ID : MRU_ 430817 | Date : Nov, 2025 | Pages : 251 | Region : Global | Publisher : MRU

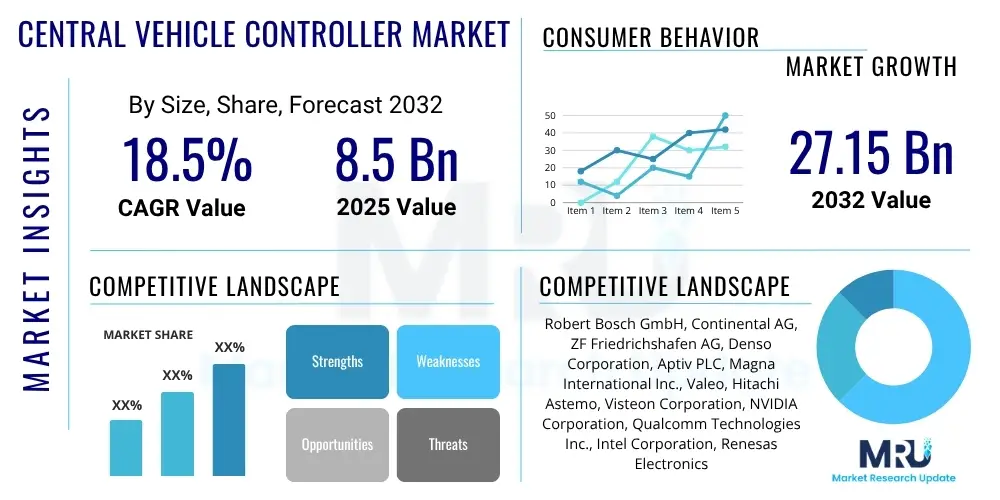

The Central Vehicle Controller Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2032. The market is estimated at USD 8.5 Billion in 2025 and is projected to reach USD 27.15 Billion by the end of the forecast period in 2032.

The Central Vehicle Controller CVC market represents a pivotal shift in automotive electronic architectures, moving from distributed electronic control units ECU to a more consolidated, domain-centralized approach. A CVC is a high-performance computing platform designed to integrate and manage multiple vehicle functions, processing vast amounts of data from various sensors and systems. This consolidation enhances computational efficiency, reduces wiring complexity, and enables advanced features previously impossible with individual ECUs.

Major applications of CVCs span across critical automotive domains including Advanced Driver Assistance Systems ADAS, infotainment and telematics, powertrain management, and body electronics. These controllers facilitate sophisticated functionalities such as autonomous driving capabilities, seamless in-car connectivity, predictive maintenance, and personalized user experiences. The inherent benefits of CVCs include improved system integration, enhanced functional safety, reduced manufacturing costs due to fewer components, and simplified over-the-air OTA update mechanisms for continuous software improvement.

The market's robust growth is primarily driven by the accelerated adoption of electric vehicles EVs, the relentless pursuit of higher levels of autonomous driving, and the pervasive demand for connected car features. As vehicles transform into complex software-defined platforms, the need for a powerful, centralized brain becomes paramount to manage the increasing data flow, intricate algorithms, and real-time decision-making processes, thereby solidifying the CVC's role as a fundamental component of future mobility.

The Central Vehicle Controller CVC market is undergoing a significant transformation, driven by fundamental shifts in automotive technology and consumer expectations. Business trends indicate a strong move towards software-defined vehicles, prompting automotive OEMs and Tier 1 suppliers to invest heavily in integrated hardware and software solutions that support high-performance computing and centralized control. This has led to strategic partnerships and acquisitions focused on consolidating expertise in semiconductor technology, artificial intelligence, and cybersecurity, aiming to offer comprehensive, scalable CVC platforms.

Regional trends highlight the Asia Pacific APAC region as a dominant force in the CVC market, propelled by its massive automotive production volumes and rapid adoption of electric vehicles and ADAS technologies, particularly in China and South Korea. Europe is characterized by stringent safety regulations and a strong emphasis on premium and luxury vehicle segments, driving demand for advanced CVCs that support sophisticated safety and infotainment features. North America, with its pioneering efforts in autonomous vehicle development and a consumer base eager for cutting-edge technology, is witnessing substantial investment in CVCs designed for higher levels of automation and connected services.

Segment trends underscore the increasing importance of CVCs in ADAS and safety applications, with a growing demand for controllers capable of real-time processing of sensor data for critical decision-making. The infotainment and telematics segment is also expanding rapidly, as CVCs enable rich, personalized in-car experiences and seamless connectivity. Furthermore, there is a clear trajectory towards more powerful microprocessors and specialized AI accelerators within CVCs, essential for handling the computational demands of future automotive functionalities, signalling a robust and dynamic market landscape.

User inquiries regarding AI's influence on the Central Vehicle Controller market frequently center on how AI can enhance performance, improve safety, and enable autonomous capabilities. Common questions revolve around the practical applications of AI in CVCs, potential cybersecurity vulnerabilities introduced by advanced AI systems, the computational demands of integrating AI, and the regulatory challenges associated with AI-driven autonomous functions. Users also express interest in how AI will personalize the driving experience and contribute to predictive maintenance, while raising concerns about the complexity of AI software development and its verification and validation processes within CVCs.

AI's integration into Central Vehicle Controllers is fundamentally reshaping automotive intelligence, allowing CVCs to move beyond deterministic control to predictive analytics and adaptive decision-making. By processing vast datasets from vehicle sensors in real-time, AI algorithms within CVCs can detect complex patterns, anticipate potential hazards, and optimize vehicle performance with unprecedented precision. This capability is crucial for advancing autonomous driving, where AI facilitates everything from perception and localization to path planning and behavioral prediction, making vehicles more responsive and safer. Beyond autonomy, AI in CVCs enhances user experience through intelligent infotainment systems, personalized comfort settings, and proactive vehicle diagnostics, identifying maintenance needs before they become critical issues.

However, the adoption of AI also introduces significant complexities and challenges. Ensuring the robustness and trustworthiness of AI algorithms, particularly in safety-critical applications, is paramount and requires rigorous testing and validation processes. Cybersecurity becomes an even greater concern as AI-powered CVCs represent a larger attack surface, necessitating sophisticated encryption and intrusion detection systems. Furthermore, the high computational requirements of advanced AI models demand powerful, energy-efficient processors and optimized software architectures, driving innovation in semiconductor technology and automotive software development. The future of CVCs is intrinsically linked with the continuous evolution and responsible deployment of artificial intelligence.

The Central Vehicle Controller market is profoundly influenced by a complex interplay of Drivers, Restraints, and Opportunities, alongside broader Impact Forces that shape its trajectory. Key drivers propelling market expansion include the accelerating global shift towards electric and autonomous vehicles, which demand highly integrated and powerful processing units to manage their intricate systems and vast data flows. The increasing sophistication of Advanced Driver Assistance Systems ADAS, coupled with stringent global safety regulations, also necessitates more capable CVCs. Furthermore, the burgeoning concept of software-defined vehicles, where functionalities are increasingly managed through code and updated over-the-air, inherently relies on a centralized, high-performance controller, acting as a crucial enabler for this automotive paradigm shift.

Despite these strong growth drivers, the CVC market faces several significant restraints. The exceptionally high research and development costs associated with designing and validating these complex systems, coupled with the rigorous functional safety standards ISO 26262 and cybersecurity requirements, present substantial barriers to entry and innovation. The inherent complexity of integrating diverse vehicle functions into a single controller, along with the need for industry-wide standardization in hardware interfaces and software protocols, poses significant technical hurdles. Additionally, vulnerabilities within the global automotive supply chain for semiconductors and other critical components can impact production and market growth, highlighting the need for robust risk management strategies.

Opportunities for market players are abundant and diverse. The shift towards zonal architectural designs, which simplify wiring harnesses and further consolidate control, offers a pathway for more efficient and scalable CVC implementations. The ability to deliver frequent over-the-air OTA software updates transforms vehicles into continuously improving platforms, opening new revenue streams for OEMs and software providers. Furthermore, the expansion of vehicle-to-everything V2X communication technologies and the emergence of new mobility services such as ride-sharing and robotaxis create fresh avenues for CVC deployment, demanding controllers that can seamlessly manage connectivity, data analytics, and fleet operations. These evolving trends present significant potential for innovative solutions and market leadership.

The Central Vehicle Controller market is meticulously segmented to provide a granular understanding of its diverse components, technologies, applications, and end-user types. This segmentation allows for a comprehensive analysis of market dynamics, growth opportunities, and competitive landscapes across various dimensions of the automotive industry. By categorizing the market based on specific criteria, stakeholders can better identify target audiences, tailor product development strategies, and forecast demand more accurately.

The segmentation primarily considers the internal architecture and capabilities of CVCs, their functional roles within the vehicle, and the types of vehicles they are integrated into. This detailed breakdown highlights the varying demands placed on CVCs by different automotive sectors and technological advancements. For instance, the requirements for a CVC in an entry-level passenger vehicle differ significantly from those in a premium autonomous electric vehicle, necessitating distinct hardware and software configurations. Understanding these distinctions is crucial for effective market penetration and innovation.

The value chain for the Central Vehicle Controller market is intricate, involving a diverse set of participants from upstream component suppliers to downstream end-users. At the upstream end, the value chain begins with semiconductor manufacturers and software developers who provide the foundational hardware and operating systems essential for CVC functionality. These include specialized chipmakers producing high-performance microcontrollers, microprocessors, and AI accelerators, as well as companies developing real-time operating systems, middleware, and automotive-grade software platforms like AUTOSAR. Sensor suppliers also play a critical role, providing the raw data inputs that CVCs process for various vehicle functions, ranging from radar and lidar to cameras and ultrasonic sensors.

Moving downstream, Tier 1 automotive suppliers are pivotal integrators in the CVC ecosystem. These companies develop and assemble the actual CVC modules, often incorporating components from various upstream providers, and adding their proprietary hardware and software layers. They are responsible for ensuring the functional safety, cybersecurity, and overall performance of the CVC system before supplying it to vehicle manufacturers. Automotive Original Equipment Manufacturers OEMs then integrate these CVCs into their vehicle platforms, designing the vehicle's electrical and electronic architecture around these central controllers. Post-sales, the downstream also includes aftermarket service providers who handle diagnostics, repairs, and software updates, though much of the advanced software updating is now managed directly by OEMs via over-the-air mechanisms.

Distribution channels predominantly involve direct relationships between Tier 1 suppliers and OEMs, given the highly customized and integrated nature of CVC solutions. These are often long-term strategic partnerships involving co-development. Indirect channels are less prevalent for the primary CVC unit but exist for some standard components or aftermarket parts through authorized distributors. The increasing complexity and strategic importance of CVCs mean that direct collaboration and robust supply chain management between all key players are critical for successful market operation and innovation, ensuring seamless integration and performance across the entire automotive value chain.

The primary potential customers and end-users of Central Vehicle Controllers are entities within the global automotive industry that design, manufacture, and operate vehicles, particularly those focused on advanced technological integration. Automotive Original Equipment Manufacturers OEMs, such as major car manufacturers across passenger and commercial vehicle segments, represent the largest customer base. These OEMs directly procure CVCs or integrate CVC systems from their Tier 1 suppliers to build their next-generation vehicle architectures, which increasingly feature high levels of automation, connectivity, and electrification.

Tier 1 automotive suppliers also function as significant purchasers and developers in this market. While they supply integrated CVC solutions to OEMs, they themselves are customers for the underlying semiconductor components, specialized software, and development tools required to build these complex controllers. Companies like Bosch, Continental, and Aptiv invest heavily in CVC technology to offer comprehensive solutions to their OEM clients, making them both suppliers and significant consumers of CVC sub-components and intellectual property.

Beyond traditional manufacturers, emerging players in new mobility services, such as autonomous robotaxi operators and large fleet management companies, are also becoming critical potential customers. These entities require robust and reliable CVCs to manage their fleets of highly automated or connected vehicles, emphasizing scalability, remote diagnostic capabilities, and efficient data processing for optimized operations. As the automotive landscape continues to evolve, the customer base for CVCs will broaden, encompassing any entity at the forefront of automotive innovation and advanced vehicle deployment.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 8.5 Billion |

| Market Forecast in 2032 | USD 27.15 Billion |

| Growth Rate | 18.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG, Denso Corporation, Aptiv PLC, Magna International Inc., Valeo, Hitachi Astemo, Visteon Corporation, NVIDIA Corporation, Qualcomm Technologies Inc., Intel Corporation, Renesas Electronics Corporation, Infineon Technologies AG, NXP Semiconductors N.V., Texas Instruments Incorporated, STMicroelectronics, Micron Technology Inc., Mobileye (an Intel Company), Tesla Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Central Vehicle Controller market is characterized by a rapidly evolving technological landscape, driven by the intense demand for higher processing power, enhanced connectivity, and robust cybersecurity. At its core, the technology revolves around high-performance computing platforms that integrate powerful microprocessors MPUs and microcontrollers MCUs, often augmented by specialized accelerators for artificial intelligence AI and digital signal processing DSP. These platforms are designed to handle vast amounts of data generated by an increasing number of sensors and communicate efficiently across the vehicle network, leveraging advanced automotive Ethernet and CAN FD FlexRay protocols for high-speed, reliable data exchange.

Software-defined vehicle architectures are a cornerstone of the modern CVC, relying heavily on sophisticated operating systems and middleware, such as AUTOSAR Adaptive, to manage complex software layers and facilitate over-the-air OTA updates. Functional safety is paramount, with CVCs being developed in accordance with ISO 26262 standards to ensure system reliability and mitigate risks in safety-critical applications like ADAS and autonomous driving. Cybersecurity is also a foundational technological requirement, incorporating hardware security modules HSM, secure boot mechanisms, and advanced encryption protocols to protect against external threats and ensure data integrity.

Emerging technologies like quantum computing and advanced neuromorphic chips are on the horizon, promising even greater processing capabilities for future CVCs. Furthermore, the development ecosystem is increasingly relying on advanced simulation and hardware-in-the-loop HIL testing to validate CVC functionality and performance before physical prototyping. The convergence of these hardware, software, and validation technologies defines the cutting-edge of the Central Vehicle Controller market, continually pushing the boundaries of automotive innovation and intelligence.

A Central Vehicle Controller (CVC) is a high-performance computing platform in modern vehicles that integrates and manages multiple electronic control functions, processing data from various sensors and systems to enable advanced features like autonomous driving and infotainment. It consolidates distributed ECUs into a centralized architecture, enhancing efficiency and reducing complexity.

The CVC market is growing rapidly due to the increasing adoption of electric vehicles (EVs), the accelerating development of autonomous driving technologies, and the rising demand for connected car features. The shift towards software-defined vehicles, requiring powerful centralized processing, is also a major driver.

AI significantly impacts CVCs by enabling real-time data processing, predictive analytics, and advanced decision-making for ADAS and autonomous functions. It enhances safety, personalizes user experiences, and optimizes vehicle performance, driving the need for more powerful and intelligent CVC hardware and software.

Key challenges include high research and development costs, stringent functional safety and cybersecurity requirements, the complexity of integrating diverse vehicle functions, and the need for industry-wide standardization. Supply chain vulnerabilities for critical components like semiconductors also pose a significant restraint.

Fundamental technologies include high-performance microprocessors and specialized AI accelerators, advanced automotive communication protocols like Ethernet and CAN FD, robust real-time operating systems (e.g., AUTOSAR), functional safety standards (ISO 26262), and comprehensive cybersecurity measures.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.