ID : MRU_ 431110 | Date : Nov, 2025 | Pages : 246 | Region : Global | Publisher : MRU

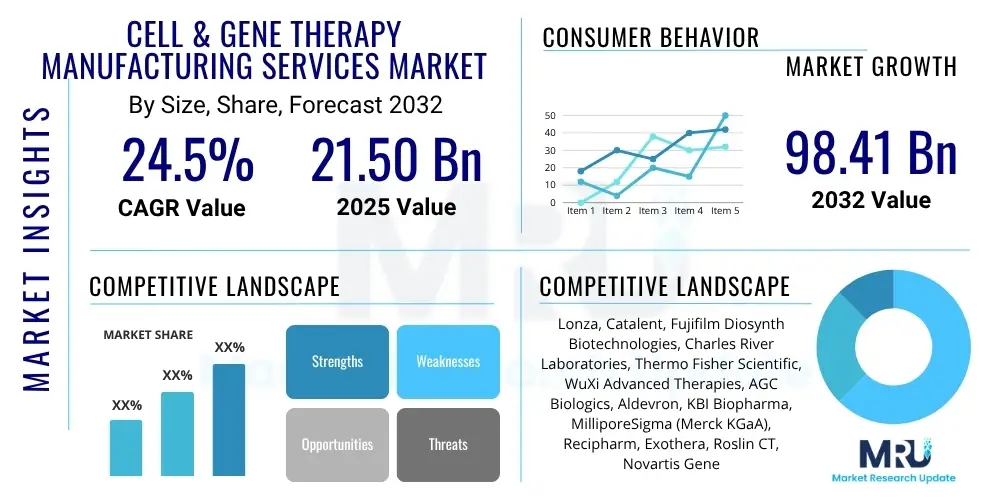

The Cell & Gene Therapy Manufacturing Services Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 24.5% between 2025 and 2032. The market is estimated at USD 21.50 Billion in 2025 and is projected to reach USD 98.41 Billion by the end of the forecast period in 2032.

The Cell & Gene Therapy (CGT) Manufacturing Services Market encompasses a comprehensive range of specialized outsourced activities essential for the development, production, and commercialization of advanced therapeutic medicinal products (ATMPs). This highly specialized sector provides critical support to biotechnology and pharmaceutical companies, as well as academic institutions, in navigating the complex and often capital-intensive landscape of cell and gene therapy manufacturing. These services are vital for accelerating the pipeline from research and development phases through to clinical trials and eventual market launch, ensuring adherence to stringent regulatory standards such as Good Manufacturing Practices (GMP).

The product description for these services includes process development, which involves optimizing cell expansion, viral vector production, and gene modification protocols to enhance efficiency, scalability, and yield. It also covers cGMP manufacturing, which ensures that products are consistently produced and controlled according to quality standards appropriate to their intended use, minimizing risks inherent in any pharmaceutical production. Additionally, services extend to cell banking, analytical testing for purity, potency, and safety, and final fill/finish operations, preparing the therapies for patient administration. The primary objective is to enable clients to outsource non-core manufacturing activities, leverage specialized expertise, and scale production as their therapeutic candidates advance through clinical stages.

Major applications for cell and gene therapy manufacturing services are predominantly found in critical therapeutic areas, notably oncology, where CAR T-cell therapies and oncolytic viruses are transforming cancer treatment. Rare genetic diseases, often addressed by gene replacement or editing therapies, also heavily rely on these services due to the highly specialized nature of their production. Beyond these, autoimmune diseases, infectious diseases, and regenerative medicine are emerging fields that increasingly utilize these advanced therapeutic modalities. The key benefits for clients engaging these services include accelerated drug development timelines, access to cutting-edge manufacturing technologies and expertise without significant upfront capital investment, enhanced cost-efficiency through economies of scale, and robust support in achieving and maintaining regulatory compliance across diverse global markets. These factors, alongside a rapidly expanding therapeutic pipeline and increasing regulatory approvals, serve as significant driving forces for market expansion.

The Cell & Gene Therapy Manufacturing Services Market is experiencing robust growth, driven by an expanding pipeline of advanced therapeutic candidates and increasing outsourcing trends within the biopharmaceutical industry. Key business trends indicate a significant shift towards strategic partnerships and consolidation among Contract Development and Manufacturing Organizations (CDMOs) to offer integrated end-to-end solutions, from early-stage process development to commercial manufacturing. There is a growing demand for specialized viral vector manufacturing capabilities and robust analytical testing services, reflecting the complexity and strict regulatory requirements of these innovative therapies. Companies are investing heavily in advanced automation, closed-system technologies, and data analytics to enhance manufacturing efficiency, reduce costs, and improve product quality and consistency across various scales of operation.

Regionally, North America and Europe continue to dominate the market, primarily due to well-established biopharmaceutical infrastructure, substantial research and development investments, supportive regulatory frameworks, and a high concentration of key market players and academic institutions. These regions benefit from a mature ecosystem that fosters innovation and commercialization of cell and gene therapies. However, the Asia Pacific region is rapidly emerging as a significant growth hub, propelled by increasing government initiatives to boost biotechnology, a growing patient population, favorable investment climates, and the development of local CDMO capabilities. Countries like China, Japan, and South Korea are witnessing substantial growth in both R&D and manufacturing capacity, driven by efforts to reduce reliance on Western manufacturing bases and to capitalize on competitive operational costs.

Segmentation trends highlight a strong demand for cGMP manufacturing services, particularly for clinical and commercial-scale production, as more therapies advance through regulatory pathways and secure market authorization. Within product types, both autologous and allogeneic cell therapies, alongside viral vector-based gene therapies, are showing substantial growth, each presenting unique manufacturing challenges and opportunities. The oncology therapeutic area remains the largest segment, but significant expansion is also observed in rare genetic diseases and autoimmune disorders. End-user demand is predominantly driven by biotechnology and pharmaceutical companies seeking to leverage external expertise and infrastructure to mitigate the high costs and technical complexities associated with in-house manufacturing, thereby accelerating their product pipelines and market entry strategies.

Common user questions regarding the impact of Artificial Intelligence (AI) on the Cell & Gene Therapy Manufacturing Services Market often revolve around efficiency gains, cost reductions, quality control enhancements, and the acceleration of drug development timelines. Users are keen to understand how AI can optimize complex biological processes, predict manufacturing outcomes, automate repetitive tasks, and manage the vast datasets generated during therapy production. Concerns frequently surface about the ethical implications of AI in personalized medicine, data security in sensitive biological information, and the potential for job displacement or the need for a highly skilled, AI-literate workforce. Expectations are high that AI will revolutionize scalability, consistency, and the overall reliability of manufacturing processes, making these advanced therapies more accessible and affordable.

The integration of AI in cell and gene therapy manufacturing services is poised to profoundly transform various operational aspects, offering solutions to some of the industry's most pressing challenges. AI algorithms can analyze vast quantities of data from process development, manufacturing runs, and quality control assays, identifying subtle patterns and correlations that human analysis might miss. This capability enables more precise process optimization, leading to higher yields, improved product quality, and reduced batch-to-batch variability. For instance, AI-driven predictive analytics can forecast equipment failures or identify potential deviations in cell growth or viral vector titer, allowing for proactive interventions and minimizing costly production losses. The predictive power of AI significantly enhances process robustness and reliability, which is crucial for therapies with limited shelf-life and patient-specific manufacturing requirements.

Furthermore, AI facilitates greater automation and efficiency across the manufacturing workflow. From automated cell counting and viability assessment using computer vision to robotic systems for sterile liquid handling and fill/finish, AI-powered automation reduces manual labor, mitigates human error, and ensures a more consistent manufacturing environment. This is particularly important for autologous therapies, where each batch is unique to a single patient. AI also plays a critical role in supply chain management, optimizing logistics for sensitive raw materials and finished products, and in quality assurance, by accelerating the review of batch records and ensuring compliance. By streamlining these complex and time-consuming tasks, AI directly contributes to accelerating the availability of life-saving therapies while simultaneously driving down their overall production costs, thereby addressing key market constraints and expanding access to patients globally.

The Cell & Gene Therapy Manufacturing Services Market is shaped by a powerful confluence of drivers, restraints, opportunities, and pervasive impact forces. A primary driver is the exponential growth in the number of cell and gene therapy candidates progressing through preclinical and clinical development, fueled by significant investments from pharmaceutical companies, venture capitalists, and government funding agencies. This burgeoning pipeline, coupled with increasing regulatory approvals for innovative therapies, creates an urgent demand for specialized manufacturing capabilities that often exceed the in-house capacity or expertise of many developers. The inherent complexity of manufacturing these living medicines, which involves intricate biological processes, stringent quality control, and specialized aseptic techniques, further compels companies to outsource to experienced CDMOs. The benefits of outsourcing, including access to cutting-edge technology, cost efficiencies, and accelerated timelines, are strong motivators for market expansion. Furthermore, the rising global prevalence of chronic and rare diseases, for which cell and gene therapies offer potentially curative solutions, also drives sustained demand for these manufacturing services, making them indispensable to the therapeutic landscape.

Despite these robust drivers, the market faces significant restraints that temper its growth. The exceptionally high cost of developing and manufacturing cell and gene therapies presents a substantial barrier, often translating into steep prices for patients and healthcare systems. The complex and often bespoke nature of these manufacturing processes, especially for autologous therapies where each batch is patient-specific, creates scalability challenges and limits throughput. Moreover, the stringent and evolving regulatory landscape across different regions imposes significant hurdles, requiring specialized expertise and substantial investment in quality management systems and validation, which can be difficult for smaller developers to manage. A persistent challenge is the limited availability of a highly skilled workforce proficient in cell and gene therapy manufacturing, from process development scientists to quality control analysts, leading to talent shortages and increased operational costs. These factors collectively necessitate a robust and adaptable manufacturing services ecosystem to overcome such inhibitors.

Opportunities within this dynamic market are vast and multifaceted. Emerging markets, particularly in Asia Pacific, represent untapped potential as healthcare infrastructure develops and regulatory pathways become more defined, offering new avenues for manufacturing expansion and patient access. The exploration of new therapeutic areas beyond oncology and rare diseases, such as infectious diseases, cardiovascular conditions, and neurodegenerative disorders, promises to broaden the market scope and diversify service demand. Technological advancements, including the adoption of advanced automation, continuous manufacturing platforms, closed-system bioreactors, and AI-driven analytics, offer pathways to improve efficiency, reduce costs, and enhance scalability, thereby addressing key restraints. Strategic partnerships, collaborations between CDMOs, technology providers, and academic institutions, are creating integrated solutions and fostering innovation. Furthermore, the growing focus on allogeneic therapies, which offer the potential for off-the-shelf products and simplified logistics, represents a significant opportunity for streamlined manufacturing processes and broader market reach, ultimately driving the evolution and expansion of manufacturing services.

The impact forces within this market are profound and exert considerable pressure on its development. The constant demand for specialized expertise in viral vector production, cell expansion, and analytical testing requires continuous investment in talent and technology by service providers. The imperative for scalability is ever-present, as therapies move from small-batch clinical production to large-scale commercial supply, demanding adaptable and robust manufacturing solutions. Pressure on cost-effectiveness from payers and healthcare systems forces CDMOs to innovate and optimize processes to make these therapies more economically viable. The rapid pace of scientific advancement and the evolving regulatory landscape necessitate agility and continuous adaptation from manufacturing service providers. These forces ensure that only those CDMOs capable of offering innovative, compliant, scalable, and cost-efficient solutions will thrive in this highly competitive and transformative market.

The Cell & Gene Therapy Manufacturing Services Market is rigorously segmented to reflect the diverse operational needs, product types, scales of development, therapeutic applications, and client bases within this rapidly evolving industry. This granular analysis provides a comprehensive understanding of market dynamics, identifying key growth areas and competitive landscapes across various dimensions. The segmentation allows stakeholders to pinpoint specific opportunities, tailor service offerings, and strategize effectively in a market characterized by high technical complexity and stringent regulatory demands. Understanding these segments is crucial for both service providers aiming to optimize their capabilities and therapeutic developers seeking the most appropriate external partners for their unique product pipelines.

The market can be broadly segmented by the type of services offered, which includes everything from foundational process development to the final preparation of therapeutic products for patient administration. Another critical dimension is the product type being manufactured, encompassing different cell therapy modalities and gene therapy approaches, each with distinct manufacturing requirements. The scale of operation segment differentiates between preclinical, clinical, and commercial manufacturing, reflecting the varying volumes and regulatory maturities required at each stage of product lifecycle. Furthermore, segmentation by therapeutic area highlights the primary disease indications these therapies address, revealing where the most significant demand and innovation are concentrated. Lastly, identifying the end-users helps delineate the client base, including the types of organizations that predominantly rely on outsourced manufacturing expertise. This multifaceted segmentation approach ensures a holistic view of the market's structure and growth trajectories.

Each segment holds unique challenges and opportunities. For instance, process development services are crucial for early-stage innovation and optimization, impacting the entire downstream manufacturing process. cGMP manufacturing, especially at commercial scale, requires significant capital investment, advanced quality systems, and regulatory expertise. Autologous cell therapies, while highly personalized, demand intricate logistical coordination and patient-specific manufacturing, whereas allogeneic therapies offer potential for large-scale, off-the-shelf production. Oncology remains the dominant therapeutic area due to a high volume of pipeline products and approvals, but emerging applications in rare diseases and regenerative medicine are diversifying the market. Ultimately, a detailed understanding of these segments enables market players to specialize, innovate, and strategically position themselves to meet the specific and evolving demands of the cell and gene therapy sector.

The value chain for the Cell & Gene Therapy Manufacturing Services Market is intricate and highly specialized, reflecting the advanced nature of these therapeutic modalities. It begins with critical upstream activities, encompassing the procurement and preparation of essential raw materials. This includes sourcing high-quality, clinical-grade cells (e.g., patient-derived cells for autologous therapies, or donor cells for allogeneic approaches), specialized viral vectors for gene delivery (such as AAV or lentivirus), cell culture media, reagents, and other consumables. Manufacturers of these raw materials and specialized equipment (like bioreactors, cell sorters, and analytical instruments) form the foundational layer of the upstream segment, providing the critical inputs necessary for the complex manufacturing processes that follow. The quality and availability of these upstream components are paramount, as they directly impact the safety, efficacy, and manufacturability of the final therapeutic product.

At the core of the value chain are the contract development and manufacturing organizations (CDMOs) and in-house manufacturing units of large biopharmaceutical companies that perform the actual manufacturing services. This midstream segment involves sophisticated process development to optimize cell expansion, gene transduction, and purification protocols, followed by cGMP manufacturing, which includes cell processing, viral vector production, gene modification, and formulation. Analytical testing for identity, purity, potency, and safety is integrated throughout this stage to ensure product quality and regulatory compliance. The expertise, technology, and quality systems implemented by these manufacturing service providers are critical value-adding steps, transforming raw biological materials into highly complex therapeutic products ready for clinical use or commercial distribution. The ability to scale up or down production efficiently while maintaining stringent quality standards is a key differentiator in this central part of the value chain.

The downstream analysis primarily focuses on the final stages of product preparation, distribution, and administration. This includes aseptic fill/finish services, where the manufactured cell or gene therapy product is packaged into its final container (e.g., cryobags or vials). Following this, specialized logistics and cold chain management are essential, as many cell and gene therapies require ultra-low temperature storage and precise handling during transport to clinical sites or treatment centers. The distribution channel is typically direct, involving close coordination between the manufacturer, specialized logistics providers, and the healthcare facility where the therapy will be administered to the patient. Indirect channels may involve third-party logistics (3PL) providers specialized in biopharmaceuticals. The direct nature of this distribution ensures traceability and maintains the integrity and viability of these highly sensitive products. The final value is realized when the therapy successfully reaches the patient, underscoring the interconnectedness and critical importance of every step in this complex value chain, from raw material sourcing to patient delivery.

The primary potential customers for Cell & Gene Therapy Manufacturing Services are diverse and span across the biopharmaceutical ecosystem, driven by the specialized nature and high investment required for in-house manufacturing of these advanced therapies. Pharmaceutical companies, particularly those expanding into the ATMP space, represent a significant client segment. While large pharmaceutical companies may possess some internal manufacturing capabilities, they frequently outsource specific stages or entire production processes to CDMOs to leverage specialized expertise, accelerate timelines, manage capacity fluctuations, and mitigate the substantial capital expenditure associated with building and maintaining state-of-the-art CGT facilities. Outsourcing allows them to focus their resources on core competencies such as R&D, clinical development, and commercialization, enhancing strategic flexibility.

Biotechnology companies, especially small to mid-sized enterprises (SMEs) and emerging biotechs, constitute another crucial segment of potential customers. These companies often lack the extensive financial resources, infrastructure, or technical bandwidth required for the complex manufacturing of cell and gene therapies. For them, partnering with an experienced CDMO is not merely a strategic choice but an operational necessity. CDMOs provide access to critical cGMP-compliant facilities, advanced manufacturing technologies, and a skilled workforce that would otherwise be unattainable. This enables biotech firms to bring their innovative therapeutic candidates through preclinical and clinical development phases efficiently and cost-effectively, significantly lowering their entry barriers into this high-growth market.

Academic and research institutions, including university medical centers and non-profit research organizations, also serve as significant end-users. While their primary focus is often on early-stage discovery and preclinical research, as their promising therapeutic candidates advance towards clinical trials, they require cGMP-compliant manufacturing to produce materials for human use. These institutions typically do not have the infrastructure or regulatory expertise for such advanced manufacturing, making CDMO partnerships essential. Additionally, clinical trial sponsors, who may include a combination of pharmaceutical companies, biotechs, and academic consortia, rely on these services to ensure consistent and compliant production of investigational medicinal products (IMPs) for their ongoing studies. The demand from these varied end-user segments underscores the critical role that specialized manufacturing service providers play in the overall advancement and commercialization of cell and gene therapies.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 21.50 Billion |

| Market Forecast in 2032 | USD 98.41 Billion |

| Growth Rate | 24.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Lonza, Catalent, Fujifilm Diosynth Biotechnologies, Charles River Laboratories, Thermo Fisher Scientific, WuXi Advanced Therapies, AGC Biologics, Aldevron, KBI Biopharma, MilliporeSigma (Merck KGaA), Recipharm, Exothera, Roslin CT, Novartis Gene Therapies, BioNTech, Legend Biotech, Cellectis, ElevateBio, Oxford Biomedica, Sartorius AG |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Cell & Gene Therapy Manufacturing Services Market is underpinned by a rapidly evolving and highly specialized technology landscape, crucial for addressing the unique complexities of producing advanced therapeutic medicinal products. A cornerstone of this landscape involves advanced viral vector production technologies, which are essential for delivering genetic material into target cells in gene therapies. This includes sophisticated bioreactor systems capable of high-titer adeno-associated virus (AAV) and lentivirus production, alongside downstream purification techniques like chromatography and tangential flow filtration (TFF) designed to yield clinical-grade vectors. The efficiency and scalability of these vector production platforms directly influence the feasibility and cost-effectiveness of gene therapy manufacturing, necessitating continuous innovation in cell line development and process intensification to meet increasing demand.

Another pivotal area is the development and adoption of closed-system and automated manufacturing platforms for cell therapy production. These systems minimize human intervention, thereby reducing the risk of contamination, enhancing sterility, and increasing batch-to-batch consistency—a critical factor for patient-specific autologous therapies and large-scale allogeneic production. Technologies like automated cell processing instruments, integrated bioreactors for cell expansion, and robotic liquid handling systems are becoming standard, replacing manual, open-pan methods. Single-use bioreactor and filtration technologies are also gaining prominence due to their benefits in reducing cleaning and validation costs, improving turnaround times between batches, and mitigating cross-contamination risks, especially important in multi-product facilities.

Furthermore, the key technology landscape includes sophisticated analytical instrumentation and data management solutions vital for comprehensive quality control and process monitoring. Techniques such as flow cytometry for cell characterization, mass spectrometry for protein and metabolite analysis, quantitative PCR for gene copy number assessment, and high-throughput sequencing for genetic integrity verification are indispensable for ensuring product safety, potency, and identity. Complementing these analytical tools are advanced data analytics platforms, often incorporating artificial intelligence and machine learning, to process the vast amounts of generated data. These platforms enable real-time process monitoring, predictive maintenance, and in-depth understanding of critical process parameters, ultimately optimizing manufacturing efficiency, facilitating regulatory submissions, and ensuring the consistent production of high-quality, life-saving cell and gene therapies. The continuous evolution and integration of these technologies are paramount for the future growth and accessibility of the cell and gene therapy market.

The global Cell & Gene Therapy Manufacturing Services Market exhibits distinct regional dynamics driven by varying levels of research and development investment, regulatory maturity, industrial infrastructure, and patient demographics. North America, particularly the United States, stands as the unequivocal leader in this market. This dominance is attributable to a robust biopharmaceutical industry, significant government and private funding for advanced therapies, a high concentration of leading academic research institutions, and a proactive regulatory environment through agencies like the FDA, which has facilitated numerous therapy approvals. The region boasts a substantial number of clinical trials for cell and gene therapies, creating consistent demand for specialized manufacturing services. Canada also contributes significantly with its strong research base and developing manufacturing capabilities. The presence of numerous key market players and a well-established outsourcing culture further solidify North America's leading position, making it a hotbed for innovation and commercialization in the CGT space.

Europe represents another major market for cell and gene therapy manufacturing services, characterized by strong scientific foundations, supportive governmental initiatives, and a growing number of approved therapies. Countries like the United Kingdom, Germany, France, and Switzerland are at the forefront, leveraging their expertise in biotechnology and pharmacology. The European Medicines Agency (EMA) plays a crucial role in harmonizing regulatory pathways, which, while complex, provides a clear framework for development and manufacturing. Investment in state-of-the-art facilities and a collaborative environment between academia and industry contribute to the region's strong growth trajectory. European CDMOs are increasingly expanding their capacities to meet both local and global demand, fostering a competitive landscape. The region's commitment to advancing ATMPs ensures sustained demand for specialized manufacturing support, making it a critical hub for global therapy development and production.

The Asia Pacific (APAC) region is emerging as the fastest-growing market segment, driven by increasing healthcare expenditure, a large patient population, improving regulatory frameworks, and government efforts to promote domestic biomanufacturing. Countries such as China, Japan, South Korea, and Australia are investing heavily in biotechnology research and infrastructure, aiming to become global leaders in cell and gene therapy development. Lower operational costs and a growing pool of skilled labor further attract foreign investment and encourage the establishment of new manufacturing facilities within the region. While still behind North America and Europe in terms of commercialized therapies, the rapid pace of clinical trials and the development of local CDMO capabilities indicate substantial future growth. Latin America, the Middle East, and Africa (MEA) represent nascent but promising markets, with increasing awareness, improving healthcare access, and forming strategic partnerships with global players to develop their own capabilities in this specialized field, albeit at a slower pace compared to the more established regions.

The primary driver is the significant increase in the number of cell and gene therapy candidates in preclinical and clinical development, coupled with a rising trend of outsourcing manufacturing to specialized CDMOs due to the therapies' complexity, high capital requirements, and the need for expert regulatory compliance.

Key challenges include the high cost of therapy development and manufacturing, the complexity and bespoke nature of manufacturing processes (especially for autologous therapies), stringent and evolving global regulatory hurdles, scalability issues from clinical to commercial production, and a persistent shortage of skilled personnel.

AI is transforming manufacturing by enabling advanced process optimization through predictive analytics, automating quality control and monitoring, accelerating drug discovery, improving supply chain logistics, and reducing human error. This leads to increased efficiency, consistency, and potential cost reductions, making therapies more accessible.

North America and Europe currently dominate the market due to their established biopharmaceutical infrastructure, substantial R&D investments, supportive regulatory environments, and a high concentration of key industry players. However, the Asia Pacific region is rapidly emerging as a significant growth hub.

Cell & Gene Therapy manufacturers offer a comprehensive range of services including process development and optimization, cGMP manufacturing (cell expansion, viral vector production, gene modification), cell banking, extensive analytical testing for quality and safety, and final fill/finish services for preparing therapeutic products.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.