ID : MRU_ 430224 | Date : Nov, 2025 | Pages : 241 | Region : Global | Publisher : MRU

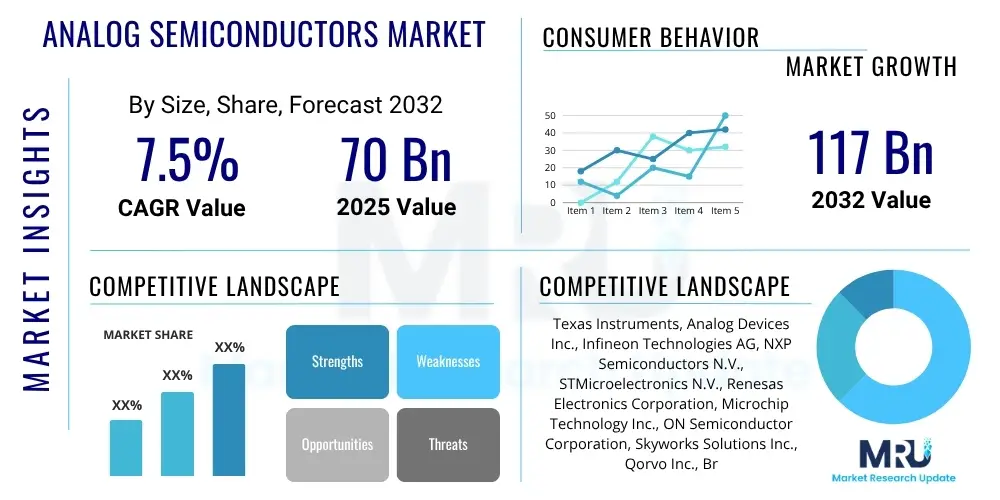

The Analog Semiconductors Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2025 and 2032. The market is estimated at USD 70 billion in 2025 and is projected to reach USD 117 billion by the end of the forecast period in 2032.

The Analog Semiconductors Market encompasses a vast array of electronic components designed for the intricate processing of continuous electrical signals, serving as the essential bridge between the physical world and the digital computational domain. These critical devices are adept at converting real-world phenomena such as temperature, pressure, light, sound, and motion into electrical signals, which are then conditioned, amplified, filtered, and managed before being converted into digital data for microprocessors. This fundamental function makes analog semiconductors indispensable across virtually all electronic systems, ensuring the seamless and accurate interaction of digital intelligence with the inherently analog physical environment. Products within this market segment range from sophisticated integrated circuits (ICs) like power management units and data converters to more fundamental components such as discrete transistors, diodes, and operational amplifiers, each playing a vital role in signal integrity and system functionality. The continued innovation in this sector is pivotal for advancing technological capabilities across industries, enabling more precise control, efficient operation, and robust performance of modern electronics.

Major applications for analog semiconductors span an incredibly diverse range of industries, reflecting their foundational importance in modern technology. In the automotive sector, they are indispensable for advanced driver-assistance systems (ADAS), electric vehicle (EV) powertrains, battery management systems, and in-car infotainment, requiring high reliability and precision under harsh conditions. Industrial automation relies heavily on analog components for accurate sensor interfaces, motor control, robotics, and power supplies, driving efficiency and safety in manufacturing. The ubiquitous consumer electronics segment integrates analog chips for power management in smartphones, laptops, and wearables, as well as for high-fidelity audio processing, display drivers, and various sensor functions, enhancing user experience and device longevity. Communication infrastructure, including 5G base stations, networking equipment, and data centers, depends on analog semiconductors for radio frequency (RF) front-ends, high-speed data transmission, and signal conditioning. Furthermore, healthcare applications utilize them in medical imaging, patient monitoring, and diagnostic equipment, where accuracy and low power consumption are paramount. The core benefits offered by these semiconductors include exceptional power efficiency, crucial for battery-operated devices and sustainable technology, high precision in signal processing for critical measurements, robust and reliable performance across varying environmental conditions, and the ability to integrate complex functionalities into smaller, more compact footprints. These attributes are continually driving the market forward, fueled by the relentless demand for smarter, more connected, and energy-efficient electronic systems across the globe.

The global analog semiconductors market is experiencing a period of robust growth, propelled by a convergence of significant business, regional, and segment-specific trends that are reshaping the technological landscape. Business trends are characterized by an intense focus on enhancing power efficiency, enabling higher levels of integration, and developing highly specialized analog solutions tailored for specific high-growth applications, such as automotive electrification, industrial automation, and edge computing for artificial intelligence. Leading manufacturers are channeling substantial investments into research and development to innovate smaller, more powerful, and increasingly energy-efficient analog chips. These advancements are critical for managing complex signal processing tasks, often leveraging cutting-edge packaging technologies and advanced materials to meet the escalating performance demands of next-generation electronic systems. The strategic importance of analog chips in managing real-world interfaces and power dynamics positions them as foundational elements for ongoing digital transformation initiatives across industries.

From a regional perspective, Asia Pacific continues to assert its dominance as the largest and fastest-growing market, primarily driven by its extensive electronics manufacturing base and the insatiable demand for connected devices in emerging economies like China, South Korea, and India. This region benefits from a thriving ecosystem of foundries, assembly, and test operations, coupled with a vast consumer market. Meanwhile, North America and Europe are witnessing significant expansion, particularly within high-value segments. Growth in these regions is fueled by advancements in automotive technologies, including electric vehicles and advanced driver-assistance systems, alongside sophisticated industrial automation and smart infrastructure projects. Innovation, stringent regulatory frameworks pushing for energy efficiency, and a strong focus on high-performance computing are key drivers in these developed markets. The Middle East and Africa, along with Latin America, present emerging opportunities, spurred by increasing digitalization, infrastructure development, and growing adoption of consumer and industrial electronics.

Segmentation trends highlight the critical role of specific analog product categories. Power management ICs (PMICs) continue to form the largest segment, remaining indispensable for optimizing energy consumption and extending battery life across an ever-expanding array of electronic devices, from consumer gadgets to industrial machinery. The demand for mixed-signal ICs is also surging, reflecting their vital function in facilitating seamless conversion and processing between analog and digital signals, a cornerstone requirement for modern embedded systems, advanced sensor fusion applications, and intricate communication interfaces. Furthermore, specialized analog components such as amplifiers, data converters, and sensors are experiencing tailored growth as industries demand higher precision, lower latency, and enhanced reliability. These segment-specific dynamics underscore the strategic importance of diversified product portfolios and targeted technological advancements to capitalize on market opportunities and address evolving customer needs effectively.

User inquiries regarding the profound impact of Artificial Intelligence (AI) on the analog semiconductors market frequently revolve around several critical questions: how AI workloads are generating novel demands for analog components, what specific types of analog chips are becoming indispensable for AI functionalities, and the inherent challenges or significant opportunities that this symbiotic integration presents. A prevailing theme in these discussions is the absolute necessity for highly efficient analog-to-digital conversion, the requirement for robust and intelligent power management solutions specifically designed for AI accelerators, and the expanding role of specialized analog circuits in enabling sophisticated edge AI processing. Users are particularly keen to understand how analog solutions can effectively address the often-contradictory requirements of stringent power efficiency and ultra-low latency, which are paramount for real-time AI applications, especially at the network edge. Furthermore, there is considerable interest in how analog components contribute to advanced sensor data processing and the complex sensor fusion necessary for highly accurate and reliable AI algorithms in diverse applications, from autonomous vehicles to industrial IoT.

The pervasive integration of AI across an ever-widening spectrum of applications is fundamentally reshaping and augmenting the demand landscape for analog semiconductors, necessitating the development of increasingly sophisticated signal conditioning, precision power delivery, and advanced interface solutions. Modern AI algorithms, particularly those designed for deployment at the edge in resource-constrained IoT devices, wearables, and autonomous systems, are critically dependent on the accurate and timely acquisition of real-world data, which is primarily gathered through an array of physical sensors. Consequently, advanced analog front-ends (AFEs) are becoming indispensable for converting these continuous physical signals into a format that is not only suitable but also optimized for subsequent digital processing by AI units. This demand drives innovation towards AFEs that offer ultra-high precision, minimal latency, and exceptional energy efficiency. Moreover, the escalating power consumption inherent in high-performance AI accelerators, whether in data centers or at the edge, mandates the development and deployment of highly advanced power management ICs (PMICs) to ensure stable, precise, and remarkably efficient power delivery, often complemented by sophisticated thermal management solutions to maintain operational integrity and longevity.

The ongoing paradigm shift towards embedding more intelligence directly onto devices and at the network edge is also creating unprecedented opportunities for pioneering advancements, such as neuromorphic analog computing. This emerging field explores the design of analog circuits that can mimic the brain's structure and function, potentially performing AI tasks with significantly lower power consumption and higher efficiency compared to conventional digital approaches. Analog semiconductors are thus not just supporting AI; they are becoming an integral part of its architectural evolution, enabling more localized, responsive, and sustainable AI deployments. This includes the development of specialized data converters optimized for AI inference, highly configurable analog filters for noise reduction in AI sensor inputs, and mixed-signal solutions that seamlessly integrate machine learning accelerators with real-world interfaces. The future trajectory of AI innovation will undoubtedly continue to be deeply intertwined with advancements in analog semiconductor technology, pushing the boundaries of what is possible in intelligent systems.

The Analog Semiconductors Market is profoundly influenced by a complex interplay of powerful drivers, persistent restraints, and significant opportunities, all operating within a dynamic landscape shaped by various external impact forces. A primary driver fueling the vigorous market expansion is the pervasive growth of the Internet of Things (IoT), which necessitates countless sensors, actuators, and connectivity solutions requiring analog interfaces for real-world interaction and data acquisition. The global rollout of 5G technology further accelerates demand, as it requires highly sophisticated radio frequency (RF) front-end modules and high-speed data converters crucial for high-bandwidth communication. Concurrently, the rapid electrification and increasing adoption of advanced driver-assistance systems (ADAS) and autonomous driving features in the automotive sector are creating an insatiable demand for robust, high-reliability analog components. Furthermore, the relentless push towards greater automation in industrial processes, coupled with the continuous evolution of consumer electronics towards smarter, more connected, and power-efficient devices, consistently boosts the need for innovative analog solutions, ranging from power management to audio processing and display drivers.

Despite these substantial tailwinds, the analog semiconductors market faces several notable restraints that can impede its growth trajectory. The most significant challenge often lies in the substantial research and development (R&D) costs associated with designing advanced analog chips, which demand extensive expertise and long design cycles, potentially deterring smaller market entrants or limiting innovation for some players. The inherent complexity of analog design, requiring deep domain knowledge and intricate simulation, contributes to longer development timelines compared to purely digital counterparts. Furthermore, the global semiconductor supply chain has demonstrated vulnerabilities, particularly highlighted by recent geopolitical tensions and natural disasters, leading to shortages and price volatility that impact production and market stability. Regulatory hurdles, evolving environmental standards, and the intense global competition also add layers of complexity, requiring continuous adaptation and strategic resource allocation from market participants. These restraints necessitate robust strategic planning, investment in diversified supply chains, and a continuous focus on operational efficiency to mitigate risks.

However, the market is simultaneously brimming with lucrative opportunities that promise new avenues for innovation and revenue generation. The proliferation of edge computing, where processing occurs closer to the data source, presents a significant opportunity for specialized analog ICs that can perform initial data conditioning and even some AI inference with ultra-low power consumption. The deeper integration of Artificial Intelligence (AI) and Machine Learning (ML) capabilities directly into analog and mixed-signal designs allows for more intelligent sensors and adaptive power management. Moreover, the global shift towards renewable energy systems, such as solar and wind power, and the expansion of energy storage solutions, are driving demand for high-performance power management and control ICs utilizing wide bandgap materials like SiC and GaN. These opportunities underscore a future where analog semiconductors will not only support but actively enable the next wave of technological innovation, particularly in areas demanding efficiency, precision, and intelligence at the interface of the physical and digital worlds. Companies that strategically invest in these emerging areas are poised for significant market share expansion and long-term success.

The Analog Semiconductors Market is meticulously segmented based on distinct product types and diverse application areas, providing a granular and comprehensive framework for understanding its intricate dynamics and identifying key growth vectors. This detailed segmentation is crucial for stakeholders, including manufacturers, investors, and policymakers, as it illuminates the varying technological requirements, specific market drivers, and unique customer demands within each category. Such an analytical approach enables a precise evaluation of market size, competitive intensity, and emergent opportunities across the expansive landscape of analog components, ranging from high-volume, general-purpose devices to highly specialized, performance-critical integrated circuits. Each segment possesses its own unique ecosystem of innovation, supply chain considerations, and strategic competitive positioning, making detailed analysis essential for informed decision-making.

A thorough understanding of these segments is paramount for market participants aiming to identify the most lucrative investment areas, strategically tailor their product development efforts, and effectively penetrate specific vertical markets. For instance, the power management ICs segment addresses the universal and critical need for optimizing energy consumption across all electronic devices, a requirement that continuously evolves with technological advancements and environmental regulations. Conversely, the mixed-signal ICs segment caters to applications that demand a seamless and highly efficient interaction between continuous analog signals and discrete digital data, which is fundamental for modern embedded systems and advanced communication platforms. The application-based segmentation further highlights the industries that are not only the largest consumers but also the primary innovators in analog technology, such as the burgeoning automotive sector with its complex ADAS and EV demands, and the rapidly expanding industrial IoT landscape that requires robust and precise sensing capabilities. This segmented view provides a strategic roadmap for market players to prioritize their efforts and maximize their impact in this dynamic industry.

The value chain for analog semiconductors is a sophisticated and highly interconnected global ecosystem, commencing with cutting-edge research and development and culminating in the delivery of critical components to diverse end-use markets. The upstream segment of this chain is foundational, encompassing advanced research, intellectual property (IP) generation, and the meticulous design of complex analog circuits. Key activities here include the development of proprietary architectures, sophisticated simulation, and verification processes. This stage heavily relies on electronic design automation (EDA) tool providers, who supply the software necessary for chip design, and highly specialized equipment suppliers, who provide the precision machinery required for semiconductor manufacturing. Furthermore, the procurement of highly purified raw materials, such as silicon wafers, specialty chemicals, and gases, is a critical upstream activity, with suppliers playing a vital role in quality and consistency.

The midstream segment constitutes the core manufacturing processes, primarily dominated by semiconductor foundries. These can be integrated device manufacturers (IDMs), which design, manufacture, and sell their own chips, or pure-play foundries, which exclusively fabricate chips for other companies. This stage involves highly specialized and capital-intensive processes, including photolithography, etching, deposition, and ion implantation, to create the intricate circuitry on silicon wafers. Following wafer fabrication, the individual semiconductor dies are separated, and then undergo assembly, packaging, and rigorous testing to ensure functionality, reliability, and adherence to performance specifications. This critical post-fabrication phase often involves outsourced semiconductor assembly and test (OSAT) providers, who specialize in these intricate processes, highlighting the globalized and highly specialized nature of the semiconductor manufacturing ecosystem, where efficiency and precision at each step are paramount to final product quality.

The downstream segment of the value chain focuses on the integration of these analog semiconductors into final electronic products and their subsequent distribution to end-users. This involves original equipment manufacturers (OEMs) and original design manufacturers (ODMs) across various industries, including automotive, industrial, consumer electronics, and communication, who incorporate analog ICs into their systems. These manufacturers are the primary buyers, integrating analog components into everything from smartphones and automotive control units to medical diagnostic equipment and industrial robots. The distribution channels for analog semiconductors are multifaceted: large integrated device manufacturers often engage in direct sales with their major, high-volume customers, leveraging established relationships and technical support capabilities. Simultaneously, an extensive network of authorized distributors plays a crucial role in serving a broader base of smaller and mid-sized enterprises, offering logistical support, inventory management, technical assistance, and access to a wide array of products globally. Both direct and indirect channels are essential for maximizing market reach and ensuring efficient product availability to the diverse customer base.

The potential customer base for analog semiconductors is remarkably broad and diverse, underscoring the ubiquitous nature and foundational importance of these components across virtually every sector of the modern economy. These end-users, or direct buyers of analog products, represent a vast spectrum of industries, ranging from global manufacturing conglomerates to agile technology startups. All these entities share a common critical requirement: the need for precise signal processing, highly efficient power management, and reliable data conversion to power their innovations, enhance product functionality, and ensure operational excellence. The intrinsic versatility of analog semiconductors means that their demand is not confined to a single industry niche but rather permeates multiple critical sectors, acting as essential building blocks for solutions spanning from high-volume consumer goods to highly specialized industrial, medical, and aerospace applications.

Key segments of potential customers include prominent players in the automotive industry, comprising both original equipment manufacturers (OEMs) and their Tier 1 suppliers. These customers demand robust and highly reliable analog ICs for advanced driver-assistance systems (ADAS), the complex powertrains of electric vehicles (EVs), sophisticated battery management systems (BMS), and cutting-edge infotainment solutions. In the industrial sector, customers encompass manufacturers of factory automation equipment, robotics, power supplies, and various sensor systems, all requiring high-precision, durable, and long-lifecycle analog solutions to ensure optimal performance and safety in challenging environments. Furthermore, the vast landscape of consumer electronics brands, developing products such as smartphones, laptops, wearables, smart home devices, and high-fidelity audio systems, represents a significant purchasing segment. Their focus is on achieving superior power efficiency, compact form factors, and enhanced user experience through advanced analog integration. The communication sector, including telecom infrastructure providers, networking equipment manufacturers, and data center operators, also heavily relies on analog ICs for 5G base stations, high-speed data transmission, RF front-ends, and signal integrity assurance, enabling the global digital infrastructure. Additionally, the medical device industry, aerospace and defense sector, and emerging renewable energy segment are increasingly pivotal customers, driving demand for specialized, high-performance, and ultra-reliable analog components tailored to their unique and stringent requirements.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 70 billion |

| Market Forecast in 2032 | USD 117 billion |

| Growth Rate | 7.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Texas Instruments, Analog Devices Inc., Infineon Technologies AG, NXP Semiconductors N.V., STMicroelectronics N.V., Renesas Electronics Corporation, Microchip Technology Inc., ON Semiconductor Corporation, Skyworks Solutions Inc., Qorvo Inc., Broadcom Inc., Maxim Integrated (now part of ADI), ROHM Co. Ltd., Vishay Intertechnology Inc., Power Integrations Inc., Diodes Incorporated, Cirrus Logic Inc., Semtech Corporation, Silicon Labs, Allegro MicroSystems |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Analog Semiconductors Market is in a perpetual state of technological evolution, constantly driven by innovations that aim to elevate performance, significantly reduce power consumption, and unlock entirely new application possibilities. One of the most transformative advancements is the widespread adoption and continuous development of wide bandgap (WBG) semiconductor materials, notably Silicon Carbide (SiC) and Gallium Nitride (GaN). These revolutionary materials are fundamentally reshaping the field of power electronics by offering vastly superior efficiency, the capability to operate at much higher temperatures, and the ability to design components with significantly smaller form factors compared to traditional silicon-based devices. This makes SiC and GaN materials indispensable for critical applications such as high-power electric vehicles (EVs), advanced renewable energy systems including solar inverters and wind turbines, and high-density data centers, where meeting stringent power efficiency demands and thermal management challenges is paramount for next-generation electronic systems.

Another pivotal area of innovation lies in advanced packaging technologies, which are rapidly evolving to meet the demands for higher integration and miniaturization without compromising performance. Techniques such as System-in-Package (SiP) and sophisticated heterogeneous integration are at the forefront of this trend. These cutting-edge approaches facilitate the seamless integration of multiple dissimilar chips—including various analog, digital, and memory components—into a single, compact package. This not only dramatically reduces the overall physical footprint of the electronic module but also yields substantial performance improvements by minimizing signal loss, reducing parasitic effects, and lowering latency. Such advancements are critically important for creating highly compact, high-performance devices demanded by modern consumer electronics, wearable technology, and edge AI applications. Furthermore, the advent of software-defined analog is fundamentally transforming how analog circuits are conceived, designed, and configured, ushering in an era of greater flexibility and adaptability in a multitude of applications. This paradigm shift enables the creation of reconfigurable analog front-ends and more agile product development cycles, allowing manufacturers to respond to diverse and rapidly changing market needs with unprecedented efficiency and responsiveness.

Beyond materials and packaging, the integration of micro-electromechanical systems (MEMS) with sophisticated analog integrated circuits is significantly expanding the capabilities and intelligence of sensor technology. This convergence facilitates the development of highly integrated, intelligent sensors for applications like precision accelerometers, gyroscopes, pressure sensors, and microphones, which can directly interface with digital processing units with enhanced accuracy and lower power. These smart sensors are critical for the growth of IoT, smart cities, and autonomous systems. Moreover, continuous advancements in process technologies, pushing the boundaries towards smaller geometries and specialized fabrication techniques tailored for analog components, play a vital role. These innovations enable higher performance characteristics, lower power consumption, and greater integration density for analog components across the entire spectrum of electronic devices. These technological strides collectively support the escalating demands of next-generation applications in the Internet of Things, Artificial Intelligence, 5G communication, and beyond, ensuring that analog semiconductors remain at the forefront of technological progress.

Analog semiconductors are electronic components that process continuous, variable electrical signals from the real world, such as temperature, sound, and pressure. They are crucial because they act as the essential interface, converting, amplifying, filtering, and managing these physical signals for interaction with digital systems, thereby enabling almost all modern electronics to function and interact with their environment accurately and efficiently.

The primary consumers of analog semiconductors span a wide range of industries including automotive (for ADAS, EV powertrains), industrial automation (robotics, process control), consumer electronics (smartphones, wearables, appliances), communication (5G, networking infrastructure), and healthcare (medical imaging, diagnostics).

The Analog Semiconductors Market is projected to experience robust growth, driven by increasing digitalization, demand for connected devices, and advancements in various end-use sectors. It is expected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2025 and 2032, reaching USD 117 billion by the end of the forecast period.

AI significantly boosts demand for analog semiconductors by requiring high-performance data converters for efficient sensor data acquisition, advanced power management ICs for powering AI accelerators, and specialized analog front-ends for processing real-world data at the edge. Analog components are vital for enabling precise data capture and energy-efficient AI operations.

Key technological trends include the increasing adoption of wide bandgap (WBG) materials like SiC and GaN for power efficiency, advancements in heterogeneous integration and System-in-Package (SiP) for miniaturization, the rise of software-defined analog for flexibility, and continued innovation in process technologies for enhanced performance and integration density.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.