ID : MRU_ 427330 | Date : Oct, 2025 | Pages : 242 | Region : Global | Publisher : MRU

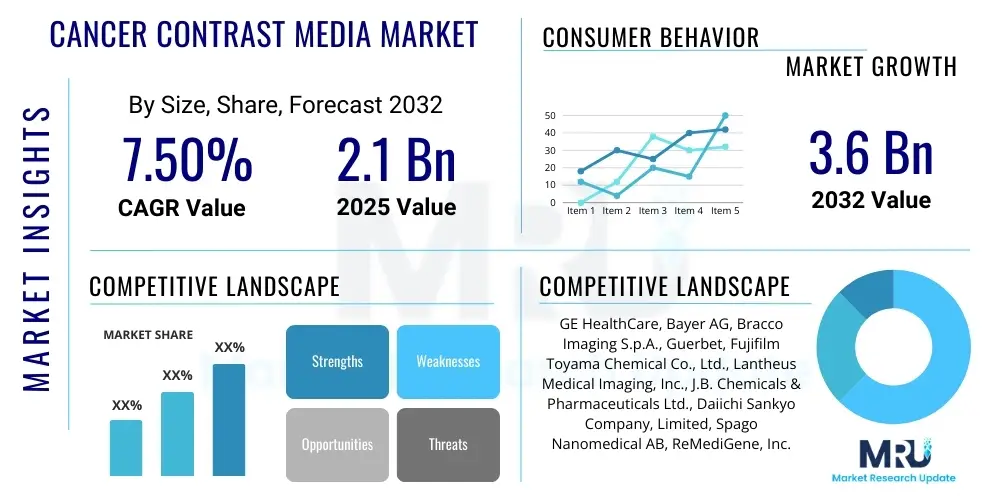

The Cancer Contrast Media Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2025 and 2032. The market is estimated at USD 2.1 billion in 2025 and is projected to reach USD 3.6 billion by the end of the forecast period in 2032.

The Cancer Contrast Media Market encompasses a specialized segment within medical diagnostics, focusing on agents designed to enhance the visibility of tissues, organs, and physiological processes during various imaging procedures for cancer detection, staging, and monitoring. These media are crucial for improving the diagnostic accuracy of techniques such as Magnetic Resonance Imaging (MRI), Computed Tomography (CT), and Ultrasound. By altering the signal intensity or acoustic properties of target areas, contrast media allow radiologists and oncologists to differentiate between healthy and cancerous tissues, identify tumor margins, and assess vascularity, which are critical steps in informed treatment planning.

Products within this market range from iodinated agents used primarily in CT scans and X-rays, to gadolinium-based compounds for MRI, and microbubble agents for ultrasound. Each class of contrast media works through distinct mechanisms to highlight abnormalities, making subtle changes more apparent to the human eye and advanced image analysis software. Their primary applications in oncology include the initial diagnosis of suspicious lesions, precise staging of tumors to determine the extent of disease, monitoring treatment response to chemotherapy or radiation, and guiding biopsies or other interventional procedures with greater precision.

The benefits derived from the use of cancer contrast media are profound, leading to earlier and more accurate cancer diagnoses, improved prognostic assessments, and more effective treatment strategies tailored to individual patient needs. The markets growth is predominantly driven by the escalating global incidence of various cancer types, the continuous advancements in imaging technology that necessitate optimized contrast enhancement, and the increasing demand for non-invasive yet highly accurate diagnostic methods. Furthermore, the rising awareness about early cancer detection and the expansion of healthcare infrastructure in emerging economies are significant factors propelling market expansion.

The Cancer Contrast Media Market is experiencing dynamic shifts, influenced by several overarching business, regional, and segmental trends. Globally, the industry is witnessing intensified research and development efforts aimed at creating novel contrast agents with improved safety profiles, enhanced specificity for tumor cells, and multi-modal capabilities. Pharmaceutical companies are increasingly investing in molecular imaging agents and targeted contrast media that can bind to specific cancer biomarkers, promising a new era of highly precise diagnostics. Strategic collaborations, mergers, and acquisitions are also prominent, as companies seek to consolidate market share, expand product portfolios, and leverage advanced technologies to gain a competitive edge.

From a regional perspective, North America continues to hold a dominant position in the cancer contrast media market, primarily due to its sophisticated healthcare infrastructure, high prevalence of cancer, significant healthcare expenditure, and the early adoption of advanced diagnostic technologies. Europe also represents a substantial market, driven by an aging population and a strong focus on cancer research and treatment. However, the Asia Pacific region is projected to exhibit the fastest growth over the forecast period. This accelerated expansion is attributed to rapidly improving healthcare facilities, increasing patient awareness, rising disposable incomes, and the growing incidence of cancer across populous nations like China and India, leading to greater demand for advanced diagnostic solutions.

Segment-wise, the market sees robust growth across various product types and imaging modalities. Gadolinium-based contrast agents for MRI and iodinated contrast media for CT scans remain the largest segments due to their established clinical utility and widespread adoption. However, the microbubble contrast agents for ultrasound are gaining traction, particularly in applications where radiation exposure is a concern or repeated imaging is required. The increasing focus on personalized medicine and theranostics is also driving demand for contrast agents that can not only diagnose but also deliver therapeutic agents, thereby blurring the lines between diagnostic and therapeutic applications and opening new avenues for market development.

User inquiries concerning the impact of Artificial Intelligence (AI) on the Cancer Contrast Media Market frequently revolve around themes of enhanced diagnostic efficiency, personalized medicine, and potential shifts in contrast agent usage. Common questions explore how AI can optimize image interpretation, predict patient response to contrast media, or even reduce the required dosage while maintaining diagnostic quality. There is a keen interest in AIs role in the discovery and development of new contrast agents, as well as its capacity to analyze vast datasets from imaging studies, leading to more precise and earlier cancer detection. Concerns also emerge regarding data privacy, the validation of AI algorithms in clinical settings, and the potential for AI to both augment and potentially alter the traditional role of contrast media.

The key themes emanating from user questions suggest a strong expectation that AI will be a transformative force, primarily by improving the diagnostic workflow and enhancing the value of contrast-enhanced imaging. Users anticipate that AI could lead to more personalized contrast media administration protocols, reducing the risk of side effects and improving cost-effectiveness. The ability of AI to detect subtle patterns in complex medical images, especially those enhanced by contrast agents, is seen as a major breakthrough for early and accurate cancer diagnosis. Moreover, AIs potential in drug discovery, particularly for identifying novel compounds or optimizing existing ones for targeted cancer imaging, is a significant area of interest.

Ultimately, the collective user sentiment indicates a future where AI and cancer contrast media are synergistic. AI is not perceived as replacing contrast media but rather as a powerful tool to maximize their efficacy, safety, and diagnostic yield. It is expected to enable more sophisticated image analysis, facilitate the development of next-generation contrast agents, and personalize diagnostic pathways, thereby profoundly influencing the markets trajectory and clinical practice. This integration promises to unlock new levels of precision in cancer care, from detection to treatment monitoring, by leveraging data-driven insights to complement the visual enhancement provided by contrast agents.

The Cancer Contrast Media Market is influenced by a complex interplay of Drivers, Restraints, and Opportunities, alongside broader Impact Forces that shape its growth trajectory. Key drivers include the persistently rising global incidence of various cancers, which directly translates into an increased demand for advanced diagnostic tools. An aging global population, a demographic segment particularly susceptible to cancer, further amplifies this demand. Continuous technological advancements in medical imaging modalities, such as ultra-high-field MRI and multi-detector CT, necessitate equally sophisticated contrast agents to fully leverage their diagnostic capabilities. Furthermore, the growing emphasis on early and accurate cancer diagnosis, which significantly improves treatment outcomes, acts as a powerful catalyst for market expansion.

However, several restraints temper this growth. Stringent regulatory approval processes for new contrast media, particularly concerning safety and efficacy, can lead to protracted and costly development cycles. The high cost associated with the research, development, and commercialization of novel contrast agents often limits market accessibility, especially in developing regions. Concerns regarding potential side effects of contrast agents, such as nephrogenic systemic fibrosis (NSF) linked to gadolinium-based agents or allergic reactions, necessitate careful patient screening and cautious administration, impacting their widespread use. Additionally, the emergence of alternative diagnostic methods that do not require contrast enhancement, or improvements in non-contrast imaging techniques, could pose a challenge to market growth.

Despite these challenges, significant opportunities abound within the market. Emerging economies, with their expanding healthcare infrastructure and increasing affordability of advanced medical care, represent untapped markets with immense growth potential. The development of novel contrast agents with improved safety profiles, enhanced targeting capabilities, and theranostic applications offers a promising avenue for innovation. The integration of artificial intelligence (AI) with contrast-enhanced imaging presents opportunities for personalized dosing, improved image analysis, and accelerated agent discovery. Furthermore, the shift towards personalized medicine and precision oncology creates a demand for highly specific contrast agents that can provide molecular-level information for tailored treatment strategies. The broader impact forces, such as the bargaining power of buyers (large hospital groups, purchasing organizations) and suppliers (raw material providers), the threat of new entrants (innovative startups), and the availability of substitutes, continually influence competitive dynamics and pricing strategies within this specialized medical market.

The Cancer Contrast Media Market is extensively segmented to provide a granular understanding of its diverse components, facilitating targeted analysis and strategic planning. This segmentation typically considers various parameters, including the distinct product types of contrast agents, the imaging modalities with which they are utilized, the specific applications within oncology, and the end-user facilities where these agents are primarily administered. Understanding these segments is crucial for identifying market hotspots, evaluating competitive landscapes, and forecasting future trends, as each segment is driven by unique technological advancements, clinical requirements, and patient demographics. The markets complexity necessitates a detailed breakdown to accurately reflect the varied demands and supply dynamics across the oncology diagnostic spectrum.

The value chain for the Cancer Contrast Media Market is a intricate network that begins with the sourcing and processing of raw materials, moving through manufacturing, distribution, and ultimately to the end-users. The upstream segment of the value chain is critical, involving the procurement and synthesis of highly specialized raw materials such as iodine and gadolinium, which are essential components for the primary classes of contrast agents. This stage also includes the development of complex chemical compounds and formulations, requiring advanced research and development capabilities, stringent quality control, and adherence to pharmaceutical manufacturing standards to ensure the purity and efficacy of the active ingredients.

As the product moves downstream, the focus shifts to manufacturing, packaging, and distribution. Manufacturers transform raw chemicals into finished contrast media products, which are then packaged in sterile vials or syringes for clinical use. The distribution channel is multifaceted, comprising both direct and indirect routes. Direct distribution typically involves manufacturers selling directly to large hospitals, integrated healthcare systems, or national health services, leveraging their own sales forces and logistics networks to ensure timely delivery and often providing technical support and training. This direct approach can foster stronger relationships and offer greater control over product placement and pricing.

Indirect distribution channels involve the use of third-party distributors, wholesalers, and pharmaceutical supply chain aggregators who manage warehousing, inventory, and delivery to a broader range of healthcare facilities, including smaller hospitals, diagnostic centers, and specialized clinics. These intermediaries play a crucial role in market penetration and reaching a wider customer base, especially in geographically dispersed areas. The effectiveness of the distribution network directly impacts product availability, accessibility, and ultimately, market share. Both direct and indirect channels must navigate complex regulatory requirements, cold chain logistics, and inventory management to ensure product integrity and patient safety throughout the entire supply chain, from manufacturing plant to point of care.

The primary potential customers and end-users of cancer contrast media are diverse, encompassing a wide array of healthcare institutions and medical professionals who rely on these agents for accurate and timely cancer diagnosis and management. Hospitals, particularly their oncology, radiology, and interventional radiology departments, represent the largest segment of end-users. Within these settings, contrast media are routinely used across various imaging modalities to detect tumors, determine their stage, monitor treatment effectiveness, and guide surgical or biopsy procedures. The comprehensive nature of hospital services, coupled with a high volume of cancer patients, makes them central to the consumption of these specialized diagnostic tools.

Specialized diagnostic imaging centers also constitute a significant customer base. These facilities, often equipped with state-of-the-art MRI, CT, and ultrasound machines, focus exclusively on performing a wide range of diagnostic scans, including a substantial number of contrast-enhanced oncology studies. Their business model relies on efficient patient throughput and high-quality imaging, making reliable access to a variety of contrast media essential for their operations. These centers frequently cater to outpatient referrals, providing crucial diagnostic services that complement those offered by larger hospital systems.

Furthermore, cancer research institutes and academic medical centers are vital customers, not only for their clinical diagnostic needs but also for their involvement in clinical trials, research into novel contrast agents, and the development of new imaging protocols. These institutions often require access to cutting-edge and experimental contrast media, driving innovation within the market. Ambulatory surgical centers, particularly those involved in minimally invasive oncology procedures or biopsies, also utilize contrast media for precise guidance. In essence, any healthcare entity involved in the diagnosis, staging, monitoring, or treatment planning of cancer, where enhanced visualization of internal structures is critical, represents a potential customer for cancer contrast media, highlighting the broad and fundamental role these agents play in modern oncology.

The technology landscape of the Cancer Contrast Media Market is characterized by continuous innovation aimed at improving diagnostic accuracy, patient safety, and clinical utility. A significant area of focus is the development of advanced molecular imaging agents that can specifically target cancer cells or their microenvironment. These agents often incorporate ligands or antibodies that bind to specific biomarkers overexpressed in tumors, allowing for highly sensitive and specific detection of cancerous lesions at earlier stages and providing insights into their biological characteristics. This move towards personalized contrast media is revolutionizing the field, offering a pathway to tailor diagnostic approaches to individual patient tumor profiles.

Another critical technological trend involves the creation of multimodal imaging agents. These agents are designed to be detectable by more than one imaging modality, such as combining properties for both MRI and optical imaging or CT and PET. Such versatility allows for complementary information from different imaging techniques, providing a more comprehensive view of the tumor and facilitating more accurate diagnosis and staging. The development of ultra-low dose contrast media is also a priority, addressing concerns about potential toxicity and aiming to reduce the overall chemical burden on patients while maintaining or even enhancing diagnostic image quality. This is particularly relevant for patients with compromised renal function or those requiring repeated imaging.

The integration of artificial intelligence (AI) and machine learning (ML) platforms represents a pivotal technological advancement within the market. AI is being deployed not only for enhanced image processing and interpretation but also for optimizing contrast media injection protocols, predicting patient responses, and accelerating the discovery of new contrast agents. AI algorithms can analyze vast datasets from contrast-enhanced scans to detect subtle patterns indicative of malignancy, quantify tumor characteristics more precisely, and potentially even reduce the need for certain types of contrast agents by improving the diagnostic yield from lower doses. Furthermore, advancements in nanotechnology are paving the way for nano-sized contrast agents that can extravasate more effectively into tumor tissues, offering superior contrast enhancement and targeted delivery, thereby pushing the boundaries of what is diagnostically possible in oncology.

Cancer contrast media are specialized diagnostic agents, such as iodinated, gadolinium-based, or microbubble substances, used to enhance the visibility of tumors and related structures in medical images. They work by altering the signal intensity of tissues during imaging procedures like MRI, CT, or ultrasound, making cancerous lesions more distinct from healthy tissue, thereby improving diagnostic accuracy and aiding in precise localization and characterization.

The primary applications of contrast media in oncology include the initial diagnosis of suspicious masses, accurate staging of cancer to determine its extent and spread, monitoring the effectiveness of cancer treatments (such as chemotherapy or radiation), and guiding interventional procedures like biopsies. These agents are critical for providing detailed anatomical and functional information necessary for informed clinical decisions.

Yes, like all pharmaceutical agents, cancer contrast media can have potential side effects. These can range from mild reactions like nausea, warmth, or localized pain at the injection site, to more severe allergic reactions. Gadolinium-based contrast agents have been linked to Nephrogenic Systemic Fibrosis (NSF) in patients with severe kidney dysfunction and also have concerns regarding gadolinium retention in the brain and other tissues. Careful patient screening and adherence to administration guidelines are crucial to mitigate risks.

Artificial intelligence is profoundly impacting the use of contrast media by enhancing image interpretation, optimizing dosing protocols, and accelerating the development of new agents. AI algorithms can detect subtle abnormalities in contrast-enhanced images more efficiently, personalize contrast administration based on patient-specific data, and aid in the discovery of novel targeted contrast media, ultimately improving diagnostic precision and patient safety in oncology.

Latest innovations include the development of molecularly targeted contrast agents that bind specifically to cancer biomarkers, multimodal agents detectable by multiple imaging techniques, and ultra-low dose formulations to enhance patient safety. Additionally, the integration of AI for advanced image analysis, personalized dosing, and accelerated research and development is a significant driver, alongside the emergence of theranostic agents that combine diagnostic and therapeutic functions.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.