ID : MRU_ 428526 | Date : Oct, 2025 | Pages : 253 | Region : Global | Publisher : MRU

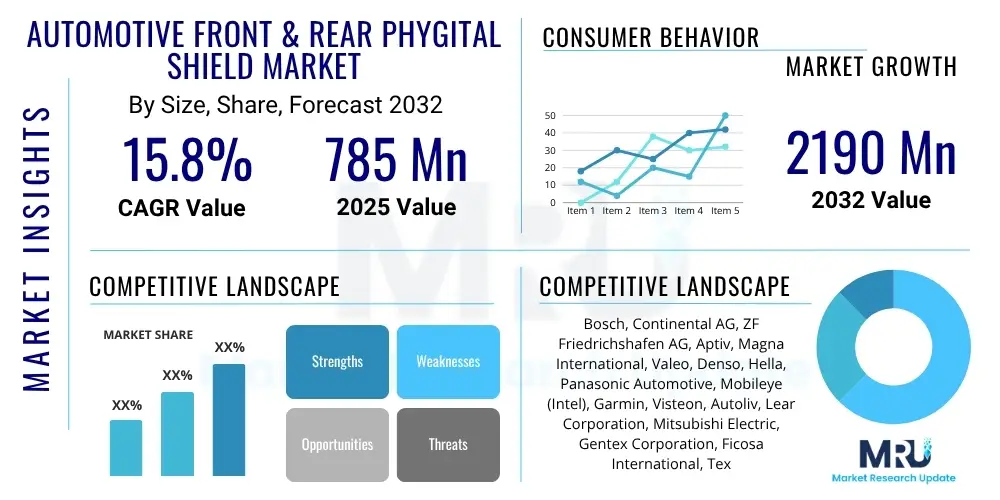

The Automotive Front & Rear Phygital Shield Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.8% between 2025 and 2032. The market is estimated at $785 million in 2025 and is projected to reach $2190 million by the end of the forecast period in 2032.

The Automotive Front & Rear Phygital Shield Market represents a significant evolution in vehicular safety, aesthetics, and connectivity. Phygital shields are advanced automotive components that seamlessly integrate physical protective structures with digital functionalities. These systems move beyond conventional bumpers and panels, incorporating a sophisticated array of sensors, communication modules, and display technologies to provide real-time information, enhanced safety features, and a more interactive driving experience. This convergence of physical resilience and digital intelligence defines the core offering of this nascent yet rapidly expanding market, addressing the growing consumer and regulatory demand for smarter, safer, and more connected vehicles. The market is characterized by continuous innovation aimed at transforming passive physical barriers into active, intelligent interfaces that contribute to both vehicle performance and passenger well-being.

The product description highlights a multifaceted system designed to protect occupants and pedestrians while simultaneously augmenting driver awareness and vehicle connectivity. Major applications span across passenger vehicles, commercial vehicles, and the burgeoning segment of autonomous vehicles, where these shields serve as crucial interfaces for environmental perception and interaction. Key benefits include superior crash protection, proactive hazard detection through integrated sensors, enhanced vehicle-to-everything (V2X) communication capabilities, and the potential for customized user experiences through embedded displays. These shields can dynamically display warnings, navigation cues, or even communicate with external infrastructure and other vehicles, making them indispensable components in the ecosystem of smart mobility solutions. Their adaptive nature allows for functionalities such as pedestrian detection, blind-spot monitoring, and even dynamic lighting for improved visibility.

The market's growth is primarily driven by several powerful factors. Foremost among these is the escalating integration of Advanced Driver-Assistance Systems (ADAS) into vehicles, which heavily relies on the precise data collection and processing capabilities offered by phygital shields. Furthermore, increasingly stringent global automotive safety regulations are compelling manufacturers to adopt more sophisticated protective and preventative technologies. The rising consumer demand for connected car features, infotainment, and personalized driving experiences also fuels innovation in this sector. Finally, the rapid advancements in sensor technology, artificial intelligence, and communication protocols are enabling the development of more capable and cost-effective phygital shield solutions, making them increasingly viable for mass market adoption. These combined forces are propelling the Automotive Front & Rear Phygital Shield Market into a period of robust expansion and technological diversification.

The Automotive Front & Rear Phygital Shield Market is experiencing transformative business trends characterized by intense competition, strategic collaborations, and a strong emphasis on research and development. Key automotive suppliers and technology giants are forming partnerships to pool expertise in materials science, sensor technology, and AI integration, aiming to create more holistic and advanced solutions. There is a discernible shift towards modular and customizable phygital shield designs, allowing OEMs greater flexibility in vehicle integration and feature differentiation. Furthermore, companies are investing heavily in intellectual property related to sensor fusion, data analytics, and secure communication protocols, recognizing these as critical differentiators in a rapidly evolving landscape. The focus is not only on hardware innovation but also on the software and algorithms that enable the intelligent functionalities of these shields, leading to a rise in demand for specialized software development capabilities within the automotive supply chain. This strategic landscape suggests a future where integrated solutions and seamless user experiences will be paramount for market leadership.

Regional trends significantly influence the market's trajectory, with distinct growth patterns emerging across continents. Asia Pacific, particularly countries like China, Japan, and South Korea, is projected to be a dominant force, driven by rapid urbanization, increasing automotive production, and government initiatives promoting smart infrastructure and electric vehicles. Europe, with its stringent safety regulations and a strong preference for premium and luxury vehicles, is a key market for advanced phygital shield adoption. North America continues to be a hub for technological innovation and early adoption, propelled by a strong consumer base for high-tech vehicles and substantial investments in autonomous driving technologies. Latin America and the Middle East & Africa regions, while currently smaller, are demonstrating promising growth potential fueled by rising disposable incomes, improving road infrastructure, and a growing awareness of vehicular safety. These regional dynamics necessitate tailored market entry and growth strategies, considering local regulatory environments, consumer preferences, and technological readiness.

Segment trends within the Automotive Front & Rear Phygital Shield Market reveal a clear progression towards more sophisticated and integrated systems. Initially, premium and luxury vehicle segments were the primary adopters, leveraging these shields for advanced ADAS features and aesthetic differentiation. However, as costs decrease and technology matures, the adoption is expanding into mid-range vehicle segments, democratizing access to enhanced safety and connectivity. The "by component" segment highlights a strong growth in advanced sensor suites, powerful processors capable of real-time AI inference, and robust V2X communication modules, which are essential for true phygital functionality. Furthermore, there is an increasing demand for sustainable and lightweight protective materials that do not compromise safety but contribute to vehicle efficiency. The aftermarket segment is also showing growth, as consumers seek to upgrade older vehicles with advanced safety and connectivity features, presenting a significant opportunity for specialized product offerings and installation services. This diversification across vehicle types and component demands underscores the broad applicability and expanding utility of phygital shield technology.

Users frequently inquire about how Artificial Intelligence will fundamentally transform automotive phygital shields, focusing on questions like whether AI can prevent accidents, how data privacy will be maintained with advanced sensors, and the potential for personalized in-car experiences. Common themes revolve around AI's ability to enhance predictive safety, process vast amounts of sensor data efficiently, and create truly intelligent, responsive vehicle interfaces. There are significant concerns regarding the reliability of AI systems in critical safety situations, the ethical implications of autonomous decision-making, and the cybersecurity vulnerabilities associated with highly connected components. Users also express expectations for AI to deliver features like advanced driver monitoring, adaptive lighting, proactive pedestrian protection, and seamless integration with smart city infrastructure, indicating a strong desire for more intuitive, safer, and highly personalized mobility solutions. The overarching sentiment is that AI is not just an additive feature but a foundational technology poised to redefine the capabilities and utility of phygital shields, shifting them from passive protection to active, intelligent guardians and interactive platforms within the vehicle ecosystem.

The Automotive Front & Rear Phygital Shield Market is profoundly shaped by a confluence of drivers, restraints, opportunities, and broader impact forces that dictate its growth trajectory and technological evolution. Among the most significant drivers is the increasing global emphasis on vehicle safety, manifested through stringent government regulations and rising consumer safety awareness. These factors compel automotive manufacturers to integrate advanced protective and preventative systems like phygital shields, which offer superior crash mitigation and active safety features. The rapid proliferation of Advanced Driver-Assistance Systems (ADAS) and the accelerating development of autonomous driving technologies further fuel market expansion, as phygital shields serve as crucial platforms for housing and integrating the myriad sensors and communication modules required for these sophisticated systems. Moreover, growing consumer demand for connected car features, enhanced in-car experiences, and personalized vehicle functionalities significantly contributes to the adoption of these advanced shields, positioning them as essential components in the smart mobility ecosystem.

Despite the strong growth drivers, the market faces several notable restraints. The high initial cost associated with the research, development, and manufacturing of these technologically advanced components poses a significant barrier to widespread adoption, particularly in cost-sensitive vehicle segments. The inherent technical complexity of integrating diverse physical and digital systems—including multiple sensor types, AI processors, communication modules, and display technologies—presents substantial engineering challenges. This complexity also extends to ensuring the seamless interoperability of various components from different suppliers. Furthermore, the reliance on advanced connectivity and data processing capabilities introduces significant cybersecurity risks, necessitating robust protection against potential breaches and unauthorized access. Consumer data privacy concerns related to the collection and transmission of vehicular and environmental data also present a restraint, requiring manufacturers to develop transparent and secure data handling protocols. Overcoming these hurdles will be crucial for the sustained growth and broader market penetration of phygital shields.

Opportunities within the Automotive Front & Rear Phygital Shield Market are abundant and diverse, promising continued innovation and market expansion. The emergence of Artificial Intelligence and Machine Learning offers vast potential for predictive analytics, enabling shields to anticipate road hazards, driver fatigue, and even vehicle component failures with unprecedented accuracy. This capability can transform reactive safety into proactive prevention. Expanding the application of phygital shields beyond passenger vehicles to commercial fleets, public transportation, and specialized autonomous shuttles represents a significant untapped market segment. The development of customizable and modular phygital shield solutions allows for greater design flexibility for OEMs and personalized upgrades for consumers, enhancing market appeal. Additionally, the integration of these shields with burgeoning smart city infrastructure and vehicle-to-everything (V2X) communication technologies presents opportunities for creating highly cooperative and efficient urban mobility systems. These opportunities, coupled with ongoing advancements in materials science for enhanced durability and lighter weight, are expected to drive substantial long-term growth and diversification for the market.

The Automotive Front & Rear Phygital Shield Market is segmented across various dimensions, including type, component, vehicle type, and sales channel, providing a comprehensive view of its intricate structure. This segmentation helps to understand the diverse applications, technological requirements, and distribution strategies prevalent in the market. Each segment highlights specific market dynamics, influencing product development, target audiences, and competitive strategies. Understanding these distinct categories is crucial for stakeholders to identify key growth areas, address specific consumer needs, and navigate the complex supply chain of the automotive industry. The market's multifaceted nature allows for specialized innovations and tailored solutions, catering to a broad spectrum of automotive requirements from basic safety enhancements to advanced autonomous functionalities.

The value chain for the Automotive Front & Rear Phygital Shield Market is a complex ecosystem, beginning with upstream activities that involve the sourcing and manufacturing of critical raw materials and components. This segment includes suppliers of advanced polymers, composites, and high-strength metals for the physical shield structure, alongside specialized manufacturers of electronic components. Key upstream players also encompass developers of sophisticated sensors such as radar, lidar, cameras, and ultrasonic systems, which form the eyes and ears of the phygital shield. Furthermore, semiconductor companies providing AI processors, microcontrollers, and communication chips (for V2X, 5G capabilities) are integral to this stage. Software developers specializing in AI algorithms, sensor fusion, data analytics, and embedded operating systems also contribute significantly, as the intelligence layer is as crucial as the physical layer. The innovation and quality at this upstream stage directly influence the performance, reliability, and cost-effectiveness of the final phygital shield product, highlighting the importance of strong supplier relationships and rigorous quality control measures.

Midstream activities primarily involve the integration and assembly of these diverse components into a cohesive phygital shield system. This stage is dominated by Tier 1 and Tier 2 automotive suppliers who specialize in designing, manufacturing, and integrating complex modules. These companies often possess expertise in mechatronics, combining mechanical, electronic, and software engineering to create functional and robust shield systems. Their processes include meticulous assembly, calibration of sensors, programming of embedded software, and rigorous testing to ensure compliance with stringent automotive safety standards and performance specifications. This stage also involves the development of proprietary algorithms for enhanced functionality, user interface design for integrated displays, and ensuring seamless communication between different shield components and the vehicle's central electronic control unit (ECU). The efficiency and precision of these integration processes are paramount for delivering high-quality, reliable, and intelligent phygital shields to the automotive industry.

Downstream analysis focuses on the distribution and end-user engagement channels. The primary distribution channel for phygital shields is directly to Original Equipment Manufacturers (OEMs). Automotive manufacturers integrate these advanced shields into their vehicle production lines as part of their factory-installed safety and connectivity packages. This direct channel requires strong technical collaboration between the phygital shield suppliers and the OEMs during the vehicle design and development phases. The indirect channel predominantly serves the aftermarket, where consumers seek to upgrade their existing vehicles with advanced phygital shield features or replace damaged components. This involves a network of authorized distributors, specialized automotive parts retailers, and professional installation centers. Marketing and sales strategies for the aftermarket often emphasize the benefits of enhanced safety, advanced technology, and improved vehicle value. Both direct and indirect channels play crucial roles in market penetration, with the OEM channel driving initial adoption and integration into new vehicle models, while the aftermarket provides opportunities for incremental growth and broader consumer access to these evolving technologies.

The primary potential customers and end-users of Automotive Front & Rear Phygital Shields are diverse, reflecting the broad applicability of these advanced systems. Foremost among these are Original Equipment Manufacturers (OEMs) of passenger vehicles, ranging from economy to luxury segments, who integrate these shields as fundamental components of their new vehicle designs to meet safety regulations, enhance ADAS capabilities, and differentiate their offerings. Commercial vehicle manufacturers, including those producing light and heavy trucks, buses, and specialized vehicles, represent another significant customer base, as these operators increasingly demand enhanced safety and operational efficiency through connected technologies. Furthermore, the burgeoning sector of autonomous vehicle developers and fleet operators for robotic taxis and shuttle services are critical end-users, relying on phygital shields for precise environmental perception and interaction in driverless operations. Finally, aftermarket consumers, seeking to upgrade their existing vehicles with state-of-the-art safety, connectivity, and intelligent features, also constitute a growing segment of potential buyers, driving demand for innovative and accessible retrofit solutions. Each of these customer groups has unique requirements, influencing the design, functionality, and pricing strategies within the market.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $785 Million |

| Market Forecast in 2032 | $2190 Million |

| Growth Rate | 15.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Bosch, Continental AG, ZF Friedrichshafen AG, Aptiv, Magna International, Valeo, Denso, Hella, Panasonic Automotive, Mobileye (Intel), Garmin, Visteon, Autoliv, Lear Corporation, Mitsubishi Electric, Gentex Corporation, Ficosa International, Texas Instruments, Infineon Technologies, STMicroelectronics |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Automotive Front & Rear Phygital Shield Market is defined by a dynamic and rapidly evolving technology landscape, where continuous innovation in various fields converges to create sophisticated intelligent systems. At the core of these shields is advanced sensor fusion technology, integrating data from multiple modalities such as high-resolution radar, lidar, camera systems, and ultrasonic sensors. This fusion provides a comprehensive and highly accurate 360-degree environmental perception, crucial for ADAS functionalities and autonomous driving. Developments in micro-electromechanical systems (MEMS) have led to smaller, more robust, and more cost-effective sensors, enabling their widespread integration into vehicle body panels. Furthermore, the advent of high-performance, low-power AI processors and specialized neural network chips is essential for real-time data processing, object detection, classification, and predictive analytics directly at the edge, minimizing latency and maximizing responsiveness. These computing advancements are foundational to unlocking the full intelligent capabilities of phygital shields, enabling them to make instantaneous decisions and provide critical insights to the vehicle's central systems.

Another pivotal technological area involves advanced display technologies and human-machine interface (HMI) innovations. Phygital shields are increasingly incorporating transparent displays, augmented reality (AR) heads-up displays (HUDs), and dynamic LED matrices that can communicate information directly to drivers, pedestrians, and other vehicles. These displays can project critical warnings, navigation cues, or even show the vehicle's intentions (e.g., turning, braking) to external observers. Coupled with these visual interfaces are haptic feedback systems and acoustic cues that provide multi-sensory warnings and interactions, enhancing driver awareness without visual distraction. Beyond visual and haptic feedback, the integration of advanced communication modules is paramount. Vehicle-to-Everything (V2X) communication, including V2V (vehicle-to-vehicle), V2I (vehicle-to-infrastructure), and V2P (vehicle-to-pedestrian), powered by 5G connectivity, enables shields to exchange real-time data with their surroundings, anticipating hazards beyond the line of sight and facilitating cooperative driving scenarios. These communication capabilities transform shields into active participants in the broader smart mobility ecosystem.

Material science and cybersecurity are also critical components of the phygital shield technology landscape. Innovations in lightweight, high-strength composite materials and advanced polymers are allowing for the creation of shields that offer superior crash protection while reducing overall vehicle weight, contributing to fuel efficiency and extended range for electric vehicles. These materials also offer greater design flexibility, enabling the seamless integration of electronic components without compromising structural integrity. Equally important is the development of robust cybersecurity measures. With phygital shields becoming integral data collection and communication hubs, they represent potential attack vectors for malicious actors. Therefore, the implementation of secure boot processes, encrypted communication protocols, intrusion detection systems, and over-the-air (OTA) update capabilities with secure authentication are essential to protect vehicle systems from cyber threats. The continuous evolution in these diverse technological domains ensures that automotive front and rear phygital shields remain at the forefront of automotive innovation, offering increasingly sophisticated safety, connectivity, and user experience enhancements for the modern vehicle.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.