ID : MRU_ 430397 | Date : Nov, 2025 | Pages : 251 | Region : Global | Publisher : MRU

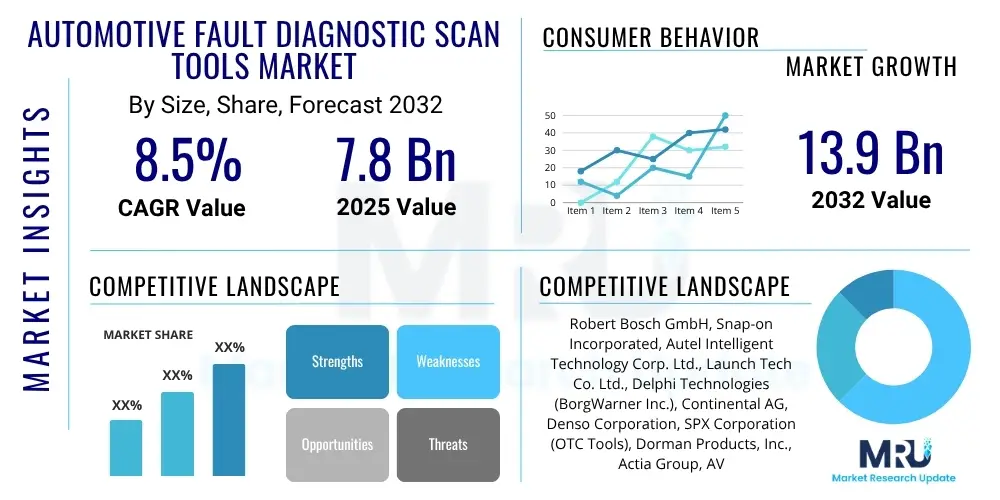

The Automotive Fault Diagnostic Scan Tools Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2032. The market is estimated at USD 7.8 Billion in 2025 and is projected to reach USD 13.9 Billion by the end of the forecast period in 2032.

The Automotive Fault Diagnostic Scan Tools Market encompasses a range of electronic devices and software solutions designed to interface with a vehicle's On-Board Diagnostics (OBD) system to identify, interpret, and clear fault codes, retrieve sensor data, and perform various system tests. These tools are indispensable for modern vehicle maintenance and repair, driven by the increasing complexity of automotive electronics and strict emission regulations. From basic code readers to sophisticated OEM-level diagnostic systems, these tools provide crucial insights into engine, transmission, ABS, airbag, and other critical vehicle systems, enabling precise and efficient troubleshooting. The primary benefit of these tools lies in their ability to minimize diagnostic time, improve repair accuracy, and reduce overall service costs for both professional technicians and individual users.

Major applications of automotive fault diagnostic scan tools span across various end-user segments, including OEM authorized service centers, independent repair workshops, fleet management companies, and even individual vehicle owners for basic checks. Key benefits include enhanced vehicle safety through timely fault identification, improved fuel efficiency by addressing engine management issues, and compliance with environmental standards by managing emission-related faults. The market is significantly driven by several factors, including the continuous evolution of vehicle technology, with more electronic control units (ECUs) and intricate software systems, the rising average age of vehicles on the road requiring more frequent diagnostics, and the growing demand for predictive maintenance solutions. Additionally, stringent government mandates regarding vehicle emissions and safety standards globally necessitate the use of advanced diagnostic equipment to ensure compliance and optimal vehicle performance.

The Automotive Fault Diagnostic Scan Tools Market is experiencing robust growth, primarily fueled by rapid technological advancements in vehicle systems and an escalating demand for efficient and accurate maintenance solutions. Business trends indicate a strong shift towards integrated, cloud-based diagnostic platforms that offer remote access, real-time data analysis, and predictive maintenance capabilities, moving beyond traditional standalone hardware. This evolution is enabling repair shops to enhance operational efficiency and cater to the diagnostic needs of increasingly complex electric and hybrid vehicles, alongside conventional internal combustion engine cars. The market is also witnessing consolidation among key players as they acquire niche technology providers to strengthen their portfolio in advanced diagnostics and telematics.

Regionally, Asia Pacific is emerging as a significant growth hub, propelled by expanding vehicle production, rising disposable incomes, and the proliferation of independent repair workshops in countries like China and India. North America and Europe continue to hold substantial market shares, driven by high vehicle parc, stringent emission regulations, and a mature automotive aftermarket infrastructure, with a particular focus on advanced driver-assistance systems (ADAS) calibration and diagnostics. Segment-wise, the wireless and mobile-based diagnostic tools are gaining considerable traction due to their flexibility, ease of use, and compatibility with various smart devices. The market also observes an increasing penetration of OEM-specific tools in authorized service centers, while independent workshops opt for multi-brand aftermarket solutions offering comprehensive coverage and cost-effectiveness. The demand for diagnostic tools with cybersecurity features is also on the rise, addressing vulnerabilities in connected vehicle systems.

Common user inquiries regarding AI's influence on the Automotive Fault Diagnostic Scan Tools Market often revolve around how artificial intelligence can enhance diagnostic accuracy, automate complex troubleshooting processes, and enable predictive maintenance. Users are keenly interested in understanding if AI will make diagnostics faster and more efficient, reduce the need for highly specialized technicians, and what the implications are for data privacy and security as more vehicle data is processed. There is also a significant expectation that AI will unlock new functionalities, such as self-healing systems and personalized maintenance recommendations, while concerns persist about the initial investment cost for AI-integrated tools and the necessary training for technicians to utilize these advanced capabilities effectively. The integration of AI is seen as a pivotal step towards more intelligent and autonomous vehicle maintenance, promising a future where vehicle issues are identified and even resolved proactively.

The Automotive Fault Diagnostic Scan Tools market is significantly influenced by a dynamic interplay of drivers, restraints, and opportunities that collectively shape its growth trajectory. Key drivers include the ever-increasing technological sophistication of modern vehicles, characterized by a proliferation of electronic control units (ECUs), complex software, and interconnected systems. This complexity necessitates advanced diagnostic capabilities to accurately identify and address issues, driving demand for sophisticated scan tools. Furthermore, stringent global emission standards and safety regulations compel manufacturers and service centers to employ precise diagnostic equipment to ensure vehicles comply with legal requirements and maintain optimal performance. The rising average age of vehicles on the road also contributes to demand, as older vehicles often require more frequent diagnostic checks and repairs, thereby increasing the utility of these tools for both professional workshops and individual owners. The growing adoption of electric vehicles (EVs) and hybrid electric vehicles (HEVs) presents a new frontier for diagnostic tools, requiring specialized software and hardware to manage their unique electrical and battery management systems. Additionally, the expansion of the automotive aftermarket, particularly in emerging economies, fuels the market as more independent workshops seek affordable yet effective diagnostic solutions to compete with OEM service centers. The integration of telematics and connectivity features in modern vehicles also drives the need for diagnostic tools capable of handling remote diagnostics and over-the-air (OTA) updates, enhancing convenience and efficiency.

However, the market also faces notable restraints. The high initial cost of advanced, OEM-level diagnostic tools can be prohibitive for smaller independent workshops, limiting their adoption of cutting-edge technology. This cost factor extends to the perpetual need for software updates and subscription fees, which represent an ongoing expense. Moreover, the rapid pace of technological change in the automotive industry means that diagnostic tools can quickly become obsolete, requiring frequent investment in newer models and training. The shortage of skilled technicians capable of operating and interpreting results from highly advanced diagnostic equipment poses another significant challenge. As vehicles become more complex, the learning curve for these tools steepens, and adequate training infrastructure is not always readily available. Issues related to data security and privacy also present a restraint, as diagnostic tools increasingly connect to vehicle networks and cloud services, raising concerns about unauthorized access to sensitive vehicle and personal information. The fragmentation of diagnostic protocols across different vehicle manufacturers can also complicate tool development and usage, requiring multi-brand tools to support a wide array of communication standards.

Despite these challenges, substantial opportunities exist for market expansion and innovation. The development of cloud-based diagnostic platforms and remote diagnostic services offers immense potential, allowing technicians to diagnose vehicles from off-site locations, improve collaboration, and access real-time technical support and data. The integration of Artificial Intelligence (AI) and Machine Learning (ML) into diagnostic tools is a transformative opportunity, enabling predictive maintenance, automated troubleshooting, and enhanced accuracy, thereby revolutionizing the diagnostic process. The growing market for advanced driver-assistance systems (ADAS) presents a specific opportunity for specialized diagnostic and calibration tools, as these systems become standard in new vehicles. Furthermore, the increasing demand for Do-It-Yourself (DIY) diagnostic tools for basic fault checking offers a distinct segment for simplified, user-friendly, and cost-effective solutions. The expansion of connected car technologies will further integrate diagnostic capabilities directly into vehicle systems, creating opportunities for partnerships between diagnostic tool manufacturers and automotive OEMs. Lastly, the development of diagnostic solutions tailored for specific market niches, such as heavy-duty vehicles, commercial fleets, and specialized vehicle types, represents untapped potential for focused product development and market penetration, addressing unique operational and maintenance requirements.

The Automotive Fault Diagnostic Scan Tools Market is intricately segmented across various dimensions, reflecting the diverse needs of end-users and the broad spectrum of vehicle technologies. These segmentations are crucial for understanding market dynamics, identifying growth pockets, and tailoring product development strategies. The market can be broadly categorized by product type, connectivity, vehicle type, and end-user, each influencing market share and competitive landscape. Analyzing these segments helps stakeholders discern market trends, capitalize on emerging opportunities, and address specific challenges within the automotive diagnostic ecosystem, ensuring that diagnostic solutions remain relevant and effective amidst rapid technological evolution. The evolution of vehicle architectures and diagnostic protocols continually shapes how these segments perform and interact.

The value chain for the Automotive Fault Diagnostic Scan Tools Market begins with upstream activities involving research and development, particularly in sensor technology, microcontrollers, and communication protocols. Key players in this stage include semiconductor manufacturers, software developers specializing in automotive diagnostics, and companies providing advanced data processing capabilities. These entities supply the foundational components and intellectual property necessary for scan tool functionality, focusing on compatibility with various vehicle makes and models, as well as emerging communication standards like CAN FD and Ethernet. The quality and innovation at this stage directly impact the capabilities and reliability of the final diagnostic products, driving continuous investment in new technologies and algorithms to keep pace with automotive advancements. Ensuring compliance with OBD-II and other regional diagnostic standards is critical at this initial phase.

Midstream, the value chain involves the manufacturing and assembly of the diagnostic scan tools. This phase includes sourcing components from upstream suppliers, designing user interfaces, developing proprietary software, and integrating hardware with sophisticated diagnostic algorithms. Manufacturers often specialize in different segments, producing everything from basic code readers to advanced professional scan tools, including OEM-specific equipment. The focus here is on product reliability, user-friendliness, multi-brand compatibility for aftermarket tools, and the robustness of hardware in workshop environments. Quality control and efficient production processes are paramount to meet market demand and competitive pricing strategies. Manufacturers also invest heavily in maintaining up-to-date vehicle databases and software definitions, which are essential for accurate diagnostics across a diverse vehicle parc.

Downstream activities encompass the distribution and sales channels, which are critical for market penetration and customer reach. This includes direct sales to large fleet operators and OEM dealerships, as well as indirect distribution through a network of automotive aftermarket retailers, specialty tool stores, and increasingly, online e-commerce platforms. Direct channels often involve training and dedicated support services, while indirect channels focus on broader availability and competitive pricing. Post-sales support, including technical assistance, software updates, and warranty services, forms an integral part of the downstream value chain, enhancing customer loyalty and brand reputation. The effectiveness of these distribution channels, coupled with strong after-sales service, significantly influences market adoption and customer satisfaction, particularly for professional-grade tools that require continuous support and data updates to remain effective.

The primary end-users and buyers of Automotive Fault Diagnostic Scan Tools are diverse, spanning the entire automotive service and maintenance ecosystem. Original Equipment Manufacturer (OEM) dealerships and their authorized service centers represent a significant customer segment. These entities require manufacturer-specific diagnostic tools that offer comprehensive access to proprietary systems, detailed wiring diagrams, and software reprogramming capabilities, ensuring precise and manufacturer-approved repairs. Their demand often revolves around cutting-edge tools that integrate seamlessly with the latest vehicle models and technologies, including specialized tools for ADAS calibration and electric vehicle diagnostics.

Independent repair workshops form another crucial customer base. These workshops typically seek multi-brand diagnostic tools that can service a wide array of vehicle makes and models, offering a balance between comprehensive functionality and cost-effectiveness. The increasing complexity of vehicles and the need to offer a broad range of services drive their demand for versatile, frequently updated diagnostic solutions. Fleet operators and management companies also constitute a growing segment of potential customers. They utilize diagnostic tools for routine maintenance, proactive fault identification, and optimizing the operational efficiency of their vehicle fleets, prioritizing tools that offer robust data logging, telematics integration, and capabilities for heavy-duty commercial vehicles. Additionally, vehicle inspection centers and government agencies also procure these tools for compliance checks and emission testing.

A burgeoning segment comprises Do-It-Yourself (DIY) enthusiasts and individual vehicle owners. While their needs are generally less sophisticated than professional workshops, this group seeks user-friendly, affordable diagnostic tools, primarily basic code readers or mobile-based apps, to perform preliminary fault checks, monitor vehicle health, and avoid costly service visits for minor issues. This segment is driven by a desire for greater control over vehicle maintenance and cost savings. The varied requirements across these customer groups underscore the need for a diverse product offering within the Automotive Fault Diagnostic Scan Tools Market, ranging from highly specialized professional-grade systems to accessible consumer-oriented devices, each tailored to specific operational demands and technical proficiencies.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 7.8 Billion |

| Market Forecast in 2032 | USD 13.9 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Robert Bosch GmbH, Snap-on Incorporated, Autel Intelligent Technology Corp. Ltd., Launch Tech Co. Ltd., Delphi Technologies (BorgWarner Inc.), Continental AG, Denso Corporation, SPX Corporation (OTC Tools), Dorman Products, Inc., Actia Group, AVL List GmbH, Pico Technology, TEXA S.p.A., Innova Electronics Corporation, Drew Technologies (Opus IVS), Siemens AG, Hella Gutmann Solutions, Hikvision Digital Technology Co., Ltd. (via Autodatalab), Rotunda (Ford Motor Company), XToolTech. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Automotive Fault Diagnostic Scan Tools Market is underpinned by a rapidly evolving technological landscape, driven by advancements in vehicle electronics and communication protocols. Central to this landscape is the widespread adoption of On-Board Diagnostics II (OBD-II) standards, which provide a standardized interface for accessing vehicle data, enabling universal compatibility for basic diagnostics across different manufacturers. Beyond OBD-II, advanced diagnostic tools leverage proprietary manufacturer-specific protocols to delve deeper into complex vehicle systems, often requiring specialized software and hardware. The evolution of vehicle communication networks, such as Controller Area Network (CAN bus), FlexRay, and increasingly Automotive Ethernet, mandates diagnostic tools capable of communicating effectively across these high-speed and complex architectures, supporting higher data throughput and sophisticated fault detection.

Connectivity solutions are another critical technological pillar. Wireless communication technologies like Bluetooth and Wi-Fi are integrated into scan tools to enable remote diagnostics, improve mobility within workshops, and facilitate data transfer to other devices or cloud platforms. The rise of cellular connectivity (4G/5G) further enhances remote diagnostic capabilities, allowing for over-the-air (OTA) software updates and real-time vehicle health monitoring from virtually anywhere. Cloud computing plays an increasingly vital role, providing centralized data storage, enabling collaborative diagnostics, offering access to vast databases of technical information, and supporting subscription-based software services. This shift to cloud-based solutions enhances scalability, provides constant access to the latest vehicle data, and facilitates seamless integration with other workshop management systems.

Furthermore, the integration of Artificial Intelligence (AI) and Machine Learning (ML) algorithms is transforming diagnostic capabilities. These technologies enable predictive maintenance by analyzing historical data and real-time sensor inputs to anticipate potential failures, significantly improving diagnostic accuracy and efficiency. AI-powered tools can also provide intelligent guided diagnostics, reducing the reliance on extensive technician knowledge for complex issues. Augmented Reality (AR) is beginning to find applications, overlaying diagnostic information onto vehicle components, simplifying complex repairs. Cybersecurity technologies are also paramount, as diagnostic tools interact with sensitive vehicle networks, requiring robust encryption and authentication mechanisms to protect against unauthorized access and data breaches. These technological advancements collectively contribute to making diagnostic processes more accurate, efficient, and accessible, driving continuous innovation in the automotive aftermarket.

An automotive fault diagnostic scan tool is an electronic device that interfaces with a vehicle's On-Board Diagnostics (OBD) system to read, interpret, and clear diagnostic trouble codes (DTCs), display real-time sensor data, and perform various system tests to identify and troubleshoot vehicle malfunctions.

Modern vehicles are equipped with complex electronic control units (ECUs) and intricate software systems that govern various functions. Scan tools are essential because they provide the necessary interface to communicate with these systems, accurately identify faults, and perform required maintenance, which is impossible with traditional mechanical methods.

The main types include handheld scan tools (portable and user-friendly), PC-based systems (offering advanced software and larger displays), and mobile-based tools (apps for smartphones/tablets often paired with a Bluetooth OBD adapter), each catering to different levels of diagnostic needs and budgets.

AI is transforming diagnostic tools by enabling predictive maintenance, enhancing fault detection accuracy through advanced data analysis, automating troubleshooting processes, and facilitating remote diagnostics. It helps identify potential issues before they become critical failures and streamlines repair workflows.

Key considerations include vehicle compatibility (make, model, year), required functionality (basic code reading vs. advanced bidirectional controls), connectivity options (wired/wireless), software update frequency, ease of use, technical support availability, and budget. Professionals often prioritize comprehensive coverage and advanced features.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.