ID : MRU_ 430894 | Date : Nov, 2025 | Pages : 253 | Region : Global | Publisher : MRU

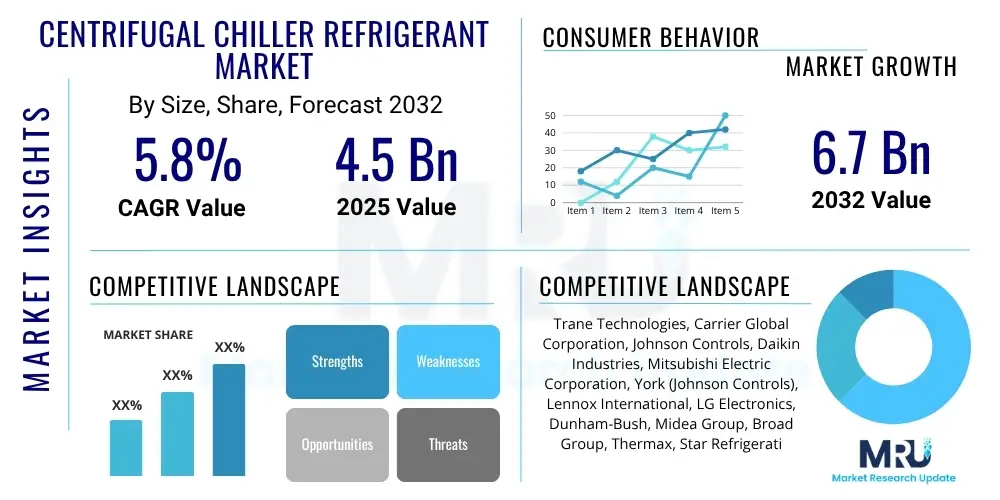

The Centrifugal Chiller Refrigerant Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2032. The market is estimated at $4.5 Billion in 2025 and is projected to reach $6.7 Billion by the end of the forecast period in 2032.

The Centrifugal Chiller Refrigerant Market encompasses the supply and demand for various refrigerants specifically designed for use in centrifugal chillers. Centrifugal chillers are large-capacity vapor compression machines widely deployed in commercial, industrial, and institutional settings for air conditioning and process cooling. These systems rely on high-efficiency compressors and heat exchangers, with the refrigerant acting as the critical medium for heat transfer, absorbing heat from the cooled space and rejecting it to the environment. The market is significantly influenced by global environmental regulations aimed at phasing out refrigerants with high Ozone Depletion Potential (ODP) and Global Warming Potential (GWP), driving innovation towards more sustainable alternatives.

The primary refrigerants utilized in this sector include hydrofluorocarbons (HFCs) such as R134a, hydrofluoroolefins (HFOs) like R1234yf and R1234ze, and an increasing focus on natural refrigerants such as ammonia (R717) and carbon dioxide (R744). Each refrigerant possesses distinct thermodynamic properties and environmental impacts, making selection crucial for specific applications. Major applications span large-scale HVAC systems in skyscrapers, shopping malls, airports, data centers, hospitals, and manufacturing plants, where energy efficiency, reliability, and cooling capacity are paramount. The product description emphasizes the need for refrigerants that offer optimal performance, safety, and compliance with evolving environmental standards.

The benefits associated with advanced centrifugal chiller refrigerants include enhanced energy efficiency, reduced carbon footprint, and improved operational longevity of cooling systems. These benefits are critical drivers for market growth, alongside increasing global infrastructure development, urbanization, and a heightened awareness of climate change. Stringent environmental regulations, such as the Kigali Amendment to the Montreal Protocol and regional F-Gas regulations, further accelerate the transition towards low-GWP refrigerants, creating significant opportunities for manufacturers of innovative and eco-friendly solutions. The market is thus propelled by a dual mandate of performance optimization and environmental stewardship.

The Centrifugal Chiller Refrigerant Market is undergoing a significant transformation driven by a confluence of business, regional, and segment trends. Business trends highlight a strong emphasis on sustainability, with companies investing heavily in research and development to introduce next-generation, low-GWP refrigerants. This involves not only the development of new chemical compounds but also the redesign of chiller systems to optimally utilize these new refrigerants, ensuring both performance and regulatory compliance. Moreover, a growing trend towards circular economy principles is evident, with increased focus on refrigerant recovery, recycling, and reclamation to minimize environmental impact and maximize resource efficiency.

Regionally, the market exhibits diverse dynamics. Asia Pacific stands out as a high-growth region, fueled by rapid urbanization, industrialization, and infrastructure expansion, particularly in emerging economies like China and India, leading to a surge in demand for large-capacity cooling solutions. North America and Europe, characterized by mature markets, are primarily driven by replacement demand, energy efficiency mandates, and stringent environmental regulations (e.g., F-Gas regulation in Europe) that accelerate the phase-down of high-GWP refrigerants. Latin America, the Middle East, and Africa are experiencing steady growth propelled by commercial and industrial development, albeit with varying rates of adoption for advanced refrigerants due to diverse regulatory landscapes and economic conditions.

Segment trends reveal a clear shift away from traditional HFCs towards HFOs and natural refrigerants. While HFCs currently hold a substantial market share, their growth is tempered by impending regulatory phase-downs. HFOs are rapidly gaining traction due to their ultralow GWP and similar performance characteristics to HFCs, making them a favored drop-in or near drop-in solution for many new chiller designs. Natural refrigerants like ammonia and CO2, despite their specific handling requirements, are also witnessing increased adoption, particularly in industrial and large commercial applications where their environmental benefits outweigh the installation complexities. This segmentation showcases a market in active transition towards a more environmentally conscious future, balanced against the critical need for efficient cooling.

User inquiries concerning AI's influence on the Centrifugal Chiller Refrigerant Market frequently revolve around how artificial intelligence can enhance efficiency, reduce operational costs, and aid in regulatory compliance. Key themes include the application of AI in optimizing chiller performance, enabling predictive maintenance, improving energy management, and facilitating the integration of chillers into smarter building ecosystems. Users are particularly interested in AI's role in diagnosing potential issues before they become critical, thereby extending equipment lifespan and ensuring continuous, efficient cooling while also managing refrigerant leakage and inventory more intelligently.

The Centrifugal Chiller Refrigerant Market is profoundly shaped by a dynamic interplay of drivers, restraints, opportunities, and external impact forces. A primary driver is the escalating global demand for energy-efficient cooling solutions across commercial, industrial, and residential sectors, fueled by urbanization, climate change, and economic development. The imperative to reduce operational costs and enhance sustainability drives end-users to adopt advanced chiller technologies and high-performance refrigerants. Concurrently, stringent environmental regulations, such as the global phase-down of high-GWP HFCs under the Kigali Amendment, act as a powerful catalyst for innovation, pushing manufacturers to develop and deploy low-GWP alternatives.

Despite these significant drivers, several restraints challenge market expansion. The high initial investment cost associated with new-generation centrifugal chillers and their compatible refrigerants can deter some potential adopters, particularly in developing regions. Furthermore, the complexities surrounding the safe handling, storage, and disposal of certain new refrigerants, some of which may have flammability or toxicity concerns, necessitate rigorous training and infrastructure upgrades. Regulatory inconsistencies across different nations and regions also create a fragmented market landscape, complicating global expansion strategies for manufacturers and leading to varied adoption rates of advanced refrigerant technologies.

Opportunities within the market primarily lie in the rapid growth of emerging economies, which are investing heavily in new infrastructure and commercial developments, creating fresh demand for large-capacity cooling systems. The continuous advancement in refrigerant technology, particularly the development of ultralow-GWP HFOs and optimized natural refrigerants, presents significant avenues for innovation and market penetration. Moreover, the integration of centrifugal chillers with smart building management systems and IoT platforms offers opportunities for enhanced operational efficiency and predictive maintenance services. Impact forces, including global economic cycles, technological advancements in compressor design, and intensifying environmental concerns, continually reshape market dynamics, compelling stakeholders to adapt to an evolving landscape characterized by both growth potential and inherent complexities.

The Centrifugal Chiller Refrigerant Market is comprehensively segmented to provide a detailed understanding of its diverse components and underlying market dynamics. This segmentation facilitates a granular analysis of various market aspects, including the types of refrigerants used, the capacity of the chillers, and the specific end-use industries they serve. Such a detailed breakdown is crucial for identifying key market trends, competitive landscapes, and growth opportunities across different categories, enabling stakeholders to make informed strategic decisions regarding product development, market entry, and investment.

The segmentation primarily revolves around the chemical composition and environmental profile of refrigerants, reflecting the industry's strong push towards sustainability. Capacity-based segmentation categorizes chillers by their cooling output, which directly correlates with the scale of the application, from medium-sized commercial buildings to expansive industrial complexes. Furthermore, end-use industry segmentation highlights the diverse applications of centrifugal chillers and their specific cooling requirements, from maintaining optimal climate conditions in office buildings to critical process cooling in manufacturing or data centers. This multi-dimensional approach ensures a holistic view of the market structure and its inherent complexities.

The value chain for the Centrifugal Chiller Refrigerant Market is intricate, involving multiple stages from raw material procurement to end-use application and eventual disposal or recycling. The upstream analysis begins with the chemical manufacturers who produce the core components and precursors for refrigerants, such as fluorocarbons for HFCs and HFOs, or suppliers of natural refrigerants like ammonia and CO2. These chemical companies form the foundational layer, providing essential ingredients to refrigerant producers and chiller manufacturers. Additionally, suppliers of specialized metals, plastics, and electronic components for chiller manufacturing are crucial upstream players, ensuring the availability of high-quality materials for system assembly.

Moving downstream, the value chain involves refrigerant producers and chiller original equipment manufacturers (OEMs) who design, assemble, and test the complete chiller units. These OEMs often collaborate closely with refrigerant suppliers to ensure compatibility and optimal performance of their systems with specific refrigerant types. Following manufacturing, the distribution channel plays a vital role. This includes a network of authorized distributors, wholesalers, and specialized HVAC contractors who facilitate the sale and installation of centrifugal chillers and their associated refrigerants to a wide range of end-users. These distributors also provide logistical support, ensuring timely delivery and inventory management.

The market employs both direct and indirect distribution models. Direct channels involve chiller OEMs selling directly to large commercial or industrial clients, often for bespoke projects requiring significant engineering and integration support. This allows for closer customer relationships and customized solutions. Indirect channels, which are more prevalent, involve sales through a network of independent contractors, installers, and service providers who purchase chillers and refrigerants from distributors. These intermediaries are critical for reaching a broader customer base, offering installation, commissioning, maintenance, and after-sales support. Post-installation, the value chain extends to maintenance service providers and specialized companies focusing on refrigerant recovery, recycling, and reclamation, which is increasingly important for environmental compliance and resource efficiency.

The Centrifugal Chiller Refrigerant Market serves a diverse range of end-users and buyers, primarily characterized by a demand for large-scale, efficient cooling solutions for comfort, process control, or environmental stability. Commercial enterprises constitute a significant segment of potential customers, including developers and owners of large office complexes, shopping malls, airports, hotels, and entertainment venues. These entities require robust HVAC systems to maintain comfortable indoor temperatures for occupants, which directly impacts customer experience and operational efficiency. The continuous growth in commercial infrastructure, especially in urban areas, consistently drives demand from this segment.

Industrial facilities represent another crucial customer base. This includes manufacturing plants across various sectors such as automotive, pharmaceuticals, chemicals, food and beverage, and electronics, where precise temperature control is vital for production processes, equipment longevity, and product quality. Data centers also fall under the industrial category, requiring immense cooling capacity to prevent overheating of servers and maintain optimal operating conditions, making them high-value customers for advanced, energy-efficient centrifugal chillers and their refrigerants. The reliability and uptime of cooling systems are non-negotiable for these critical operations, driving investment in high-quality solutions.

Institutional clients, comprising hospitals, universities, government buildings, and other large public and private organizations, also form a substantial part of the potential customer landscape. Hospitals, for instance, need reliable and consistent cooling for patient comfort, specialized medical equipment, and critical care environments. Educational institutions, especially large campuses, require centralized cooling for numerous buildings. These customers typically prioritize long-term operational efficiency, maintenance costs, and adherence to sustainability mandates, making them receptive to innovative, environmentally friendly refrigerant solutions that offer long-term value and compliance with evolving regulations.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $4.5 Billion |

| Market Forecast in 2032 | $6.7 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Trane Technologies, Carrier Global Corporation, Johnson Controls, Daikin Industries, Mitsubishi Electric Corporation, York (Johnson Controls), Lennox International, LG Electronics, Dunham-Bush, Midea Group, Broad Group, Thermax, Star Refrigeration, Smardt Chiller Group Inc., Multistack |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Centrifugal Chiller Refrigerant Market is driven by a dynamic technology landscape focused on enhancing efficiency, reducing environmental impact, and improving system intelligence. Key advancements include the widespread adoption of variable speed drive (VSD) technology, which allows chillers to adjust compressor speed to match cooling load demands, significantly improving part-load efficiency and reducing energy consumption. This technology is crucial for optimizing performance in diverse operating conditions, leading to substantial operational cost savings for end-users. Furthermore, the development and integration of magnetic bearing compressors are transforming the market by eliminating the need for oil, reducing friction, and improving mechanical efficiency, while also minimizing maintenance requirements and enhancing reliability.

Another significant technological trend involves the development and application of advanced refrigerants, particularly hydrofluoroolefins (HFOs) such as R1234yf and R1234ze, which boast ultralow Global Warming Potential (GWP) values. These refrigerants are designed to meet stringent environmental regulations while offering thermodynamic properties comparable to phased-out high-GWP HFCs. Alongside HFOs, there is a renewed and growing interest in natural refrigerants like ammonia (R717) and carbon dioxide (R744), especially in large industrial and specialized applications, driven by their excellent environmental profiles. The technological landscape also includes the continuous innovation in heat exchanger designs, optimizing heat transfer efficiency and enabling chillers to operate more effectively with these new-generation refrigerants.

The integration of intelligent controls and Internet of Things (IoT) capabilities is rapidly becoming a standard feature in modern centrifugal chillers. These smart systems incorporate advanced algorithms for real-time monitoring, diagnostic capabilities, and predictive maintenance, allowing operators to proactively identify and address potential issues. IoT connectivity facilitates remote monitoring, data analysis, and seamless integration with broader Building Management Systems (BMS), leading to optimized system performance, reduced downtime, and enhanced overall operational efficiency. These technological advancements collectively contribute to a more sustainable, efficient, and intelligent cooling infrastructure, addressing both economic and environmental objectives.

The primary refrigerants include Hydrofluorocarbons (HFCs) like R134a, Hydrofluoroolefins (HFOs) such as R1234yf and R1234ze, and natural refrigerants like Ammonia (R717) and Carbon Dioxide (R744). The choice depends on environmental impact, efficiency, and specific application requirements.

Environmental regulations, particularly those aimed at phasing down high Global Warming Potential (GWP) refrigerants, significantly drive the market. They necessitate a shift from traditional HFCs to low-GWP alternatives like HFOs and natural refrigerants, influencing product development and adoption rates globally.

Energy efficiency is a critical driver. End-users prioritize chillers and refrigerants that offer optimal efficiency to reduce operational costs and meet sustainability goals. Technologies like Variable Speed Drives and magnetic bearing compressors, coupled with advanced refrigerants, contribute to significant energy savings.

AI is transforming the market through predictive maintenance, optimizing energy consumption, enhancing fault detection, and enabling smarter chiller controls. It leads to improved reliability, reduced downtime, and more efficient operation of cooling systems by analyzing real-time data.

Key challenges include the high initial cost of new-generation chillers and refrigerants, complexities in handling novel refrigerant types (some with flammability or toxicity concerns), and fragmented regulatory landscapes across different regions. Ensuring safe and compliant adoption remains a priority.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.