ID : MRU_ 428876 | Date : Oct, 2025 | Pages : 253 | Region : Global | Publisher : MRU

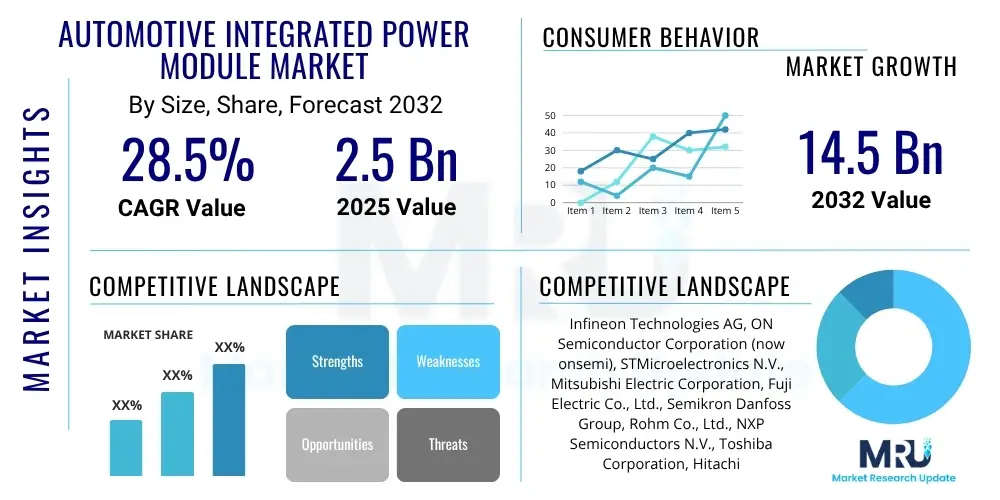

The Automotive Integrated Power Module Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 28.5% between 2025 and 2032. The market is estimated at $2.5 Billion in 2025 and is projected to reach $14.5 Billion by the end of the forecast period in 2032.

The Automotive Integrated Power Module (IPM) Market is at the forefront of the automotive industry's transformation towards electrification and enhanced energy efficiency. Integrated Power Modules are sophisticated semiconductor devices designed to consolidate multiple power components, such as Insulated Gate Bipolar Transistors (IGBTs) or Metal-Oxide-Semiconductor Field-Effect Transistors (MOSFETs), along with their respective gate drivers and protection circuits, into a single, compact, and highly reliable package. This integration is crucial for optimizing power conversion and management within various automotive systems, ensuring robust performance under demanding operational conditions including wide temperature variations and mechanical stress.

The core product in this market encompasses various types of IPMs, differentiated by their semiconductor material (e.g., Silicon, Silicon Carbide, Gallium Nitride), voltage ratings, and application-specific designs. These modules are fundamental to the efficient operation of electric vehicles (EVs), hybrid electric vehicles (HEVs), plug-in hybrid electric vehicles (PHEVs), and even advanced internal combustion engine vehicles that incorporate mild hybrid systems. Major applications include traction inverters for electric motor control, high-voltage DC-DC converters for managing power flow between different voltage domains (e.g., battery to auxiliary systems), and on-board chargers (OBCs) for battery charging, as well as components within off-board charging infrastructure and electric power steering systems.

The primary benefits derived from IPMs are enhanced power density, leading to more compact and lighter vehicle designs; improved thermal management capabilities, which reduce energy losses and extend component lifespan; and simplified system design due to fewer discrete components, which lowers manufacturing complexity and cost. The driving factors for this market are overwhelmingly linked to the accelerating global adoption of electric vehicles, the increasingly stringent governmental regulations concerning vehicle emissions and fuel economy, and the continuous push for higher performance, greater efficiency, and superior reliability in automotive power electronics. As vehicle autonomy and connectivity advance, the demand for highly efficient and robust power management solutions embedded within IPMs will only intensify.

The Automotive Integrated Power Module Market is currently undergoing a period of significant expansion and technological innovation, primarily propelled by the global shift towards electric mobility. Key business trends indicate a strong focus on strategic collaborations and mergers & acquisitions among semiconductor manufacturers, Tier 1 automotive suppliers, and OEMs. These partnerships aim to pool resources for advanced research and development, particularly in the realm of wide-bandgap (WBG) materials like Silicon Carbide (SiC) and Gallium Nitride (GaN), which promise superior efficiency and power density compared to traditional silicon-based solutions. Furthermore, there is an increasing emphasis on developing modular and scalable IPM platforms to cater to diverse vehicle architectures and power requirements, while also addressing ongoing challenges related to supply chain resilience and raw material sourcing.

Regional trends highlight Asia-Pacific as the dominant market, largely driven by the colossal growth in EV production and adoption in countries like China, South Korea, and Japan. Robust government support, extensive investments in charging infrastructure, and the presence of major automotive and electronics manufacturing hubs contribute significantly to the region's leadership. Europe is a close second, showcasing rapid growth fueled by stringent environmental regulations, ambitious decarbonization targets, and significant R&D initiatives in nations such as Germany, France, and the Nordic countries. North America is also experiencing substantial market expansion, supported by favorable government policies, increasing consumer demand for EVs, and growing investments in domestic EV manufacturing capabilities and charging networks.

From a segmentation perspective, the Electric Vehicle (EV) and Hybrid Electric Vehicle (HEV) segments are the primary growth engines, with full Battery Electric Vehicles (BEVs) demonstrating the most dynamic expansion due to their complete reliance on electric powertrains. The material segment is witnessing a rapid transition, with Silicon Carbide (SiC) based IPMs gaining significant traction over traditional Silicon (Si) modules, particularly for high-voltage (800V and above) and high-power applications, driven by the demand for faster charging and extended driving ranges. Similarly, within applications, traction inverters for motor control and on-board chargers are projected to maintain their leading positions, while DC-DC converters and off-board charging infrastructure also show robust growth, reflecting the comprehensive electrification of the automotive ecosystem.

Users frequently inquire about the transformative potential of artificial intelligence (AI) in revolutionizing the design, operational efficiency, and longevity of Automotive Integrated Power Modules. Common questions center on how AI can optimize power conversion algorithms, enable predictive maintenance, enhance thermal management strategies, and contribute to the development of more compact, reliable, and intelligent IPMs. Stakeholders are keen to understand AI's role in facilitating real-time fault diagnosis, adapting power delivery for autonomous driving, and ultimately accelerating the innovation cycle for next-generation power electronics. The prevailing themes underscore user expectations for AI to deliver unprecedented levels of efficiency, reliability, and smart functionality within automotive power systems.

The Automotive Integrated Power Module Market is driven by a powerful confluence of factors that underscore its critical role in modern transportation. The paramount driver is the exponential growth in the production and sales of electric vehicles (EVs), including Battery Electric Vehicles (BEVs), Hybrid Electric Vehicles (HEVs), and Plug-in Hybrid Electric Vehicles (PHEVs), globally. IPMs are indispensable for the efficient operation of EV powertrains, including traction inverters and on-board chargers. Complementing this is the intensifying demand for higher power density and increased energy efficiency in all automotive electronics. IPMs directly address this by reducing volumetric footprint while improving power conversion capabilities, crucial for extending EV range and reducing charging times. Furthermore, increasingly stringent global emission regulations compel automotive manufacturers to transition towards electrification, making advanced IPM technologies fundamental to compliance and competitive advantage.

However, the market also contends with significant restraints. A primary challenge is the high initial cost associated with advanced power semiconductor materials, particularly Silicon Carbide (SiC) and Gallium Nitride (GaN), which, despite their superior performance, can inflate the overall manufacturing costs for automotive systems. The inherent complexity of integrating these sophisticated modules into diverse and often space-constrained vehicle architectures poses substantial engineering hurdles, requiring extensive design, testing, and validation. Additionally, effective thermal management becomes progressively difficult with higher power densities, necessitating specialized cooling solutions that add to system complexity and cost. Supply chain vulnerabilities for critical semiconductor components, as highlighted by recent global events, also represent a persistent restraint, leading to potential production delays and increased costs.

Despite these challenges, the market is rife with opportunities for innovation and expansion. The ongoing development and commercialization of next-generation wide-bandgap (WBG) materials such as SiC and GaN promise even greater efficiencies, smaller form factors, and enhanced reliability, opening new avenues for high-voltage and ultra-fast charging applications. The burgeoning ecosystem around vehicle-to-grid (V2G) technology, which enables EVs to return power to the electrical grid, and bidirectional charging systems, demands highly sophisticated IPMs capable of managing complex two-way power flows. Moreover, the increasing sophistication of Advanced Driver-Assistance Systems (ADAS) and the progression towards fully autonomous vehicles necessitate extremely reliable, efficient, and compact power management solutions, providing a fertile ground for IPM innovation. The relentless impact force of regulatory pressure for decarbonization and energy efficiency will continue to stimulate technological advancements and market growth, ensuring IPMs remain central to the future of automotive power electronics.

The Automotive Integrated Power Module market is meticulously segmented to provide a comprehensive understanding of its various facets, enabling stakeholders to identify key growth areas, competitive landscapes, and strategic opportunities. This detailed analysis allows for a nuanced perspective on market dynamics, illustrating how different technological advancements, vehicle types, and application areas contribute to the overall market trajectory. The segmentation categories reflect the diverse functional requirements and design considerations inherent in modern automotive power electronics, offering granular insights into consumer preferences and industry adoption patterns.

The value chain for the Automotive Integrated Power Module market is a multi-layered and technologically sophisticated ecosystem, stretching from the foundational raw material extraction to the final integration into complex automotive systems. Upstream activities are dominated by specialized material providers and component manufacturers. This includes suppliers of ultra-pure silicon wafers, high-quality silicon carbide (SiC) substrates, gallium nitride (GaN) epitaxy, and various metallic components (e.g., copper, aluminum) for interconnects and heat sinks. Additionally, suppliers of advanced ceramic substrates (like AlN or Si3N4) for thermal management and specialty polymers for encapsulation are critical. Semiconductor foundries then transform these raw materials into discrete power semiconductor devices such as IGBTs, MOSFETs, and diodes, forming the core building blocks of an IPM.

In the midstream segment, specialized IPM manufacturers take these discrete power semiconductor components, along with gate driver ICs, sensing elements, and protection circuitry, and integrate them into a single, highly optimized module. This stage involves cutting-edge manufacturing processes, including advanced die attach techniques (e.g., silver sintering for superior thermal performance), precise wire bonding, sophisticated substrate mounting, and robust encapsulation to ensure mechanical integrity and environmental protection. Rigorous quality control, extensive testing for reliability under automotive stress conditions (e.g., temperature cycling, vibration), and adherence to strict automotive industry standards (like AEC-Q101) are absolutely paramount at this stage to guarantee the performance and safety of the final module. Design houses and engineering firms often play a significant role here, collaborating to optimize module layout and thermal characteristics.

Downstream, the completed Integrated Power Modules are primarily supplied to Tier 1 automotive suppliers. These Tier 1 companies are responsible for integrating the IPMs into larger, functional sub-systems such as complete EV powertrain inverters, DC-DC converters, on-board chargers, or electric power steering units. They often customize the IPM-based solutions to meet the specific performance, size, and interface requirements of various Original Equipment Manufacturers (OEMs). The distribution channels for IPMs are predominantly direct, involving close technical collaboration and long-term supply agreements between IPM manufacturers and Tier 1 suppliers or directly with large automotive OEMs due to the high degree of technical complexity, customization, and significant volume requirements. Indirect channels, typically through specialized industrial distributors, may serve smaller volume clients or aftermarket needs. This direct engagement throughout the value chain ensures efficient technical support, seamless integration, and a responsive supply chain essential for the fast-paced and demanding automotive industry.

The primary potential customers and end-users of Automotive Integrated Power Modules are integral to the global automotive industry's electrification efforts, representing a diverse yet interconnected ecosystem. Foremost among these are the global automotive Original Equipment Manufacturers (OEMs) who are at the forefront of designing, manufacturing, and bringing to market Battery Electric Vehicles (BEVs), Hybrid Electric Vehicles (HEVs), Plug-in Hybrid Electric Vehicles (PHEVs), and Fuel Cell Electric Vehicles (FCEVs). These OEMs require IPMs for critical components of their electric powertrains, including traction inverters that convert DC battery power to AC for electric motors, high-voltage DC-DC converters essential for managing power flow between varying voltage systems, and on-board chargers for efficient battery replenishment. Their continuous innovation in EV platforms directly translates into a sustained demand for increasingly efficient, compact, and reliable IPMs.

Beyond the vehicle manufacturers themselves, Tier 1 automotive suppliers constitute a significant and growing customer segment. These companies specialize in developing and producing comprehensive automotive sub-systems and modules, such as complete electric drive units, advanced power electronics modules, and sophisticated battery management systems. They frequently integrate IPMs as core components into their offerings, often customizing solutions to meet the specific technical specifications and volume demands of various OEMs. Additionally, a rapidly expanding customer base includes developers and operators of electric vehicle charging infrastructure. Both on-board and off-board charging solutions, particularly high-power fast-charging stations, necessitate robust and efficient power modules for effective energy conversion and management. As the global charging network expands, so too will the demand from these infrastructure providers for high-performance IPMs capable of handling significant power loads and ensuring charging efficiency and reliability.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $2.5 Billion |

| Market Forecast in 2032 | $14.5 Billion |

| Growth Rate | 28.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Infineon Technologies AG, ON Semiconductor Corporation (now onsemi), STMicroelectronics N.V., Mitsubishi Electric Corporation, Fuji Electric Co., Ltd., Semikron Danfoss Group, Rohm Co., Ltd., NXP Semiconductors N.V., Toshiba Corporation, Hitachi Ltd., ABB Ltd., Denso Corporation, Magna International Inc., Valeo S.A., Continental AG, BorgWarner Inc., Vitesco Technologies GmbH, Delphi Technologies (BorgWarner), Renesas Electronics Corporation, Texas Instruments Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Automotive Integrated Power Module market is defined by a dynamic and highly innovative technological landscape, primarily driven by the relentless pursuit of enhanced efficiency, increased power density, and superior reliability in automotive power electronics. A foundational technological shift involves the accelerating adoption and refinement of wide-bandgap (WBG) semiconductors, predominantly Silicon Carbide (SiC) and, with increasing momentum, Gallium Nitride (GaN). These advanced materials fundamentally outperform traditional silicon-based devices, particularly in high-voltage, high-frequency, and high-temperature environments, owing to their superior breakdown voltage, lower switching losses, and faster switching speeds. This transition to SiC and GaN is paramount for achieving critical performance metrics such as extending EV range, enabling ultra-fast charging capabilities, and reducing the overall weight and size of power electronic systems.

Beyond the fundamental semiconductor materials, significant technological advancements are occurring in packaging and integration techniques. Innovations include advanced die attach methods like silver sintering, which offers significantly improved thermal conductivity and reliability compared to traditional solder. Lead-frame-less designs, double-sided cooling architectures, and advanced substrate materials (e.g., AlN, Si3N4 ceramics with direct bond copper or active metal brazing) are revolutionizing thermal management, allowing IPMs to dissipate heat more effectively. This enables higher power output from smaller physical footprints, which is critical for the compact and integrated designs required in modern vehicles. Furthermore, the integration of sophisticated intelligence within the module, encompassing highly optimized gate drivers, advanced embedded sensors for real-time temperature and current monitoring, and robust self-protection circuits, is transforming IPMs into intelligent power units capable of autonomous fault detection and prevention.

Another crucial aspect of the evolving technology landscape is the increasing level of integration and functionality within IPMs. Manufacturers are developing modules that not only house power switches and drivers but also incorporate additional features such as DC-DC conversion, battery management functions, and even communication interfaces. This higher level of system-in-package integration reduces component count, simplifies the overall system design for automotive OEMs and Tier 1 suppliers, and enhances the reliability of the entire power electronics system. The ongoing research and development in novel material combinations, advanced manufacturing processes like additive manufacturing for heat sinks, and the application of digital twin technology for predictive performance modeling further underscore the rapid pace of innovation, ensuring that automotive IPMs remain at the cutting edge of power electronics engineering, continuously meeting the escalating demands of electrified and intelligent vehicles.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.