ID : MRU_ 428860 | Date : Oct, 2025 | Pages : 242 | Region : Global | Publisher : MRU

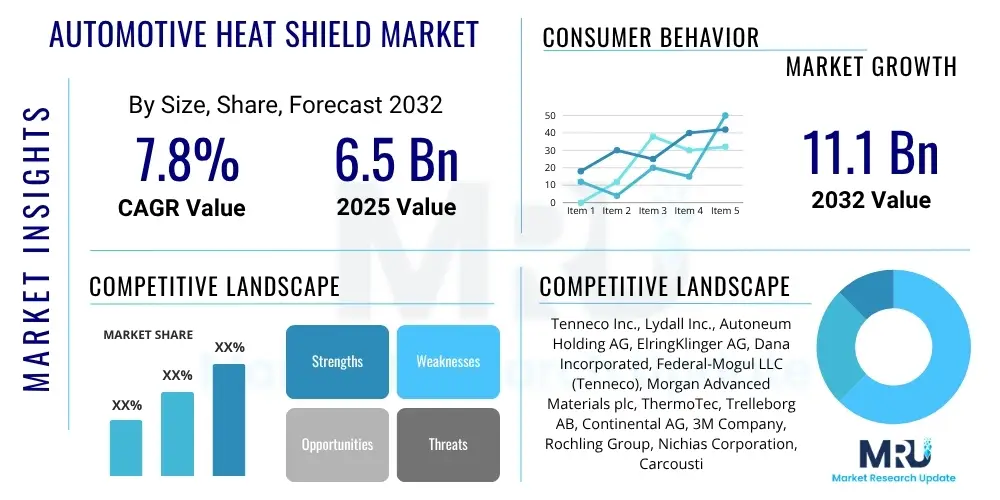

The Automotive Heat Shield Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2032. The market is estimated at USD 6.5 Billion in 2025 and is projected to reach USD 11.1 Billion by the end of the forecast period in 2032.

The Automotive Heat Shield Market encompasses a critical segment within the automotive industry, focused on components designed to protect various vehicle parts from excessive heat generated by the engine, exhaust system, brakes, and other high-temperature areas. These shields play an indispensable role in ensuring the operational longevity of sensitive components, maintaining cabin comfort for occupants, and enhancing overall vehicle safety. The fundamental principle behind automotive heat shields is to mitigate thermal transfer through reflection, absorption, or dissipation of heat, thereby preventing heat-related damage to nearby components and reducing fire risks. As modern vehicles incorporate more intricate electronic systems and operate under more demanding conditions, the need for effective thermal management solutions has become increasingly paramount across all vehicle types.

Automotive heat shields are typically fabricated from a diverse range of materials, including various grades of metallic alloys such as aluminum and stainless steel, as well as non-metallic compounds like fiberglass, ceramics, and advanced composite materials. Each material offers distinct advantages in terms of thermal resistance, weight, durability, and cost-effectiveness, allowing manufacturers to select optimal solutions based on specific application requirements. Major applications of these heat shields include protecting the engine compartment, exhaust system components such catalytic converters and mufflers, turbochargers, fuel lines, wiring harnesses, brake systems, and increasingly, battery packs in electric vehicles. Their ability to manage thermal energy efficiently directly contributes to improved component lifespan, reduced maintenance costs, and enhanced vehicle performance by preventing heat-induced degradation.

The market's growth is primarily driven by several key factors, including the global increase in automotive production, particularly in emerging economies, and the continuous evolution of stricter emission regulations worldwide. These regulations often necessitate higher operating temperatures for exhaust after-treatment systems, consequently increasing the demand for robust thermal management solutions. Furthermore, the growing trend towards lightweight vehicle construction to improve fuel efficiency and reduce carbon emissions, coupled with the rapid expansion of the electric vehicle (EV) segment, significantly propels the demand for innovative heat shield technologies. Heat shields in EVs are crucial for maintaining optimal battery operating temperatures and protecting power electronics, showcasing a broader range of applications beyond traditional internal combustion engine vehicles and underscoring their critical role in future automotive design and engineering.

The Automotive Heat Shield Market is experiencing robust growth, driven by an confluence of technological advancements, evolving regulatory landscapes, and shifting consumer preferences. Key business trends indicate a strong emphasis on lightweight and high-performance materials, multi-layer insulation designs, and integrated thermal management solutions. Manufacturers are increasingly investing in research and development to create heat shields that offer superior thermal efficiency while contributing to overall vehicle weight reduction, aligning with global efforts to improve fuel economy and reduce emissions. The market is witnessing a surge in strategic partnerships and collaborations among raw material suppliers, component manufacturers, and original equipment manufacturers (OEMs) to innovate and scale production of advanced heat shield technologies. Furthermore, the burgeoning demand for electric vehicles is profoundly reshaping market dynamics, introducing new requirements for battery thermal management and protection of sensitive power electronics, thus creating novel growth avenues for specialized heat shield products.

Regionally, the Asia Pacific market stands out as a dominant force, primarily fueled by high automotive production volumes in countries like China, India, and Japan, coupled with rapid urbanization and increasing disposable incomes driving vehicle sales. Europe also presents a significant market share, characterized by stringent environmental regulations and a strong focus on premium and luxury vehicle segments, which often incorporate advanced thermal management systems. North America demonstrates consistent growth, largely attributed to steady demand for light commercial vehicles, SUVs, and a rapidly expanding electric vehicle ecosystem. Emerging economies in Latin America, the Middle East, and Africa are progressively contributing to market expansion as their automotive industries mature and vehicle parc increases, although these regions are typically more price-sensitive and focused on foundational heat shield applications.

Segmentation trends within the market highlight the increasing adoption of non-metallic and composite materials over traditional metallic shields, driven by their superior weight-to-performance ratio and enhanced thermal insulation properties. By product type, multi-layer heat shields are gaining traction due to their ability to offer multi-faceted thermal protection in complex environments. Application-wise, while engine compartment and exhaust system protection remain foundational, the battery heat shield segment for electric vehicles is projected to witness the fastest growth, underscoring the transformative impact of electrification on thermal management requirements. Vehicle type analysis reveals passenger cars as the largest segment, but commercial vehicles and particularly electric vehicles are exhibiting accelerated growth rates, necessitating customized and more sophisticated heat shield designs to meet their unique operational demands and safety standards.

Common user questions regarding the impact of Artificial Intelligence on the Automotive Heat Shield Market typically revolve around how AI can enhance design, optimize material selection, improve manufacturing processes, and contribute to the predictive maintenance of thermal management systems. Users frequently inquire about the potential for AI-driven simulations to create more efficient heat shield geometries, the role of machine learning in discovering novel heat-resistant materials, and the application of AI in identifying and rectifying manufacturing defects to ensure product quality. There is also significant interest in AI's capacity to integrate heat shield performance data with broader vehicle telematics for real-time thermal management adjustments and proactive fault detection, particularly in complex electric vehicle architectures. These questions underscore a collective expectation that AI will lead to more intelligent, adaptive, and performance-optimized thermal solutions, ultimately enhancing vehicle safety, longevity, and efficiency.

The Automotive Heat Shield Market is significantly shaped by a dynamic interplay of various Drivers, Restraints, and Opportunities, which collectively constitute its Impact Forces. Primary drivers propelling market expansion include the unwavering global growth in automotive production, driven by increasing demand for both passenger and commercial vehicles, particularly in developing economies. Alongside this, the continuous tightening of global emission standards, such as Euro 7 and CAFE regulations, mandates higher operating temperatures for exhaust systems to efficiently reduce pollutants, thereby necessitating more robust and effective thermal management solutions. Furthermore, the escalating consumer and regulatory demand for lighter, more fuel-efficient vehicles pushes manufacturers to adopt advanced, lightweight heat shield materials and designs. Crucially, the rapid electrification of the automotive industry introduces a new imperative: the stringent thermal management requirements for electric vehicle battery packs and power electronics, which are highly sensitive to temperature fluctuations and require sophisticated heat shielding to ensure safety, performance, and longevity.

Conversely, several significant restraints challenge the market's growth trajectory. The volatility of raw material prices, particularly for specialized metals and composites, presents a constant economic challenge for manufacturers, impacting production costs and ultimately influencing the final pricing of heat shield components. The inherent complexity of designing and manufacturing heat shields that must withstand extreme temperatures, vibrations, and corrosive environments while meeting stringent dimensional and weight specifications also acts as a restraint, requiring significant capital investment in advanced manufacturing techniques and skilled labor. Moreover, the integration of these advanced thermal management systems into increasingly compact and complex vehicle architectures poses substantial engineering challenges, demanding sophisticated design and testing processes that can prolong development cycles and increase costs for automotive OEMs and their suppliers.

Despite these challenges, substantial opportunities exist within the Automotive Heat Shield Market that promise future expansion and innovation. The ongoing development of advanced materials, including novel ceramics, multi-layer composites, and smart materials with active thermal regulation capabilities, represents a key growth avenue. These materials offer enhanced performance characteristics and can open up new application possibilities. The accelerating global adoption of electric vehicles, hybrid vehicles, and hydrogen fuel cell vehicles creates a rapidly expanding market for specialized thermal management solutions, particularly for battery protection, motor cooling, and power electronics insulation, which are critical for EV safety and performance. Moreover, the increasing focus on passenger comfort and safety, coupled with the rising demand for premium and luxury vehicle segments that prioritize advanced noise, vibration, and harshness (NVH) reduction alongside thermal management, continues to fuel innovation and market demand for sophisticated heat shield technologies, ensuring a robust outlook for the industry.

The Automotive Heat Shield Market is comprehensively segmented across various dimensions to provide a granular understanding of its dynamics and growth trajectories. These segmentations allow for a detailed analysis of product types, material compositions, end-use applications, and vehicle categories, revealing specific market niches and potential areas for innovation and investment. The market's diverse nature reflects the wide range of thermal protection needs across different vehicle components and types, from traditional internal combustion engines to emerging electric powertrains. Understanding these segments is crucial for manufacturers to tailor their offerings, for suppliers to identify key demand centers, and for investors to pinpoint high-growth opportunities within the rapidly evolving automotive landscape.

The value chain for the Automotive Heat Shield Market is a complex and interconnected network of activities that spans from raw material extraction to the final integration into a vehicle, involving multiple tiers of suppliers and specialized processes. At the upstream stage, the market relies heavily on a diverse range of raw material suppliers providing crucial inputs such as various grades of metallic sheets (e.g., aluminum, stainless steel, mild steel), non-metallic fibers (e.g., fiberglass, ceramic fibers, basalt fibers), specialized coatings, adhesives, and composite resins. These suppliers are foundational, as the quality and characteristics of their materials directly dictate the thermal performance, durability, and cost-effectiveness of the final heat shield product. Innovation in advanced materials at this stage, such as ultra-lightweight alloys or high-temperature resistant composites, can significantly influence the entire value chain.

Moving downstream, the midstream segment of the value chain involves the transformation of these raw materials into finished or semi-finished heat shield components by specialized manufacturers. This stage encompasses a variety of complex manufacturing processes, including stamping, deep drawing, hydroforming, vacuum forming, laser cutting, welding, and advanced bonding techniques. These manufacturers, often Tier 1 or Tier 2 automotive suppliers, possess specialized expertise in thermal management engineering, material science, and precision fabrication. They are responsible for designing heat shields that meet stringent OEM specifications for thermal performance, noise reduction, weight, and dimensional accuracy, often leveraging advanced simulation software for optimal design and performance validation. Their output can range from simple single-layer shields to intricate multi-layer systems tailored for specific vehicle architectures.

The distribution channel plays a critical role in connecting the heat shield manufacturers with the final automotive integrators and the aftermarket. Direct distribution channels involve heat shield manufacturers supplying components directly to Original Equipment Manufacturers (OEMs) for integration into new vehicle assembly lines. This relationship is often characterized by long-term contracts, stringent quality control, and just-in-time delivery systems. Indirect distribution channels primarily cater to the aftermarket segment, where heat shields are sold through a network of independent distributors, wholesalers, and retail outlets for replacement or upgrade purposes. These channels also include supplies to Tier 1 automotive suppliers who then integrate the heat shields into larger sub-assemblies before delivering to OEMs. Effective logistics and supply chain management are paramount to ensure timely delivery and cost efficiency across these diverse channels, supporting both new vehicle production and the ongoing maintenance and repair needs of the global vehicle fleet.

The primary potential customers and end-users of automotive heat shields are deeply embedded within the global automotive ecosystem, comprising a broad spectrum of entities that range from large-scale vehicle manufacturers to individual consumers seeking aftermarket solutions. At the forefront are the Original Equipment Manufacturers (OEMs) of passenger cars, commercial vehicles, and increasingly, electric vehicles. These automotive giants represent the largest segment of demand, as heat shields are integral components in the design and production of virtually every new vehicle. OEMs require a consistent supply of high-quality, precisely engineered heat shields that meet their stringent specifications for thermal performance, weight, durability, and integration into complex vehicle architectures. Their purchasing decisions are heavily influenced by factors such as material innovation, cost-effectiveness, adherence to regulatory standards, and the ability of suppliers to meet large-volume production demands and just-in-time delivery schedules. The shift towards electrification has further diversified OEM needs, with specialized heat shields required for battery packs, electric motors, and power electronics.

Beyond the direct OEM market, Tier-1 automotive suppliers constitute another significant customer base. These suppliers often integrate heat shields into larger sub-assemblies, such as exhaust systems, engine modules, or body components, before delivering them to the OEMs. For instance, a major exhaust system manufacturer might source heat shield components from specialized suppliers and then assemble them into a complete exhaust system that is then supplied to a car manufacturer. This intricate supply chain necessitates strong collaborative relationships between heat shield producers and Tier-1 suppliers, involving joint development and rigorous testing to ensure compatibility and optimal system performance. Their needs often include customization capabilities, advanced engineering support, and competitive pricing for high-volume orders. The symbiotic relationship between heat shield manufacturers and Tier-1 suppliers is crucial for innovation and seamless integration within the broader automotive production process.

Furthermore, the automotive aftermarket represents a growing segment of potential customers, encompassing independent repair shops, automotive parts retailers, and individual vehicle owners. As vehicles age, heat shields can degrade, become damaged, or require replacement due to wear and tear. The aftermarket provides opportunities for manufacturers to offer replacement heat shields that match or exceed OEM specifications. Specialty vehicle manufacturers, involved in producing niche vehicles like recreational vehicles (RVs), agricultural machinery, construction equipment, and high-performance racing cars, also represent a targeted customer segment. These manufacturers often have unique and highly demanding thermal management requirements that necessitate custom-engineered heat shield solutions, driven by specific operational environments and performance objectives. The evolving landscape of mobility, including autonomous vehicles and new forms of urban transportation, also signals emerging customer segments for advanced thermal management components.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 6.5 Billion |

| Market Forecast in 2032 | USD 11.1 Billion |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Tenneco Inc., Lydall Inc., Autoneum Holding AG, ElringKlinger AG, Dana Incorporated, Federal-Mogul LLC (Tenneco), Morgan Advanced Materials plc, ThermoTec, Trelleborg AB, Continental AG, 3M Company, Rochling Group, Nichias Corporation, Carcoustics International GmbH, BASF SE, Sumitomo Riko Company Limited, Magna International Inc., DuPont de Nemours Inc., SGL Carbon SE, Insul-Fab Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Automotive Heat Shield Market is characterized by continuous innovation aimed at enhancing thermal efficiency, reducing weight, improving durability, and optimizing cost-effectiveness. A significant area of advancement is in the development of advanced materials. This includes lightweight metallic alloys, such as high-strength aluminum and specialized stainless steel grades that offer superior corrosion resistance and high-temperature performance with reduced mass. Simultaneously, there is a strong push towards advanced non-metallic materials, including multi-layer composite structures incorporating ceramic fibers, basalt, and fiberglass encapsulated within high-performance polymer matrices. These materials are engineered to provide excellent insulation properties, vibration damping, and acoustic attenuation, catering to the increasingly complex demands of modern vehicle design, including stringent noise, vibration, and harshness (NVH) requirements.

Manufacturing processes have also undergone significant technological evolution. Precision stamping and hydroforming techniques are widely used to create complex, three-dimensional heat shield geometries with tight tolerances, ensuring optimal fit and thermal performance in confined spaces. Laser cutting and robotic welding have become standard for high-volume production, offering unparalleled accuracy and efficiency. Furthermore, vacuum forming and advanced molding techniques are employed for non-metallic and composite heat shields, enabling the creation of lightweight components with intricate designs. The integration of advanced simulation and modeling software, such as Computational Fluid Dynamics (CFD) and Finite Element Analysis (FEA), is crucial at the design stage. These tools allow engineers to virtually test and optimize heat shield designs for thermal performance, material stress, and acoustic properties before physical prototyping, significantly reducing development time and costs while improving product effectiveness.

Emerging technologies are further reshaping the market, with a strong focus on smart and adaptive thermal management. This includes the exploration of phase-change materials (PCMs) and active cooling technologies, particularly for electric vehicle battery thermal management, where maintaining a precise temperature range is critical for performance and safety. Research into smart materials that can dynamically adjust their thermal properties in response to temperature changes, or self-healing materials that can repair minor damage, represents the cutting edge of innovation. Additive manufacturing (3D printing) is also gaining traction for prototyping and producing highly customized or geometrically complex heat shields, offering unparalleled design freedom and enabling the rapid iteration of new solutions. These technological advancements collectively drive the market towards more efficient, lighter, and more intelligently integrated thermal protection systems, critical for both traditional and future automotive powertrains.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.