ID : MRU_ 428087 | Date : Oct, 2025 | Pages : 246 | Region : Global | Publisher : MRU

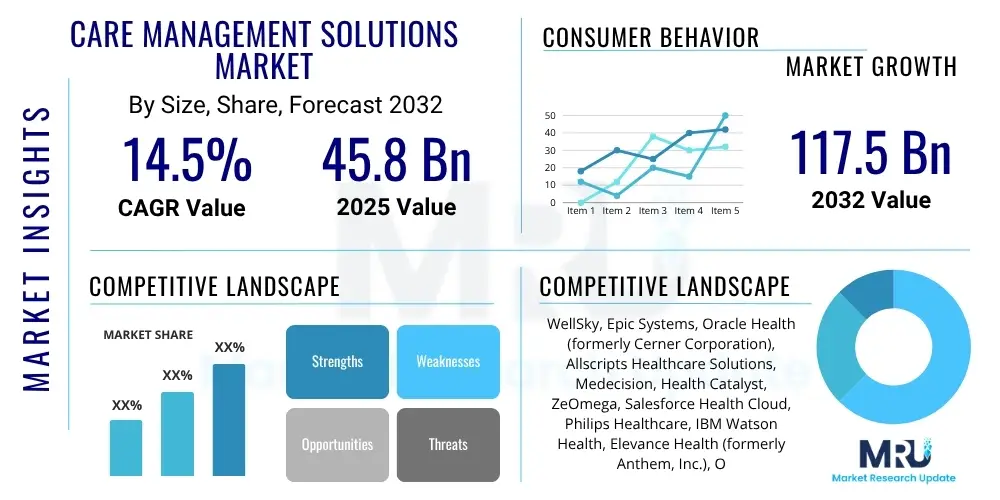

The Care Management Solutions Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 14.5% between 2025 and 2032. The market is estimated at USD 45.8 billion in 2025 and is projected to reach USD 117.5 billion by the end of the forecast period in 2032.

The Care Management Solutions market is currently experiencing a profound transformation, propelled by the urgent need to address the global rise in chronic disease prevalence, the demographic shift towards an aging population, and the relentless pressure to curb escalating healthcare expenditures. These sophisticated solutions encompass a wide array of integrated software and professional services specifically engineered to streamline and coordinate patient care across the entire healthcare continuum, spanning from primary care to specialized treatments and long-term support. Their fundamental purpose is to improve patient health outcomes by ensuring continuity of care, enhancing preventative measures, and optimizing resource allocation within increasingly complex healthcare ecosystems. This market segment is instrumental in facilitating the transition from traditional volume-based payment models to more sustainable value-based care paradigms, which prioritize quality of care, patient satisfaction, and cost-effectiveness over the sheer quantity of services provided.

Product offerings within this market are typically robust, modular platforms that integrate critical functionalities such as comprehensive patient risk assessment, individualized care plan development, precise medication management, automated appointment scheduling, and secure, real-time communication channels for multidisciplinary care teams. These platforms serve a diverse range of major applications, including meticulous disease management for prevalent chronic conditions like diabetes, hypertension, and congestive heart failure; nuanced case management for patients with complex, co-morbid conditions; judicious utilization management to ensure the appropriate and efficient use of healthcare resources; and broad population health management initiatives designed to improve the health trajectories of entire communities. The multifaceted benefits derived from these solutions are significant, encompassing superior care coordination, heightened patient engagement through personalized interactions, a substantial reduction in administrative overhead for healthcare providers, and significant long-term cost savings for both healthcare payers and providers by preventing avoidable complications and readmissions.

The market's dynamic growth is further energized by several key driving factors. The increasing burden of chronic illnesses globally necessitates continuous, proactive oversight, which these solutions are uniquely positioned to provide. Moreover, the burgeoning emphasis on patient-centric care models demands tools that can empower individuals in their health journey and foster greater collaboration between patients and their care teams. Crucially, rapid technological advancements, particularly in areas like artificial intelligence, machine learning, and cloud computing, have rendered these solutions more sophisticated, scalable, and accessible, making them indispensable components of modern healthcare infrastructure. The accelerated adoption of remote patient monitoring (RPM) and telehealth services, intensified by recent global health crises, has also played a pivotal role, allowing for continuous data collection and virtual care delivery, thus expanding the reach and efficacy of care management far beyond traditional clinical settings.

The Care Management Solutions Market is characterized by vigorous expansion, fueled by the imperative for healthcare systems worldwide to simultaneously optimize patient health outcomes and mitigate the relentless increase in operational costs. Current business trends unmistakably point towards the increasing adoption of highly integrated platforms that consolidate an array of care management functionalities, such as population health analytics, chronic disease management, and utilization review, into a unified, interoperable system. This strategic integration not only streamlines workflows but also provides a holistic view of patient data, enabling more informed clinical decisions. Furthermore, the market is witnessing a notable acceleration in mergers, acquisitions, and strategic partnerships, as established technology giants and innovative healthcare organizations seek to fortify their capabilities, broaden their market footprint, and stimulate technological advancements through synergistic collaborations. The shift towards flexible, scalable Software-as-a-Service (SaaS) and subscription-based deployment models is gaining considerable momentum, as these approaches offer reduced upfront capital expenditures and enhanced operational agility, thereby lowering the entry barriers for smaller healthcare providers and facilities.

Regionally, North America maintains its position as the preeminent market, underpinned by its highly advanced healthcare infrastructure, substantial governmental backing for digital health initiatives, and a widespread understanding and commitment to value-based care frameworks. This region benefits from early adoption of cutting-edge technologies and a proactive regulatory environment that encourages innovation in healthcare IT. In parallel, Europe is experiencing robust growth, driven by similar catalysts including stringent regulatory pushes for integrated care delivery and a growing investment in digital health solutions across key economies. However, varying levels of digital maturity and slower adoption rates in certain European countries present nuanced challenges. The Asia Pacific (APAC) region is rapidly emerging as the fastest-growing market, propelled by skyrocketing healthcare expenditures, an expanding middle class with increasing access to healthcare, and proactive government investments in modernizing healthcare IT infrastructure, particularly evident in populous nations like China, India, and Japan. These countries are leveraging technology to address significant healthcare access and quality disparities.

Segmentation trends unequivocally emphasize the burgeoning preference for cloud-based deployment models over traditional on-premise solutions. This preference is largely attributed to the inherent advantages of cloud computing, including superior scalability, enhanced accessibility, reduced maintenance overhead, and greater cost-efficiency, which align perfectly with the dynamic needs of contemporary healthcare organizations. Among end-users, large healthcare providers, encompassing hospitals, extensive health systems, and consolidated physician groups, continue to be primary adopters, leveraging these solutions for complex patient populations and intricate operational demands. Simultaneously, healthcare payers, including health insurance companies and large employer groups, are making substantial investments in care management platforms to proactively manage chronic conditions among their beneficiaries, thereby driving greater cost efficiencies and improving member health. In terms of application, population health management and remote patient monitoring represent the most significant growth segments, reflecting the industry's strategic pivot towards preventative medicine, continuous patient engagement, and community-wide health improvement initiatives, increasingly integrating artificial intelligence and machine learning for predictive insights and personalized care pathways.

Common user questions concerning the impact of Artificial Intelligence (AI) on the Care Management Solutions Market consistently revolve around AI's transformative potential to revolutionize patient outcomes, dramatically enhance operational efficiencies, and effectively address the intricate demands of personalized care delivery. Users frequently inquire about the precise mechanisms through which AI can accurately predict patient deterioration, automate myriad routine administrative tasks, and facilitate the development of more precise, data-driven treatment plans. Recurring concerns invariably include the paramount issues of patient data privacy and security, the ethical implications inherent in algorithmic decision-making, and the potential for technological unemployment or significant role shifts among human care managers. Despite these concerns, expectations remain exceptionally high regarding AI's unparalleled ability to extract and synthesize profound insights from vast, complex healthcare datasets, thereby enabling a paradigm shift from reactive to profoundly proactive care. This capability is expected to empower healthcare systems to deliver significantly more value-based care with optimized resource utilization, setting new benchmarks for efficiency and effectiveness in the entire care continuum.

The Care Management Solutions market's trajectory is profoundly influenced by a dynamic interplay of potent drivers, significant restraints, emerging opportunities, and pervasive impact forces. A foremost driver is the inexorable global surge in the prevalence of chronic diseases, such as diabetes, cardiovascular conditions, chronic obstructive pulmonary disease (COPD), and various autoimmune disorders, which necessitates continuous, meticulously coordinated care interventions to prevent acute exacerbations, manage symptoms effectively, and ultimately improve patients' long-term quality of life. Concurrently, the accelerating demographic shift towards an aging global population significantly intensifies the demand for sophisticated long-term care management solutions, preventative health programs, and support systems designed to help seniors maintain independence and manage multiple co-morbidities. Furthermore, the persistent and often escalating healthcare expenditures across both developed and rapidly developing nations serve as a powerful catalyst, compelling healthcare systems to embrace solutions that can genuinely deliver value-based care, substantially reduce costly hospital readmissions, and optimally allocate increasingly scarce resources to achieve better health outcomes at lower costs. The escalating adoption of digital health technologies, coupled with pervasive government mandates and initiatives promoting integrated care delivery and interoperability standards, further provides a substantial impetus for market expansion.

However, several inherent restraints present considerable challenges to the otherwise robust growth of this market. Paramount among these are the complex issues surrounding patient data privacy and stringent security requirements, given the highly sensitive nature of protected health information (PHI). Compliance with evolving global and regional regulations, such as HIPAA in the United States and GDPR in Europe, imposes significant technical and operational burdens on solution providers and healthcare organizations alike. Persistent interoperability challenges remain a formidable hurdle, as integrating disparate legacy IT systems and electronic health records (EHRs) across a fragmented ecosystem of healthcare providers, payers, and ancillary services can be exceedingly complex, time-consuming, and cost-prohibitive. The substantial initial capital investment required for implementing comprehensive, enterprise-level care management platforms, along with the associated expenses for specialized staff training, infrastructure upgrades, and system customization, can often deter smaller healthcare organizations or those with limited budgets. Moreover, deeply ingrained resistance to change from healthcare professionals who are accustomed to traditional workflows and paper-based processes poses a critical human factor challenge, necessitating robust change management strategies, extensive stakeholder engagement, and strong leadership commitment to ensure successful adoption and long-term utilization.

Despite these formidable challenges, the Care Management Solutions market is replete with substantial and transformative opportunities for innovative market players. The rapid expansion and widespread adoption of remote patient monitoring (RPM) and telehealth services, particularly catalyzed by the global public health exigencies of recent years, present a vast and burgeoning growth avenue. These technologies facilitate continuous monitoring of patient vitals and health metrics outside traditional clinical settings, enabling early intervention and reducing the need for frequent in-person visits. The increasing integration of advanced Artificial Intelligence (AI) and Machine Learning (ML) algorithms offers unprecedented capabilities for sophisticated predictive analytics, highly personalized care plans, and the automation of myriad routine administrative tasks, fundamentally transforming the efficiency, accuracy, and overall effectiveness of care delivery. Furthermore, a significant opportunity lies in addressing the social determinants of health (SDOH) through integrated care management platforms that can identify and mitigate non-clinical factors influencing patient outcomes, thus enabling a more holistic approach to population health. The pronounced shift towards preventive care models and proactive health management provides fertile ground for the development and deployment of solutions that can identify health risks early, intervene effectively, and create sustainable long-term value for patients, providers, and payers. Pervasive impact forces, including rapidly evolving regulatory landscapes, the relentless pace of technological disruption, heightened patient expectations for personalized digital health experiences, and unrelenting economic pressures to achieve superior outcomes with constrained resources, continually shape the strategic direction, investment priorities, and innovation agendas within this dynamic market.

The Care Management Solutions market is intricately segmented to provide a detailed understanding of its diverse components, deployment methods, end-user applications, and the specific problems they address. This segmentation helps stakeholders, including solution providers, healthcare organizations, and investors, to identify key growth areas and tailor strategies effectively. The market can be broadly categorized by component into software solutions and services, reflecting the dual need for robust technological platforms and expert support for implementation and ongoing optimization. This distinction is crucial as it highlights that while advanced software forms the backbone, the complex nature of healthcare operations necessitates comprehensive service support for successful integration and utilization.

Deployment models differentiate between cloud-based and on-premise solutions, catering to varying organizational sizes, IT infrastructures, and security preferences. Cloud-based solutions offer scalability and reduced infrastructure costs, appealing to organizations seeking agility and remote access, while on-premise solutions provide maximum control over data and security, often favored by larger institutions with established IT departments and stringent regulatory requirements. End-user segmentation then highlights the primary beneficiaries, namely payers and providers, each with distinct requirements and value propositions from these solutions. Payers focus on population health management and cost containment, whereas providers prioritize clinical efficiency, patient engagement, and improved outcomes. Understanding these nuances is key to developing targeted solutions and market penetration strategies.

Finally, application-based segmentation delves into the specific clinical and operational problems that care management solutions are designed to solve. This includes highly specialized areas such as disease management for chronic conditions, complex case management, utilization management to ensure appropriate resource allocation, and broad population health management initiatives. Furthermore, specialized applications like electronic health records (EHR) integration and remote patient monitoring are critical sub-segments addressing distinct but interconnected needs within the care continuum. Each application area addresses unique challenges within the healthcare landscape, underscoring the versatility and critical importance of these solutions in modern healthcare delivery.

The value chain within the Care Management Solutions market initiates with upstream activities predominantly focused on fundamental technology development, rigorous research and development, and sophisticated data acquisition and processing capabilities. This critical stage involves a diverse array of highly specialized professionals, including expert software architects, advanced data scientists, and pioneering AI/ML engineers, who are responsible for conceptualizing, designing, and building the foundational technological platforms, proprietary algorithms, and essential integration functionalities that underpin modern care management systems. Key activities at this juncture encompass extensive research into and development of advanced predictive analytics models, the establishment of highly secure and scalable cloud infrastructure, and the construction of robust, efficient data ingestion pipelines capable of seamlessly integrating information from myriad sources such as electronic health records (EHRs), wearable health devices, claims data, and patient-reported outcomes. Strategic collaborations with leading academic institutions, medical research centers, and clinical experts are paramount at this stage to ensure the clinical relevance, efficacy, and ethical grounding of the developed solutions. The upstream segment also critically involves hardware providers who supply the specialized devices essential for remote patient monitoring, including a range of sensors, wearable trackers, and advanced telemedicine equipment, all of which contribute vital real-time data back into the central care management platforms. Adherence to and development of industry-wide interoperability standards, such as FHIR, at this early stage is absolutely crucial for facilitating seamless and secure data exchange throughout the complex healthcare ecosystem.

Subsequent downstream activities concentrate intensely on the meticulous delivery, precise implementation, and continuous, robust support of these advanced care management solutions to a diverse array of end-users. This phase necessitates the provision of extensive, specialized consulting services designed to meticulously customize platforms to align with the unique operational workflows, patient populations, and strategic objectives of individual healthcare organizations. It also involves intricate system integration with existing, often disparate, IT infrastructures, and the delivery of comprehensive, hands-on training programs for clinical staff, administrative personnel, and IT support teams to ensure optimal adoption and utilization. Post-implementation support, encompassing responsive technical assistance, regular software updates, performance monitoring, and ongoing optimization, is absolutely critical for realizing sustained value and maximizing the return on investment. Strategic marketing and targeted sales efforts play a pivotal role in effectively educating potential customers, including both healthcare payers and providers, about the tangible benefits, advanced functionalities, and proven efficacy of these complex solutions. The ultimate success of downstream operations is intrinsically linked to cultivating strong, enduring client relationships, possessing a profound understanding of diverse clinical workflows, and the demonstrable ability to illustrate tangible improvements in patient outcomes, such as reduced readmissions, enhanced patient engagement, or optimized resource utilization. This phase also frequently includes sophisticated data analysis and bespoke reporting services, which provide invaluable feedback and actionable insights back to healthcare organizations for continuous quality improvement initiatives.

Distribution channels for Care Management Solutions are inherently multifaceted, typically employing a blended approach that incorporates both direct sales and indirect partnership strategies. Direct sales models involve solution vendors engaging directly with large-scale hospitals, extensive health systems, and major insurance companies through dedicated, specialized sales teams and experienced account managers. This direct engagement model allows for highly tailored solution customization, in-depth needs assessment, and direct negotiation of complex contracts. Conversely, indirect channels often leverage strategic partnerships with influential system integrators, expert value-added resellers (VARs), and specialized technology consultants who possess the capability to bundle care management solutions with other complementary IT offerings or provide bespoke implementation and integration expertise. For cloud-based solutions, which are increasingly prevalent and delivered via flexible Software-as-a-Service (SaaS) models, the internet serves as the primary distribution channel, enabling broader market reach, simpler deployment procedures, and eliminating the need for extensive on-premise hardware investments. The strategic selection and optimization of distribution channels are often contingent upon factors such such as the target customer's organizational size, their level of technical sophistication, existing IT vendor relationships, and geographic dispersion. Effective and diversified distribution is paramount for achieving deep market penetration, ensuring that these advanced and critically important solutions effectively reach the wide and varied spectrum of healthcare entities poised to benefit significantly from enhanced care coordination, streamlined patient management, and improved overall health outcomes.

The extensive roster of potential customers for Care Management Solutions spans the entirety of the intricate healthcare ecosystem, encompassing everything from expansive integrated delivery networks and large-scale hospital systems to individual physician practices and, crucially, a broad spectrum of health insurance payers. The overarching, unifying objective for all these diverse end-users is the fundamental improvement of patient health outcomes, the significant enhancement of operational efficiencies, and the imperative to manage escalating healthcare costs effectively within an increasingly complex, regulated, and financially constrained operational environment. Hospitals and large health systems represent a particularly significant customer segment, driven by their critical need to demonstrably reduce costly hospital readmission rates, substantially improve the efficacy of their chronic disease management programs, and optimize the allocation of increasingly strained resources across their extensive networks. These institutions are increasingly compelled by value-based care initiatives that directly link reimbursement to measurable patient outcomes, rendering sophisticated, integrated care management platforms indispensable tools for achieving critical quality metrics, realizing performance-based financial incentives, and demonstrating superior patient care. They typically require highly robust, scalable solutions capable of seamlessly integrating with their often-complex existing electronic health records (EHRs) and effectively supporting vast and diverse patient populations across multiple specialties and care settings.

Independent physician groups and smaller clinics constitute another vital and growing customer segment, increasingly adopting these advanced solutions to significantly streamline patient follow-up protocols, facilitate seamless coordination of care with external specialists, and efficiently manage preventive care schedules for their patient panels. For these smaller practices, factors such as intuitive ease of use, inherent scalability, and the availability of flexible cloud-based deployment options are often paramount considerations, enabling them to leverage sophisticated care management capabilities without requiring substantial upfront IT infrastructure investments or extensive internal technical expertise. Furthermore, long-term care facilities, including nursing homes and skilled nursing facilities, along with a rapidly expanding network of home healthcare agencies, represent substantial potential customers. These entities require specialized solutions to adeptly manage the intricate care needs of their often-frail and chronically ill patient populations, ensure rigorous medication adherence, and facilitate continuous remote monitoring for elderly individuals or those recovering at home. Given the frequent transitions of care that characterize these settings, robust communication capabilities, comprehensive data sharing features, and alert systems provided by advanced care management solutions are absolutely critical for preventing adverse events, ensuring continuity of care, and improving overall patient safety and well-being.

Beyond direct patient care providers, health insurance companies and large self-insured employer groups collectively form a substantial and strategically important segment of potential customers, often referred to broadly as "payers." These payers proactively utilize care management solutions to significantly improve the health status and outcomes of their vast member populations, to effectively manage and mitigate the high costs associated with complex chronic conditions, and to ultimately reduce overall healthcare expenditures through targeted, proactive interventions. By precisely identifying at-risk members through sophisticated analytics and deploying highly individualized care coordination programs, payers can dramatically lower claims costs associated with avoidable emergency room visits, preventable hospitalizations, and unnecessary procedures. Similarly, large employer groups, particularly those operating under self-insured health plans, are making strategic investments in these solutions to actively promote employee wellness, effectively manage chronic illnesses within their workforce, and consequently achieve substantial reductions in their health benefit costs. Both payers and employer groups actively seek platforms that offer comprehensive data analytics capabilities, advanced risk stratification tools, and personalized member engagement features designed to empower beneficiaries to make better health decisions, thereby aligning their financial incentives with measurably improved population health outcomes and enhanced overall well-being.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 45.8 Billion |

| Market Forecast in 2032 | USD 117.5 Billion |

| Growth Rate | 14.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | WellSky, Epic Systems, Oracle Health (formerly Cerner Corporation), Allscripts Healthcare Solutions, Medecision, Health Catalyst, ZeOmega, Salesforce Health Cloud, Philips Healthcare, IBM Watson Health, Elevance Health (formerly Anthem, Inc.), Optum, Evolent Health, Change Healthcare, Cognizant, Lumeris, CareCentrix, Conifer Health Solutions, GuidingCare, Casenet, Healthways (Tivity Health) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Care Management Solutions market is fundamentally powered and propelled by a rapidly evolving and highly dynamic technological landscape, with several key innovations serving as foundational pillars for its continuous growth and increasing sophistication. Cloud computing, specifically, stands as a critical enabling technology, offering the inherent advantages of scalable, universally accessible, and highly cost-effective deployment of advanced care management platforms. Cloud-based solutions facilitate seamless, secure data sharing across geographically distributed healthcare networks, robustly support real-time remote patient monitoring initiatives, and inherently ensure high availability, strong data redundancy, and effective disaster recovery capabilities, making them absolutely crucial for the resilient operations of modern healthcare organizations. This flexible infrastructure empowers healthcare providers and payers to securely access powerful analytical tools, comprehensive patient data, and critical clinical insights from virtually any location, significantly enhancing operational flexibility, responsiveness, and collaborative care delivery. Moreover, the inherent agility and elasticity of cloud environments enable rapid innovation cycles and seamless software updates, ensuring that care management platforms consistently remain at the cutting edge of technological advancements and continually adhere to evolving regulatory compliance mandates, thereby securing their long-term relevance and effectiveness.

Artificial Intelligence (AI) and Machine Learning (ML) algorithms are rapidly becoming indispensable components within care management solutions, providing extraordinarily advanced capabilities for sophisticated predictive analytics, precise patient risk stratification, and the development of highly personalized intervention strategies. AI algorithms possess the unique ability to process and synthesize vast, complex quantities of patient data, drawn from diverse sources such as electronic health records (EHRs), insurance claims, patient-generated health data, and wearable device metrics, to accurately identify individuals at elevated risk of clinical deterioration, medication non-adherence, or costly hospital readmissions, thereby enabling proactive and preventative care. Natural Language Processing (NLP), a powerful subset of AI, plays a crucial role by intelligently extracting actionable clinical insights and contextual information from unstructured data sources, including physician's notes, discharge summaries, and patient communication logs, significantly enriching the holistic understanding of a patient's health journey and social determinants of health. These AI-driven insights empower care managers to develop uniquely individualized care plans, automate numerous routine administrative tasks, and provide invaluable, evidence-based support for complex clinical decision-making, ultimately leading to more efficient, effective, and patient-centric health outcomes. The continuous learning capabilities inherent in advanced ML models ensure that these intelligent systems adapt and improve over time, continually enhancing their predictive accuracy, relevance, and overall utility in a dynamic healthcare environment.

Beyond cloud and AI/ML, several other significant technologies collectively contribute to the robustness and comprehensiveness of the Care Management Solutions market. Big Data Analytics, for instance, provides the essential infrastructure and methodologies for the aggregation, processing, and insightful analysis of massive, diverse datasets. This capability allows healthcare organizations to uncover critical population health trends, identify health disparities within communities, and inform evidence-based public health interventions at scale. The Internet of Medical Things (IoMT) and its associated remote patient monitoring (RPM) devices are fundamentally transforming how chronic conditions are managed, by providing continuous, real-time data streams on vital signs, physical activity levels, blood glucose readings, and medication adherence directly to care teams. Telehealth platforms are equally critical, facilitating seamless virtual consultations, remote diagnostics, and patient education sessions, thereby significantly extending the geographical reach of care services and improving patient access, particularly for underserved populations and those in rural areas. Mobile health (mHealth) applications further enhance active patient engagement by offering intuitive tools for self-management of conditions, personal health tracking, and secure, convenient communication with care providers. Emerging blockchain technology is also gaining traction as a promising solution for significantly enhanced data security, immutable record-keeping, and improved interoperability, by creating tamper-proof transaction logs and facilitating secure, transparent data exchanges across the inherently complex and often fragmented healthcare ecosystem, thereby fostering greater trust and accountability in patient information management.

Care Management Solutions are comprehensive software and service platforms designed to coordinate patient care, improve health outcomes, and enhance operational efficiency within healthcare systems. They facilitate the management of chronic diseases, complex cases, and population health through integrated tools for assessment, care planning, communication, and monitoring.

AI significantly impacts Care Management Solutions by enabling predictive analytics for patient risk stratification, personalizing care plans, automating administrative tasks, and enhancing clinical decision support. It improves efficiency, accuracy, and the ability to intervene proactively, leading to better patient outcomes and cost savings.

The primary end-users are healthcare providers (hospitals, physician groups, long-term care facilities, home healthcare agencies) and payers (health insurance companies, employer groups). Both seek to improve patient health, manage costs, and enhance care coordination.

Key drivers include the rising prevalence of chronic diseases, an aging global population, the increasing need to control healthcare costs, the shift towards value-based care models, and continuous technological advancements in digital health and AI.

The Care Management Solutions Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 14.5% between 2025 and 2032, reaching an estimated USD 117.5 billion by 2032 from USD 45.8 billion in 2025.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.