities, the proliferation of advanced offensive aerial weaponry, and a heightened focus on counter-UAV technologies.

The continuous development of sophisticated threats necessitates constant innovation in defense technologies, leading to significant investments in research and development. This includes advancements in radar systems, command and control architectures, interceptor missiles, and electronic warfare capabilities. The market is characterized by long development cycles, high capital expenditure, and strong government involvement, reflecting its strategic importance in national defense strategies.

The Air Defense System market is witnessing robust growth, fueled by rising global tensions and the modernization of defense capabilities across various nations. Key business trends include the increasing integration of artificial intelligence and machine learning for enhanced threat assessment and autonomous operations, a pivot towards directed energy weapons for cost-effective and precise engagements, and the development of modular, scalable systems adaptable to diverse operational environments. Furthermore, there is a strong emphasis on networked air defense architectures that enable seamless communication and coordination between different defense assets, creating a more resilient and comprehensive protective shield against sophisticated aerial threats.

Regionally, the market dynamics are heavily influenced by geopolitical flashpoints and defense spending priorities. The Asia Pacific region is emerging as a significant growth engine, driven by escalating territorial disputes and military modernization programs by countries such as China, India, Japan, and South Korea. Europe is also seeing a resurgence in defense investments, prompted by regional conflicts and a renewed focus on collective security, leading to substantial upgrades in air and missile defense capabilities. Meanwhile, the Middle East continues to be a high-demand area due to persistent regional instabilities and the need for advanced threat interception technologies. North America maintains its position as a leading market, characterized by extensive research and development in next-generation defense solutions.

Segment-wise, the market is experiencing notable trends across various categories. The missile defense segment continues to dominate, with significant investments in anti-ballistic and anti-cruise missile systems. The counter-Unmanned Aerial System (C-UAS) segment is rapidly expanding, responding to the growing threat posed by drones in both military and civilian contexts. By component, advanced radar systems and sophisticated command and control centers are seeing substantial technological advancements and increased adoption. The trend towards integrated, multi-layered air defense systems is overarching, ensuring comprehensive protection against a broad spectrum of aerial threats, from low-flying drones to high-altitude hypersonic weapons, thereby shaping the future trajectory of the market.

Common user inquiries regarding the impact of Artificial Intelligence on the Air Defense System market predominantly revolve around questions of enhanced operational efficiency, decision-making speed, and autonomous capabilities. Users are keen to understand how AI can improve threat detection accuracy, shorten response times, and manage complex threat environments with multiple simultaneous engagements. There is also significant interest in AI's role in predictive maintenance, resource optimization, and the potential for AI-powered systems to operate with reduced human intervention, while simultaneously expressing concerns about the ethical implications, reliability, and the crucial need for human oversight in lethal decision processes.

The Air Defense System market is significantly shaped by a confluence of driving forces, restraining factors, and emerging opportunities, all operating under the influence of various impact forces. The primary drivers include intensifying geopolitical tensions across various regions, leading to increased defense spending and a strong imperative for national security. The proliferation of advanced aerial threats, such as hypersonic missiles, stealth aircraft, and sophisticated unmanned aerial vehicles (UAVs), necessitates continuous upgrades and modernization of existing air defense capabilities. Furthermore, ongoing technological advancements in radar systems, interceptor missiles, and command and control systems are creating demand for next-generation defense solutions, while the growing need for effective counter-UAS technologies specifically addresses modern asymmetric warfare challenges.

Conversely, several restraints hinder the market's growth trajectory. The inherently high research and development costs associated with developing cutting-edge air defense technologies often limit the number of nations capable of substantial investment. The complexity of integrating disparate systems from various manufacturers into a cohesive defense architecture presents significant challenges, both technical and logistical. Export controls and stringent regulatory frameworks also restrict the global dissemination of advanced defense technologies. Moreover, the long procurement cycles and substantial capital expenditures required for air defense systems can strain national budgets, especially in developing economies, thereby influencing purchasing decisions. Ethical concerns surrounding autonomous weapon systems also pose a potential restraint, prompting debates on the level of human involvement in lethal engagements.

Despite these challenges, substantial opportunities exist within the market. Emerging economies, particularly in Asia Pacific and the Middle East, are actively pursuing defense modernization programs, creating new avenues for market players. The development and integration of directed energy weapons, such as lasers and high-power microwaves, offer potential for more cost-effective and precise threat neutralization, representing a significant technological leap. The growing emphasis on cyber defense integration within air defense systems addresses vulnerabilities in networked architectures, enhancing overall resilience. Furthermore, the development of multi-layered, integrated air and missile defense systems that combine various short, medium, and long-range capabilities ensures comprehensive protection against a wide spectrum of aerial threats, offering robust solutions for national security needs and fostering international collaborations in defense technology sharing and joint development initiatives.

The Air Defense System market is comprehensively segmented across several key dimensions to provide a granular understanding of its structure and dynamics. These segments help in analyzing market trends, identifying growth opportunities, and understanding the specific requirements of various end-users. The primary segmentation categories include the type of air defense system, the components that constitute these systems, their operational range, the platforms on which they are deployed, and the end-user entities utilizing these crucial defense assets. Each segment reflects distinct technological characteristics, operational requirements, and market demand patterns, contributing to the overall market landscape.

This multi-faceted segmentation allows for a detailed assessment of market performance, highlighting the areas of most significant investment and innovation. For instance, the demand for missile defense systems differs considerably from that for counter-UAS solutions, driven by different threat perceptions and strategic priorities. Similarly, the technological sophistication and procurement processes for land-based systems vary from those for naval or airborne platforms. Analyzing these segments provides strategic insights for manufacturers, policymakers, and defense organizations to better allocate resources, develop targeted technologies, and formulate effective defense strategies in an increasingly complex global security environment.

The value chain for the Air Defense System market is a complex ecosystem, beginning with upstream activities involving numerous specialized suppliers and extending through intricate manufacturing and integration processes to downstream distribution and end-user engagement. Upstream activities primarily involve the research, development, and supply of raw materials and highly specialized components. This includes advanced semiconductors, specific metals and composites for missile bodies, complex electronic circuits for radar and C2 systems, and propulsion systems for interceptors. Key players in this stage are often specialized component manufacturers and technology providers who supply critical sub-systems to prime contractors, ensuring the integration of cutting-edge technologies into the final products.

Midstream activities are dominated by prime defense contractors who specialize in system integration, manufacturing, and assembly of the various components into a complete air defense system. This stage involves extensive engineering, testing, and quality control to ensure the systems meet stringent military specifications and operational requirements. Downstream activities involve the direct procurement by national defense ministries and various military branches. The distribution channel is predominantly direct, with defense contractors engaging in direct sales and long-term contracts with government entities. Indirect distribution might occur through international defense agreements or when prime contractors utilize smaller local partners for specific regional deployments or maintenance services. The entire chain is characterized by high capital intensity, long project lifecycles, and strict regulatory oversight.

Effective management of this value chain is critical for ensuring the timely delivery of advanced defense capabilities and maintaining national security. Strong collaborations between upstream component suppliers, midstream system integrators, and government end-users are essential. The direct nature of the distribution channel emphasizes the importance of robust relationships, trusted partnerships, and comprehensive after-sales support, including training, maintenance, and upgrades. These relationships are often built on long-term trust, technical expertise, and adherence to strict security and confidentiality protocols.

The primary potential customers and end-users of Air Defense Systems are sovereign nations, specifically their government defense ministries and various military branches. These entities are directly responsible for national security, border protection, and the safeguarding of critical national assets and populations against aerial threats. This includes national air forces, which require advanced systems for airspace control and interdiction; naval forces, which integrate air defense capabilities into warships for fleet protection; and land forces, which deploy ground-based systems to protect deployed troops, bases, and strategic locations.

Beyond traditional military applications, there is an expanding demand from other governmental agencies responsible for homeland security and critical infrastructure protection. This includes organizations tasked with securing airports, nuclear power plants, government buildings, and other high-value civilian targets from emerging aerial threats, particularly unmanned aerial vehicles (UAVs) or drones. The increasing sophistication and accessibility of drones have broadened the customer base to include entities that historically may not have required such specialized defense capabilities, driving growth in the counter-UAS segment of the market.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 45.2 Billion |

| Market Forecast in 2032 | USD 71.8 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Raytheon Technologies, Lockheed Martin, Northrop Grumman, BAE Systems, Saab AB, Rafael Advanced Defense Systems, Israel Aerospace Industries, Thales Group, MBDA, Rheinmetall AG, Leonardo S.p.A., Diehl Defence, Kongsberg Gruppen, L3Harris Technologies, Boeing, Hanwha Systems, Nexter Systems, General Dynamics, Mitsubishi Heavy Industries, Embraer S.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Air Defense System market is at the forefront of defense technology innovation, continuously integrating advanced solutions to counter evolving threats. Key technological developments include the widespread adoption of Phased Array Radars, which offer superior detection, tracking, and target classification capabilities due to their electronic beam steering and multi-functionality. Artificial Intelligence and Machine Learning algorithms are increasingly being embedded into command and control systems for rapid threat assessment, automated decision support, and optimized resource allocation, significantly reducing human response times and enhancing system effectiveness against complex attack scenarios. Directed Energy Weapons (DEW), such as high-energy lasers and high-power microwave systems, are emerging as a game-changer, promising cost-effective, precise, and virtually unlimited engagements against a variety of aerial targets, particularly drones and missiles, moving beyond traditional kinetic interceptors.

Another critical area of technological advancement is the development of advanced Counter-UAS (C-UAS) solutions, which leverage a combination of kinetic, electronic warfare, and cyber capabilities to detect, track, and neutralize small, low-observable unmanned aerial vehicles. These systems are crucial for protecting critical infrastructure and military assets from drone threats. Hypersonic missile defense remains a significant R&D focus, driving innovations in sensor technology, interceptor speeds, and engagement algorithms to counter these extremely fast and maneuverable threats. Furthermore, the integration of networked sensors and command architectures ensures seamless communication and data sharing across disparate defense assets, creating a robust, layered defense system. The future also holds promise for integrating quantum computing for enhanced data processing and cryptographic security, further solidifying the capabilities of air defense systems.

The emphasis is increasingly on creating integrated, multi-layered defense solutions that combine various technologies to provide comprehensive protection against a wide spectrum of threats. This includes combining long-range missile defense systems with short-range anti-aircraft guns, electronic warfare, and C-UAS capabilities. Miniaturization of components and modular design principles are also key trends, enabling easier deployment and adaptability of these systems to various platforms and operational environments. The continuous push for greater autonomy, enhanced precision, and reduced collateral damage drives the technological landscape, ensuring air defense systems remain effective against current and future aerial adversaries.

An Air Defense System is a comprehensive network of technologies designed to detect, track, intercept, and neutralize aerial threats such as missiles, aircraft, and drones. It is crucial for national security, protecting critical infrastructure, and safeguarding military assets and populations from various airborne attacks.

Key drivers include escalating global geopolitical tensions, the proliferation of advanced aerial threats (e.g., hypersonic missiles, sophisticated drones), increasing defense budgets worldwide, and continuous technological advancements in radar, command and control, and interceptor systems.

AI significantly impacts air defense by enhancing threat detection and classification, speeding up decision-making, enabling autonomous targeting (with human oversight), optimizing resource allocation, and improving predictive maintenance for higher operational readiness. It helps manage complex, multi-threat environments.

North America currently holds a significant market share due to high defense spending and R&D. The Asia Pacific region is projected to be the fastest-growing market, driven by military modernization and geopolitical disputes, while Europe is also seeing substantial investment in integrated air and missile defense.

Modern Air Defense Systems are designed to counter a wide spectrum of threats including ballistic missiles, cruise missiles, hostile fighter jets and bombers, various classes of unmanned aerial vehicles (UAVs/drones), and emerging threats like hypersonic weapons and swarm attacks. They provide layered defense against both conventional and asymmetric aerial challenges.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.