ID : MRU_ 428832 | Date : Oct, 2025 | Pages : 242 | Region : Global | Publisher : MRU

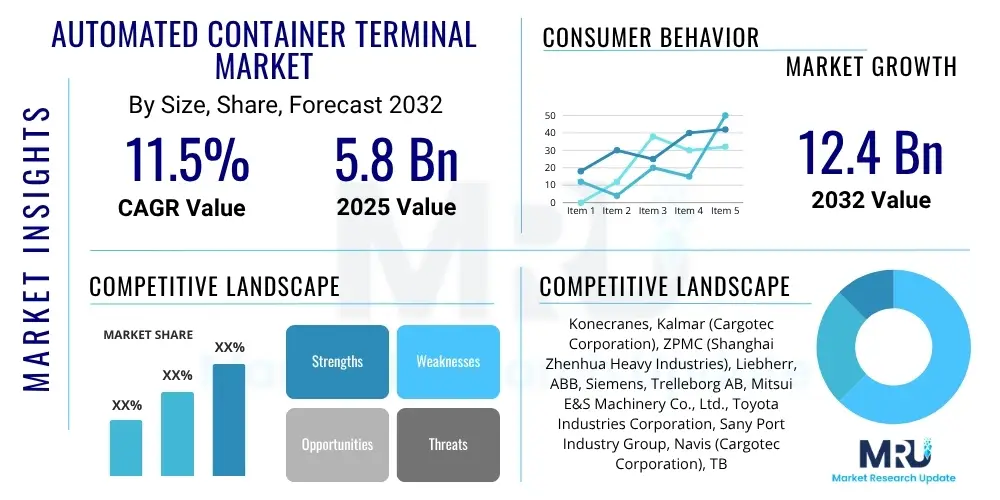

The Automated Container Terminal Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2025 and 2032. The market is estimated at USD 5.8 Billion in 2025 and is projected to reach USD 12.4 Billion by the end of the forecast period in 2032.

The Automated Container Terminal (ACT) Market encompasses the infrastructure, technologies, and systems designed to manage and move shipping containers with minimal human intervention. This sophisticated ecosystem includes automated cranes, automated guided vehicles (AGVs), automated stacking cranes (ASCs), and advanced terminal operating systems (TOS) that collectively enhance port efficiency, safety, and throughput. Automated terminals represent a significant evolutionary leap from traditional manual operations, addressing the escalating demands of global trade, increasing vessel sizes, and the imperative for faster turnaround times.

The primary product offerings within this market are comprehensive automation solutions that integrate hardware and software components to streamline container handling from vessel to gate. Major applications span large-scale international shipping hubs, transshipment ports, and inland intermodal facilities, where the benefits of automation, such as reduced labor costs, improved operational consistency, and optimized space utilization, are most pronounced. The driving factors for this market's expansion include the continuous growth in global seaborne trade, the need for enhanced operational efficiency to manage larger container volumes, mounting pressure to reduce environmental impact, and the escalating costs and scarcity of skilled manual labor in developed economies.

The benefits derived from adopting automated container terminals are multifaceted, ranging from significant operational cost reductions through energy optimization and reduced damage rates to a substantial improvement in worker safety by minimizing human exposure to hazardous heavy machinery. Furthermore, these terminals offer unparalleled predictability and reliability in operations, enabling ports to handle peak demands more effectively and maintain competitive service levels in a dynamic global logistics landscape. The ability to operate 24/7 in various weather conditions, coupled with precise container tracking and optimized yard management, underscores the transformative impact of automation on modern port logistics.

The Automated Container Terminal Market is experiencing robust growth driven by an evolving global trade landscape, persistent labor challenges, and the continuous push for enhanced operational efficiency and sustainability within the maritime industry. Business trends indicate a strong focus on digital transformation, with increasing integration of AI, IoT, and big data analytics to optimize decision-making, improve predictive maintenance, and enable fully autonomous operations. There is a discernible shift towards remote operation capabilities, allowing for centralized control and management, which further improves safety and resource allocation across multiple terminal sites. Moreover, sustainability initiatives are influencing investment decisions, pushing for electrification of equipment and energy-efficient designs to meet stringent environmental regulations and corporate social responsibility goals.

Regionally, Asia Pacific continues to dominate the market, largely due to significant investments in new port infrastructure and the expansion of existing facilities to support rapid economic growth and burgeoning trade volumes, particularly in China and Southeast Asian nations. Europe and North America are characterized by a strong emphasis on modernizing existing terminals, driven by high labor costs, limited expansion space, and the need to maintain competitiveness through technological upgrades. These regions are also pioneering advanced automation solutions and integration with broader logistics networks. The Middle East and Africa present emerging opportunities, with strategic investments in state-of-the-art port facilities to establish regional trade hubs and diversify economies, supported by government initiatives to improve logistics infrastructure.

Segment-wise, the fully automated terminal segment is projected to exhibit the fastest growth, propelled by its superior efficiency, scalability, and long-term cost benefits, despite higher initial investment. The software component segment, particularly Terminal Operating Systems (TOS) and advanced analytics platforms, is becoming increasingly critical, acting as the central nervous system for complex automated operations. This segment’s growth is fueled by the need for seamless integration, real-time data processing, and intelligent decision support across all automated assets. The equipment segment, including automated stacking cranes and automated guided vehicles, remains a foundational pillar, with continuous advancements in battery technology, navigation systems, and machine vision improving performance and reliability. Overall, the market is moving towards highly integrated, data-driven, and environmentally conscious automation solutions to address the multifaceted challenges of global container logistics.

Common user questions regarding AI's impact on Automated Container Terminals often revolve around several core themes: the extent of efficiency gains, the potential for predictive maintenance and operational optimization, concerns about job displacement, the robustness of cybersecurity measures for AI-driven systems, the complexities of AI integration with existing infrastructure, and the ability of AI to enhance real-time decision-making in dynamic port environments. Users are keen to understand how AI can move beyond basic automation to intelligent, self-optimizing operations, addressing unforeseen challenges and maximizing resource utilization. There is also significant interest in the ROI of AI investments in terms of long-term operational savings and competitive advantage, alongside inquiries into the necessary skill sets for managing and maintaining these advanced AI systems. The overarching expectation is that AI will unlock new levels of performance and resilience in container logistics.

The Automated Container Terminal Market is primarily driven by a confluence of factors aimed at enhancing efficiency, reducing costs, and improving safety in global logistics. The ever-increasing volume of global trade necessitates higher throughput and faster vessel turnaround times, which manual operations struggle to achieve, thus pushing terminals towards automation. Furthermore, the rising labor costs, particularly in developed economies, coupled with a shortage of skilled port workers, make automation an economically compelling solution for long-term operational sustainability. Stringent environmental regulations and corporate sustainability mandates are also significant drivers, as automated electric equipment offers a greener alternative to traditional diesel-powered machinery, contributing to reduced carbon footprints and noise pollution. The inherent safety benefits of removing humans from hazardous operational areas further bolster the case for automation, minimizing workplace accidents and associated liabilities.

Despite these strong drivers, the market faces significant restraints. The exceptionally high initial capital investment required for automated systems, encompassing specialized equipment, advanced software, and complex infrastructure modifications, presents a substantial barrier to entry for many port operators. The complexity of integrating disparate automation technologies with existing legacy systems and the need for extensive customization often lead to prolonged implementation timelines and potential cost overruns. Cybersecurity risks associated with highly interconnected, data-driven automated systems represent a critical concern, as breaches could lead to operational paralysis and significant financial losses. Additionally, the potential for job displacement due to automation often leads to resistance from labor unions and requires careful social management strategies to ensure a smooth transition and maintain industrial harmony.

Opportunities for growth in this market are abundant, particularly in emerging economies where new port developments can be designed with automation from the ground up, bypassing the challenges of retrofitting older infrastructure. The continuous advancements in artificial intelligence, IoT, and 5G connectivity are creating avenues for more sophisticated, predictive, and truly autonomous operations, unlocking further efficiency gains. The increasing demand for resilient and transparent supply chains, highlighted by recent global disruptions, positions automated terminals as critical enablers of robust logistics networks. Additionally, the development of modular and scalable automation solutions, along with innovative financing models, could make automation more accessible to a broader range of terminals, including medium-sized ports seeking incremental upgrades. The impact forces shaping this market include rapid technological evolution driving innovation, evolving global economic conditions influencing trade volumes and investment capacities, geopolitical stability affecting shipping routes and port development, and the increasing pressure from environmental and social governance (ESG) factors demanding sustainable and responsible operations.

The Automated Container Terminal Market is comprehensively segmented to provide a detailed understanding of its diverse components and evolving dynamics. This segmentation facilitates targeted strategic planning and investment decisions by identifying key growth areas and specific market needs. The market can be broadly categorized based on the level of automation employed, the types of components involved in an automated system, the specific terminal environments where these technologies are deployed, and the nature of the projects undertaken. Each segment represents distinct technological requirements, operational models, and investment considerations, reflecting the varied landscape of global port operations and their readiness for digital transformation.

The value chain for the Automated Container Terminal Market involves a complex interplay of various stakeholders, starting from the conceptualization and manufacturing of specialized components to the ultimate operation of a fully functional automated port. This chain begins with upstream activities focused on research, development, and production of key technologies and equipment. These include heavy machinery manufacturers that produce automated cranes and vehicles, as well as software developers who create the sophisticated Terminal Operating Systems (TOS) and control algorithms that serve as the brain of the terminal. System integrators play a pivotal role in combining these diverse components into a cohesive, operational system, often customizing solutions to specific port layouts and operational requirements. This upstream segment is characterized by high R&D investment, specialized engineering expertise, and stringent quality control standards.

Moving downstream, the value chain extends to the deployment, operation, and maintenance of automated terminals. The primary entities at this stage are port authorities and terminal operating companies, who are the end-users and direct beneficiaries of the automation solutions. Shipping lines and logistics providers also form crucial parts of the downstream value chain, as they interact directly with the automated terminals to move their cargo efficiently. The distribution channels for automated terminal solutions are typically direct sales from manufacturers and system integrators to port authorities or terminal operators, often facilitated through long-term contracts and strategic partnerships. Indirect channels may involve engineering, procurement, and construction (EPC) contractors who manage large-scale port development projects and integrate automation as part of their broader scope.

The interaction between these upstream and downstream participants is highly collaborative, given the bespoke nature and high capital expenditure associated with automated terminal projects. Direct distribution channels ensure close communication and customization, allowing solutions to be tailored precisely to the client’s needs, addressing unique geographical, operational, and regulatory challenges. Indirect channels, through EPC firms, provide a streamlined approach for clients seeking a single point of contact for complex infrastructure projects, where automation is a critical, integrated component. The efficiency and success of the automated terminal market depend heavily on strong partnerships, technological innovation, and a robust service and support infrastructure throughout the entire lifecycle of the terminal, ensuring optimal performance and continuous improvement.

The primary potential customers and end-users of Automated Container Terminal solutions are diverse, yet all share a common objective: to enhance the efficiency, capacity, and sustainability of their port operations. Port Authorities, as the owners and regulators of port infrastructure, represent a significant customer segment. Their decisions to invest in automation are often driven by strategic national interests, such as increasing global trade competitiveness, accommodating larger vessels, and improving overall logistics capabilities. They seek solutions that offer long-term operational cost savings, contribute to environmental compliance, and improve safety standards within their jurisdictions. These entities typically engage in large-scale infrastructure projects, including the development of new greenfield terminals or the comprehensive modernization of existing facilities, making them crucial drivers of market demand.

Terminal Operating Companies (TOCs), which manage and operate the day-to-day activities of container terminals, form another critical customer base. Their motivations for adopting automation are directly linked to improving operational metrics such as container moves per hour, vessel turnaround times, and yard utilization rates, all of which directly impact profitability and service quality. TOCs often face intense competition and pressure to handle increasing cargo volumes while minimizing operational expenses. They seek automation solutions that are reliable, scalable, and offer a strong return on investment, enabling them to optimize labor deployment, reduce equipment wear and tear, and gain a competitive edge in attracting shipping lines. Their purchasing decisions are often influenced by proven technology, comprehensive service agreements, and the ability to seamlessly integrate with their existing operational frameworks.

Furthermore, major Shipping Lines and global Logistics Providers are increasingly influencing the adoption of automated terminals. While not direct purchasers of the automation systems themselves, these entities are key stakeholders that benefit immensely from the efficiencies provided by automated ports. Their preference for faster, more reliable, and predictable port calls directly incentivizes port authorities and terminal operators to invest in automation. Governments, particularly those investing in national infrastructure projects to boost trade and economic development, also act as significant influencers and sometimes direct funders or promoters of automated terminal initiatives. Their long-term strategic visions for maritime trade and logistics infrastructure often align perfectly with the capabilities offered by advanced automation, supporting smart port initiatives and regional economic growth.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 5.8 Billion |

| Market Forecast in 2032 | USD 12.4 Billion |

| Growth Rate | 11.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Konecranes, Kalmar (Cargotec Corporation), ZPMC (Shanghai Zhenhua Heavy Industries), Liebherr, ABB, Siemens, Trelleborg AB, Mitsui E&S Machinery Co., Ltd., Toyota Industries Corporation, Sany Port Industry Group, Navis (Cargotec Corporation), TBA Group, ORTS (Operating & Real-Time Systems), INFORM GmbH, Camco Technologies, Conductix-Wampfler, Beumer Group, igus GmbH, Phoenix Contact, Dellner Polymer Components |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Automated Container Terminal market is characterized by a sophisticated and evolving technological landscape, driven by continuous innovation aimed at enhancing efficiency, reliability, and scalability. At the core are Automated Stacking Cranes (ASCs) and Automated Rail Mounted Gantry (ARMG) cranes, which efficiently manage container storage and retrieval in the yard, often operating with high precision and minimal human oversight. These are complemented by Automated Guided Vehicles (AGVs) or Automated Container Shuttles (ACSs) that transport containers between the quay, yard, and gate, offering flexibility and reducing human exposure to heavy machinery. The operational intelligence is largely provided by advanced Terminal Operating Systems (TOS) and Equipment Control Systems (ECS), which integrate all hardware, manage container movements, optimize yard layouts, and provide real-time data for decision-making. These systems leverage complex algorithms and simulation capabilities to predict and optimize port operations.

Further technological advancements include Optical Character Recognition (OCR) systems for automated container identification and tracking, which significantly speed up gate processes and reduce errors. The Internet of Things (IoT) plays a crucial role through widespread sensor deployment across equipment and infrastructure, collecting vast amounts of data on performance, environmental conditions, and maintenance needs. This data feeds into predictive maintenance systems and artificial intelligence (AI) and machine learning (ML) algorithms, which optimize resource allocation, forecast demand, and enable truly self-learning and self-optimizing terminal operations. The deployment of 5G connectivity is also becoming increasingly vital, providing the low latency and high bandwidth necessary for real-time communication between automated equipment and centralized control systems, enabling more reliable and distributed control of terminal operations.

Emerging technologies continue to reshape this landscape, including blockchain for enhanced supply chain transparency and security, digital twins for virtual modeling and simulation of terminal operations, and advanced robotics for specialized tasks within the terminal environment. The focus is increasingly on achieving seamless integration between these disparate technologies, creating a highly resilient, adaptive, and efficient ecosystem. Robotics-as-a-Service (RaaS) models are also gaining traction, offering flexible deployment options for automation solutions without the massive upfront capital investment. Overall, the market is moving towards a future where terminals are not just automated but are intelligent, interconnected, and predictive, capable of responding dynamically to global trade fluctuations and optimizing performance autonomously while minimizing environmental impact and maximizing safety.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.