ID : MRU_ 428148 | Date : Oct, 2025 | Pages : 253 | Region : Global | Publisher : MRU

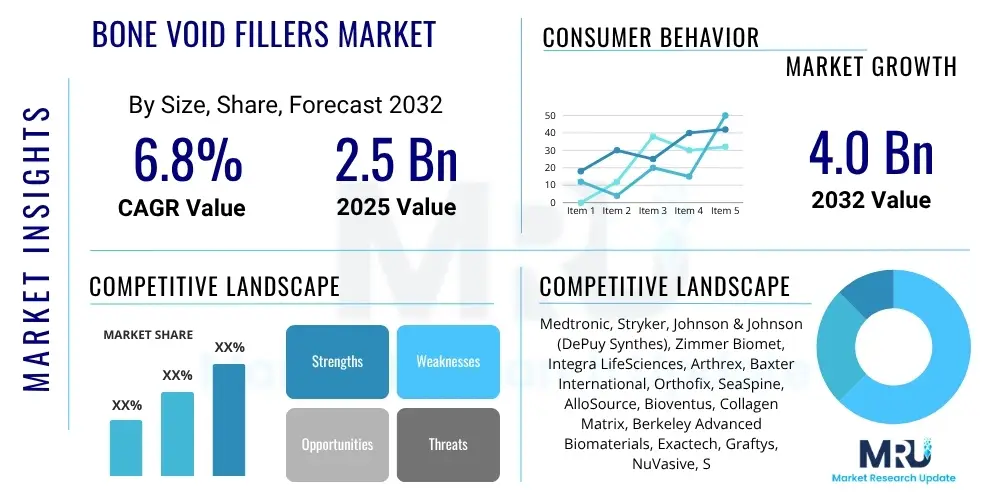

The Bone Void Fillers Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2032. The market is estimated at US$ 2.5 billion in 2025 and is projected to reach US$ 4.0 billion by the end of the forecast period in 2032. This robust growth trajectory is underpinned by an escalating global demand for advanced orthopedic and dental treatments, coupled with an aging population and increasing incidence of bone-related disorders. The continuous innovation in biomaterials and surgical techniques further solidifies this market's expansion.

Bone void fillers are specialized biocompatible materials designed to fill bone defects, promote osteogenesis (new bone formation), and provide structural support in various surgical procedures. These crucial medical devices serve as scaffolds that facilitate the natural healing process, integrating seamlessly with existing bone tissue to restore anatomical function and integrity. Their application spans a wide array of medical disciplines, primarily orthopedics, dentistry, and spinal surgery, where they address challenges such as non-union fractures, bone loss due to trauma or disease, and skeletal reconstruction. The evolution of bone void fillers has moved from rudimentary grafting techniques to sophisticated biomaterials, offering improved efficacy and reduced patient morbidity. Product descriptions generally categorize these fillers into allografts (derived from human donors), xenografts (derived from animal sources), and synthetic materials (such as calcium phosphates, bioactive glass, and polymers), each presenting unique advantages in terms of biocompatibility, osteoconductivity, and mechanical properties, thereby catering to diverse clinical requirements and patient profiles with enhanced precision and reliability.

Major applications of bone void fillers are predominantly found in spinal fusion surgeries, where they are critical for promoting vertebral stability and fusing adjacent bones, significantly improving patient outcomes for conditions like degenerative disc disease or scoliosis. In joint reconstruction procedures, particularly for hip and knee arthroplasty, these fillers are vital for addressing bone defects and ensuring secure implant fixation. Orthopedic trauma and extremities repair also heavily rely on bone void fillers to mend complex fractures, especially those involving significant bone loss, accelerating recovery and mitigating complications. Furthermore, in the field of dental bone grafting, these materials are indispensable for procedures such as alveolar ridge augmentation, sinus lifts, and the regeneration of periodontal defects, which are crucial for successful dental implant placement and restoration of oral health, thus expanding their utility across diverse surgical landscapes and patient needs.

The benefits associated with the use of bone void fillers are substantial, encompassing reduced surgical time, decreased incidence of donor site morbidity (a common issue with autografts), and faster patient recovery rates. These materials provide a reliable alternative to traditional autografts, which are often limited by supply and necessitate an additional surgical site. Driving factors for market growth include a rapidly expanding global geriatric population, inherently prone to osteoporosis, fractures, and degenerative joint diseases, which mandates a higher volume of reconstructive surgeries. An increasing prevalence of chronic orthopedic conditions, sports-related injuries, and traumatic accidents further propels the demand for effective bone regeneration solutions. Moreover, continuous advancements in biomaterials science, leading to the development of more effective, customizable, and safer bone void fillers, along with the growing adoption of minimally invasive surgical techniques, which favor injectable and easily manipulable filler forms, are pivotal in fostering the sustained expansion and innovation within this critical medical device market.

The Bone Void Fillers Market is experiencing a period of significant expansion and innovation, characterized by evolving business trends that underscore a strategic focus on research and development, particularly in the realm of synthetic and biologically active materials. Key players are increasingly engaging in strategic collaborations, mergers, and acquisitions to consolidate market share, leverage complementary technologies, and expand their geographical footprint. This consolidation aims to enhance product portfolios with advanced solutions that offer superior osteoconductive and osteoinductive properties, catering to the growing demand for more efficient and predictable bone regeneration. Manufacturers are prioritizing the development of customizable, resorbable, and injectable fillers, which align with the trend towards minimally invasive surgical procedures and patient-specific treatments, thereby enhancing market competitiveness and driving product differentiation.

Regional trends indicate North America and Europe as the dominant markets, primarily due to their robust healthcare infrastructures, high healthcare expenditure, and a large geriatric population base that contributes significantly to the incidence of orthopedic and spinal disorders. These regions also benefit from advanced research capabilities and favorable reimbursement policies, which support the adoption of innovative bone void filler technologies. However, the Asia Pacific region is rapidly emerging as a high-growth market, propelled by improving economic conditions, increasing investments in healthcare infrastructure, a burgeoning medical tourism sector, and a growing awareness among both patients and healthcare professionals about advanced treatment options. Countries like China, India, and Japan are at the forefront of this regional expansion, driven by their large populations and the rising demand for orthopedic and dental surgeries. Latin America and the Middle East & Africa also present promising growth opportunities, albeit from a smaller base, as healthcare access and technological adoption steadily improve.

Segment-wise, the market is witnessing dynamic shifts. Synthetic bone void fillers, including calcium phosphates, bioactive glass, and polymers, are projected to experience substantial growth. This growth is attributable to their consistent availability, reduced risk of disease transmission compared to allografts, and the ability to be engineered with tailored properties such as specific resorption rates and mechanical strengths. While allografts continue to hold a significant market share due to their proven efficacy and biological compatibility, challenges related to supply chain management and processing complexity drive innovation towards synthetic alternatives. The application segment sees spinal fusion and orthopedic trauma remaining as primary areas of demand, with dental bone grafting also showing robust expansion. The increasing adoption of advanced materials and technologies across these segments reflects a concerted effort to enhance clinical outcomes, reduce complications, and improve the overall efficiency of bone regeneration therapies, ultimately shaping the market's future trajectory.

User inquiries concerning the influence of Artificial Intelligence (AI) on the Bone Void Fillers Market predominantly center on its potential to revolutionize personalized treatment approaches, optimize material science, and enhance diagnostic precision. Common questions explore how AI could facilitate the design of patient-specific bone scaffolds, predict the most effective filler type for individual healing profiles, and automate the analysis of complex medical imaging for pre-operative planning and post-operative monitoring. Users are keenly interested in AI's role in accelerating the discovery and development of novel biomaterials through predictive modeling and high-throughput screening, significantly reducing the traditional R&D timeline. While enthusiasm for AI's capabilities is high, concerns are also voiced regarding the ethical implications of data privacy, the imperative for robust validation of AI algorithms in clinical settings to ensure safety and efficacy, and the potential need for extensive training among healthcare professionals to integrate these advanced tools into daily practice. The collective expectation is that AI will be a transformative force, leading to more predictable, efficient, and highly individualized bone regeneration therapies that improve patient outcomes and redefine the standard of care in orthopedic and regenerative medicine.

The Bone Void Fillers Market is experiencing substantial momentum driven by several powerful factors. Primarily, the accelerating growth of the global geriatric population is a paramount driver, as older individuals are significantly more susceptible to degenerative bone diseases such as osteoporosis, osteoarthritis, and age-related fractures, necessitating advanced reconstructive and regenerative surgical interventions. Concurrently, the increasing worldwide prevalence of orthopedic conditions, sports-related injuries, and traumatic accidents, often resulting in complex bone defects and significant bone loss, further fuels the demand for effective and reliable bone void fillers. Technological advancements in biomaterials science represent another critical driver, with continuous research and development leading to the creation of more sophisticated, biocompatible, and osteoinductive synthetic and allograft-based fillers that offer superior clinical outcomes. Moreover, the growing adoption of minimally invasive surgical (MIS) techniques across orthopedic and spinal procedures acts as a significant catalyst, as these procedures often favor injectable and moldable bone void fillers, which align with the objectives of reduced patient morbidity, faster recovery times, and improved surgical efficiency.

Despite the strong growth drivers, the market navigates several notable restraints. A significant impediment is the relatively high cost associated with advanced bone void fillers and the intricate surgical procedures required for their application. This can limit their accessibility and adoption, particularly in emerging economies or for patients without comprehensive insurance coverage, leading to disparities in treatment. Furthermore, stringent and often prolonged regulatory approval processes for new biomaterials and therapeutic devices impose considerable financial and time burdens on manufacturers, potentially delaying market entry and stifling innovation. Concerns regarding potential post-operative complications, though generally rare, such as infection at the surgical site, immune responses to graft materials, or unpredictable material degradation, can sometimes create hesitancy among both clinicians and patients. Additionally, the inherent limitations in the supply of allograft materials, coupled with ethical and processing complexities related to donor tissue procurement and sterilization, present ongoing challenges for segments reliant on human-derived bone fillers, prompting a greater emphasis on synthetic alternatives.

Notwithstanding these restraints, the Bone Void Fillers Market is replete with significant opportunities for future expansion and innovation. The untapped potential in emerging economies, characterized by rapidly developing healthcare infrastructures, increasing healthcare expenditure, and a growing patient awareness regarding advanced medical treatments, presents a substantial avenue for market penetration and growth. The advent of personalized medicine, leveraging advanced diagnostics and manufacturing technologies like 3D printing, offers a promising frontier for developing custom-fit bone void fillers tailored to individual patient anatomies and specific defect characteristics, thereby enhancing surgical precision and clinical efficacy. Moreover, the synergistic integration of biologics, such as growth factors (e.g., bone morphogenetic proteins), stem cells, or platelet-rich plasma, with existing bone void filler technologies to create innovative combination products with superior osteoinductive properties, represents a pivotal opportunity to significantly improve bone regeneration outcomes. The increasing educational initiatives and growing awareness among healthcare professionals about the distinct advantages and clinical benefits of modern bone void fillers over conventional grafting methods are expected to drive greater adoption and expand the market's reach into new clinical indications and geographical regions, fostering sustained market evolution and development.

The Bone Void Fillers Market is intricately segmented across various dimensions, including material type, form, application, and end-user, providing a comprehensive framework for understanding market dynamics and identifying distinct growth opportunities. This detailed segmentation is crucial for market participants to tailor their product development strategies and marketing efforts to specific clinical requirements and patient populations. The categorization by material type, ranging from biological grafts to advanced synthetic compounds, highlights the diverse therapeutic options available, each with its own set of advantages regarding biocompatibility, osteoconductivity, and mechanical strength, thus influencing adoption rates and market share across different surgical specialties and geographical regions.

Further segmentation by the physical form of the filler, such as injectable pastes, moldable putties, granules, or pre-formed strips, directly impacts its ease of surgical application, suitability for various defect sizes and anatomical locations, and compatibility with minimally invasive techniques. This characteristic is paramount for surgeons seeking optimal handling properties and efficient integration within complex surgical environments. Moreover, the broad spectrum of applications, from critical spinal fusion procedures to intricate dental bone grafting, underscores the versatility and indispensable role of bone void fillers in addressing a wide array of bone-related pathologies. Analyzing these segmentations allows for a granular assessment of demand patterns, competitive landscapes, and technological preferences, enabling stakeholders to strategically position their offerings and capitalize on specific unmet clinical needs within the continuously evolving global healthcare ecosystem.

The value chain for the Bone Void Fillers Market is a multi-faceted process beginning with sophisticated upstream activities centered on raw material sourcing, extensive research and development (R&D), and initial processing. This critical phase involves the meticulous procurement and handling of diverse raw materials, which include human bone tissue for allografts, animal bone for xenografts, and the precise chemical synthesis of various inorganic and organic compounds for synthetic fillers like calcium phosphates, bioactive glass, and biodegradable polymers. Manufacturers invest heavily in R&D to innovate biomaterial compositions, enhance critical properties such as osteoconductivity, osteoinductivity, and biodegradability, and to develop novel delivery systems that improve surgical efficacy. Stringent quality control measures and rigorous adherence to international regulatory standards, including those from organizations like the FDA and EMA, are paramount at this stage to ensure product safety, efficacy, and batch consistency, minimizing risks and ensuring the foundational integrity of the final product.

Moving downstream, the value chain encompasses the specialized manufacturing, meticulous packaging, and rigorous sterilization of bone void filler products, followed by their strategic distribution to a global network of healthcare providers. Manufacturing processes are often highly specialized, involving techniques such as lyophilization for allografts, precision molding for synthetic materials to achieve specific porosities, and various methods for incorporating bioactive agents. Robust, sterile packaging is crucial to maintain product integrity and prevent contamination during storage and transit. The distribution channel is a complex network involving a combination of global wholesalers, regional distributors, and direct sales teams. These entities are responsible for efficiently delivering products to end-users, which include major hospitals, ambulatory surgical centers (ASCs), and specialized orthopedic and dental clinics worldwide. Effective supply chain management is indispensable to ensure timely product availability, manage inventory, and respond promptly to dynamic market demands, particularly considering the often critical and time-sensitive nature of surgical supplies.

Both direct and indirect distribution channels play pivotal roles in the market's reach. Direct sales involve manufacturers establishing direct relationships with large hospital networks, academic medical centers, and key opinion leaders, providing technical support, product training, and direct procurement options. This approach allows for greater control over brand messaging and fosters deeper clinical relationships. Indirect channels, on the other hand, leverage third-party distributors who possess established logistical networks, local market knowledge, and sales expertise. These partners are instrumental in penetrating diverse geographical regions, reaching smaller healthcare facilities, and navigating complex local regulatory landscapes. The success of these intricate distribution strategies relies heavily on strong collaborative relationships, highly efficient logistical operations, comprehensive product education for end-users, and robust post-market surveillance. This ensures that the appropriate bone void filler solutions are available at the right place and time for optimal patient care, while also addressing market-specific requirements and competition effectively.

The primary potential customers and end-users for products within the Bone Void Fillers Market represent a broad and diverse spectrum of medical professionals and healthcare institutions deeply involved in orthopedic, spinal, dental, and craniomaxillofacial surgical specialties. Orthopedic surgeons constitute a core and substantial segment, extensively utilizing these advanced materials for a wide range of procedures, including complex fracture repair, intricate joint reconstruction, tumor resection, and the treatment of various bone defects arising from trauma or degenerative diseases. Similarly, spinal surgeons are critical consumers, relying on bone void fillers as an indispensable component in fusion procedures aimed at promoting robust vertebral stability and encouraging new bone growth to alleviate pain and restore spinal function. Beyond these, dentists and oral maxillofacial surgeons represent another significant end-user group, applying these materials for crucial procedures such as alveolar ridge augmentation, sinus lifts, and the regeneration of periodontal defects, all of which are vital for the successful placement of dental implants and the comprehensive restoration of oral health and aesthetics.

In addition to individual medical practitioners, healthcare institutions form a substantial customer base. Hospitals, particularly those with well-established orthopedic, trauma, and surgical departments, are major purchasers due to the high volume and complexity of surgeries performed that necessitate diverse types of bone void fillers. These large facilities often have dedicated procurement departments responsible for evaluating and acquiring medical devices based on clinical efficacy, safety profiles, cost-effectiveness, and supplier reliability. Ambulatory surgical centers (ASCs) are an increasingly important and rapidly growing segment of end-users, as more orthopedic and spinal procedures transition to outpatient settings, driven by their efficiency, lower costs, and patient convenience. Specialized orthopedic clinics and dental clinics also represent a significant customer segment, catering to specific patient populations with distinct bone regeneration needs, ranging from routine bone grafting to more complex reconstructive interventions, thereby expanding the market's reach across various care settings.

Ultimately, the overarching objective of these end-users and buyers is to significantly improve patient outcomes, substantially reduce recovery times, and consistently enhance the overall success rates of surgical interventions. Their purchasing decisions are profoundly influenced by a confluence of factors, including robust clinical evidence and peer-reviewed studies demonstrating product efficacy, positive recommendations from key opinion leaders, continuous product innovations that offer superior performance, and strict adherence to regulatory compliance. The dynamic landscape of healthcare economics, marked by evolving reimbursement policies and increasing pressure to optimize costs, coupled with a growing societal demand for minimally invasive procedures and increasingly personalized treatment options, continuously shapes the procurement patterns, product preferences, and strategic decisions of these critical customer segments within the highly competitive Bone Void Fillers Market, driving ongoing demand for advanced and effective solutions.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | US$ 2.5 billion |

| Market Forecast in 2032 | US$ 4.0 billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Medtronic, Stryker, Johnson & Johnson (DePuy Synthes), Zimmer Biomet, Integra LifeSciences, Arthrex, Baxter International, Orthofix, SeaSpine, AlloSource, Bioventus, Collagen Matrix, Berkeley Advanced Biomaterials, Exactech, Graftys, NuVasive, Smith & Nephew, OrthoPediatrics, Wright Medical Group N.V., Advanced Biologics. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Bone Void Fillers Market is characterized by a rapidly evolving and highly innovative technology landscape, driven by continuous advancements in biomaterials science, tissue engineering, and surgical methodologies. A primary focus of technological development revolves around creating materials that intimately mimic the structural and biological properties of native bone, thereby offering superior osteoconductivity, osteoinductivity, and precise biodegradability. This includes sophisticated formulations of synthetic materials such as advanced calcium phosphate cements (e.g., highly porous hydroxyapatite and tricalcium phosphate composites), which not only provide a stable scaffold for new bone growth but also resorb over a predictable timeframe, allowing for gradual replacement by host bone. Bioactive glasses and ceramics are also at the forefront, renowned for their ability to form strong chemical bonds with surrounding bone tissue and actively stimulate cellular activity, accelerating the healing process through their unique ion-release mechanisms that encourage osteoblast proliferation and differentiation.

Furthermore, the integration of cutting-edge manufacturing techniques, most notably 3D printing and various additive manufacturing processes, is profoundly transforming the production of bone void fillers. These advanced technologies enable the fabrication of customized, patient-specific implants with highly intricate and controlled pore architectures, which are optimized for cell infiltration, vascularization, and nutrient exchange, significantly enhancing the regenerative potential. The development of sophisticated composite materials, which strategically combine different types of biomaterials—suchfor example, integrating the mechanical strength of ceramics with the flexibility of biodegradable polymers, or embedding growth factors and antibiotics—represents another significant technological trend. These synergistic approaches aim to leverage the distinct advantages of multiple components to achieve superior healing outcomes, including enhanced mechanical integrity, modulated resorption kinetics, and potent antimicrobial properties, addressing a wider range of clinical challenges with increased efficacy and precision.

The technological landscape also encompasses significant efforts in enhancing the intrinsic biological activity of bone void fillers, moving beyond mere passive osteoconduction. This involves innovative surface modification techniques, such as plasma treatment or biomimetic coatings, designed to actively promote cell adhesion, proliferation, and differentiation. A particularly promising area is the sophisticated incorporation of biologics, which includes loading fillers with recombinant growth factors (e.g., bone morphogenetic proteins), autologous stem cells, or even gene therapy vectors to actively stimulate bone formation and accelerate healing at the cellular and molecular levels. Additionally, the continuous refinement of injectable and minimally invasive delivery systems, utilizing advanced syringes, cannulas, and catheters, represents a crucial technological frontier. These systems facilitate easier, more precise, and less invasive application of bone void fillers during surgery, thereby contributing to reduced surgical trauma, decreased patient morbidity, and accelerated post-operative recovery times. The relentless pursuit of materials that offer greater versatility, predictability, and biological efficacy continues to drive profound innovation across this highly competitive and clinically essential market segment.

Bone void fillers are biocompatible materials used in surgical procedures, primarily orthopedic and dental, to fill bone defects, promote new bone growth, and provide structural stability, ultimately facilitating faster and more complete healing of bone tissue.

The primary categories include allografts (human donor bone), xenografts (animal donor bone), and synthetic materials such as calcium phosphates, bioactive glass, and various polymers, each offering unique biological and mechanical properties for diverse clinical needs.

Bone void fillers are extensively used in spinal fusion, joint reconstruction (e.g., hip and knee), repair of orthopedic trauma and complex fractures, and a range of dental bone grafting procedures like alveolar ridge augmentation and sinus lifts.

AI is impacting the market by enabling the design of personalized bone void fillers, optimizing material composition for enhanced efficacy, aiding in precise surgical planning through advanced imaging analysis, and accelerating the research and development of novel biomaterials.

Market growth is primarily driven by an aging global population, the rising incidence of orthopedic conditions and injuries, continuous advancements in biomaterials technology, and the increasing adoption of minimally invasive surgical techniques that favor these advanced solutions.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.