ID : MRU_ 427986 | Date : Oct, 2025 | Pages : 246 | Region : Global | Publisher : MRU

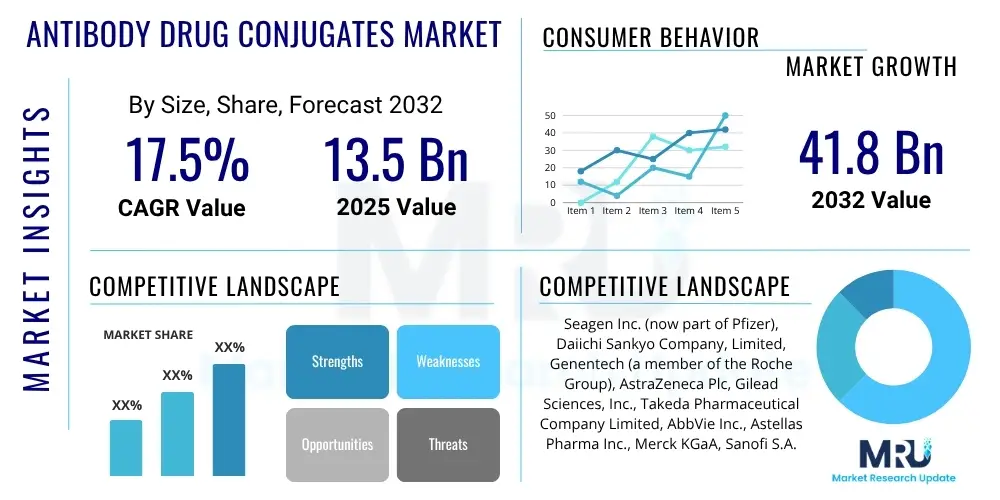

The Antibody Drug Conjugates Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 17.5% between 2025 and 2032. The market is estimated at USD 13.5 Billion in 2025 and is projected to reach USD 41.8 Billion by the end of the forecast period in 2032.

The Antibody Drug Conjugates (ADC) market represents a rapidly evolving and highly promising segment within oncology, offering a sophisticated approach to targeted cancer therapy. ADCs are a class of biopharmaceutical drugs designed to deliver highly potent cytotoxic agents directly to cancer cells, minimizing damage to healthy tissues. This precision is achieved by conjugating a monoclonal antibody (mAb), which specifically targets an antigen expressed on cancer cells, to a cytotoxic small-molecule drug (payload) via a chemical linker. The mAb acts as a homing device, guiding the potent drug to its intended target, thereby enhancing therapeutic efficacy and reducing systemic toxicity commonly associated with traditional chemotherapy regimens.

Key applications of Antibody Drug Conjugates primarily lie within the oncology sector, addressing a wide range of solid tumors and hematological malignancies, including but not limited to breast cancer, lung cancer, gastric cancer, bladder cancer, and various lymphomas and leukemias. The benefits of ADCs are multifaceted; they offer improved therapeutic indices, enhanced specificity, and often greater efficacy compared to conventional treatments, leading to better patient outcomes and reduced side effects. This targeted delivery mechanism is critical for overcoming drug resistance and improving response rates in difficult-to-treat cancers, thereby expanding the therapeutic landscape for patients with limited options.

The market is significantly driven by several factors, including the escalating global incidence of cancer, which creates an urgent and sustained demand for innovative and more effective treatment modalities. Continuous advancements in antibody engineering, linker technology, and payload chemistry are crucial driving forces, leading to the development of next-generation ADCs with optimized stability, potency, and safety profiles. Furthermore, the increasing number of regulatory approvals for novel ADCs, coupled with robust research and development activities by pharmaceutical and biotechnology companies, are propelling market growth. These developments underscore the transformative potential of ADCs as a cornerstone of modern cancer therapy, attracting substantial investment and fostering a competitive landscape focused on innovation.

The Antibody Drug Conjugates market is experiencing robust growth, driven by an expanding understanding of cancer biology, significant technological advancements, and increasing clinical success of approved ADCs. Business trends indicate a highly dynamic environment characterized by intense research and development efforts, strategic collaborations, mergers, and acquisitions aimed at consolidating pipelines and leveraging synergistic expertise. Pharmaceutical and biotechnology companies are heavily investing in ADC platforms, focusing on discovering novel targets, developing more stable linkers, and exploring potent payloads to enhance therapeutic efficacy and broaden the applicability of these targeted therapies. The increasing number of ADCs entering late-stage clinical trials reflects the industry's confidence in this modality, signaling a future where ADCs will play an even more central role in personalized oncology.

Regionally, North America continues to dominate the Antibody Drug Conjugates market, primarily due to its well-established healthcare infrastructure, high research and development spending, significant presence of key market players, and favorable regulatory environment that expedites drug approvals. Europe also represents a substantial market, driven by advanced medical research, a growing aging population, and increasing awareness of innovative cancer treatments. However, the Asia Pacific region is rapidly emerging as a high-growth market, propelled by increasing healthcare expenditure, rising cancer incidence rates, improving access to advanced therapies, and the expansion of clinical research activities. Countries like China, Japan, and India are becoming pivotal for market expansion, offering significant opportunities for market participants.

Segmentation trends within the ADC market highlight diverse areas of innovation and growth. By application, breast cancer, lung cancer, and hematological malignancies currently represent major segments, with ongoing research expanding into other solid tumors such as gastric, bladder, and ovarian cancers. Technology advancements are leading to a shift towards next-generation ADCs featuring site-specific conjugation, cleavable linkers, and novel payload mechanisms, promising even greater precision and reduced off-target effects. The market is also seeing differentiation by specific targets, with HER2, CD30, and Trop-2 being prominent, alongside a pipeline of new targets under investigation. These trends collectively underscore a market poised for sustained expansion and continuous innovation, continually redefining the standards of cancer care.

Common user questions regarding the impact of Artificial Intelligence (AI) on the Antibody Drug Conjugates market often revolve around how AI can accelerate drug discovery, optimize therapeutic design, enhance clinical trial efficiency, and improve patient stratification. Users are particularly interested in AI's potential to identify novel tumor-specific antigens, predict the efficacy and toxicity profiles of new ADC constructs, streamline the complex manufacturing processes, and even personalize treatment strategies by analyzing vast amounts of patient data. There is a strong expectation that AI will significantly reduce the time and cost associated with ADC development, mitigate risks associated with clinical failures, and ultimately lead to more effective and safer therapies reaching patients faster. Concerns sometimes include the accuracy of AI predictions, data privacy, and the integration challenges of AI tools into existing pharmaceutical workflows.

The Antibody Drug Conjugates market is significantly propelled by several robust drivers. A primary driver is the persistent high unmet medical need in oncology, particularly for cancers that are resistant to conventional therapies or where existing treatments are associated with severe systemic toxicities. ADCs offer a more targeted approach, promising improved efficacy with reduced side effects, which is highly appealing to both clinicians and patients. Furthermore, the continuous and rapid pace of technological innovation in antibody engineering, linker chemistry, and cytotoxic payload development is enabling the creation of next-generation ADCs with enhanced stability, potency, and tumor-specificity. The increasing number of successful clinical trials and subsequent regulatory approvals for ADCs across various cancer types further fuels market expansion, demonstrating their clinical utility and paving the way for broader adoption.

However, the market also faces considerable restraints that could impede its growth trajectory. The complexity and high cost associated with the research, development, and manufacturing of ADCs represent a significant barrier. Developing a successful ADC requires expertise in multiple disciplines, including immunology, medicinal chemistry, and bioconjugation, leading to prolonged development timelines and substantial financial investment. The potential for off-target toxicity, despite the targeted nature of ADCs, remains a concern, necessitating careful selection of targets and optimization of conjugation strategies. Immunogenicity, where the body's immune system reacts to the foreign antibody component, can also limit treatment efficacy and patient eligibility. Additionally, challenges related to reimbursement policies and market access in different healthcare systems can affect the commercial uptake of these high-cost therapies.

Despite these challenges, the Antibody Drug Conjugates market presents numerous lucrative opportunities. The exploration of novel tumor-associated antigens (TAAs) beyond established targets opens new avenues for therapeutic development, allowing ADCs to address a wider array of cancers. The potential for combination therapies, where ADCs are used in conjunction with other anti-cancer agents such as immunotherapies or conventional chemotherapies, offers synergistic effects and improved overall survival rates. Advancements in site-specific conjugation techniques and innovative linker designs promise to yield ADCs with superior pharmacological properties, further expanding their therapeutic window. Moreover, the increasing adoption of ADCs in emerging economies and the development of biosimilar ADCs once patents expire will contribute to broader market penetration and accessibility. The integration of advanced computational tools, including AI and machine learning, throughout the ADC development pipeline also presents a transformative opportunity to accelerate discovery and optimization.

The impact forces influencing the ADC market are multifaceted and dynamic. Technological innovation remains the paramount force, continuously pushing the boundaries of what is possible in targeted drug delivery and enabling the creation of more sophisticated and effective constructs. The evolving regulatory environment, with agencies like the FDA and EMA streamlining approval pathways for breakthrough therapies, significantly impacts market entry and commercial success. The competitive landscape is intense, driven by a growing number of pharmaceutical and biotechnology companies vying for market share, fostering innovation but also leading to pricing pressures and the need for differentiation. Furthermore, global healthcare spending trends and the increasing demand for personalized medicine solutions are key macro-economic forces shaping investment and strategic decisions within the ADC sector. Patent expirations of early-generation ADCs will also exert pressure, opening opportunities for biosimilar development and increasing market competition.

The Antibody Drug Conjugates market is comprehensively segmented across various crucial parameters, providing a detailed understanding of its complex structure and growth dynamics. These segmentations allow for a granular analysis of market trends, identifying key areas of innovation, therapeutic focus, and geographical influence. Understanding these segments is vital for stakeholders, including pharmaceutical companies, investors, and healthcare providers, to pinpoint specific opportunities, assess competitive landscapes, and formulate strategic decisions. The market is typically categorized by target antigen, payload type, linker technology, application (cancer type), and end-user, each reflecting distinct technological and clinical imperatives. This structured approach helps in evaluating the market's current state and projecting its future trajectory based on evolving scientific advancements and clinical needs, particularly in the highly specialized field of oncology where precision medicine is paramount.

The value chain for the Antibody Drug Conjugates market is intricate, involving multiple specialized stages from initial drug discovery to final patient administration, each contributing to the overall complexity and cost of these advanced therapies. The upstream segment of the value chain is critical and encompasses the sourcing and manufacturing of essential raw materials. This includes the production of high-quality monoclonal antibodies (mAbs) through mammalian cell culture, the synthesis of highly potent cytotoxic payloads, and the development and manufacturing of specialized chemical linkers. These components are often sourced from a diverse network of suppliers, including contract development and manufacturing organizations (CDMOs) specializing in biopharmaceuticals and fine chemical synthesis. The quality and purity of these raw materials are paramount, as they directly impact the efficacy and safety of the final ADC product, necessitating rigorous quality control measures.

Moving downstream, the value chain encompasses the sophisticated processes of ADC conjugation, purification, formulation, and clinical development. The conjugation step, where the antibody, linker, and payload are precisely joined, is technically challenging and requires specialized expertise and infrastructure to ensure consistency and optimal drug-to-antibody ratio (DAR). After conjugation, the ADC undergoes extensive purification to remove unconjugated components and aggregates, followed by formulation into a stable drug product suitable for clinical use. The subsequent stages involve rigorous preclinical testing to assess safety and efficacy in animal models, followed by multiple phases of clinical trials in human subjects. These trials are essential for demonstrating the ADC's therapeutic benefits and establishing its safety profile, ultimately leading to regulatory approval. Contract research organizations (CROs) often play a significant role in managing and executing these complex preclinical and clinical studies, providing specialized services and accelerating development timelines.

The distribution channel for Antibody Drug Conjugates is highly regulated and specialized, reflecting the nature of these potent oncology drugs. Direct distribution typically involves pharmaceutical companies directly supplying their ADC products to hospitals, specialized oncology clinics, and academic medical centers, especially for newly launched or high-value therapies. This direct approach allows for closer control over inventory, temperature-controlled logistics, and direct communication with healthcare providers regarding proper handling and administration. Indirect distribution involves working with third-party logistics (3PL) providers and specialized pharmaceutical distributors who manage the complex supply chain, ensuring that ADCs are stored and transported under stringent conditions to maintain their integrity and efficacy. Given the high cost and sensitivity of ADCs, robust cold chain management and adherence to Good Distribution Practices (GDP) are non-negotiable across both direct and indirect channels. The ultimate goal is to ensure timely and safe delivery of these life-saving medications to patients worldwide, supported by comprehensive post-market surveillance and pharmacovigilance programs.

The primary potential customers and end-users of Antibody Drug Conjugates are predominantly within the oncology landscape, driven by the critical need for advanced cancer therapies. Hospitals, particularly large university-affiliated medical centers and regional cancer hospitals, represent a significant customer segment. These institutions treat a vast number of cancer patients and are equipped with the infrastructure, specialists (oncologists, hematologists, pathologists), and research capabilities required for administering complex biologic therapies like ADCs. They serve as key points of care where ADCs are prescribed, dispensed, and administered, often within the context of comprehensive cancer treatment plans. The decision-making process within hospitals involves multidisciplinary teams, considering clinical guidelines, patient profiles, and drug availability, with a strong emphasis on efficacy, safety, and cost-effectiveness for managing various cancer types.

Specialty cancer clinics, including private oncology practices and outpatient infusion centers, also constitute a crucial segment of potential customers. These clinics specialize in providing targeted cancer care, offering a more personalized and accessible environment for patients receiving infusion therapies. As ADCs become more widely adopted and their administration protocols become standardized, these clinics play an increasingly important role in delivering treatment closer to patients' homes, improving convenience and adherence. The oncologists and hematologists practicing in these specialty clinics are direct prescribers and administrators of ADCs, making them key opinion leaders and decision-makers in the adoption and utilization of these therapies. Their insights into patient needs and treatment outcomes are invaluable for pharmaceutical companies developing and commercializing ADCs, often influencing real-world evidence and market penetration.

Beyond direct patient care settings, academic and research institutions are significant indirect customers, playing a vital role in advancing the ADC field. These institutions conduct extensive basic and translational research on cancer biology, identify novel therapeutic targets, develop new antibody constructs and conjugation chemistries, and participate in early-stage clinical trials. While they may not directly purchase commercial ADCs for routine patient treatment, their research activities drive future market growth by identifying new indications, improving existing ADC platforms, and discovering next-generation therapies. Pharmaceutical and biotechnology companies are also customers in a broader sense, often engaging in licensing agreements, collaborations, and partnerships for ADC development, access to proprietary technologies, or co-development initiatives. These collaborations are essential for sharing expertise, mitigating risks, and accelerating the development and commercialization pipeline of innovative Antibody Drug Conjugates, thereby expanding the overall market ecosystem.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 13.5 Billion |

| Market Forecast in 2032 | USD 41.8 Billion |

| Growth Rate | 17.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Seagen Inc. (now part of Pfizer), Daiichi Sankyo Company, Limited, Genentech (a member of the Roche Group), AstraZeneca Plc, Gilead Sciences, Inc., Takeda Pharmaceutical Company Limited, AbbVie Inc., Astellas Pharma Inc., Merck KGaA, Sanofi S.A., Bristol Myers Squibb Company, ADC Therapeutics SA, RemeGen Co., Ltd., Kyowa Kirin Co., Ltd., MabLink Bioscience, Sutro Biopharma, Inc., MacroGenics, Inc., Immunogen, Inc., Shanghai Miracogen Inc., Zymeworks Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Antibody Drug Conjugates market is defined by a dynamic and continuously evolving technological landscape that underpins the design, development, and manufacturing of these sophisticated therapeutics. A cornerstone of this landscape is advanced antibody engineering, which focuses on developing highly specific monoclonal antibodies that selectively target antigens expressed on cancer cells while sparing healthy tissues. This involves optimizing antibody affinity, specificity, and pharmacokinetics, alongside minimizing immunogenicity, often through humanization or fully human antibody platforms. Innovations in antibody design, such as bispecific antibodies or antibody fragments, are also being explored to enhance tumor penetration and improve therapeutic window, pushing the boundaries of targeted delivery and reducing the potential for off-target binding, thereby improving the overall safety profile of ADCs.

Another critical technological area is linker chemistry, which is pivotal for the stability of the ADC in circulation and the efficient release of the cytotoxic payload within the tumor cell. The market leverages various linker types, broadly categorized into cleavable and non-cleavable designs. Cleavable linkers, such as those sensitive to pH, proteases (e.g., valine-citrulline based), or glutathione, are designed to release the payload specifically within the tumor microenvironment or inside cancer cells. Non-cleavable linkers, on the other hand, require the complete degradation of the antibody to release the active drug, offering different pharmacokinetic and safety profiles. Recent advancements focus on site-specific conjugation technologies (e.g., enzymatic conjugation, sortase-mediated ligation, genetic code expansion), which allow for precise control over the drug-to-antibody ratio (DAR) and conjugation site, leading to more homogeneous and stable ADCs with improved therapeutic indices and predictable pharmacology, representing a significant leap forward from traditional random conjugation methods.

Furthermore, the key technology landscape includes innovations in cytotoxic payload chemistry and manufacturing processes. The payloads used in ADCs are extremely potent small molecules, often derived from natural products or synthetically designed, engineered to induce cell death through various mechanisms such as microtubule disruption (e.g., auristatins, maytansinoids) or DNA damage (e.g., calicheamicins, duocarmycins, exatecan derivatives). The development of novel payloads with higher potency and different mechanisms of action is an ongoing area of research. On the manufacturing front, advanced bioconjugation techniques, process analytical technologies (PAT), and robust quality control systems are crucial for ensuring the reproducibility, purity, and consistency of ADC production. The integration of high-throughput screening, automation, and advanced analytical methods (e.g., mass spectrometry, hydrophobic interaction chromatography) throughout the development and manufacturing lifecycle is essential for overcoming the complex challenges associated with producing these intricate biopharmaceutical products at scale, ensuring both product quality and supply chain reliability for global distribution.

Antibody Drug Conjugates (ADCs) are a sophisticated class of targeted cancer therapies that combine the specificity of monoclonal antibodies with the potency of cytotoxic drugs. An ADC consists of three main components: a monoclonal antibody (mAb) that specifically binds to an antigen highly expressed on the surface of cancer cells, a highly potent cytotoxic small-molecule drug (payload) capable of inducing cell death, and a chemical linker that covalently connects the mAb to the payload. The mAb acts as a precise delivery system, guiding the cytotoxic drug directly to tumor cells. Once the ADC binds to the target antigen on the cancer cell surface, it is internalized through receptor-mediated endocytosis. Inside the cell, the linker is cleaved (either enzymatically or non-enzymatically, depending on the linker design) in the lysosome, releasing the active cytotoxic payload. This localized release of the drug leads to targeted cell killing, minimizing systemic exposure and reducing damage to healthy tissues, thereby improving the therapeutic index and reducing side effects compared to traditional chemotherapy.

Antibody Drug Conjugates are primarily used in the treatment of various solid tumors and hematological malignancies, with their applications continuously expanding as new ADCs receive regulatory approval and advance through clinical trials. Currently approved ADCs are effectively used to treat a range of cancers including HER2-positive breast cancer, certain types of non-small cell lung cancer (NSCLC), gastric cancer, urothelial cancer (bladder cancer), and specific hematological malignancies such as Hodgkin lymphoma, diffuse large B-cell lymphoma (DLBCL), and multiple myeloma. Extensive research and development efforts are underway, with numerous ADCs in late-stage clinical trials for additional indications like triple-negative breast cancer, colorectal cancer, ovarian cancer, head and neck squamous cell carcinoma, pancreatic cancer, and other challenging solid tumors. The exploration of novel tumor-associated antigens and the development of next-generation ADC platforms are continuously broadening the therapeutic scope and potential impact of ADCs across a wider spectrum of oncological conditions, offering hope for patients with limited treatment options.

Antibody Drug Conjugates offer several significant advantages over traditional chemotherapy and even some other targeted therapies due to their unique mechanism of action. The primary advantage is their enhanced specificity: ADCs can precisely target cancer cells that express a specific antigen, thereby delivering a highly potent cytotoxic payload directly to the tumor site. This targeted approach significantly reduces systemic exposure to the cytotoxic drug, leading to a substantial decrease in off-target toxicity and fewer severe side effects commonly associated with conventional chemotherapy, such as bone marrow suppression, alopecia, and gastrointestinal issues. By localizing the therapeutic effect, ADCs improve the therapeutic index, allowing for the administration of more potent drugs that might otherwise be too toxic. Furthermore, ADCs can overcome certain mechanisms of drug resistance observed with traditional treatments, leading to improved efficacy and higher response rates in difficult-to-treat cancers. Their ability to deliver a concentrated dose of cytotoxic agents directly inside cancer cells, even those with limited access, makes them a powerful tool in personalized oncology, offering better patient outcomes and an improved quality of life.

Despite their significant promise, the Antibody Drug Conjugates market faces several substantial challenges and restraints that can impact its growth. One of the primary concerns is the inherent complexity and exceedingly high cost associated with the research, development, and manufacturing of ADCs. The multi-component nature of ADCs, involving antibody engineering, linker chemistry, and payload synthesis, necessitates specialized expertise, advanced facilities, and rigorous quality control at every stage, leading to prolonged development timelines and substantial financial investment. Another significant restraint is the potential for off-target toxicity, even with targeted delivery. While ADCs aim to minimize systemic exposure, partial antigen expression on healthy cells or premature linker cleavage in circulation can still lead to undesirable side effects. Immunogenicity, where the patient's immune system develops anti-drug antibodies against the ADC, can also compromise efficacy and necessitate treatment discontinuation. Furthermore, challenges related to market access, high pricing of these innovative therapies, and complex reimbursement landscapes across different healthcare systems can limit their widespread adoption and affordability for patients, particularly in emerging markets, necessitating strategic pricing models and evidence-based value propositions.

The Antibody Drug Conjugates market is poised for significant future evolution driven by continuous innovation and emerging trends. One major trend is the development of next-generation ADCs featuring enhanced site-specific conjugation technologies, which allow for precise control over the drug-to-antibody ratio (DAR) and conjugation location, leading to more homogeneous and stable products with improved therapeutic windows. There is also a strong focus on discovering novel tumor-associated antigens (TAAs) to expand the applicability of ADCs to a broader range of cancer types, including those currently lacking effective targeted options. The exploration of new cytotoxic payloads with different mechanisms of action and higher potency, including immunostimulatory agents, is another key trend. Combination therapies, where ADCs are used in conjunction with immunotherapies, PARP inhibitors, or other anti-cancer agents, are gaining traction to achieve synergistic effects and overcome resistance mechanisms. Furthermore, the integration of artificial intelligence (AI) and machine learning (ML) in various stages of ADC development, from target identification and linker design to clinical trial optimization and patient selection, is expected to accelerate discovery, improve efficiency, and personalize treatment strategies. Finally, the development of bispecific ADCs and ADCs with alternative formats (e.g., antibody fragments) represents a frontier for enhanced tumor penetration and reduced toxicity.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.