ID : MRU_ 429563 | Date : Nov, 2025 | Pages : 248 | Region : Global | Publisher : MRU

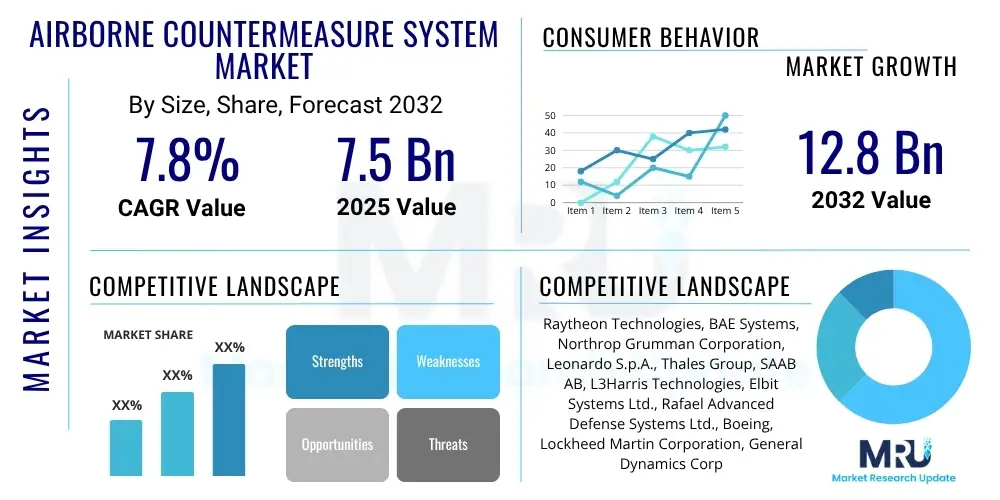

The Airborne Countermeasure System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2032. The market is estimated at USD 7.5 billion in 2025 and is projected to reach USD 12.8 billion by the end of the forecast period in 2032.

Airborne Countermeasure Systems (ACM) represent a critical segment within the global defense industry, primarily focused on enhancing the survivability of aerial platforms against a spectrum of missile threats, including radar-guided, infrared-guided, and advanced heat-seeking munitions. These sophisticated systems are integral to modern military operations, providing a proactive defense mechanism for various aircraft types, from fighter jets and transport aircraft to helicopters and increasingly, unmanned aerial vehicles (UAVs). The core function of ACM involves the detection of incoming threats, their accurate classification, and the subsequent deployment of appropriate counter-techniques to either divert or neutralize the threat.

The product description encompasses a range of technologies, including electronic warfare (EW) systems that jam or deceive enemy radars, expendable countermeasures such as flares to decoy infrared missiles, and chaff to confuse radar-guided missiles. More advanced systems integrate directed energy countermeasures and sophisticated towed decoys. Major applications span across military aviation for combat missions, intelligence, surveillance, and reconnaissance (ISR) operations, and critical transport and logistics roles. The inherent benefits of these systems are multifaceted, offering enhanced aircraft survivability, safeguarding valuable military assets, and crucially, protecting aircrew personnel, thereby enabling sustained operational readiness in contested airspaces.

Driving factors for the expansion of this market are predominantly linked to the intensifying geopolitical tensions worldwide, leading nations to prioritize defense modernization and strengthen their aerial defense capabilities. The continuous evolution of missile technology by potential adversaries necessitates the development and deployment of more advanced and adaptive countermeasure solutions. Furthermore, increasing military expenditures by major global powers and emerging economies, coupled with a focus on upgrading aging aircraft fleets with modern self-protection suites, significantly contributes to market growth. The imperative to maintain air superiority and ensure operational effectiveness in high-threat environments underscores the strategic importance and sustained demand for airborne countermeasure systems.

The Airborne Countermeasure System Market is experiencing robust expansion, propelled by a confluence of evolving geopolitical landscapes, continuous technological innovation, and heightened global defense spending. Business trends indicate a strong emphasis on research and development into next-generation systems, particularly those incorporating artificial intelligence (AI), machine learning (ML), and directed energy technologies. Manufacturers are focusing on developing more compact, integrated, and autonomous systems capable of addressing sophisticated multi-spectral threats. Strategic partnerships and collaborations between defense contractors and technology providers are becoming increasingly prevalent to pool expertise and accelerate innovation, especially in areas like sensor fusion and cognitive electronic warfare. The integration of open architecture designs is also gaining traction, allowing for easier upgrades and interoperability across platforms, which is crucial for modernizing existing fleets and future-proofing new procurements. This dynamic environment encourages robust competition and drives continuous product enhancement aimed at improving system effectiveness and reducing false alarm rates, thereby enhancing overall operational reliability.

Regionally, the market exhibits a concentrated demand from established defense powers in North America and Europe, alongside significant growth momentum from the Asia Pacific region. North America continues to dominate due to substantial defense budgets, extensive R&D investments, and the presence of numerous key market players. European nations are actively involved in modernizing their air forces, investing in new platforms and upgrading existing ones with advanced countermeasure capabilities, often through multinational programs. The Asia Pacific region is rapidly emerging as a critical growth hub, driven by escalating regional tensions, ambitious military modernization programs, particularly in countries like China, India, Japan, and South Korea, and an increasing procurement of advanced fighter jets and helicopters. Other regions such as the Middle East and Africa are also showing steady growth, influenced by regional conflicts and the need to bolster national security. Latin America, while smaller, is witnessing gradual adoption for specific security and surveillance applications.

Segmentation trends within the market highlight the dominance of electronic countermeasures (ECM) and expendable decoys (flares and chaff), which remain foundational components due to their proven effectiveness and cost-efficiency. However, the market is also seeing accelerated growth in directed energy countermeasures and advanced towed decoy systems, reflecting the industry's shift towards more active and precise threat neutralization. By platform, fixed-wing aircraft, especially advanced fighter jets and bombers, continue to be the primary beneficiaries of these systems, but there is a notable increase in the integration of countermeasures for rotary-wing aircraft and, significantly, for unmanned aerial vehicles (UAVs). The demand for miniaturized and autonomous countermeasure solutions for UAVs is a rapidly expanding niche. Furthermore, advancements in sensor technology, including multi-spectral sensors and passive detection systems, are driving innovation across all segments, leading to more comprehensive and integrated self-protection suites capable of detecting and defeating a wider array of threats.

Common user inquiries regarding AI's influence on the Airborne Countermeasure System Market frequently center on its potential to revolutionize threat detection, improve the autonomy of countermeasure deployment, and enhance system effectiveness. Users are keen to understand how AI algorithms can process vast amounts of sensor data more rapidly and accurately than traditional systems, thereby reducing response times. Concerns often arise regarding the reliability and ethical implications of AI-driven autonomous decision-making in critical combat scenarios, particularly concerning potential false positives or misinterpretations of threats. Expectations are high for AI to provide predictive capabilities, adaptive jamming techniques, and the ability to operate effectively in complex, dynamic electromagnetic environments, ultimately minimizing pilot workload and maximizing aircraft survivability. The integration of AI is seen as a pivotal step towards more intelligent, self-learning defense systems that can continuously adapt to evolving threats and seamlessly integrate with broader networked defense architectures, promising a significant leap in defensive capabilities.

The Airborne Countermeasure System Market is significantly shaped by a combination of key drivers, inherent restraints, and emerging opportunities, all influenced by dynamic impact forces. Major drivers include the increasing global geopolitical instability, which necessitates robust national defense capabilities and continuous modernization of air forces. The proliferation of advanced missile threats, including hypersonic and stealthy munitions, compels military establishments to invest in cutting-edge countermeasure technologies to ensure aircraft survivability. Furthermore, the growing demand for enhanced aircraft protection across various platforms, from manned combat aircraft to unmanned aerial vehicles (UAVs), fuels market expansion. Benefits such as safeguarding personnel and high-value assets further underscore the imperative for advanced countermeasure systems.

However, the market faces several significant restraints. The exceptionally high research and development (R&D) costs associated with developing sophisticated countermeasure technologies, which often involve extensive testing and validation, present a considerable barrier. Stringent regulatory approval processes and lengthy procurement cycles, particularly in the defense sector, can delay market entry and product deployment. Budgetary constraints in certain nations or shifts in defense spending priorities can also limit the adoption of new systems. Additionally, the complexity of integrating these systems into existing aircraft platforms, requiring extensive modifications and interoperability considerations, poses technical and financial challenges for defense departments.

Despite these restraints, numerous opportunities are poised to drive future growth. The integration of artificial intelligence (AI) and machine learning (ML) offers avenues for creating more autonomous, adaptive, and effective countermeasure systems capable of real-time threat analysis and response. The development of directed energy weapons, such as laser-based systems, holds significant promise for non-kinetic threat neutralization, offering reusable and precise defensive capabilities. Miniaturization of components and systems is creating new possibilities for deploying countermeasures on smaller platforms like advanced drones and tactical UAVs, broadening the market's application scope. Furthermore, international collaborations and joint ventures between defense contractors can mitigate R&D costs and accelerate technological advancements, fostering innovation and market penetration. These impact forces, including technological evolution, geopolitical shifts, and economic considerations, collectively dictate the trajectory and competitive landscape of the Airborne Countermeasure System Market, compelling continuous innovation and strategic adaptation.

The Airborne Countermeasure System Market is broadly segmented based on several key characteristics to provide a comprehensive understanding of its diverse landscape and specialized applications. These segmentation categories reflect the varying technologies, platforms, end-users, and operational needs within the global defense sector. Each segment represents distinct market dynamics, growth trajectories, and competitive environments, driven by specific technological advancements and strategic military requirements. Analyzing these segments helps in identifying key growth areas, understanding customer preferences, and strategizing product development and market entry. The market's complexity necessitates a granular view to accurately assess its potential and evolution across different dimensions, from the type of countermeasure deployed to the specific aerial platform it protects and the underlying technological principles.

The value chain for the Airborne Countermeasure System Market is intricate, spanning from raw material suppliers to the ultimate end-users, primarily national defense forces. It begins with the upstream segment, which includes fundamental research and development by academic institutions and specialized technology companies, alongside the manufacturing of core components such as advanced sensors (e.g., UV, IR, RF), high-performance processors, specialized power supply units, and active electronic components like Gallium Nitride (GaN) transistors crucial for electronic warfare systems. These suppliers provide the critical building blocks that form the basis of sophisticated countermeasure systems, requiring high precision, reliability, and often, MIL-SPEC (military specification) compliance. Innovations at this stage, particularly in material science and microelectronics, directly influence the performance and capabilities of the final products.

The midstream segment involves the original equipment manufacturers (OEMs) and system integrators who design, develop, and assemble these components into complete airborne countermeasure systems. This phase encompasses complex engineering, software development for threat detection and response algorithms, extensive testing, and certification processes to meet stringent aviation and military standards. These prime contractors often collaborate with a network of specialized subcontractors for various sub-systems, such as dispenser mechanisms for flares/chaff, laser emitters for directed energy systems, or antenna arrays for electronic jamming. Their role is to ensure seamless integration of diverse technologies into a cohesive and effective self-protection suite that can be retrofitted onto existing aircraft or incorporated into new platforms.

The downstream segment primarily involves the distribution and delivery of these systems to end-user military organizations. Distribution channels are predominantly direct, involving direct contracts between defense contractors and government defense ministries or air forces globally. Due to the strategic nature, high cost, and specialized requirements, commercial off-the-shelf (COTS) distribution is rare; instead, customized solutions and extensive after-sales support, including installation, training, maintenance, and upgrades, are provided. Indirect channels might exist through prime integrators who procure countermeasure systems from specialized vendors as part of a larger aircraft or defense platform package. The end of the value chain involves the operational deployment, ongoing maintenance, and eventual upgrades or decommissioning of these systems by the military, emphasizing long-term support and lifecycle management from the manufacturers.

The primary potential customers and end-users for Airborne Countermeasure Systems are sovereign national defense organizations and their various branches. This includes global air forces responsible for air superiority, air defense, and combat operations, as they operate the fighter jets, bombers, and attack helicopters that are most susceptible to missile threats. Naval aviation units also represent a significant customer base, requiring countermeasure systems for carrier-borne aircraft, maritime patrol aircraft, and naval helicopters operating in maritime environments where anti-ship and air-to-air threats are prevalent. These military entities prioritize advanced self-protection suites to safeguard personnel, protect high-value aerial assets, and ensure mission success in hostile airspace. The continuous modernization of military fleets across developed and emerging economies drives consistent demand for these systems, with procurement cycles often spanning several years and involving substantial investments to equip both new aircraft acquisitions and upgrade existing platforms for enhanced operational longevity and effectiveness.

Beyond traditional air forces and naval aviation, other specialized military and governmental agencies also constitute important end-users. Special operations forces (SOF) often operate unique aerial platforms, including specialized transport aircraft and helicopters, that require advanced defensive systems for high-risk infiltration, exfiltration, and reconnaissance missions. Border patrol agencies and certain governmental security forces operating surveillance aircraft or high-value VIP transport planes in high-threat regions may also invest in these systems, albeit typically less complex versions than those used on frontline combat aircraft. Furthermore, the growing proliferation of Unmanned Aerial Vehicles (UAVs) across military domains is creating a new and rapidly expanding customer segment. As UAVs take on more critical and autonomous roles, ensuring their survivability against advanced air defenses becomes paramount, driving the demand for miniaturized and highly integrated countermeasure solutions specifically designed for these platforms, transforming them from mere surveillance tools into robust, survivable assets capable of operating in contested environments. This diversification of platforms and mission profiles expands the traditional customer base and introduces new requirements for system adaptability and scalability.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 7.5 Billion |

| Market Forecast in 2032 | USD 12.8 Billion |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Raytheon Technologies, BAE Systems, Northrop Grumman Corporation, Leonardo S.p.A., Thales Group, SAAB AB, L3Harris Technologies, Elbit Systems Ltd., Rafael Advanced Defense Systems Ltd., Boeing, Lockheed Martin Corporation, General Dynamics Corporation, Dassault Aviation, Airbus S.A.S., Roketsan A.S., ASELSAN A.S., Terma A/S, Indra Sistemas, UTC Aerospace Systems (Collins Aerospace), Cobham plc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Airborne Countermeasure System Market is characterized by continuous innovation aimed at enhancing detection capabilities, improving response accuracy, and increasing the effectiveness against increasingly sophisticated threats. A core area of advancement is sensor fusion technology, which integrates data from multiple sensor types such as radar warning receivers (RWR), missile approach warning systems (MAWS) operating in UV/IR bands, and laser warning receivers (LWR). This multi-spectral approach allows for more accurate threat detection, classification, and tracking, significantly reducing false alarms and providing a comprehensive situational awareness to the aircrew. The development of advanced signal processing algorithms, often powered by machine learning (ML) and artificial intelligence (AI), is critical for interpreting this complex sensor data in real-time and identifying novel threat signatures, enabling systems to adapt to previously unknown or rapidly evolving threats with greater autonomy and precision.

Another pivotal technological trend is the evolution of electronic warfare (EW) capabilities, particularly in the realm of active electronically scanned array (AESA) jammers and cognitive EW. AESA technology provides superior beamforming capabilities, allowing for highly targeted and adaptive jamming techniques that can precisely counter modern radar-guided missiles while minimizing interference with friendly communications. Cognitive EW systems leverage AI to learn from the electromagnetic environment, predict enemy radar behavior, and autonomously generate optimal jamming strategies, providing a dynamic defense against complex and adaptive threats. Furthermore, significant advancements are being made in directed energy (DE) systems, primarily laser-based countermeasures. These systems offer the potential for a "magazine-less" and reusable defense against infrared-guided missiles, providing a more sustainable and potentially more effective solution compared to traditional expendable decoys, albeit with higher power requirements and integration challenges that are currently being addressed through ongoing research and miniaturization efforts.

Material science and component miniaturization also play a crucial role in shaping the technology landscape, particularly for applications on smaller platforms like unmanned aerial vehicles (UAVs) and rotary-wing aircraft where space and weight are critical constraints. The development of Gallium Nitride (GaN) based components for RF systems is enabling more powerful, efficient, and compact electronic warfare transmitters. Similarly, advancements in micro-electromechanical systems (MEMS) are leading to smaller, more robust sensors and control mechanisms. Software-defined countermeasures (SDC) are gaining traction, allowing for rapid reprogramming and upgrades of system functionalities without significant hardware modifications, providing agility in responding to new threats. The increasing focus on networked electronic warfare suites, where multiple platforms share threat data and coordinate countermeasure responses, represents a paradigm shift towards a more integrated and robust air defense posture, leveraging secure data links and advanced command and control systems to create a layered defense network against aerial threats.

An airborne countermeasure system is a self-protection suite integrated into aircraft, designed to detect, classify, and defeat incoming missile threats using various active and passive techniques to enhance aircraft survivability.

These systems protect aircraft by employing sensors to identify missile launches and then deploying countermeasures such as flares to decoy infrared missiles, chaff to confuse radar-guided missiles, or electronic jamming to disrupt missile guidance systems.

Key technologies include electronic countermeasures (ECM), expendable decoys (flares and chaff), missile approach warning systems (MAWS), radar warning receivers (RWR), and emerging directed energy countermeasures (DECM) like laser-based systems.

AI is significantly impacting countermeasures by enabling enhanced threat detection, autonomous decision-making for deployment, adaptive jamming techniques, and real-time optimization of defensive responses, leading to more intelligent and effective systems.

North America holds the largest market share due to high defense spending and R&D. Asia Pacific is the fastest-growing region, driven by extensive military modernization programs and increasing geopolitical tensions.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.