ID : MRU_ 429631 | Date : Nov, 2025 | Pages : 257 | Region : Global | Publisher : MRU

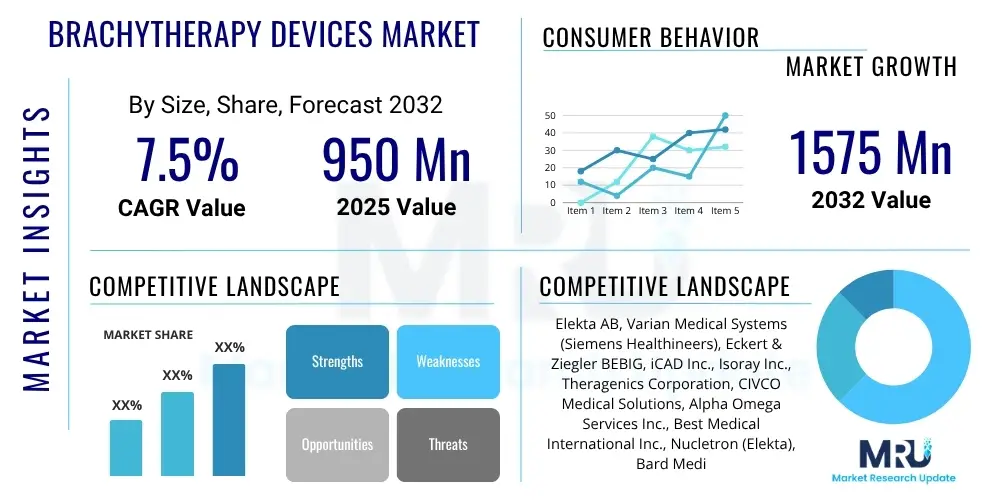

The Brachytherapy Devices Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2025 and 2032. The market is estimated at $950 million in 2025 and is projected to reach $1575 million by the end of the forecast period in 2032.

The Brachytherapy Devices Market encompasses a highly specialized segment within medical technology, focused on instruments and radioactive sources essential for delivering brachytherapy, an advanced form of internal radiation therapy. This therapeutic modality involves the precise placement of radioactive materials directly into or in close proximity to the cancerous tumor, ensuring a concentrated dose of radiation directly to the malignant cells while concurrently minimizing exposure to surrounding healthy tissues and organs. Brachytherapy is widely recognized for its unparalleled precision, remarkable efficacy, and significantly shorter treatment durations when compared to conventional external beam radiation therapy, solidifying its position as a highly desirable and often preferred treatment option across a spectrum of diverse cancer types.

The product landscape within this dynamic market is extensive and includes sophisticated high-dose-rate (HDR) afterloaders, which are robotic systems designed for automated and remote delivery of powerful radioactive sources. It also comprises low-dose-rate (LDR) seeds, which are small, encapsulated radioactive sources implanted permanently or temporarily. Complementing these core devices are a variety of precision applicators, flexible catheters, and advanced software solutions crucial for meticulous treatment planning and flawless radiation delivery. These tools collectively empower clinicians to tailor treatments with exceptional accuracy, offering a versatile arsenal against various oncological conditions.

Brachytherapy finds major applications across a broad range of oncological conditions, prominently including prostate cancer, breast cancer, various gynecological cancers such as cervical and endometrial carcinomas, head and neck cancers, and specific types of skin cancers. The overarching benefits derived from employing brachytherapy are manifold: they include highly targeted radiation delivery that spares critical organs, superior local control rates of the tumor, a marked reduction in systemic and localized side effects, and enhanced convenience for patients due largely to shorter overall treatment schedules. The market's robust growth is fundamentally driven by the alarming increase in the global incidence of cancer, the heightened awareness and accelerating adoption of brachytherapy due to its clinical advantages, continuous technological advancements that yield more precise and safer devices, and the demographic shift towards an aging global population, which inherently possesses a higher susceptibility to developing various forms of cancer, further solidifying the market's trajectory.

The Brachytherapy Devices Market is currently experiencing a period of significant expansion, underpinned by the escalating worldwide prevalence of cancer and relentless innovation within the field of radiation oncology. Contemporary business trends indicate a pronounced strategic pivot towards the development of highly advanced HDR (High-Dose-Rate) systems, which offer enhanced treatment control and flexibility. There is also a strong emphasis on the seamless integration of real-time imaging technologies (such as ultrasound, CT, and MRI) directly into brachytherapy procedures, allowing for unprecedented accuracy in applicator and source placement. Furthermore, considerable efforts are being directed towards creating sophisticated, AI-driven personalized treatment planning software. These innovations collectively aim to drastically improve treatment precision, optimize patient outcomes, and enhance the overall efficiency of oncology workflows. Strategic alliances, partnerships, and collaborations between leading device manufacturers, academic institutions, and healthcare providers are increasingly common, serving as critical mechanisms for expanding market reach, accelerating technological adoption, and ultimately improving patient access to these cutting-edge therapies on a global scale. Concurrently, a discernible shift towards minimally invasive procedural techniques and outpatient treatment settings is profoundly influencing product design and service delivery models within the brachytherapy industry, placing a premium on efficiency, patient comfort, and reduced hospital stays.

Analysis of regional trends reveals that North America and Europe currently represent the most mature and dominant markets for brachytherapy devices. This leadership position is primarily attributable to the presence of highly advanced and well-established healthcare infrastructures, consistently high adoption rates of sophisticated cancer treatments, and substantial ongoing investments in research and development activities aimed at refining radiation oncology techniques. These regions benefit from strong regulatory frameworks that support innovation and a population that is well-informed and actively seeking advanced therapeutic options. Conversely, the Asia Pacific region is rapidly emerging as a high-growth frontier within the global brachytherapy market. This accelerating growth is predominantly fueled by a confluence of factors including a burgeoning increase in healthcare expenditure across the region, a rapidly expanding burden of cancer cases attributed to demographic shifts and lifestyle changes, and significantly improving access to modern medical technologies as economies develop and healthcare policies become more progressive. Emerging markets in Latin America, the Middle East, and Africa are also presenting nascent yet promising opportunities for market expansion, albeit with a generally slower rate of adoption, driven by incremental improvements in healthcare awareness, expanding medical infrastructure, and a growing recognition of brachytherapy’s clinical benefits.

Segmentation-specific trends further illuminate market dynamics. The high-dose-rate (HDR) brachytherapy segment continues to exert dominance, primarily due to its inherent advantages in terms of treatment convenience, flexible fractionation schedules, and proven clinical efficacy for a wide array of cancers. However, low-dose-rate (LDR) brachytherapy, particularly with permanent seed implants, maintains a crucial and well-defined niche, especially in the treatment of early-stage prostate cancer, where it offers excellent long-term control rates with minimal disruption to patient lifestyle. From an application perspective, prostate cancer treatment consistently remains the largest and most significant segment within the market. Nevertheless, applications in breast cancer and various gynecological cancers are demonstrating particularly strong and accelerated growth, driven by increasing clinical evidence supporting brachytherapy's role in these indications and the development of specialized applicators. In terms of end-users, hospitals, particularly large university-affiliated medical centers and specialized cancer treatment facilities, continue to be the primary consumers of brachytherapy devices. There is also a discernible trend towards the establishment of integrated oncology care facilities and dedicated outpatient cancer clinics, which emphasizes a comprehensive, patient-centric approach to cancer management, often integrating brachytherapy into multimodal treatment plans.

Common user questions consistently revolve around the transformative potential of artificial intelligence in revolutionizing the precision, efficiency, and accessibility of brachytherapy treatments. A significant portion of user inquiries centers on how AI can fundamentally optimize various stages of the brachytherapy workflow, from initial treatment planning and dose calculation to real-time image guidance during the procedure itself. Users also frequently express interest in AI's capacity to predict individual patient outcomes and potential toxicities, thereby enabling highly personalized therapeutic approaches. Furthermore, there is considerable interest in how AI can streamline clinical workflows, automate repetitive tasks, and ultimately reduce the cognitive load on healthcare professionals. Concerns raised often touch upon critical issues such as the robust validation and regulatory approval pathways required for AI-powered medical devices, ensuring absolute patient safety and efficacy. Additionally, data privacy, the potential for algorithmic bias, and the necessity for extensive clinical evidence to support AI's widespread adoption are frequently highlighted. Despite these concerns, expectations are overwhelmingly positive, with users anticipating that AI will significantly shorten the laborious treatment planning process, substantially improve dose conformity to the tumor while sparing healthy tissues, and facilitate the development of more adaptive and patient-specific treatment strategies. Ultimately, it is widely expected that AI integration will lead to superior therapeutic results, a reduction in adverse side effects, and an overall enhanced patient experience for individuals undergoing brachytherapy.

The Brachytherapy Devices Market is primarily propelled by a confluence of powerful drivers, most notably the escalating global incidence of various malignant cancers. The relentless rise in diagnoses for prostate cancer, breast cancer, and gynecological cancers, among others, creates an urgent and expanding demand for highly effective and precisely targeted radiation therapies. This increasing patient burden acts as a fundamental impetus for market growth. Concurrently, a continuous stream of technological advancements, manifesting in the development of increasingly sophisticated high-dose-rate (HDR) afterloaders, intelligent treatment planning software, and innovative applicators, is dramatically improving the precision and efficacy of brachytherapy. These innovations lead to superior patient outcomes, which in turn accelerates the adoption and integration of these devices into standard oncology practices. Moreover, the worldwide demographic shift towards an aging population, which is inherently more susceptible to cancer development, combined with growing public and medical community awareness about the significant benefits of brachytherapy—including its minimally invasive nature, shorter overall treatment schedules, and excellent local control rates—further stimulates market expansion. Substantial investments in modernizing healthcare infrastructure, particularly in developing economies, and a general upward trend in global healthcare expenditure also contribute positively by expanding access to these advanced cancer treatments in previously underserved regions.

However, the market's growth trajectory is tempered by several discernible restraints. A prominent barrier is the inherently high cost associated with acquiring, installing, and maintaining state-of-the-art brachytherapy equipment, radioactive sources, and the specialized facility infrastructure required for safe and effective operation. This significant capital outlay can severely limit adoption, especially within healthcare systems in resource-constrained or emerging market settings. Another critical restraint is the acute scarcity of highly skilled radiation oncologists, experienced medical physicists, and proficient radiation therapists who possess specialized training and expertise in executing complex brachytherapy procedures. The highly technical nature of brachytherapy demands extensive knowledge and precision, and the shortage of such personnel can hinder the widespread implementation of these therapies. Furthermore, the industry operates under stringent and complex regulatory approval processes for both new medical devices and radioactive materials, which often lead to protracted delays in product launches and market entry, impeding innovation and market responsiveness. Lastly, the presence of well-established and continually evolving competitive alternatives, such as advanced external beam radiation therapy (EBRT) techniques (e.g., IMRT, SBRT, proton therapy), and various surgical interventions, coupled with potential patient concerns or anxieties regarding radiation exposure, continue to present formidable market restraints.

Amidst these challenges, considerable opportunities for sustained market growth abound. A significant opportunity lies in the global healthcare trend towards personalized medicine and highly targeted therapies, where brachytherapy, with its ability to deliver precise, localized radiation, offers distinct and compelling advantages. The development and commercialization of more cost-effective, compact, and potentially portable brachytherapy systems could substantially enhance market penetration, particularly within emerging economies and smaller community hospitals, making advanced treatment more accessible. Robust ongoing research and development into novel radioactive isotopes with improved dosimetric properties, alongside the creation of advanced biomaterials for seed encapsulation and implantation, promises to further elevate treatment efficacy and safety profiles. Crucially, the deeper integration of artificial intelligence (AI) and real-time advanced imaging modalities (such as functional MRI and PET-CT) into the brachytherapy workflow represents a transformative opportunity, potentially leading to unprecedented levels of precision and adaptive treatment capabilities. Expanding the clinical applications of brachytherapy to encompass a broader spectrum of cancer indications, improving patient access through dedicated professional training programs, and launching comprehensive public awareness campaigns about its benefits are also key strategic avenues for future market expansion. The overarching impact forces influencing this market include global economic conditions that directly affect healthcare spending and investment, the pace and direction of technological innovations, the evolving regulatory landscapes in different geographies, and dynamic changes in patient demographics and disease burden, all of which collectively shape the market's trajectory and potential for growth.

The Brachytherapy Devices Market is meticulously segmented across several critical dimensions, providing a granular and comprehensive understanding of its intricate dynamics and diverse offerings. This systematic segmentation includes categorization by product type, reflecting the different devices and components involved; by application, detailing the specific cancer types treated; by dose rate, differentiating between the intensity of radiation delivery; by end-user, identifying the primary healthcare facilities utilizing these technologies; and by technology, highlighting the advanced methodologies employed. This multi-faceted approach to segmentation is essential for dissecting market trends, identifying key growth areas, and understanding the specific needs and preferences of various stakeholders within the oncology landscape. Each segment contributes uniquely to the overall market ecosystem, revealing distinct demand patterns, competitive landscapes, and technological adoption rates across the global healthcare sector.

Analyzing these segments allows for strategic insights into where innovation is most concentrated and where patient needs are most pressing. For instance, the product type segment differentiates between the hardware (afterloaders, applicators) and the software (treatment planning systems) components, each with its own development cycles and market drivers. The application segment clearly shows the therapeutic areas with the highest demand for brachytherapy, such as prostate and gynecological cancers, while also indicating emerging applications. Dose rate segmentation, between HDR and LDR, reflects clinical preferences based on tumor characteristics and patient convenience. Understanding these segmentations is paramount for market players to develop targeted strategies, optimize product portfolios, and align with evolving clinical practices and patient care models. The ongoing evolution within these segments, driven by both clinical research and technological breakthroughs, underscores the dynamic nature of the brachytherapy devices market.

The value chain for the Brachytherapy Devices Market is a complex and highly specialized ecosystem that commences with rigorous upstream activities, which are fundamental to the existence and efficacy of these life-saving devices. This initial phase primarily involves extensive research and development (R&D) efforts focused on discovering and refining radioactive isotopes, designing innovative device components, and pioneering advanced treatment methodologies. Key participants at this crucial stage include highly specialized isotope manufacturers responsible for producing medical-grade radioactive materials such as Iridium-192, Iodine-125, and Palladium-103. Also vital are materials suppliers who provide high-quality biocompatible materials for applicators and seeds, and dedicated R&D firms intensely focused on pushing the boundaries of radiation delivery technologies. This upstream segment demands substantial and sustained investment in scientific expertise, cutting-edge laboratory infrastructure, and meticulous adherence to a myriad of stringent regulatory compliance standards to guarantee the utmost safety, purity, and efficacy of both the radioactive sources and the medical-grade materials used in device fabrication. The consistent availability, quality, and secure supply chain of these critical raw materials are absolutely paramount for the uninterrupted production of brachytherapy seeds and other essential sources.

Proceeding along the value chain, midstream activities encompass the sophisticated manufacturing, precision engineering, and meticulous assembly of the diverse range of brachytherapy devices. This phase involves highly specialized medical device companies that meticulously design and produce remote afterloaders, an array of versatile applicators, flexible catheters, and advanced treatment planning software. These manufacturers are at the forefront of integrating state-of-the-art robotics, sophisticated imaging technologies, and complex software algorithms to engineer systems that are not only exceptionally accurate but also user-friendly and clinically efficient. Throughout this manufacturing stage, adherence to the most rigorous quality control protocols and compliance with stringent international medical device standards (such as ISO 13485 and FDA regulations) are of paramount importance, ensuring the unwavering reliability, safety, and consistent performance of every product. The protection and enforcement of intellectual property rights, encompassing device design patents and technological innovations, also represent critical assets that are carefully managed and defended at this pivotal point in the value chain, safeguarding competitive advantage.

The final segment of the value chain involves downstream activities, which are centered on the efficient distribution, strategic sales, and comprehensive post-sales support for brachytherapy devices delivered to end-users. These end-users are predominantly highly specialized healthcare providers, including large hospitals, dedicated cancer centers, and specialty oncology clinics. Distribution channels can manifest in two primary forms: direct sales, where manufacturers engage directly with healthcare providers, offering tailored solutions and direct technical support; or indirect sales, involving a network of specialized distributors and third-party logistics providers who facilitate broader market reach, especially in geographically dispersed regions. Effective post-sales services are absolutely vital for maintaining long-term customer satisfaction and ensuring the optimal functioning of these complex, high-value devices. These services typically include professional installation, comprehensive clinical and technical training for medical staff, routine maintenance, and responsive technical support. The overall efficiency and effectiveness of these distribution and support channels directly and significantly influence market penetration rates, product adoption levels, and the overall clinical integration of brachytherapy solutions within the global healthcare system, underscoring their critical role in the market's success.

The primary potential customers for Brachytherapy Devices are an array of specialized healthcare institutions and dedicated medical facilities that are at the forefront of cancer treatment and research globally. This prominent segment predominantly includes large, multifaceted hospitals, especially those boasting comprehensive oncology departments and state-of-the-art radiation therapy units. These institutions typically possess the requisite robust infrastructure, including specialized operating theaters and shielded treatment rooms, along with a high volume of cancer patients, which collectively justify the substantial financial investment required for acquiring and integrating sophisticated brachytherapy equipment. These leading hospitals serve a diverse and extensive patient base afflicted with various forms of cancer, positioning them as absolutely central to the market's sustained demand. The complex decision-making process within these large hospital systems often involves a collaborative effort from multidisciplinary teams, which typically comprise highly experienced radiation oncologists, expert medical physicists, influential hospital administrators, and specialized procurement departments. Therefore, market penetration for device manufacturers necessitates a compelling demonstration of robust clinical evidence, clear cost-effectiveness, and seamless integration capabilities with existing hospital workflows and information systems.

Beyond major hospitals, independent cancer centers and specialty clinics, particularly those with a focused expertise in specific cancer types such as prostate cancer or breast cancer, represent another critically important and expanding customer segment. These specialized facilities often seek to adopt advanced, targeted therapeutic modalities like brachytherapy to provide highly specialized, cutting-edge care, thereby distinguishing themselves and attracting a specific patient demographic seeking specialized treatment options. Furthermore, leading academic medical centers and prestigious research institutes constitute a significant customer base. These entities not only provide direct patient care but are also actively engaged in groundbreaking clinical trials, pushing the boundaries of brachytherapy techniques, and playing a vital role in educating and training the next generation of oncology practitioners. For these research-intensive customers, the emphasis extends beyond mere clinical efficacy to encompass access to cutting-edge technology, robust research capabilities, and comprehensive educational support, making partnerships with device manufacturers crucial. Additionally, group purchasing organizations (GPOs) increasingly play a pivotal role in aggregating demand across a network of healthcare providers, leveraging their collective purchasing power to negotiate favorable pricing and contract terms for brachytherapy devices, influencing procurement decisions significantly.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $950 million |

| Market Forecast in 2032 | $1575 million |

| Growth Rate | CAGR 7.5% |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Elekta AB, Varian Medical Systems (Siemens Healthineers), Eckert & Ziegler BEBIG, iCAD Inc., Isoray Inc., Theragenics Corporation, CIVCO Medical Solutions, Alpha Omega Services Inc., Best Medical International Inc., Nucletron (Elekta), Bard Medical (BD), Accuray Incorporated, Genesis Medical, BEVCO Medical, Sun Nuclear Corporation, Brainlab AG, RaySearch Laboratories AB, MIM Software Inc., P-Cure Ltd., GE Healthcare. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Brachytherapy Devices market is defined by a dynamic and continually evolving technological landscape, with relentless innovation driving advancements in precision, safety, and ultimately, patient outcomes. At its core, high-dose-rate (HDR) brachytherapy systems, featuring sophisticated remote afterloaders, remain a cornerstone technology. These cutting-edge systems leverage advanced robotic mechanisms to precisely and safely deliver potent radioactive sources, most commonly Iridium-192, into specialized applicators that are strategically placed within or immediately adjacent to the tumor. This highly controlled delivery method allows for meticulously planned dose fractionation schedules and significantly shorter overall treatment times, thereby enhancing both clinical efficacy and patient convenience. A crucial technological advancement that has profoundly impacted the field is the seamless integration of advanced imaging modalities, including Computed Tomography (CT), Magnetic Resonance Imaging (MRI), and ultrasound, directly into the brachytherapy planning and delivery workflow. This integration facilitates image-guided brachytherapy (IGBT), which provides clinicians with real-time, high-resolution visualization of the tumor and surrounding healthy anatomical structures. This visual guidance is instrumental in achieving exceptionally accurate applicator and radioactive source placement, thereby ensuring optimal dose distribution, which significantly minimizes the risk of collateral damage to healthy tissues and substantially improves overall therapeutic efficacy.

Sophisticated treatment planning software represents another pivotal technological component, continuously evolving with the integration of advanced algorithms for dose optimization and immersive 3D visualization capabilities. These highly specialized software platforms empower medical physicists and radiation oncologists to meticulously contour target volumes and critical organs at risk, perform complex dose calculations with unparalleled accuracy, and simulate a myriad of treatment scenarios prior to the actual radiation delivery. This meticulous pre-treatment planning ensures the generation of highly conformal radiation treatment plans, maximizing tumor coverage while rigorously sparing healthy surrounding tissues, which is a hallmark of modern brachytherapy. Furthermore, the ongoing development of innovative applicators and flexible catheters, custom-engineered for specific anatomical sites such as the prostate, breast, cervix, or head and neck regions, has vastly expanded the versatility and clinical applicability of brachytherapy. These highly specialized devices are meticulously designed to optimize patient comfort during placement and ensure ultra-precise radioactive source positioning, enabling highly effective radiation delivery even in the most anatomically challenging areas, thereby addressing unmet clinical needs across diverse cancer types. The increasing integration of automation and robotics into device handling, radioactive source management, and delivery systems is also gaining significant traction, substantially enhancing operational safety for clinical staff by reducing direct handling of radioactive materials, while simultaneously boosting procedural efficiency and reproducibility.

The horizon of brachytherapy technology is further illuminated by the accelerating adoption of artificial intelligence (AI) and machine learning (ML) paradigms. AI algorithms are actively being developed to automate and refine traditionally manual and time-consuming tasks such as anatomical contouring, to intelligently optimize treatment plans based on a multitude of patient-specific factors, and to accurately predict patient responses and potential treatment toxicities. These AI-driven advancements promise to further streamline clinical workflows, significantly personalize therapeutic approaches, and elevate the overall standard of care. Real-time adaptive brachytherapy, a truly visionary concept where treatment plans can be dynamically modified and re-optimized during the actual procedure based on instantaneous anatomical changes detected by live imaging, represents a groundbreaking future direction that could revolutionize precision. Beyond these, miniaturization efforts in device design, the ongoing research into novel radioactive sources with enhanced dosimetric characteristics and reduced half-lives, and the strategic integration of telemedicine platforms for remote consultation and collaborative planning are also crucial areas of technological advancement. These innovations collectively aim to make brachytherapy more accessible, more efficient, and even more effective on a global scale, cementing its role as a vital tool in the ongoing fight against cancer.

Brachytherapy is an advanced form of internal radiation therapy where radioactive sources are meticulously placed directly inside or in close proximity to the cancerous tumor. This targeted delivery differentiates it from external beam radiation therapy, which delivers radiation from outside the body. Brachytherapy's primary advantage is its ability to deliver a very high dose of radiation precisely to the tumor, minimizing exposure and damage to surrounding healthy tissues and often requiring significantly fewer treatment sessions, thus offering enhanced clinical benefits and reduced side effects.

Brachytherapy devices are primarily and extensively utilized to treat a range of localized solid tumors. The most common applications include prostate cancer, various gynecological cancers such as cervical, endometrial, and vaginal cancers, breast cancer (often for partial breast irradiation), head and neck cancers, and certain types of skin cancer. Its unparalleled ability for highly targeted radiation delivery makes it an exceptionally effective therapeutic option for well-defined and localized malignant tumors, either as a standalone treatment or as a crucial component of multimodal cancer therapy regimens.

The sustained growth of the brachytherapy devices market is primarily fueled by several powerful factors. Foremost among these is the escalating global incidence of various cancer types, which inherently drives demand for effective oncology treatments. Continuous and rapid technological advancements in brachytherapy devices and planning software are significantly enhancing treatment precision, efficacy, and safety, leading to improved patient outcomes. Additionally, the increasing global geriatric population, which is more susceptible to cancer, along with growing awareness among both clinicians and patients about the substantial clinical benefits and convenience offered by targeted internal radiation therapies, further contribute to market expansion and adoption.

Artificial intelligence is profoundly impacting the brachytherapy device market and clinical practice by revolutionizing several key areas. AI algorithms are increasingly employed to optimize treatment planning processes, enabling highly accurate and personalized dose distributions while reducing manual effort. AI also enhances real-time image guidance during procedures, ensuring superior precision in radioactive source placement. Furthermore, AI contributes to automating various workflow tasks, predicting patient outcomes and potential toxicities, and facilitating the development of adaptive brachytherapy, which leads to more efficient, precise, and patient-centric cancer treatments.

Currently, North America and Europe are the leading geographical regions in the global brachytherapy devices market. Their leadership is attributed to advanced healthcare infrastructures, high cancer prevalence, and substantial investments in medical technology and research. However, the Asia Pacific (APAC) region is projected to demonstrate the most significant growth potential during the forecast period. This accelerated growth in APAC is driven by a large and aging population, rapidly increasing healthcare expenditure, and improving access to modern medical technologies and cancer care facilities across countries like China, India, and Japan.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.