ID : MRU_ 430884 | Date : Nov, 2025 | Pages : 258 | Region : Global | Publisher : MRU

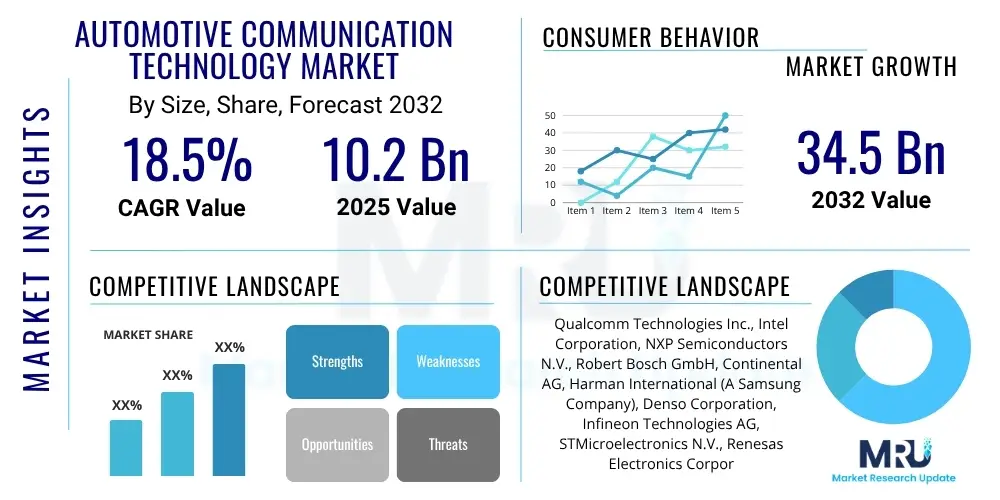

The Automotive Communication Technology Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2032. The market is estimated at USD 10.2 Billion in 2025 and is projected to reach USD 34.5 Billion by the end of the forecast period in 2032.

The Automotive Communication Technology Market encompasses the advanced systems and networks facilitating seamless data exchange within a vehicle, between vehicles (V2V), and between vehicles and external entities such as infrastructure (V2I), pedestrians (V2P), and the network (V2N). This broad spectrum of technologies is crucial for the development of connected, autonomous, shared, and electric (CASE) vehicles, driving significant transformations across the automotive industry. These communication solutions enable a myriad of functions from enhanced safety features like collision avoidance and traffic warnings to sophisticated infotainment systems and real-time diagnostic capabilities.

Products within this market range from various in-vehicle networks such as CAN, LIN, FlexRay, and automotive Ethernet, to external communication technologies including Dedicated Short-Range Communication (DSRC), Cellular Vehicle-to-Everything (C-V2X), 5G, Wi-Fi, and Bluetooth. Major applications span across advanced driver assistance systems (ADAS), autonomous driving, telematics, remote diagnostics, and in-car entertainment, all contributing to a more integrated and intelligent driving experience. The primary benefits include significantly improved road safety through reduced accidents, optimized traffic flow, reduced emissions, and enhanced convenience and comfort for vehicle occupants through sophisticated connectivity services.

Key driving factors propelling the growth of the Automotive Communication Technology Market include stringent governmental regulations mandating vehicle safety and environmental compliance, a rapidly increasing demand for connected and autonomous vehicles, and the proliferation of internet of things (IoT) and cloud-based services within the automotive ecosystem. Furthermore, consumer expectations for advanced in-car experiences and the increasing adoption of telematics for fleet management and insurance purposes are also contributing substantially to market expansion. The continuous evolution of communication standards and the integration of artificial intelligence are opening new avenues for innovation and market penetration.

The Automotive Communication Technology Market is experiencing dynamic growth, characterized by significant business trends such as escalating investments in research and development by automotive original equipment manufacturers (OEMs) and Tier 1 suppliers, alongside strategic collaborations between technology firms and traditional automotive players. The shift towards software-defined vehicles is profoundly influencing business models, emphasizing recurring revenue streams from services and over-the-air updates. Furthermore, the imperative for robust cybersecurity solutions is shaping product development, as connected vehicles become more vulnerable to external threats, driving a focus on secure communication protocols and architectures. Business strategies are increasingly centered on building comprehensive ecosystems that integrate hardware, software, and services.

Regional trends highlight Asia Pacific as a dominant and rapidly expanding market, fueled by high vehicle production, rapid urbanization, and increasing government support for smart city initiatives and connected infrastructure, particularly in countries like China, Japan, and South Korea. North America and Europe continue to be strongholds for technological innovation and early adoption, driven by stringent safety regulations, a high concentration of premium vehicle sales, and a robust automotive R&D ecosystem. These regions are actively deploying advanced V2X infrastructure and conducting pilot projects for autonomous driving, fostering an environment conducive to market growth. Emerging markets in Latin America and the Middle East and Africa are witnessing gradual adoption, primarily in telematics and basic connectivity services, with future growth anticipated as infrastructure develops and affordability improves.

Segment trends within the market indicate a robust expansion in both in-vehicle and vehicle-to-everything (V2X) communication technologies. Automotive Ethernet is rapidly gaining traction as a high-bandwidth backbone for in-vehicle networks, crucial for handling the immense data generated by advanced sensors and infotainment systems in modern vehicles. The V2X segment, encompassing DSRC and C-V2X, is witnessing significant deployment, driven by the promise of enhanced safety and efficient traffic management, with C-V2X emerging as a preferred standard due to its compatibility with existing cellular networks and evolving 5G capabilities. The software and services segments are projected to demonstrate accelerated growth, reflecting the industry's pivot towards connected services, remote diagnostics, and infotainment offerings, which generate continuous revenue streams and enhance the overall user experience.

User inquiries regarding AI's impact on automotive communication technology frequently revolve around how artificial intelligence enhances decision-making in autonomous vehicles, improves data processing efficiency, addresses cybersecurity vulnerabilities, and personalizes the in-car experience. Key concerns often include the reliability of AI algorithms in safety-critical communications, the implications of AI on data privacy, and the challenges associated with integrating complex AI systems into existing vehicle architectures. Expectations largely center on AI driving significant advancements in predictive analytics for maintenance, optimizing network bandwidth usage, and enabling more sophisticated and responsive vehicle interactions with their environment. The overarching theme is AI's potential to transform raw communication data into actionable intelligence, thereby making vehicles safer, smarter, and more user-centric.

The Automotive Communication Technology Market is significantly shaped by a combination of powerful drivers, inherent restraints, and burgeoning opportunities, all interacting to create dynamic impact forces. A primary driver is the accelerating demand for advanced connectivity features in modern vehicles, propelled by consumer expectations for seamless integration with personal devices and digital services. This is further amplified by the global push towards autonomous vehicles, which critically rely on robust, low-latency communication for safe and efficient operation. Governmental mandates for enhanced vehicle safety, coupled with environmental regulations promoting intelligent transport systems to reduce congestion and emissions, also act as strong catalysts for market growth. These factors collectively create a positive feedback loop, encouraging innovation and investment across the value chain, while fostering widespread adoption of advanced communication solutions.

However, several restraints temper this growth trajectory. Cybersecurity remains a paramount concern, as increased connectivity exposes vehicles to potential hacking and data breaches, necessitating significant investment in secure communication architectures. The high cost associated with implementing advanced communication technologies, including research and development, component manufacturing, and infrastructure deployment, poses a challenge, particularly in cost-sensitive markets. Furthermore, the lack of universally accepted standardization for V2X communication (e.g., DSRC vs. C-V2X) creates fragmentation and slows down large-scale deployment. Infrastructure limitations, particularly in less developed regions, hinder the full potential of vehicle-to-infrastructure (V2I) communication, requiring substantial public and private investment to overcome.

Despite these challenges, substantial opportunities are emerging. The global rollout of 5G networks presents a transformative opportunity, offering ultra-low latency and high bandwidth capabilities essential for next-generation connected and autonomous driving applications. The increasing proliferation of software-defined vehicles allows for greater flexibility and upgradability of communication systems through over-the-air updates, fostering new business models centered on subscription services. The growing trend of shared mobility and electric vehicles (EVs) also creates new avenues for communication technologies, supporting fleet management, charging infrastructure communication, and enhanced user experiences. These opportunities, when strategically leveraged, can mitigate the existing restraints and propel the market towards sustained expansion, creating a highly competitive landscape where innovation is key to capturing market share and influencing future automotive mobility paradigms.

The Automotive Communication Technology Market is intricately segmented based on various factors such as technology, application, vehicle type, and communication range, providing a granular view of market dynamics and growth opportunities. Understanding these segments is crucial for stakeholders to identify lucrative niches, tailor product development, and formulate effective market entry strategies. Each segment reflects unique technological requirements, end-user demands, and regulatory landscapes, contributing distinctively to the overall market ecosystem. This comprehensive segmentation allows for a precise analysis of competitive advantages and evolving trends across different facets of automotive communication.

The value chain for the Automotive Communication Technology Market is a complex ecosystem involving multiple layers of stakeholders, beginning with upstream activities focused on raw material procurement and fundamental component manufacturing. This upstream segment is dominated by semiconductor manufacturers, sensor producers, and specialized electronic component suppliers who provide the essential building blocks for communication modules and units. These suppliers are critical for providing high-performance processors, transceivers, antennas, and memory chips that are specifically designed to meet the rigorous automotive standards for reliability, temperature tolerance, and electromagnetic compatibility. Innovation at this stage is crucial, as advancements in chip design and material science directly influence the capabilities and cost-effectiveness of subsequent products.

Moving downstream, the value chain progresses through Tier 2 and Tier 1 suppliers who integrate these components into more complex communication modules, electronic control units (ECUs), and telematics control units (TCUs). Tier 1 suppliers, such as continental, Bosch, and Harman, play a pivotal role in developing complete communication systems, integrating hardware with embedded software and ensuring compliance with automotive industry standards and customer specifications. These integrated solutions are then supplied directly to automotive original equipment manufacturers (OEMs) who incorporate them into their vehicles during the manufacturing process. This stage involves significant collaboration between Tier 1 suppliers and OEMs to ensure seamless integration and optimal performance of communication technologies within the vehicle architecture, covering aspects like in-vehicle networks and external connectivity solutions.

The final stages involve distribution channels, which are primarily direct from Tier 1 suppliers to OEMs for new vehicle production. For aftermarket services and software updates, indirect channels through authorized service centers, telematics service providers, and over-the-air (OTA) update platforms become prominent. Direct distribution ensures tight control over product quality and supply chain logistics, fostering strong long-term relationships between suppliers and automakers. Indirect distribution channels, on the other hand, focus on delivering continuous value to end-users through ongoing services, software enhancements, and maintenance, thus extending the lifecycle and utility of the communication technologies. The evolution of software-defined vehicles is further emphasizing these indirect channels, where recurring service revenues and feature upgrades via cloud connectivity are becoming a significant part of the overall market value.

The primary potential customers and end-users of automotive communication technology are diverse, reflecting the broad application spectrum of these solutions across the entire mobility ecosystem. Automotive OEMs represent the largest customer segment, as they integrate these communication systems directly into new vehicles to meet consumer demand for connectivity, safety regulations, and the foundational requirements for autonomous driving. These manufacturers procure a wide range of hardware, software, and services from Tier 1 suppliers to equip their passenger cars and commercial vehicles with advanced communication capabilities, from basic telematics to sophisticated V2X modules. Their purchasing decisions are driven by factors such as technology innovation, cost-effectiveness, reliability, and compliance with industry standards and safety ratings.

Beyond vehicle manufacturing, fleet operators, including logistics companies, ride-sharing services, and public transportation agencies, are significant buyers of automotive communication technologies. They leverage telematics for real-time tracking, remote diagnostics, fuel efficiency monitoring, and driver behavior analysis, enhancing operational efficiency and safety across their commercial vehicle fleets. The growth of connected services and vehicle management platforms tailored for fleet applications underscores their importance as a customer segment. Additionally, government agencies and municipal authorities are increasingly investing in automotive communication technology, particularly for smart city initiatives that involve vehicle-to-infrastructure (V2I) communication, intelligent traffic management systems, and emergency service vehicle coordination, aiming to improve urban mobility and public safety.

Lastly, technology companies specializing in software development, cloud services, and data analytics also represent a key customer group, albeit indirectly, as they partner with OEMs and Tier 1 suppliers to provide the backend infrastructure and application layers that enable connected car services. Consumers, while not direct buyers of the core communication modules, are the ultimate beneficiaries and indirectly drive demand through their preference for connected features, advanced infotainment, and safety systems in their personal vehicles. This consumer demand, filtered through OEMs, is a powerful force shaping product development and innovation in the automotive communication technology market. Furthermore, insurance providers utilize data from telematics and communication systems to offer usage-based insurance, while automotive repair and maintenance shops increasingly rely on remote diagnostics for efficient service delivery.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 10.2 Billion |

| Market Forecast in 2032 | USD 34.5 Billion |

| Growth Rate | CAGR 18.5% |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Qualcomm Technologies Inc., Intel Corporation, NXP Semiconductors N.V., Robert Bosch GmbH, Continental AG, Harman International (A Samsung Company), Denso Corporation, Infineon Technologies AG, STMicroelectronics N.V., Renesas Electronics Corporation, V2X Network (Kapsch TrafficCom AG), Cohda Wireless Pty Ltd., Autotalks Ltd., Huawei Technologies Co. Ltd., Marvell Technology Group Ltd., Broadcom Inc., NVIDIA Corporation, Ericsson AB, Siemens AG, Cisco Systems Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Automotive Communication Technology Market is defined by a rapidly evolving technological landscape, driven by the intense demands of connected and autonomous vehicles for higher bandwidth, lower latency, and superior reliability. At the core are in-vehicle networks, which include traditional protocols like Controller Area Network (CAN) and Local Interconnect Network (LIN) for basic control, alongside higher-bandwidth solutions such as FlexRay for safety-critical applications. However, the burgeoning data volume from advanced sensors and infotainment systems is increasingly pushing automotive Ethernet to the forefront as the backbone for next-generation vehicle architectures. Automotive Ethernet provides the necessary speed and scalability for gigabit-level data transmission, crucial for integrating complex ADAS and autonomous driving modules. This shift represents a significant move towards software-defined vehicle architectures, enabling more flexible and modular system designs.

External communication technologies are equally pivotal, with Vehicle-to-Everything (V2X) communication being a cornerstone. This encompasses both Dedicated Short-Range Communication (DSRC), a Wi-Fi based standard that has seen early deployments, and Cellular Vehicle-to-Everything (C-V2X), which leverages cellular network technology and is rapidly gaining prominence due to its compatibility with the existing and evolving 5G infrastructure. The rollout of 5G networks is a game-changer for the automotive industry, promising ultra-reliable low-latency communication (URLLC), massive machine-type communication (mMTC), and enhanced mobile broadband (eMBB), all of which are essential for fully autonomous driving, real-time traffic management, and rich in-car experiences. These advanced cellular technologies enable vehicles to communicate not just with each other and infrastructure, but also with cloud services and network operators seamlessly.

Further enhancing this landscape are technologies like Bluetooth and Wi-Fi for short-range personal device connectivity and hotspot functionalities within the vehicle. Near Field Communication (NFC) is also finding applications for secure access and payment systems. Beyond these communication protocols, the underlying technology stack includes advanced semiconductor components such as System-on-Chips (SoCs), microcontrollers, and dedicated communication modules from leading players like Qualcomm, NXP, and Intel. Software platforms, including operating systems, middleware, and application programming interfaces (APIs), are crucial for managing and orchestrating these diverse communication flows. Cloud computing and edge computing are increasingly integrated to handle the massive data generated by connected cars, enabling real-time processing, analytics, and over-the-air (OTA) updates, thus driving the intelligence and adaptability of automotive communication systems.

Automotive communication technology refers to the systems and networks that enable vehicles to exchange data internally (between components) and externally (with other vehicles, infrastructure, pedestrians, and the cloud) to enhance safety, efficiency, and infotainment.

V2X (Vehicle-to-Everything) communication allows vehicles to communicate with various entities: V2V (Vehicle-to-Vehicle) for collision avoidance, V2I (Vehicle-to-Infrastructure) for traffic management, V2P (Vehicle-to-Pedestrian) for safety, and V2N (Vehicle-to-Network) for cloud-based services and telematics. It uses technologies like DSRC or C-V2X to transmit crucial real-time data.

The market is driven by increasing demand for connected and autonomous vehicles, stringent government regulations for vehicle safety and emissions, rapid integration of IoT, and growing consumer expectations for advanced in-car experiences and digital services.

Key challenges include robust cybersecurity threats, the high cost of R&D and implementation, ongoing debates and lack of universal standardization for V2X protocols, and the need for significant infrastructure development, particularly for V2I communication in various regions.

5G significantly impacts automotive communication by offering ultra-low latency, high bandwidth, and massive connectivity, which are critical for autonomous driving, real-time V2X interactions, and high-definition in-car infotainment. It enables faster data exchange and more reliable connections, transforming vehicle capabilities.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.