ID : MRU_ 430573 | Date : Nov, 2025 | Pages : 245 | Region : Global | Publisher : MRU

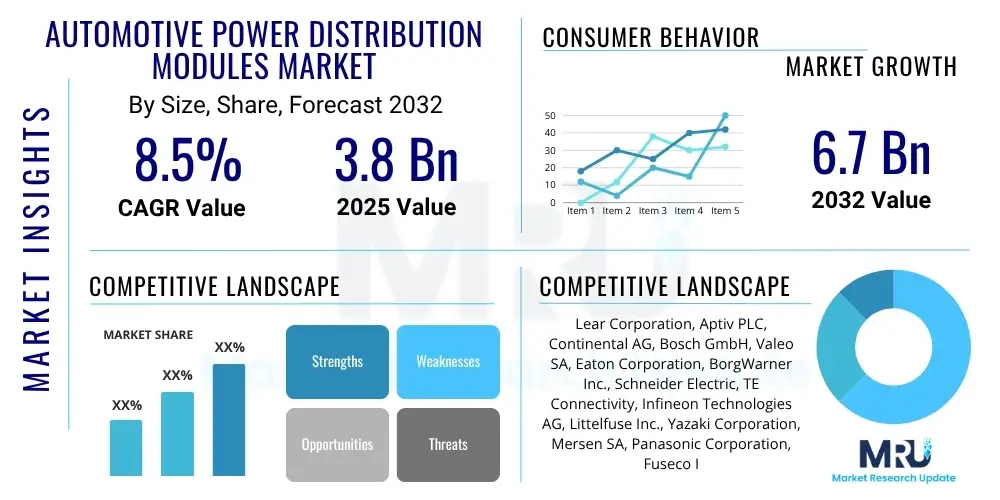

The Automotive Power Distribution Modules Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2032. The market is estimated at USD 3.8 Billion in 2025 and is projected to reach USD 6.7 Billion by the end of the forecast period in 2032.

The Automotive Power Distribution Modules (PDMs) market is experiencing significant evolution driven by the increasing complexity of vehicle electrical and electronic (E/E) architectures. PDMs serve as critical components that centralize or distribute electrical power and signals efficiently throughout a vehicle, replacing traditional, more cumbersome wiring harnesses and fuse boxes. These modules are essential for managing the growing array of electronic systems, from infotainment and driver assistance to powertrain control and safety features, ensuring optimal performance and reliability across various automotive applications. The primary benefits of advanced PDMs include significant weight reduction, space optimization, enhanced diagnostic capabilities, and improved electrical system protection and reliability. These advantages are crucial for modern vehicles, particularly with the widespread adoption of electrification and advanced connectivity features. The market's expansion is fundamentally propelled by the surging demand for electric vehicles (EVs), the integration of sophisticated Advanced Driver Assistance Systems (ADAS), and the overall increase in electronic content within both passenger and commercial vehicles, all requiring more efficient and robust power management solutions.

The Automotive Power Distribution Modules market is characterized by robust growth and transformative trends, largely shaped by the automotive industry's pivot towards electrification, autonomous driving, and enhanced connectivity. Business trends indicate a strong focus among manufacturers on developing highly integrated, modular, and software-defined PDMs that can adapt to diverse vehicle platforms and evolving electrical demands. Strategic collaborations and mergers are prevalent as companies aim to consolidate expertise and streamline product development for next-generation solutions. Regionally, Asia Pacific continues to dominate the market due to high vehicle production volumes and rapid adoption of advanced automotive technologies, while Europe and North America are focusing on premium vehicle segments and accelerated EV integration, driving demand for intelligent and high-performance PDMs. Emerging markets in Latin America and the Middle East and Africa are also showing promising growth as automotive manufacturing capabilities expand and consumer preferences shift towards more technologically advanced vehicles.

Segment-wise, the market is witnessing a notable shift towards smart PDMs and those specifically designed for electric and hybrid vehicles, reflecting the industry's investment priorities. The increasing complexity of ADAS and infotainment systems is fueling demand for PDMs with enhanced communication capabilities and fault tolerance. Furthermore, there is a growing emphasis on power efficiency and thermal management within these modules, critical for optimizing the performance and longevity of vehicle electrical systems. These trends collectively underscore a market moving towards more sophisticated, adaptable, and resilient power distribution solutions that can support the continuous innovation in automotive technology.

Users frequently inquire about how Artificial Intelligence (AI) can revolutionize power management within vehicles, specifically concerning predictive maintenance, dynamic power allocation, and the integration of autonomous driving systems. Common questions center around the reliability and safety implications of AI-driven power distribution, the potential for cybersecurity vulnerabilities, and the practical implementation challenges in current and future automotive architectures. There is also significant interest in how AI can optimize energy consumption, extend battery life in electric vehicles, and enhance the overall diagnostic capabilities of PDMs. The overarching theme reflects a desire to understand AI's tangible benefits in creating more efficient, intelligent, and resilient automotive electrical systems, while also addressing inherent complexities and risks associated with its deployment.

The Automotive Power Distribution Modules market is significantly influenced by a confluence of drivers, restraints, opportunities, and broader impact forces. Key drivers include the relentless growth in vehicle electrification, encompassing both hybrid and battery electric vehicles, which necessitates sophisticated power management for high-voltage systems and numerous electronic loads. The escalating integration of Advanced Driver Assistance Systems (ADAS) and autonomous driving technologies also mandates more robust and intelligent PDMs to power complex sensor arrays, processing units, and actuators reliably. Furthermore, the overall increase in electronic content within modern vehicles, from sophisticated infotainment systems to advanced safety features, consistently drives the demand for more efficient, compact, and lighter power distribution solutions to accommodate these innovations without adding excessive weight or bulk. These factors collectively create a strong upward trajectory for the market, pushing manufacturers to innovate and provide more integrated and capable modules.

Despite these growth drivers, the market faces several significant restraints. High development and integration costs associated with advanced PDM technologies, particularly for solid-state and smart modules, pose a challenge for smaller manufacturers and can impact vehicle pricing. The inherent complexity of integrating these new systems into diverse vehicle architectures, coupled with the need for rigorous testing and validation, often leads to extended development cycles. Additionally, the lack of universal standardization across different vehicle manufacturers and regions can hinder mass adoption and increase design costs. Technical challenges such as efficient thermal management for high-power applications and ensuring electromagnetic compatibility (EMC) within increasingly dense electrical environments also represent ongoing hurdles for innovation. Navigating these restraints requires substantial investment in research and development, along with collaborative efforts across the automotive supply chain.

Opportunities for market expansion are abundant, particularly with the continued advancements in autonomous vehicle technology, which will demand unprecedented levels of electrical reliability and redundancy. The emergence of software-defined vehicles (SDVs) presents a significant opportunity for highly configurable and adaptive PDMs, enabling over-the-air updates and feature upgrades for power management. Innovations in smart charging infrastructure and vehicle-to-grid (V2G) technologies will also require advanced PDMs capable of handling bidirectional power flows. Furthermore, the increasing consumer expectation for seamless connectivity and personalized in-car experiences will continue to drive the demand for PDMs that can efficiently power and manage sophisticated infotainment and telematics systems. The market is also shaped by external impact forces, including stringent global regulatory pressures regarding vehicle safety and emissions, which necessitate lighter and more efficient electrical systems, and macroeconomic factors such as fluctuating raw material prices and supply chain disruptions, which can influence production costs and market dynamics. Technological advancements from semiconductor industries and material sciences continuously open new avenues for improved PDM performance and miniaturization, profoundly shaping the competitive landscape.

The Automotive Power Distribution Modules market is broadly segmented to provide a detailed understanding of its diverse applications, technological approaches, and end-user requirements. This segmentation allows for precise market analysis, identifying specific growth areas and technological preferences across various vehicle types and functionalities. The market's structure reflects the evolving needs of the automotive industry, moving towards more intelligent, efficient, and integrated power distribution systems.

The value chain for Automotive Power Distribution Modules is a complex network involving multiple tiers of suppliers, manufacturers, and distribution channels, all contributing to the final product delivered to the end-user. The upstream segment is characterized by specialized component manufacturers and raw material suppliers, forming the foundational layer of the production process. This includes providers of semiconductors, passive components like capacitors and resistors, high-grade plastics for housing, and various metals for connectors and wiring harnesses. Key players in this stage focus on delivering high-quality, reliable, and cost-effective materials and electronic components that meet stringent automotive standards for performance, durability, and thermal management. Advances in material science and semiconductor technology at this stage directly influence the innovation and capabilities of the downstream PDM products, affecting their size, efficiency, and intelligence. Maintaining a robust and resilient supply chain for these foundational elements is crucial, given the global nature of automotive manufacturing and the potential for disruptions.

Moving downstream, the value chain encompasses Tier-2 and Tier-1 automotive suppliers responsible for manufacturing the complete PDM assemblies, incorporating components from the upstream segment. Tier-1 suppliers, such as major automotive electronics companies, design, develop, and produce complex PDMs that meet specific OEM requirements, often integrating software and advanced control features. These suppliers engage in extensive research and development to innovate new PDM architectures, focusing on miniaturization, enhanced diagnostic capabilities, and integration with vehicle communication networks. The distribution channel primarily involves direct sales from Tier-1 suppliers to Automotive Original Equipment Manufacturers (OEMs), where PDMs are integrated into new vehicle assembly lines. This direct interaction allows for close collaboration in design, testing, and customization, ensuring that the PDMs are perfectly tailored to the vehicle's electrical architecture. Indirect distribution channels also exist, particularly for the aftermarket, where replacement PDMs or upgrade kits are supplied through dealership networks, independent repair shops, and specialized automotive parts distributors. These indirect channels cater to vehicle maintenance, repairs, and customization needs, though they represent a smaller portion of the overall market compared to OEM supply. The efficiency and reliability of both direct and indirect distribution are critical for ensuring timely supply and widespread market penetration.

The primary potential customers for Automotive Power Distribution Modules are diverse, reflecting the broad application spectrum within the automotive ecosystem. At the forefront are Automotive Original Equipment Manufacturers (OEMs), including global giants such as Toyota, Volkswagen, General Motors, Ford, Hyundai, and emerging electric vehicle manufacturers like Tesla, Rivian, and Lucid. These OEMs integrate PDMs directly into their vehicle assembly lines as foundational components of the electrical system, requiring customized solutions that align with their specific vehicle platforms, technological roadmaps, and regulatory compliance. The demand from OEMs is driven by the continuous innovation in vehicle design, the electrification trend, and the increasing sophistication of in-car electronics and safety systems, all necessitating advanced and reliable power management. OEMs seek PDMs that offer weight savings, space optimization, enhanced diagnostic capabilities, and seamless integration with other vehicle control units.

Beyond OEMs, Tier-1 automotive suppliers represent another significant customer segment. These companies, such as Bosch, Continental, Denso, Aptiv, and ZF, often develop sub-systems or modules that require integrated power distribution solutions. They procure PDMs from specialized manufacturers or develop them in-house for their larger system offerings (e.g., ADAS modules, infotainment systems) which are then supplied to OEMs. This segment values modularity, compatibility with various communication protocols, and high-performance specifications to ensure their integrated systems function optimally. Furthermore, the aftermarket segment, comprising independent repair shops, authorized service centers, and automotive parts retailers, constitutes potential customers for replacement or upgrade PDMs. As vehicles age, components may require replacement due to wear or malfunction, creating a steady demand for aftermarket PDMs. Specialized vehicle modifiers and fleet operators also form a niche customer base, requiring robust and sometimes customized PDMs for their unique vehicle configurations and operational demands. The growing adoption of software-defined vehicles will further expand the customer base to include software developers and technology companies seeking highly configurable power hardware.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 3.8 Billion |

| Market Forecast in 2032 | USD 6.7 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Lear Corporation, Aptiv PLC, Continental AG, Bosch GmbH, Valeo SA, Eaton Corporation, BorgWarner Inc., Schneider Electric, TE Connectivity, Infineon Technologies AG, Littelfuse Inc., Yazaki Corporation, Mersen SA, Panasonic Corporation, Fuseco Inc., Methode Electronics, Sumitomo Electric Industries, Inc., Delta Electronics, Inc., Marelli Holdings Co. Ltd., Mitsubishi Electric Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Automotive Power Distribution Modules market is undergoing a significant technological transformation, moving from conventional fuse and relay boxes to highly integrated and intelligent systems. A pivotal advancement is the increasing adoption of solid-state power distribution technology, which replaces traditional mechanical fuses and relays with semiconductor-based switches (like MOSFETs). This technology offers superior reliability, faster switching speeds, precise current control, and advanced diagnostic capabilities, including programmable overload protection and fault detection, all while reducing weight and size. The shift towards software-defined power management is also critical, enabling over-the-air updates for power allocation and system configuration, crucial for adapting to new features and optimizing energy consumption in connected and autonomous vehicles. These technologies are foundational for the next generation of PDMs, offering unprecedented flexibility and control over vehicle electrical systems.

Furthermore, the integration of advanced communication protocols such as CAN bus, FlexRay, and increasingly automotive Ethernet within PDMs is enhancing their ability to communicate with other electronic control units (ECUs) and sensors across the vehicle. This improved communication facilitates more sophisticated power management strategies, enabling dynamic load shedding and optimized power routing. Thermal management solutions are also advancing, with the development of more efficient heat dissipation materials and designs, critical for maintaining the performance and longevity of increasingly powerful and compact PDMs. The incorporation of integrated circuits for smart sensing and control, along with advanced packaging techniques, is leading to smaller, lighter, and more robust modules capable of withstanding harsh automotive environments. These technological advancements collectively contribute to the development of PDMs that are not only more efficient and reliable but also smarter and more adaptable to the complex demands of modern automotive architectures.

Automotive Power Distribution Modules are critical electrical components that manage and distribute power and signals throughout a vehicle's electrical system, optimizing efficiency and replacing traditional wiring harnesses and fuse boxes.

PDMs are vital due to the rising complexity of vehicle electronics, the growth of electric vehicles, and the integration of advanced features like ADAS, all of which require efficient, reliable, and compact power management solutions.

Advanced PDMs offer significant benefits including weight reduction, space optimization, enhanced diagnostic capabilities, improved electrical system protection, and increased overall vehicle reliability and safety.

AI enhances PDMs by enabling features like predictive maintenance, dynamic power management, advanced fault detection, and seamless integration with autonomous driving systems, leading to more intelligent and resilient electrical architectures.

The primary drivers include the global trend of vehicle electrification, the widespread adoption of Advanced Driver Assistance Systems (ADAS), and the continuous increase in electronic content within both passenger and commercial vehicles.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.