ID : MRU_ 428725 | Date : Oct, 2025 | Pages : 255 | Region : Global | Publisher : MRU

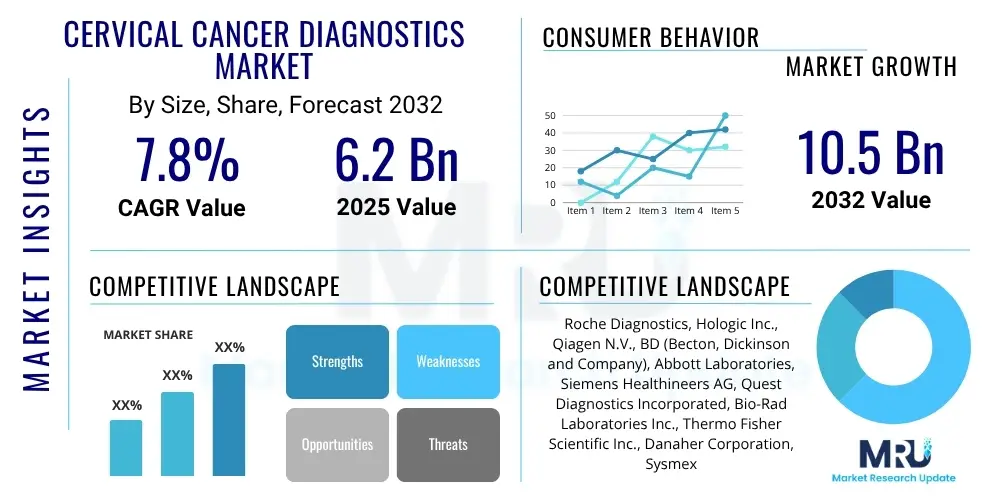

The Cervical Cancer Diagnostics Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2032. The market is estimated at USD 6.2 Billion in 2025 and is projected to reach USD 10.5 Billion by the end of the forecast period in 2032.

The Cervical Cancer Diagnostics Market encompasses a comprehensive array of medical tests, devices, and procedures meticulously developed for the effective screening, early detection, and definitive diagnosis of cervical cancer. This malignancy, primarily caused by persistent infection with high-risk human papillomaviruses (HPVs), poses a significant global health challenge, making robust diagnostic capabilities critically important. The core offerings within this market range from established cytological examinations, such as conventional Pap tests and advanced liquid-based cytology, to highly sensitive molecular tests designed for the detection of HPV DNA or RNA. Further diagnostic steps include visual assessments like colposcopy and tissue sampling via biopsy for histological confirmation, forming a multi-faceted approach to disease identification.

These diagnostic methodologies find their major applications across diverse healthcare settings, including widespread population-based screening programs aimed at asymptomatic women, targeted diagnostic assessments for individuals presenting with symptoms or abnormal screening results, and ongoing monitoring protocols for patients undergoing treatment or those with a history of precancerous lesions. The overarching benefits derived from a thriving cervical cancer diagnostics market are profound, leading to substantial reductions in disease incidence, significantly improved survival rates, and a decrease in mortality by enabling intervention at highly treatable stages. Early and accurate diagnosis not only saves lives but also enhances the quality of life for patients by facilitating less aggressive and more effective treatment options, preventing advanced disease progression and its associated morbidities.

Driving factors that continue to fuel the expansion and innovation within this vital market include the persistent and increasing global prevalence of HPV infection, a critical risk factor for cervical cancer. Concurrent with this is the success of public health campaigns that have significantly raised awareness about the importance of regular cervical cancer screening. Government initiatives worldwide, often supported by international health organizations, are actively promoting and funding national screening programs, especially in regions with high disease burden. Furthermore, the continuous stream of technological advancements, from highly automated cytology systems to sophisticated molecular assays and the burgeoning integration of artificial intelligence, is consistently enhancing the accuracy, efficiency, and accessibility of diagnostic solutions, ensuring the market remains dynamic and responsive to evolving clinical needs.

The Cervical Cancer Diagnostics Market is currently navigating a period of accelerated growth and transformative innovation, propelled by a convergence of global health imperatives and rapid technological progress. Key business trends underscore a strategic imperative among leading market players towards strengthening their competitive positions through targeted mergers, acquisitions, and collaborative partnerships. These strategic alliances are primarily aimed at expanding product portfolios, enhancing research and development capabilities, and extending geographical reach, with a particular emphasis on penetrating high-growth emerging markets. A significant paradigm shift is observed from traditional, labor-intensive cytology-based screening towards more precise, automated, and molecular diagnostic solutions, reflecting a broader industry move towards personalized medicine and improved diagnostic accuracy.

From a regional perspective, established markets such as North America and Europe continue to hold a substantial market share, primarily due to their advanced healthcare infrastructures, well-ingrained public health screening programs, and high adoption rates of cutting-edge diagnostic technologies. These regions benefit from significant investments in healthcare and a strong regulatory environment that fosters innovation. Conversely, the Asia Pacific region is rapidly emerging as a critical growth engine, poised for exponential expansion. This growth is underpinned by rising healthcare expenditures, a large and aging population, increasing incidence of cervical cancer, and proactive government support for preventative health initiatives and improved diagnostic access. Latin America, the Middle East, and Africa also present considerable, albeit nascent, market opportunities, driven by improving healthcare infrastructure and burgeoning awareness campaigns, though challenges related to affordability and accessibility of advanced diagnostics persist.

Analysis of market segments reveals that molecular diagnostics, particularly those focused on Human Papillomavirus (HPV) testing, are anticipated to experience the most significant growth trajectory. This is attributed to their superior sensitivity, specificity, and ability to identify high-risk HPV types, thereby enabling more effective risk stratification. The application segment for screening continues to represent the largest portion of the market, highlighting the enduring emphasis on preventive care and early detection. Furthermore, within end-use facilities, while hospitals remain a dominant segment, the increasing proliferation of specialized diagnostic laboratories and women's health clinics is markedly contributing to market expansion, driven by their specialized expertise and capacity to handle high volumes of diagnostic tests efficiently.

User inquiries surrounding the impact of Artificial Intelligence (AI) on the Cervical Cancer Diagnostics Market predominantly highlight the enthusiastic anticipation of AI's capabilities to significantly enhance diagnostic accuracy, dramatically streamline clinical workflows, and profoundly improve accessibility to screening and diagnostic services, especially within underserved and resource-constrained settings. Users frequently question how AI can integrate seamlessly into the interpretation of complex cytology and histology slides, offering consistent and objective analyses that potentially surpass human capabilities. The feasibility and efficacy of AI-driven remote screening solutions are also a major point of interest, along with the quantifiable benefits in terms of reducing human error rates and boosting overall operational efficiency in diagnostic laboratories globally.

Beyond the immediate clinical applications, there is considerable interest in exploring the broader implications of AI adoption. This includes delving into critical ethical considerations such as patient data privacy and security, navigating the intricate web of regulatory hurdles necessary for widespread AI tool deployment, and understanding the robust validation studies required to build unwavering trust among clinicians and patients alike. Furthermore, user concerns often touch upon the substantial initial investment costs associated with integrating sophisticated AI platforms and the imperative for comprehensive training programs to ensure healthcare professionals can effectively utilize these advanced tools. The overarching sentiment points to a collective desire to leverage AI as a transformative force, capable of democratizing access to high-quality diagnostics.

The core expectations from AI in this domain center around its ability to automate labor-intensive, repetitive tasks, thereby freeing up skilled personnel for more complex diagnostic challenges. AI is expected to identify subtle, early-stage patterns indicative of malignancy that might be imperceptible or easily overlooked by the human eye, thus enabling earlier and more precise interventions. Additionally, its capacity to provide highly personalized risk assessments based on vast datasets of patient history and diagnostic information is seen as a game-changer for preventative care. Ultimately, users envision AI as a powerful augmentative tool, designed to enhance rather than replace human expertise, fostering a synergistic diagnostic environment that yields quicker, more reliable results, and significantly contributes to global efforts in cervical cancer eradication.

The Cervical Cancer Diagnostics Market is significantly influenced by a dynamic interplay of propelling forces, restrictive elements, and emerging opportunities, all meticulously shaped by various intrinsic and extrinsic impact forces. The primary drivers underpinning market expansion include the escalating global burden of cervical cancer and Human Papillomavirus (HPV) infections, which necessitate widespread and effective screening. Concurrently, a surge in global awareness campaigns, coupled with proactive government-backed initiatives, is promoting regular screening and early diagnosis, driving demand for diagnostic solutions. Continuous technological advancements in molecular diagnostics, liquid-based cytology, and automated screening systems are further propelling market growth by offering more sensitive, specific, and efficient diagnostic solutions, enhancing early detection capabilities and significantly improving patient prognosis. Moreover, increasing healthcare expenditure in both developed and developing regions contributes directly to the expansion of diagnostic infrastructure and accessibility, especially through public health programs.

Despite these robust growth drivers, the market faces a formidable array of restraints. A significant barrier is the high cost associated with advanced diagnostic tests and specialized equipment, which can critically limit adoption, particularly in low-income and middle-income countries. The persistent lack of skilled healthcare professionals, including cytopathologists, gynecologists, and trained technicians, in many parts of the world poses a substantial challenge to the effective implementation and scaling of screening programs. Furthermore, deeply entrenched social stigma surrounding cervical cancer and HPV, alongside various cultural barriers, can significantly deter women from seeking timely and regular screening, thereby impacting early detection rates. Practical issues such as unacceptably high false positive or false negative rates in traditional screening methods can also lead to unnecessary patient anxiety, over-diagnosis, or, more critically, delayed diagnosis, thereby impacting patient trust and the optimal allocation of already strained healthcare resources.

Nevertheless, the market is rife with substantial opportunities for innovation and expansion. The rapid development and deployment of point-of-care (POC) diagnostics represent a transformative opportunity, offering quick results and enhanced accessibility, especially in remote or resource-limited areas where centralized laboratories are scarce. The burgeoning integration of artificial intelligence (AI) and machine learning (ML) for automated image analysis, predictive analytics, and enhanced diagnostic precision represents a monumental opportunity to improve efficiency and accuracy. Moreover, the expansion of organized screening programs in emerging economies, often supported by public-private partnerships aimed at reducing diagnostic costs and increasing reach, is expected to unlock vast new market potentials. The ongoing shift towards less invasive testing methods, such as liquid biopsy for the detection of circulating tumor DNA or other biomarkers, also presents a highly promising avenue for market diversification, enhanced patient comfort, and accelerated growth. The overall market trajectory is profoundly influenced by dynamic regulatory frameworks, evolving healthcare policy changes, and the prevailing global economic landscape affecting healthcare investments and public health priorities.

The Cervical Cancer Diagnostics Market is meticulously segmented across several critical dimensions to provide a granular and comprehensive understanding of its intricate structure and underlying dynamics. These segmentation categories encompass the specific type of diagnostic test employed, the clinical application area, the end-use facilities where these diagnostics are performed, and the underlying technological platforms that enable them. Each of these segments, individually and collectively, plays a pivotal role in shaping the overall market landscape, offering distinct growth opportunities and challenges that reflect the evolving paradigms in cervical cancer detection and prevention. This detailed analytical approach is essential for identifying key market drivers and restraints pertinent to specific product categories and user groups.

Understanding the market through these well-defined segments allows for the formulation of highly targeted market strategies, facilitates precision in product development to meet specific clinical requirements, and optimizes the allocation of resources by market players. For instance, the distinct needs of a large urban hospital differ significantly from those of a rural public health clinic, and segmentation helps to address these variances. By analyzing the growth rates and market shares of each segment, stakeholders can identify promising areas for investment, pinpoint competitive advantages, and uncover unmet diagnostic needs within the broader cervical cancer diagnostics ecosystem. This structured approach to market analysis is instrumental in fostering informed decision-making and strategic planning for both established multinational corporations and agile emerging innovators in the diagnostic field.

The continuous innovation within each segment, such as the evolution from conventional Pap smears to advanced molecular HPV testing or the integration of AI into imaging technologies, underscores the market's dynamic nature. This robust segmentation analysis not only provides a snapshot of the current market state but also offers forward-looking insights into future trends and potential disruptions, empowering companies to anticipate changes and adapt their strategies proactively. It also highlights the interconnectivity between segments, where advancements in one area, such as molecular technology, often spur innovation and demand in another, like screening applications or specialized diagnostic centers, thereby driving holistic market growth.

The value chain for the Cervical Cancer Diagnostics Market is a complex and interconnected network of activities that spans from raw material sourcing to the final delivery of diagnostic results to patients. The upstream segment of this chain is characterized by intensive research and development efforts, which are crucial for the discovery and validation of novel biomarkers and diagnostic assays. This stage involves specialized biotechnology companies and academic institutions focused on genomics, proteomics, and immunology. Concurrently, manufacturers of raw materials and core components, such as highly purified reagents, specialized chemical compounds, microfluidic chips, and precision optical components for diagnostic instruments, play a foundational role. These suppliers ensure the quality and consistency of inputs for diagnostic kit production and instrument manufacturing, thereby directly impacting the performance and reliability of downstream diagnostic products.

The midstream activities are dominated by the manufacturing, assembly, and quality control of complete diagnostic kits, instruments, and automated systems by major diagnostic companies. This stage involves sophisticated engineering, rigorous testing, and adherence to stringent regulatory standards to produce high-quality Pap test kits, HPV molecular diagnostic platforms, colposcopes, and biopsy tools. Following manufacturing, these finished products move into the distribution phase. This segment involves a robust network of logistics, warehousing, and sales operations. The distribution channels are critical for effectively reaching a diverse customer base, encompassing both direct sales forces that engage directly with large institutional clients and indirect channels that leverage distributors, wholesalers, and third-party logistics providers to reach smaller clinics and remote healthcare facilities, ensuring broad market penetration.

Downstream activities in the value chain primarily involve the actual deployment and execution of diagnostic tests at various healthcare provider settings. This includes hospitals, specialized oncology and gynecology clinics, independent diagnostic laboratories, and public health screening centers. These end-users utilize the diagnostic products and instruments to perform screening, confirm diagnoses, and monitor disease progression in patients. The effectiveness of this final stage heavily relies on the availability of skilled healthcare professionals—such as pathologists, cytotechnologists, and gynecologists—who are proficient in sample collection, laboratory analysis, result interpretation, and patient counseling. The value chain culminates with the delivery of accurate and timely diagnostic results to patients, which directly informs treatment decisions and ultimately contributes to improved patient outcomes and public health initiatives globally. The efficiency and integrity of each stage are paramount for the overall success and impact of the cervical cancer diagnostics market.

The potential customers and end-users within the Cervical Cancer Diagnostics Market are remarkably diverse, representing a broad spectrum of healthcare entities and professionals who collectively drive the demand for diagnostic products and services. At the forefront are hospitals, encompassing large tertiary care centers, specialized cancer hospitals, and dedicated women's health clinics. These institutions require a comprehensive suite of diagnostic solutions, ranging from routine cytological screening and advanced HPV molecular tests to more invasive procedures like colposcopy and tissue biopsies, to cater to their extensive patient populations. Hospitals often seek high-throughput, integrated diagnostic platforms that can seamlessly manage large volumes of samples and deliver rapid, accurate results, making them a significant purchasing segment.

Independent diagnostic laboratories and reference laboratories constitute another critical customer segment. These facilities specialize in processing a high volume of various medical tests, including cervical cancer diagnostics, for referring clinicians and smaller healthcare providers. Their demand is primarily for high-performance reagents, automated analytical equipment, and advanced molecular diagnostic kits that offer superior sensitivity and specificity. They prioritize efficiency, scalability, and adherence to stringent quality control and regulatory standards. Additionally, public health programs and government-funded screening initiatives, particularly prominent in developing countries, represent substantial buyers. These programs often focus on implementing widespread, cost-effective screening strategies at a population level, driving demand for accessible and scalable diagnostic tools that can be deployed across varied geographical and socioeconomic contexts.

Furthermore, a significant portion of the market includes private clinics, such as gynecologists' offices, family medicine practices, and primary care physicians. These clinics often serve as the first point of contact for women seeking routine check-ups and initial screenings. They predominantly utilize point-of-care tests or facilitate referrals for more advanced diagnostic procedures. Academic and research institutions also form an essential, albeit niche, customer base, primarily for cutting-edge molecular diagnostic technologies, research-grade reagents, and experimental assays employed in clinical trials, biomarker discovery, and the development of next-generation diagnostic modalities. Ultimately, the end-beneficiaries of these diagnostics are women globally, underscoring the vital role of timely, accurate, and accessible diagnostics in effective patient management, preventative healthcare, and global public health efforts to eradicate cervical cancer.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 6.2 Billion |

| Market Forecast in 2032 | USD 10.5 Billion |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Roche Diagnostics, Hologic Inc., Qiagen N.V., BD (Becton, Dickinson and Company), Abbott Laboratories, Siemens Healthineers AG, Quest Diagnostics Incorporated, Bio-Rad Laboratories Inc., Thermo Fisher Scientific Inc., Danaher Corporation, Sysmex Corporation, Seegene Inc., Enzo Biochem Inc., PerkinElmer Inc., CooperSurgical Inc., Eiken Chemical Co. Ltd., Femasys Inc., OncoHealth Corporation, GenMark Diagnostics Inc., Agilent Technologies Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Cervical Cancer Diagnostics Market is underpinned by an exceptionally dynamic and continuously evolving technological landscape, driven by the imperative to enhance diagnostic accuracy, improve efficiency, and expand accessibility of screening and confirmatory procedures. At the core of this landscape lies molecular diagnostics, a transformative field utilizing sophisticated techniques such as Polymerase Chain Reaction (PCR), real-time PCR, and Next-Generation Sequencing (NGS). These technologies enable highly sensitive and specific detection and genotyping of high-risk Human Papillomavirus (HPV), which is the primary etiologic agent for cervical cancer. The shift towards primary HPV screening, facilitated by these molecular methods, offers superior predictive value compared to traditional cytology alone, enabling more effective risk stratification and more targeted follow-up for patients. Advanced hybrid capture technologies also play a significant role by providing quantitative HPV DNA detection, further refining patient management strategies.

Beyond molecular approaches, significant and continuous advancements are revolutionizing the fields of cytology and imaging. Liquid-based cytology (LBC) has largely become the standard of care, offering substantial improvements over conventional Pap smears by providing better cell sample collection, preparation, and preservation, which in turn leads to clearer microscopic slides, reduced obscured results, and enhanced diagnostic yield. Colposcopy, a direct visual examination of the cervix, is increasingly being augmented with advanced imaging systems that incorporate digital cameras, high-resolution optics, and even AI-powered image analysis algorithms to assist clinicians in identifying suspicious areas with greater precision and objectivity. Furthermore, the burgeoning field of digital pathology, which involves the high-resolution digitization of conventional microscope slides, is facilitating remote consultation, enabling automated image analysis, and significantly improving workflow efficiency within diagnostic laboratories, particularly those managing high volumes of samples globally.

Emerging technologies, while some are still in their nascent stages for widespread cervical cancer diagnostics, hold immense promise for the future. Liquid biopsy, for instance, which involves the non-invasive detection of circulating tumor DNA (ctDNA), circulating tumor cells (CTCs), or other cancer-specific biomarkers from blood or other body fluids, represents a less intrusive and potentially more

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.