ID : MRU_ 427910 | Date : Oct, 2025 | Pages : 253 | Region : Global | Publisher : MRU

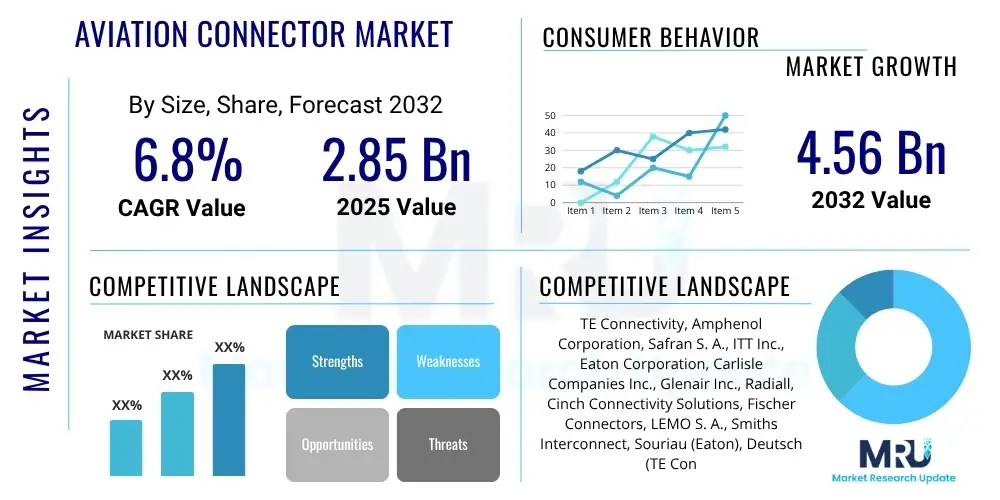

The Aviation Connector Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2032. The market is estimated at USD 2.85 billion in 2025 and is projected to reach USD 4.56 billion by the end of the forecast period in 2032.

The aviation connector market encompasses a critical segment within the broader aerospace industry, providing essential electrical, electronic, and fiber optic interconnect solutions for a vast array of airborne and ground support applications. These specialized connectors are engineered to meet the extremely rigorous demands of aviation environments, including extreme temperatures, vibration, shock, electromagnetic interference (EMI), and stringent safety regulations. Their primary function is to ensure reliable data transmission, power distribution, and signal integrity across complex aircraft systems, ranging from avionics and flight control to cabin entertainment and landing gear.

Aviation connectors are vital components that enable the functionality and safety of modern aircraft. They come in diverse forms, including circular, rectangular, RF, fiber optic, and hybrid configurations, each designed for specific performance requirements. Key features often include robust construction from advanced materials like aluminum alloys, stainless steel, and high-performance composites, alongside advanced sealing mechanisms to resist moisture, fuel, and other contaminants. The constant drive for lighter, more compact, and higher-performing aircraft necessitates continuous innovation in connector technology, leading to solutions that offer enhanced data rates, reduced weight, and improved durability.

Major applications for aviation connectors span the entire aviation ecosystem, including commercial aircraft, military jets, helicopters, business jets, unmanned aerial vehicles (UAVs), and emerging urban air mobility (UAM) platforms. Benefits derived from these connectors are numerous, fundamentally ensuring operational reliability, passenger safety, and mission success. The market is predominantly driven by increasing global air passenger traffic, new aircraft deliveries, the modernization of aging fleets, rising defense expenditures, and the continuous technological advancements in avionics and in-flight entertainment systems that demand more sophisticated and reliable interconnectivity.

The Aviation Connector Market is experiencing dynamic growth, propelled by several key business trends including the imperative for miniaturization, the demand for higher data transmission speeds, and the integration of lightweight, advanced materials. Manufacturers are increasingly focusing on developing modular and hybrid connector solutions that can accommodate multiple signal types (electrical, optical, data) within a single housing, optimizing space and reducing installation complexity. The industry is also witnessing a surge in research and development aimed at enhancing resistance to extreme environmental conditions, ensuring extended operational lifespans and reduced maintenance requirements. These trends are directly influenced by the evolving design philosophies of next-generation aircraft, which prioritize efficiency, connectivity, and reliability.

From a regional perspective, North America continues to be a dominant force in the aviation connector market, driven by a robust aerospace and defense industry, significant R&D investments, and a large installed base of commercial and military aircraft. However, the Asia Pacific region is rapidly emerging as a high-growth market, fueled by expanding economies, increasing air travel demand, and substantial investments in new aircraft procurement and airport infrastructure development, particularly in countries like China and India. Europe also maintains a strong market share, primarily due to the presence of major aircraft manufacturers like Airbus and a well-established MRO (Maintenance, Repair, and Overhaul) sector that consistently requires advanced connector solutions for fleet upgrades and servicing. Latin America, the Middle East, and Africa are showing steady growth, often driven by fleet modernization programs and the expansion of regional airlines.

Segmentation trends within the market highlight significant shifts towards specific connector types and applications. The fiber optic and hybrid connector segments are projected to experience accelerated growth due to the escalating demand for high-bandwidth data transmission in modern avionics, in-flight entertainment, and communication systems. Furthermore, connectors designed for specialized applications such as UAVs and space systems are seeing increased adoption, reflecting the rapid innovation and expansion in these emerging aerospace domains. The constant upgrade cycles for existing aircraft fleets also drive demand for connectors that offer backward compatibility alongside enhanced performance, emphasizing the market's dual focus on new installations and MRO activities.

The integration of Artificial Intelligence (AI) is poised to profoundly transform various facets of the aviation connector market, addressing common user concerns related to efficiency, reliability, and cost-effectiveness. Users are keenly interested in how AI can enhance predictive maintenance schedules for connectors, optimize design processes, and improve the accuracy of quality control during manufacturing. There is an expectation that AI will lead to more intelligent connector systems capable of self-monitoring and reporting, thereby minimizing downtime and extending operational lifespans. Furthermore, inquiries often revolve around AI's role in streamlining supply chain logistics for these highly specialized components, reducing lead times, and mitigating risks associated with component availability. The overall sentiment is one of anticipation for AI-driven solutions that will elevate the performance, safety, and economic viability of aviation interconnectivity.

AI's influence is anticipated across the entire lifecycle of aviation connectors, from initial design and development through manufacturing, maintenance, and end-of-life management. In the design phase, generative AI can explore vast parameter spaces to create optimized connector geometries and material compositions that meet stringent performance criteria while reducing weight and cost. During manufacturing, AI-powered vision systems and robotics can significantly enhance quality inspection processes, identifying micro-defects with unparalleled precision and consistency, thereby improving product reliability and reducing scrap rates. This leads to a more efficient and error-free production line, directly benefiting manufacturers and end-users.

For the operational phase, AI is expected to revolutionize predictive maintenance. By analyzing real-time data from embedded sensors within smart connectors – monitoring parameters like temperature, vibration, and signal degradation – AI algorithms can forecast potential failures before they occur. This shift from reactive to proactive maintenance can drastically reduce unscheduled downtime, lower maintenance costs, and enhance the overall safety of aircraft operations. Moreover, AI can optimize supply chain management by predicting demand fluctuations and identifying potential bottlenecks, ensuring a steady and timely supply of critical aviation connectors. This comprehensive impact underscores AI's potential to drive innovation and efficiency across the aviation connector value chain.

The Aviation Connector Market is shaped by a complex interplay of drivers, restraints, opportunities, and external impact forces. A primary driver is the continuous growth in global air passenger traffic, which necessitates an expansion of commercial aircraft fleets and consequently fuels demand for new connector installations. Coupled with this, significant global defense spending and modernization efforts for military aircraft fleets also contribute substantially to market growth. Technological advancements in avionics, in-flight entertainment, and high-speed data requirements further accelerate the demand for more sophisticated and reliable connector solutions capable of handling increased bandwidth and complex signals. The ongoing maintenance, repair, and overhaul (MRO) activities for aging aircraft fleets worldwide also represent a consistent demand driver, as connectors are regularly replaced or upgraded during routine servicing.

Despite robust growth drivers, the market faces notable restraints. The high cost associated with the research, development, and manufacturing of aviation-grade connectors is a significant barrier, largely due to the use of specialized materials and intricate production processes. More critically, the industry is subject to extremely stringent regulatory and certification requirements from bodies like the FAA and EASA, which impose long and costly qualification cycles for new products. This lengthy approval process can hinder innovation and slow down market entry for new technologies. Furthermore, the specialized nature of the supply chain, often involving a limited number of qualified suppliers, can lead to vulnerabilities, making the market susceptible to disruptions and price volatility.

Opportunities for growth are abundant, particularly in emerging aerospace segments. The rapid proliferation of Unmanned Aerial Vehicles (UAVs) across commercial, military, and recreational applications presents a burgeoning market for compact, lightweight, and high-performance connectors. Similarly, the nascent but rapidly developing Urban Air Mobility (UAM) sector, encompassing eVTOL aircraft, offers a substantial long-term growth avenue. Investments in satellite constellations and space exploration programs also necessitate highly specialized connectors capable of enduring the extreme conditions of space. Furthermore, the industry's increasing focus on sustainable aviation solutions and the adoption of advanced, lighter materials provide opportunities for connector manufacturers to innovate with eco-friendly and performance-optimized products. These opportunities highlight the dynamic future potential of the aviation connector market beyond traditional applications.

The market's landscape is also shaped by several impact forces. The bargaining power of buyers, primarily large aircraft OEMs and defense contractors, is considerable due to their scale and consolidated purchasing power, often leading to competitive pricing pressures. Conversely, the bargaining power of suppliers, especially for highly specialized raw materials or unique components, can be significant due to limited alternative sources. The threat of new entrants is relatively low owing to the high capital investment, technological expertise, and stringent regulatory hurdles required to compete effectively. However, the threat of substitutes, while traditionally low for core aviation applications, could emerge from entirely new wireless technologies or integrated systems that reduce the need for physical connectors in certain contexts, pushing manufacturers to continuously innovate. Intense competitive rivalry among established players also drives product differentiation and technological advancement.

The Aviation Connector Market is intricately segmented based on various critical parameters, reflecting the diverse applications and technical requirements within the aerospace industry. These segmentations provide a granular view of market dynamics, enabling stakeholders to identify key growth areas and understand the evolving demands from different end-users and technological advancements. A comprehensive analysis across these segments reveals the underlying trends driving innovation and investment across the entire aviation connector ecosystem, from raw material selection to final product integration in complex aircraft systems.

The value chain for the Aviation Connector Market is a complex, multi-tiered structure that begins with the sourcing of specialized raw materials and culminates in the integration of finished connector products into sophisticated aircraft systems. Upstream analysis highlights a critical reliance on suppliers of high-performance metals such as aluminum, stainless steel, and various copper alloys, along with advanced polymer composites and ceramics, all of which must meet aerospace-grade specifications for strength, durability, and resistance to extreme environments. These raw material providers feed into a specialized component manufacturing segment responsible for producing pins, sockets, housings, insulators, and seals, requiring precision engineering and adherence to strict quality controls. The integrity of this upstream segment is paramount as it forms the foundational quality for the entire connector system, influencing overall reliability and safety.

Further along the value chain, these components are assembled by aviation connector manufacturers who leverage highly automated and specialized processes to produce the final interconnect solutions. These manufacturers often engage in extensive research and development to innovate new designs that meet evolving aerospace standards and requirements for miniaturization, higher data rates, and enhanced environmental sealing. Once manufactured, the finished aviation connectors move into the downstream segment, where they are integrated into larger sub-systems and platforms by major Original Equipment Manufacturers (OEMs) such as aircraft manufacturers (e.g., Boeing, Airbus), engine manufacturers (e.g., GE Aviation, Rolls-Royce), and avionics suppliers (e.g., Honeywell, Thales). Beyond initial OEM integration, the downstream market also includes Maintenance, Repair, and Overhaul (MRO) providers and defense contractors, who require connectors for fleet upgrades, repairs, and routine servicing of existing aircraft.

The distribution channel for aviation connectors primarily involves both direct and indirect approaches. Direct sales are common for large volume orders and highly customized solutions, where connector manufacturers work directly with major OEMs and Tier 1 suppliers to ensure precise specification adherence and technical support. This direct engagement fosters deep relationships and facilitates collaborative design efforts. Indirect distribution channels typically involve a network of specialized aerospace distributors and value-added resellers who maintain inventories of standard connectors and offer logistical support to a wider array of customers, including smaller MRO facilities, general aviation manufacturers, and defense sub-contractors. This dual-channel approach ensures market penetration across different customer segments, catering to both the high-volume, custom needs of major players and the broader, more standardized requirements of the wider aerospace ecosystem, while ensuring strict traceability and quality assurance throughout the supply chain.

The Aviation Connector Market serves a diverse yet highly specialized customer base, primarily comprised of entities deeply embedded within the aerospace and defense sectors. At the forefront are the major commercial aircraft manufacturers, such as Boeing, Airbus, Embraer, and Bombardier, who integrate vast quantities of connectors into every aspect of new aircraft production, from fuselage wiring to sophisticated avionics suites. These OEMs demand connectors that offer unparalleled reliability, lightweight design, and compliance with stringent aviation standards. Similarly, engine manufacturers like GE Aviation, Rolls-Royce, and Safran S. A. represent significant buyers, requiring specialized connectors for engine control units and sensor systems that can withstand extreme temperatures and vibrations.

Beyond the primary aircraft and engine manufacturers, a substantial segment of potential customers includes leading avionics and sub-system suppliers such as Honeywell, Thales, Collins Aerospace, and Leonardo S.p.A. These companies integrate connectors into their navigation systems, communication equipment, flight control computers, and in-flight entertainment systems. The defense sector also constitutes a critical customer segment, with national defense organizations and military aircraft manufacturers requiring robust, high-performance connectors for fighter jets, transport aircraft, helicopters, and advanced weapon systems, often with added requirements for ruggedization, EMI shielding, and security features. The MRO (Maintenance, Repair, and Overhaul) industry forms another vital customer group, as airlines and third-party MRO providers continuously purchase replacement and upgrade connectors for the maintenance and servicing of existing aircraft fleets, ensuring ongoing airworthiness and operational efficiency.

Emerging segments within the aviation industry are also expanding the customer base. Manufacturers of Unmanned Aerial Vehicles (UAVs) and drones, for both military and commercial applications, are rapidly increasing their demand for compact, lightweight, and high-performance connectors. The burgeoning Urban Air Mobility (UAM) sector, with companies developing eVTOL (electric Vertical Take-Off and Landing) aircraft, represents a future growth area, seeking innovative connector solutions for electric propulsion systems and integrated flight controls. Furthermore, space agencies and private space companies developing rockets, satellites, and spacecraft require ultra-reliable, radiation-hardened connectors capable of functioning in the harsh vacuum of space. These diverse end-users collectively underscore the broad and critical role of aviation connectors across the entire aerospace ecosystem, each with unique technical and logistical requirements.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 2.85 Billion |

| Market Forecast in 2032 | USD 4.56 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | TE Connectivity, Amphenol Corporation, Safran S. A., ITT Inc., Eaton Corporation, Carlisle Companies Inc., Glenair Inc., Radiall, Cinch Connectivity Solutions, Fischer Connectors, LEMO S. A., Smiths Interconnect, Souriau (Eaton), Deutsch (TE Connectivity), Molex, JAE, Nexans, Aptiv, Conesys, Interpoint (Crane Aerospace & Electronics) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Aviation Connector Market is characterized by a relentless pursuit of technological advancement, driven by the aerospace industry's demand for ever-increasing performance, reliability, and efficiency. A primary focus in the technology landscape is miniaturization, where manufacturers strive to reduce the size and weight of connectors without compromising electrical performance or environmental ruggedness. This is crucial for modern aircraft that require more systems and wiring in confined spaces, contributing directly to fuel efficiency and payload capacity. Concurrently, there is a significant push towards developing connectors capable of high-speed data transmission, supporting protocols like Gigabit Ethernet, Fiber Channel, and USB 3.0/4.0, which are essential for advanced avionics, sophisticated in-flight entertainment systems, and real-time data exchange across aircraft networks. This emphasis on high-bandwidth capabilities is transforming traditional wiring architectures.

Another critical area of technological innovation revolves around harsh environment sealing and protection. Aviation connectors must reliably operate in conditions involving extreme temperatures, high vibration, intense shock, pressure variations, and exposure to various fluids like fuel, hydraulic fluid, and de-icing chemicals. Manufacturers are continuously developing advanced sealing technologies, corrosion-resistant platings, and robust housing materials, including high-performance composites and specialized alloys, to ensure long-term durability and operational integrity. Furthermore, effective electromagnetic interference (EMI) and radio frequency interference (RFI) shielding are paramount for maintaining signal integrity in electrically noisy aircraft environments, leading to the development of sophisticated shielding solutions integrated directly into connector designs. These advancements are vital for protecting sensitive electronic systems from external disturbances.

The technology landscape also includes the evolution of modular and hybrid connector designs, which allow for the integration of multiple signal types—power, data, and fiber optics—into a single connector housing. This modularity simplifies wiring harnesses, reduces installation time, and enhances system flexibility. The emergence of intelligent or "smart" connectors, incorporating embedded sensors, processors, and communication capabilities, represents a future trend. These smart connectors could potentially monitor their own health, environmental conditions, and signal quality, providing real-time data for predictive maintenance and system diagnostics. Such innovations are poised to redefine the role of connectors, moving them beyond passive components to active elements within an integrated, networked aircraft ecosystem, thereby enhancing safety, reliability, and maintenance efficiency.

Aviation connectors are specialized electrical, electronic, and fiber optic interconnects designed for aircraft and aerospace applications, ensuring reliable data, signal, and power transmission in harsh environments. They are critical for safety and operational integrity.

Key drivers include rising global air passenger traffic, increasing new aircraft deliveries, modernization of aging fleets, growing defense expenditures, and continuous technological advancements in avionics and in-flight entertainment systems.

Major trends involve miniaturization, high-speed data transmission capabilities (e.g., Gigabit Ethernet), enhanced harsh environment sealing, EMI/RFI shielding, use of lightweight composite materials, modular/hybrid designs, and the development of intelligent, sensor-equipped connectors.

North America currently holds the largest market share due to its robust aerospace and defense industry. However, the Asia Pacific region is projected to be the fastest-growing market, driven by expanding aviation sectors in countries like China and India.

AI is transforming the market through generative design for optimization, enhanced quality control in manufacturing, predictive maintenance capabilities for in-service connectors, and improved supply chain management. This leads to more reliable and efficient interconnect solutions.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.