ID : MRU_ 429530 | Date : Nov, 2025 | Pages : 258 | Region : Global | Publisher : MRU

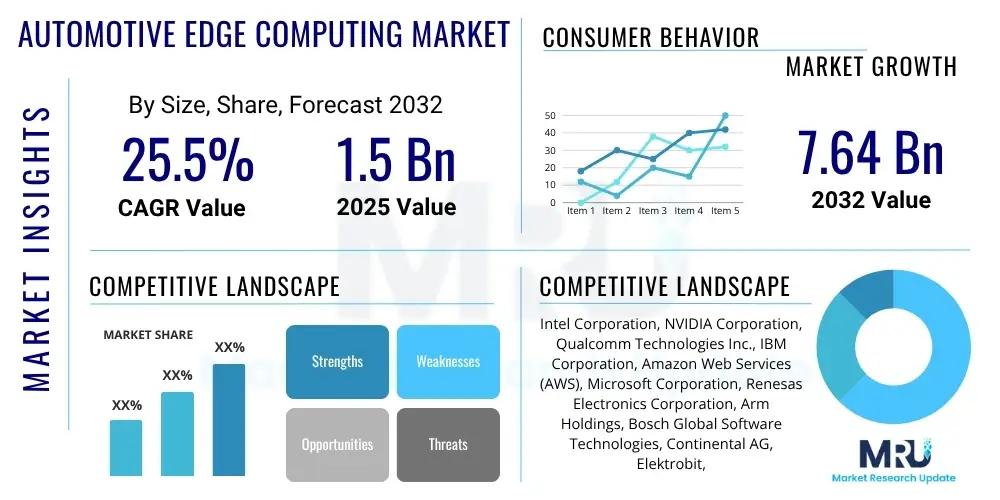

The Automotive Edge Computing Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 25.5% between 2025 and 2032. The market is estimated at $1.5 Billion in 2025 and is projected to reach $7.64 Billion by the end of the forecast period in 2032.

The Automotive Edge Computing Market encompasses the deployment of computing infrastructure and capabilities closer to the data source within vehicles, at roadside units, or in localized automotive data centers. This paradigm shift enables real-time data processing, analysis, and decision-making crucial for advanced automotive applications. The primary objective is to minimize latency, enhance data security, and reduce bandwidth requirements by moving computational tasks away from centralized cloud servers.

This market is driven by the escalating demand for connected cars, autonomous driving systems, and sophisticated in-vehicle infotainment experiences, all of which generate vast amounts of data requiring immediate processing. Edge computing solutions in the automotive sector typically involve specialized hardware and software components designed to handle high-volume, high-velocity data streams from sensors, cameras, and communication modules. These solutions are vital for improving vehicle safety, optimizing performance, and delivering personalized services to occupants.

Major applications of automotive edge computing include advanced driver-assistance systems (ADAS), fully autonomous driving functions, predictive maintenance, vehicle-to-everything (V2X) communication, and personalized in-car experiences. The benefits extend to enhanced operational efficiency, reduced data transmission costs, improved cybersecurity posture through localized data processing, and the ability to execute mission-critical functions with extremely low latency, which is paramount for safety-critical applications like collision avoidance and real-time navigation updates.

The Automotive Edge Computing Market is experiencing robust growth, fueled by transformative shifts within the automotive industry towards electrification, connectivity, and autonomous capabilities. Business trends highlight increasing strategic partnerships between automotive original equipment manufacturers (OEMs), technology providers, and semiconductor companies to develop integrated edge solutions. There is a strong emphasis on creating software-defined vehicles, where edge computing platforms serve as the foundational architecture for flexible feature deployment and over-the-air (OTA) updates, fostering new revenue streams through subscription services and personalized applications.

Geographically, North America and Europe currently lead the market, driven by significant investments in autonomous vehicle research and development, stringent safety regulations, and a mature infrastructure for connected technologies. However, the Asia Pacific region is poised for the fastest growth, propelled by the rapid adoption of electric vehicles, smart city initiatives, and substantial government support for advanced automotive technologies in countries like China, Japan, and South Korea. These regions are becoming hotbeds for innovation in V2X communication and localized data processing.

Segment-wise, the market is witnessing strong traction in both hardware and software components. The demand for high-performance edge processors, sensors, and communication modules is surging, while software platforms for data analytics, AI inference at the edge, and secure operating systems are critical enablers. Applications such as autonomous driving and ADAS represent the largest and fastest-growing segments, given their inherent need for real-time processing and ultra-low latency. The integration of 5G connectivity is further accelerating the deployment of edge computing, enabling more sophisticated and reliable vehicle-to-cloud and vehicle-to-infrastructure interactions.

User inquiries concerning the impact of Artificial Intelligence (AI) on the Automotive Edge Computing Market frequently center on how AI enhances vehicle autonomy, improves safety, and personalizes user experiences. Key themes include the role of AI in real-time sensor data processing for immediate decision-making, the capabilities it introduces for predictive maintenance and advanced diagnostics, and the security implications of deploying AI models at the edge. Users also express interest in understanding the computational demands placed on edge devices by complex AI algorithms and how these challenges are being addressed to ensure both efficiency and reliability in critical automotive functions. There is a clear expectation that AI will be a primary driver for the evolution of edge computing in vehicles.

The Automotive Edge Computing Market is significantly influenced by a confluence of driving forces, inherent restraints, and emerging opportunities. The primary driver is the exponentially increasing volume of data generated by connected vehicles, autonomous systems, and advanced sensors, necessitating localized processing to manage network congestion and ensure real-time responsiveness. The imperative for ultra-low latency in safety-critical applications like collision avoidance and autonomous navigation further accelerates the adoption of edge solutions. Additionally, the proliferation of vehicle-to-everything (V2X) communication technologies and the ongoing advancements in 5G infrastructure are creating a robust ecosystem for edge computing deployment.

Despite strong drivers, several restraints pose challenges to market growth. Significant security and privacy concerns surrounding sensitive vehicle and occupant data processed at the edge require robust encryption and authentication mechanisms, which can add complexity and cost. The lack of standardized protocols and interoperability across different OEM and technology provider platforms complicates widespread adoption and integration. Furthermore, the high initial investment required for developing and deploying sophisticated edge hardware and software, coupled with the inherent complexity of integrating these systems into existing vehicle architectures, can deter smaller players and slow market penetration.

Nevertheless, the market is replete with opportunities driven by technological advancements and evolving consumer demands. The rapid development and deployment of 5G networks are opening new possibilities for high-bandwidth, low-latency communication, enhancing the capabilities of edge computing. The advent of software-defined vehicles is creating a flexible architecture that is highly conducive to edge computing, allowing for dynamic updates and personalized feature delivery. Moreover, the potential for new data monetization models, where insights derived from edge-processed data can be sold to insurance providers, urban planners, or advertising platforms, presents substantial economic opportunities for market participants, fueling further innovation and investment in advanced sensor fusion and predictive analytics at the edge.

The Automotive Edge Computing Market is segmented across various dimensions to provide a detailed understanding of its dynamics and growth prospects. These segmentations allow for a granular analysis of market trends, identifying key areas of demand and technological development. The market can be broadly categorized by component, application, vehicle type, connectivity, and deployment model, each revealing distinct growth patterns and competitive landscapes. Understanding these segments is crucial for stakeholders to tailor strategies and product offerings effectively, addressing specific needs within the diverse automotive ecosystem.

The value chain for the Automotive Edge Computing Market is complex and highly interdependent, involving a multitude of players from hardware manufacturing to end-user application development. At the upstream end, the value chain begins with semiconductor manufacturers and component providers who design and produce the high-performance processors, memory, storage, and communication modules essential for edge devices. This also includes sensor manufacturers providing the eyes and ears for autonomous systems, and operating system developers creating the foundational software for edge platforms. These upstream suppliers are critical for providing the raw computational power and data input capabilities that define the edge ecosystem.

Moving downstream, the value chain involves Tier 1 suppliers who integrate these components into sophisticated edge computing platforms and modules, working closely with automotive OEMs. These Tier 1 companies often develop specialized software stacks, middleware, and AI inference engines optimized for automotive applications. Further down the chain, automotive OEMs are the direct integrators of these edge solutions into vehicles, designing the overall architecture and ensuring seamless functionality across various in-vehicle systems. Additionally, software integrators and application developers play a crucial role in building the final user-facing applications and services that leverage the edge computing infrastructure, from autonomous driving algorithms to personalized infotainment experiences.

Distribution channels for automotive edge computing solutions primarily involve direct sales and partnerships between technology providers and automotive OEMs and Tier 1 suppliers. This direct engagement ensures deep integration and customization required for complex automotive systems. Indirect channels include collaborations with fleet operators, ride-sharing companies, and smart city infrastructure developers who deploy edge computing solutions for specific use cases like traffic management or intelligent logistics. The ecosystem is further supported by cloud service providers who offer hybrid edge-cloud solutions, enabling a balanced approach to data processing and storage, thereby extending the capabilities of in-vehicle edge systems with the scalability and advanced analytics of the cloud.

The primary potential customers and end-users of Automotive Edge Computing solutions are diverse, reflecting the broad applicability of this technology across the automotive ecosystem. Automotive Original Equipment Manufacturers (OEMs) stand as key consumers, directly integrating edge computing capabilities into their next-generation vehicles to enable advanced features like autonomous driving, ADAS, and sophisticated infotainment systems. These manufacturers are increasingly investing in edge technology to build software-defined vehicles that can receive over-the-air updates and offer new digital services, providing a competitive edge in a rapidly evolving market.

Beyond OEMs, Tier 1 suppliers play a critical role, often acting as intermediaries by developing and providing integrated edge computing modules and platforms to vehicle manufacturers. Fleet management companies are also significant potential customers, leveraging edge computing for real-time tracking, predictive maintenance of their vehicle fleets, route optimization, and enhanced driver safety monitoring. Ride-sharing and logistics companies utilize edge solutions to improve operational efficiency, manage their autonomous vehicle fleets, and ensure seamless service delivery, processing vast amounts of data generated during transit at the source for immediate insights and actions.

Furthermore, automotive software developers and technology companies specializing in AI, machine learning, and connectivity solutions represent a growing segment of potential customers. These entities develop the applications and algorithms that run on edge platforms, ranging from advanced perception systems for autonomous vehicles to personalized in-car user interfaces. Smart city planners and infrastructure developers are also emerging customers, employing roadside edge units for traffic management, intelligent parking solutions, and enhancing vehicle-to-infrastructure (V2I) communication, demonstrating the expanding scope of automotive edge computing beyond just the vehicle itself.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $1.5 Billion |

| Market Forecast in 2032 | $7.64 Billion |

| Growth Rate | 25.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Intel Corporation, NVIDIA Corporation, Qualcomm Technologies Inc., IBM Corporation, Amazon Web Services (AWS), Microsoft Corporation, Renesas Electronics Corporation, Arm Holdings, Bosch Global Software Technologies, Continental AG, Elektrobit, Harman International (Samsung), NXP Semiconductors, Visteon Corporation, Siemens AG, HPE (Aruba), Capgemini, Ericsson, Cisco Systems, Google LLC. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Automotive Edge Computing Market is characterized by a sophisticated and rapidly evolving technological landscape, driven by the intense demands of real-time data processing and decision-making in vehicles. Central to this landscape are high-performance processing units, including specialized System-on-Chips (SoCs), Graphics Processing Units (GPUs), Application Specific Integrated Circuits (ASICs), and Field-Programmable Gate Arrays (FPGAs), which are designed to handle complex AI and machine learning algorithms with low power consumption. These processors are crucial for enabling functions like sensor fusion, object detection, and path planning directly within the vehicle, minimizing latency inherent in cloud-based processing.

Communication technologies form another critical pillar, with 5G and Vehicle-to-Everything (V2X) solutions, encompassing Dedicated Short Range Communication (DSRC) and Cellular V2X (C-V2X), being paramount. These technologies provide the high-bandwidth, low-latency connectivity required for vehicles to communicate with each other, roadside infrastructure, and the cloud, facilitating cooperative autonomous driving and smart city applications. Furthermore, robust and secure operating systems, often real-time operating systems (RTOS), are essential for managing computational tasks and ensuring the reliability and safety of automotive edge applications, providing the foundational software layer for complex in-vehicle systems.

The integration of Artificial Intelligence (AI) and Machine Learning (ML) algorithms is a defining characteristic of the modern automotive edge, enabling advanced analytics, predictive capabilities, and enhanced decision-making at the device level. This includes AI for perception, behavioral prediction, and personalized user experiences. Containerization technologies like Docker and Kubernetes are gaining traction for deploying and managing applications on edge devices, offering flexibility and scalability for software updates and deployment. Moreover, robust cybersecurity frameworks, often incorporating blockchain for data integrity and secure firmware updates, are vital to protect the integrity and privacy of data processed at the automotive edge, addressing the inherent vulnerabilities of distributed computing environments.

Automotive Edge Computing involves processing data closer to the source within vehicles or localized roadside units, rather than solely relying on centralized cloud servers. This minimizes latency, enhances security, and enables real-time decision-making crucial for connected and autonomous vehicles.

For autonomous vehicles, edge computing is critical for ultra-low latency decision-making. It enables real-time processing of vast sensor data, allowing immediate responses to dynamic driving conditions, which is paramount for safety and reliable autonomous operation.

5G connectivity significantly enhances automotive edge computing by providing high-bandwidth, ultra-low latency, and highly reliable communication. This facilitates seamless V2X communication, faster data transfer to edge nodes, and enables more sophisticated distributed intelligence for advanced vehicle functions.

Key challenges include ensuring robust cybersecurity for distributed data, developing standardized protocols for interoperability across diverse platforms, managing the high initial investment in hardware and software, and overcoming the complexity of integrating edge solutions into existing vehicle architectures.

Prominent players include technology giants like Intel, NVIDIA, Qualcomm, IBM, AWS, and Microsoft, alongside automotive suppliers such as Bosch, Continental, and NXP Semiconductors, all actively developing and deploying edge solutions for the automotive sector.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.