ID : MRU_ 429740 | Date : Nov, 2025 | Pages : 258 | Region : Global | Publisher : MRU

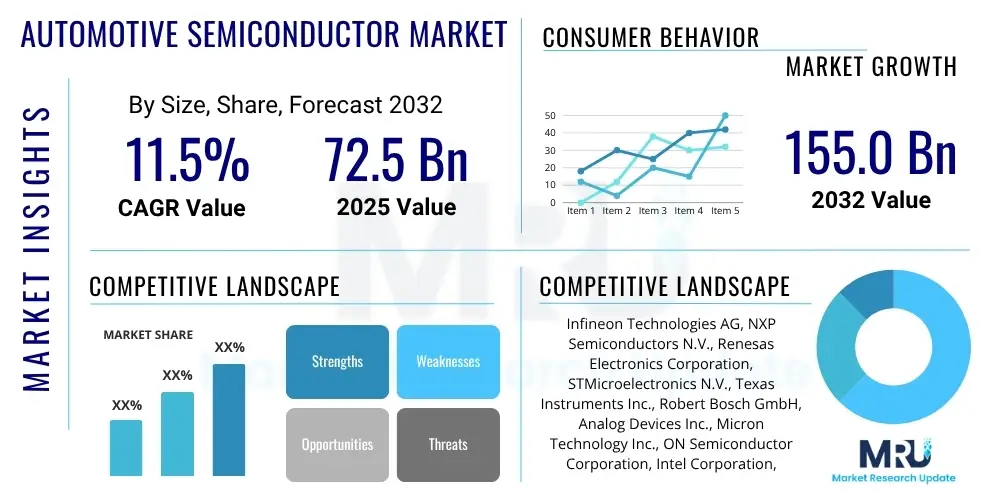

The Automotive Semiconductor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2025 and 2032. The market is estimated at USD 72.5 billion in 2025 and is projected to reach USD 155.0 billion by the end of the forecast period in 2032.

The Automotive Semiconductor Market encompasses a broad and rapidly evolving array of electronic components critically essential for the functioning and advancement of modern vehicles. These sophisticated components serve as the foundational bedrock for an increasing number of vehicle features, driving significant advancements across key areas such as vehicle safety, advanced connectivity, and overall operational efficiency. The market includes a diverse range of products, notably encompassing high-performance microcontrollers (MCUs) that act as the brains of electronic control units, various types of memory devices for data storage, an extensive suite of analog integrated circuits (ICs) for power management and signal conditioning, and a wide array of sensors crucial for environmental perception and vehicle monitoring.

These semiconductors find major applications across virtually every aspect of contemporary automotive design. They are indispensable for Advanced Driver Assistance Systems (ADAS), which include features like adaptive cruise control, lane-keeping assist, and automatic emergency braking, all relying heavily on precise sensor data processing. Furthermore, they are central to advanced infotainment and telematics systems, enabling in-car navigation, connectivity, and entertainment; powertrain control systems for optimizing engine and transmission performance; critical vehicle safety systems like airbags and electronic stability control; and sophisticated body electronics that manage lighting, climate control, and comfort features. The integration of these components fundamentally transforms the driving experience from a mechanical interaction to a highly intelligent and digitally enhanced one.

The market’s robust growth is propelled by several potent driving factors. A primary catalyst is the global surge in electric vehicle (EV) adoption, which dramatically increases the semiconductor content per vehicle for power electronics, battery management, and motor control. Concurrently, there is an escalating consumer and regulatory demand for advanced safety and convenience features, necessitating more complex ADAS functionalities. The continuous evolution of in-car infotainment systems, driven by consumer desire for seamless digital integration and personalized experiences, also fuels demand. Ultimately, the industry's long-term strategic push towards fully autonomous vehicles remains a powerful underlying driver, requiring exponentially more powerful and reliable semiconductor solutions to process vast amounts of data and make real-time, safety-critical decisions. These benefits combined with technological innovation underscore the market's trajectory.

The global Automotive Semiconductor Market is experiencing a period of profound transformation, characterized by dynamic business trends, evolving regional market landscapes, and distinct growth patterns across various product and application segments. From a business perspective, the industry is witnessing an accelerating trend towards consolidation, with major players acquiring specialized firms to enhance their technological portfolios and market share, particularly in emerging areas like AI and power electronics. Strategic partnerships and collaborative ventures are also becoming commonplace, as companies pool resources to tackle the immense research and development costs associated with next-generation automotive technologies and to navigate complex supply chain dynamics. Furthermore, there is a pronounced industry-wide shift towards adopting more advanced manufacturing nodes and processes, essential for producing higher-performance, energy-efficient, and smaller form-factor semiconductor components demanded by modern vehicles.

Regionally, the market exhibits varying degrees of maturity and growth drivers. The Asia Pacific region continues to stand as the dominant force, not only in terms of semiconductor manufacturing capacity but also in consumption, propelled by its massive automotive production base, the rapid and widespread adoption of electric vehicles, and significant governmental support for advanced technology integration in countries like China, Japan, and South Korea. Europe remains a critical hub for innovation, particularly in the areas of Advanced Driver Assistance Systems (ADAS), vehicle safety, and stringent environmental regulations, which consistently drive demand for sophisticated and reliable semiconductor solutions. North America, similarly, is a key player, leading investments in autonomous driving research and development, fostering an accelerating transition towards electric mobility, and demonstrating a strong appetite for cutting-edge infotainment and connectivity features.

Examining market segments, the components vital for Advanced Driver Assistance Systems (ADAS) and the comprehensive electrification of vehicle powertrains are currently experiencing the most significant and accelerated growth. This surge is a direct reflection of the industry's overarching focus on enhancing vehicle intelligence, improving safety standards, and significantly reducing carbon emissions. Microcontrollers, crucial for managing a multitude of in-vehicle functions, alongside various types of sensors (LiDAR, Radar, camera) for environmental perception, and power management ICs (PMICs) for efficient energy utilization, are seeing robust demand. This segmentation trend underscores the strategic direction of the automotive industry towards a future defined by autonomy, connectivity, and sustainability, with semiconductors as the core enablers of this vision.

Common user inquiries surrounding AI's impact on the Automotive Semiconductor Market frequently revolve around its pivotal role in advancing autonomous driving capabilities and enhancing ADAS functionalities. Users are keen to understand how AI-driven algorithms enable more sophisticated sensor fusion, real-time decision-making, and predictive capabilities within vehicles, directly influencing the demand for higher-performance, AI-optimized semiconductor solutions. Key concerns also include the immense data processing requirements, the need for specialized AI accelerators, and the associated challenges in developing energy-efficient and reliable chips capable of handling complex neural networks for critical automotive applications. Expectations highlight AI as the fundamental enabler for the next generation of software-defined vehicles, driving innovation in chip architecture and system integration, and necessitating significant investments in both hardware and software co-development.

The Automotive Semiconductor Market operates within a complex framework influenced by a dynamic interplay of propelling drivers, inherent systemic restraints, emerging strategic opportunities, and broader external impact forces. A primary driver is the accelerating trend of vehicle electrification, which encompasses Battery Electric Vehicles (BEVs), Plug-in Hybrid Electric Vehicles (PHEVs), and Hybrid Electric Vehicles (HEVs). This shift exponentially increases the demand for power semiconductors, such as Silicon Carbide (SiC) and Gallium Nitride (GaN) devices, as well as sophisticated battery management systems (BMS) and motor control units, all of which are semiconductor-intensive. Concurrently, the rapid proliferation of Advanced Driver Assistance Systems (ADAS) across all vehicle segments – ranging from basic features like automatic emergency braking to more advanced functionalities like adaptive cruise control and lane-keeping assist – necessitates a vast array of high-performance sensors, specialized microcontrollers, and powerful processing units for real-time data interpretation and decision-making, further fueling market expansion. Moreover, the escalating consumer demand for advanced in-car infotainment and seamless connectivity features, integrating smartphones, navigation, and entertainment, significantly boosts the need for high-speed processors and memory components.

However, the market also confronts several substantial restraints that temper its growth potential. Persistent and often unpredictable global supply chain disruptions, exacerbated by geopolitical events and natural disasters, have repeatedly highlighted vulnerabilities in semiconductor manufacturing and logistics, leading to production delays and increased costs for automotive OEMs. The development of cutting-edge, automotive-grade semiconductors is characterized by exceptionally high research and development (R&D) costs, requiring significant capital investment and prolonged development cycles, which can be particularly challenging for smaller players. Additionally, the industry is subject to increasingly stringent regulatory requirements for vehicle safety, emissions, and cybersecurity across major global markets, demanding extensive testing and certification processes that add complexity and cost to semiconductor design and integration. Geopolitical tensions and trade disputes between key manufacturing nations also introduce uncertainty, impacting raw material access, manufacturing locations, and market stability.

Despite these challenges, the Automotive Semiconductor Market is replete with promising opportunities. The conceptual and technological evolution towards software-defined vehicles (SDVs) presents a transformative opportunity, enabling manufacturers to update vehicle functionalities and introduce new features via over-the-air (OTA) updates, extending vehicle lifecycles and creating new revenue streams, all underpinned by flexible and powerful semiconductor architectures. The integration of 5G connectivity into vehicles opens new avenues for enhanced vehicle-to-everything (V2X) communication, real-time traffic data, and superior infotainment streaming. Advancements in packaging technologies, allowing for greater miniaturization, improved thermal management, and heterogeneous integration of diverse chiplets, are also creating new possibilities for compact and high-performance automotive modules. Furthermore, the exploration of untapped emerging markets in developing economies, where vehicle ownership is on the rise and demand for advanced features is growing, represents a significant long-term growth avenue. These opportunities, coupled with ongoing technological advancements in areas like AI, quantum computing, evolving regulatory frameworks, changing economic conditions, and shifting consumer preferences towards sustainable and technologically rich vehicles, collectively shape the competitive landscape and strategic direction of the automotive semiconductor industry.

The Automotive Semiconductor Market is meticulously segmented across various dimensions to provide a granular and comprehensive understanding of its intricate structure and diverse dynamics. This systematic classification enables market analysts and industry stakeholders to pinpoint specific growth drivers, identify emerging technological requirements, and discern key competitive landscapes within the broader automotive ecosystem. The multi-faceted segmentation highlights the increasing complexity and specialization of electronic components required to power the advanced functionalities of modern vehicles, from basic operational systems to sophisticated autonomous capabilities. It also allows for the differentiation of market trends based on component type, the specific application within the vehicle, the category of vehicle in which the semiconductors are deployed, and the propulsion technology driving the vehicle, offering critical insights for strategic planning and product development.

Understanding these detailed market segments is paramount for semiconductor manufacturers, automotive OEMs, and Tier 1 suppliers alike. It facilitates the precise allocation of research and development resources, informs targeted marketing and sales strategies, and supports informed investment decisions. For instance, analyzing the growth trajectory of sensors within the ADAS segment provides clear signals for investment in LiDAR or Radar technologies, while the propulsion type segmentation reveals the accelerating demand for power management ICs in electric vehicles. Each segment represents a unique set of technological demands, market drivers, and competitive pressures, making a thorough segmentation analysis indispensable for navigating the complexities and capitalizing on the opportunities present in this rapidly evolving and high-stakes market.

The value chain for the Automotive Semiconductor Market is a highly complex and interconnected ecosystem, spanning multiple stages from the extraction of raw materials to the final integration of sophisticated electronic components into vehicles. The upstream segment of this chain is characterized by capital-intensive and technologically advanced processes. It begins with the procurement of raw materials such as ultra-pure silicon, various metals, and chemicals. Following this, wafer manufacturers transform these materials into silicon wafers, which serve as the fundamental substrates for semiconductor fabrication. This stage also includes the critical role of semiconductor equipment providers, who supply the highly specialized machinery required for lithography, deposition, etching, and other intricate manufacturing steps. These initial stages are marked by high barriers to entry due to significant capital expenditure, extensive R&D, and the need for proprietary manufacturing expertise.

Moving further along, the midstream processes are dominated by semiconductor design and manufacturing companies. Here, the silicon wafers undergo intricate fabrication processes, including front-end-of-line (FEOL) and back-end-of-line (BEOL) steps, to create integrated circuits (ICs) tailored for automotive applications. This involves designing specific chip architectures, fabricating the chips, and then packaging them into robust, automotive-grade modules that can withstand harsh operating environments (e.g., extreme temperatures, vibrations). Rigorous testing and quality assurance procedures are paramount at this stage to ensure the reliability, functional safety, and compliance with stringent automotive industry standards such as AEC-Q100. This segment often involves partnerships between fabless design houses and dedicated foundries, or vertically integrated device manufacturers (IDMs) that handle both design and fabrication.

The downstream segment primarily involves Tier 1 automotive suppliers (e.g., Bosch, Continental, ZF, Denso) who integrate these packaged semiconductors into larger, more complex automotive modules and sub-systems, such as engine control units (ECUs), Advanced Driver Assistance Systems (ADAS) modules, infotainment dashboards, and body control modules. These integrated systems are then supplied directly to Automotive Original Equipment Manufacturers (OEMs) like Toyota, Volkswagen, General Motors, and Tesla, who ultimately assemble them into the final vehicles. Distribution channels for automotive semiconductors are typically bifurcated: direct sales are common for high-volume, specialized components where semiconductor manufacturers work closely with major Tier 1s and OEMs to ensure customized solutions and supply chain stability. Indirect distribution, through a network of specialized electronics distributors, caters to smaller manufacturers, prototyping needs, and the aftermarket segment, providing a broader reach and logistical support for diverse customer requirements, often emphasizing established long-term partnerships and robust supply agreements to manage complex inventory and demand fluctuations.

The Automotive Semiconductor Market serves a broad and evolving spectrum of potential customers and end-users, each with distinct needs and procurement strategies that drive innovation and demand within the industry. At the forefront are the global Automotive Original Equipment Manufacturers (OEMs), including established giants like Toyota, Volkswagen, General Motors, Ford, and Hyundai, as well as disruptive newcomers such as Tesla and Rivian. These OEMs are the ultimate integrators of semiconductor technology into their vehicles, directly influencing component specifications and design, and their increasing engagement in semiconductor selection and even co-development highlights the strategic importance of these electronic components in differentiating their products and achieving technological leadership.

Equally crucial are the Tier 1 automotive suppliers, such as Bosch, Continental, Denso, ZF Friedrichshafen, and Magna International. These companies are major purchasers of semiconductors, as they design, develop, and manufacture complex automotive systems and modules—like braking systems, powertrain components, infotainment systems, and ADAS modules—which are then supplied to OEMs. Their role is pivotal in translating raw semiconductor technology into functional automotive solutions, often acting as intermediaries who integrate multiple chips into a cohesive system. The growing sophistication of these modules means Tier 1s require a vast array of high-performance, reliable, and automotive-grade semiconductors.

Furthermore, the rapid expansion of the Electric Vehicle (EV) segment, encompassing Battery Electric Vehicles (BEVs), Plug-in Hybrid Electric Vehicles (PHEVs), and Hybrid Electric Vehicles (HEVs), has introduced a specialized and rapidly growing set of customers. These EV manufacturers drive significant demand for power semiconductors (e.g., SiC, GaN), battery management integrated circuits (BMICs), and advanced microcontrollers essential for efficient power conversion, energy storage, and motor control. Beyond manufacturing, companies dedicated to developing autonomous vehicle technology, including both traditional automakers and specialized tech firms, represent a key customer segment for AI processors, high-resolution sensors, and secure communication chips. Lastly, providers of aftermarket automotive solutions, diagnostic tools, and repair services also form an important customer base for various types of automotive semiconductors, ranging from replacement parts to upgrade modules, ensuring the longevity and continued performance of vehicles throughout their lifecycle.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 72.5 Billion |

| Market Forecast in 2032 | USD 155.0 Billion |

| Growth Rate | 11.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Infineon Technologies AG, NXP Semiconductors N.V., Renesas Electronics Corporation, STMicroelectronics N.V., Texas Instruments Inc., Robert Bosch GmbH, Analog Devices Inc., Micron Technology Inc., ON Semiconductor Corporation, Intel Corporation, Qualcomm Inc., NVIDIA Corporation, ROHM Co. Ltd., Toshiba Corporation, Broadcom Inc., Continental AG, Denso Corporation, Magna International Inc., Valeo, ZF Friedrichshafen AG |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Automotive Semiconductor Market is fundamentally shaped by a dynamic and continually advancing technology landscape, striving to meet the increasingly stringent demands for higher performance, greater efficiency, and enhanced reliability in modern vehicles. A significant trend involves the widespread adoption of advanced process nodes, with manufacturers migrating towards smaller geometries like 7nm and 5nm. These finer manufacturing processes enable the integration of a greater number of transistors onto a single chip, leading to significantly higher processing power and greater power efficiency in critical components such as microcontrollers (MCUs) and System-on-Chips (SoCs), which are essential for complex computations in ADAS and infotainment systems. This miniaturization also allows for more compact designs, crucial for space-constrained vehicle architectures.

Furthermore, the industry is experiencing a profound shift towards Wide Bandgap (WBG) semiconductors, particularly Silicon Carbide (SiC) and Gallium Nitride (GaN) devices, especially prevalent in the rapidly expanding electric vehicle (EV) segment. These advanced materials offer superior performance characteristics compared to traditional silicon, including higher power density, significantly improved energy efficiency, and better thermal management capabilities. This makes SiC and GaN indispensable for high-voltage and high-frequency applications like EV inverters, on-board chargers, and DC-DC converters, which are critical for optimizing range and charging speed. Concurrently, the proliferation of sophisticated sensor technologies forms the perception layer of autonomous vehicles and ADAS. This includes high-resolution LiDAR (Light Detection and Ranging) for 3D mapping, advanced Radar sensors for object detection in all weather conditions, and high-megapixel camera sensors for visual perception and image recognition, all requiring specialized image processors and robust sensor fusion capabilities.

The integration of Artificial Intelligence (AI) and Machine Learning (ML) processors, including dedicated AI accelerators and neuromorphic computing architectures, is becoming indispensable for real-time data processing, complex pattern recognition, object classification, and decision-making in autonomous driving systems. These processors demand robust computing power at the edge, capable of handling immense data streams generated by vehicle sensors. Moreover, secure connectivity solutions, such as automotive Ethernet, CAN FD, and the impending integration of 5G cellular technology, are paramount for enabling reliable vehicle-to-everything (V2X) communication, facilitating seamless over-the-air (OTA) software updates, and supporting advanced cloud-connected services. Finally, advancements in packaging technologies, including 3D stacking and chiplet integration, are being increasingly employed to integrate diverse functionalities into smaller, more reliable, and thermally efficient packages, suitable for the harsh and demanding operating environments found within automotive applications, ensuring long-term durability and performance.

The Automotive Semiconductor Market is projected to achieve a robust Compound Annual Growth Rate (CAGR) of 11.5% between 2025 and 2032. This significant expansion is primarily fueled by the accelerating global shift towards vehicle electrification, the pervasive integration of advanced driver assistance systems (ADAS), and the increasing demand for enhanced in-car connectivity and intelligence across all vehicle segments, leading to substantial growth in market value.

The demand for automotive semiconductors is primarily driven by critical applications such as Advanced Driver Assistance Systems (ADAS), which enhance safety and driving convenience; sophisticated infotainment and telematics systems for connectivity and entertainment; efficient powertrain and chassis control for performance and fuel economy; essential vehicle safety systems including airbags and electronic stability control; and various body electronics for vehicle functionality. Each application necessitates a diverse range of specialized semiconductor components.

Electric Vehicles (EVs) are profoundly impacting the automotive semiconductor market by significantly boosting the demand for specific component categories. They require a much higher content of power semiconductors, such as Silicon Carbide (SiC) and Gallium Nitride (GaN) devices, crucial for efficient power conversion in inverters and chargers. Furthermore, EVs drive demand for advanced battery management integrated circuits (BMICs) and high-performance microcontrollers essential for precise motor control, battery optimization, and overall energy management, thus acting as a major growth catalyst for the market.

Key technological trends shaping the automotive semiconductor landscape include the adoption of advanced process nodes like 7nm and 5nm for higher performance and efficiency; the increasing use of wide bandgap materials such as SiC and GaN in power electronics; the proliferation of sophisticated sensor technologies like LiDAR, Radar, and high-resolution cameras for advanced perception; the integration of powerful AI/ML processors for autonomous driving intelligence; and the deployment of secure, high-bandwidth connectivity solutions, including automotive Ethernet and the upcoming 5G integration for advanced vehicle-to-everything (V2X) communication capabilities.

The automotive semiconductor industry faces several significant challenges, including persistent global supply chain disruptions that can impede production and increase costs; the substantial financial burden of high research and development (R&D) costs required for cutting-edge technologies; navigating complex and stringent global regulatory compliance for safety, reliability, and cybersecurity; and adapting to geopolitical trade tensions that can impact raw material sourcing, manufacturing locations, and market access, all of which necessitate robust strategic planning and adaptability from market participants.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.