ID : MRU_ 429718 | Date : Nov, 2025 | Pages : 253 | Region : Global | Publisher : MRU

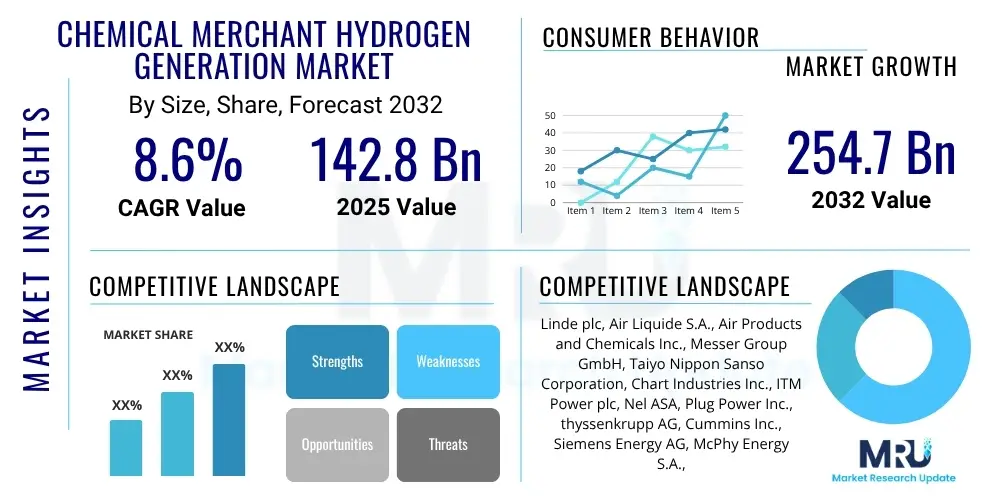

The Chemical Merchant Hydrogen Generation Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.6% between 2025 and 2032. The market is estimated at USD 142.8 billion in 2025 and is projected to reach USD 254.7 billion by the end of the forecast period in 2032.

The Chemical Merchant Hydrogen Generation Market encompasses the production and supply of hydrogen by third-party providers to various industrial end-users, rather than captive generation. This crucial sector provides a reliable and flexible source of high-purity hydrogen, a fundamental chemical commodity, to industries ranging from petroleum refining and chemical manufacturing to advanced electronics and food processing. The product, primarily hydrogen gas, is generated through diverse methods including well-established steam methane reforming (SMR), coal gasification, and increasingly, water electrolysis. These methods are chosen based on factors such as feedstock availability, cost considerations, desired purity levels, and environmental sustainability goals, ensuring a tailored supply solution for specific client operational requirements and technical specifications. Merchant hydrogen generation plays an absolutely vital role in enabling numerous industrial processes that critically rely on hydrogen as a key reactant, a clean fuel source, a reducing agent, or a carrier gas, thereby underpinning significant segments of the global industrial economy and strategically contributing to global energy security.

Major applications of merchant hydrogen span extensively across the industrial landscape. In petroleum refining, hydrogen is indispensable for hydrotreating to remove impurities like sulfur, nitrogen, and heavy metals from crude oil fractions, and for hydrocracking processes to convert heavier, less valuable hydrocarbons into lighter, higher-value products such as gasoline and jet fuel, enhancing both product quality and refinery economics. The chemical industry is another cornerstone, leveraging hydrogen for large-scale ammonia production, which is crucial for fertilizers, and for methanol synthesis, a versatile chemical building block essential for plastics, solvents, and fuel additives. Beyond these traditional heavy industrial uses, hydrogen is increasingly critical in metallurgy for annealing processes to improve material properties like ductility and strength, in the electronics industry for semiconductor manufacturing where ultra-high purity hydrogen is required for epitaxial growth and as a carrier gas, and in the food processing industry for the precise hydrogenation of edible oils and fats to produce margarines and shortenings. The benefits of sourcing merchant hydrogen are substantial, including significantly reduced capital expenditure for on-site generation facilities, enhanced operational flexibility through scalable supply agreements, guaranteed supply continuity from expert providers, and often, higher efficiency and lower environmental impact due to economies of scale at centralized, optimized production plants. This model allows industries to focus intensely on their core competencies and production while relying on specialized hydrogen suppliers for their critical gas needs.

Several potent driving factors are propelling the growth of this market. Foremost among them is the escalating global demand for cleaner fuels and chemicals, which positions hydrogen as a pivotal enabler of a sustainable future. Stringent environmental regulations and ambitious decarbonization targets set by governments and international bodies are pushing industries to adopt lower carbon footprint solutions, favoring hydrogen, especially green and blue variants. The continuous expansion of industrial production capacities across developing economies, particularly in Asia Pacific, further fuels the demand for merchant hydrogen. The global push towards hydrogen as a key enabler for the broader energy transition and decarbonization, particularly through "green" hydrogen initiatives powered by renewable energy and "blue" hydrogen incorporating carbon capture technologies, is creating unprecedented opportunities for merchant suppliers to significantly expand and diversify their offerings. Furthermore, ongoing technological advancements in production efficiency, storage solutions, and distribution logistics are consistently enhancing the market's overall attractiveness and economic viability. The unparalleled flexibility, specialized expertise, and scale offered by merchant hydrogen suppliers make them an indispensable and increasingly strategic partner within the industrial supply chain for this essential and transformative gas, supporting the transition towards a sustainable, low-carbon economy.

The Chemical Merchant Hydrogen Generation Market is currently experiencing a period of robust and transformative growth, propelled by a confluence of escalating industrial demand, aggressive global decarbonization mandates, and profound technological advancements in hydrogen production and delivery. Key business trends underscore a strategic and accelerating shift towards developing and deploying green and blue hydrogen solutions, signifying a critical evolution away from purely fossil-fuel-based generation. This involves substantial strategic investments in advanced electrolysis capacity, particularly in regions with abundant renewable energy resources, and the concurrent expansion of sophisticated, integrated gas supply networks designed to significantly enhance distribution efficiency and reliability. Leading companies within this dynamic market are increasingly forging strategic partnerships and collaborative ventures to jointly develop scalable, sustainable, and economically viable hydrogen solutions, which are essential for addressing the diverse and rapidly evolving end-user requirements across crucial sectors such as petroleum refining, chemical manufacturing, advanced electronics, and metallurgy. The market is intensely competitive, characterized by the dominant presence of established industrial gas giants alongside a growing cohort of innovative emerging players who are keenly focused on pioneering renewable hydrogen technologies and disrupting traditional supply chains. This competitive landscape fosters continuous innovation in sophisticated delivery models, bespoke purity levels, and comprehensive service offerings. A pronounced emphasis on securing long-term supply contracts and implementing highly competitive pricing strategies remains absolutely central to achieving and maintaining strong market positioning and securing sustainable revenue streams for merchant hydrogen providers.

From a regional perspective, Asia Pacific continues to assert its dominant position within the global merchant hydrogen generation market, primarily driven by its unparalleled pace of industrialization, the burgeoning and ever-increasing demand from its massive chemical manufacturing sector, and significant, sustained investments in advanced hydrogen production and distribution infrastructure, particularly evident in economic powerhouses like China, India, and other rapidly developing Southeast Asian nations. Europe is witnessing exceptionally strong growth, significantly spurred by its ambitious and progressive green hydrogen mandates, the strategic development of interconnected hydrogen valleys, and highly supportive regulatory frameworks explicitly designed to accelerate the achievement of net-zero emissions targets across the continent. North America's market remains fundamentally robust, underpinned by its well-established and mature petroleum refining and chemical sectors, coupled with an escalating interest and substantial investments in hydrogen for emerging applications such as fuel cell electric vehicles and widespread industrial decarbonization, extensively bolstered by substantial government incentives and private sector funding aimed at fostering a hydrogen economy. Latin America, the Middle East, and Africa are collectively demonstrating promising nascent growth, particularly through the initiation of groundbreaking green hydrogen projects that leverage their abundant renewable energy resources, positioning them as future exporters and significant consumers of clean hydrogen.

Regarding market segmentation, steam methane reforming (SMR) currently retains its position as the predominant hydrogen generation technology, primarily due to its proven cost-effectiveness, established operational expertise, and extensive existing infrastructure. However, its market share is increasingly and steadily being challenged by the rapid advancements and growing economic viability of electrolysis, as the costs of renewable energy continue their downward trend and policy support strengthens. Both liquid hydrogen and gaseous hydrogen delivery methods are critical components of the supply chain, with pipeline distribution gaining considerable traction for serving large industrial clusters requiring continuous, high-volume supply. While end-use applications in petroleum refining and ammonia production continue to hold the largest individual market shares, demand from innovative and emerging sectors like hydrogen mobility, utility-scale power generation, and green steel production is projected to drive substantial future growth and market diversification. The overarching trend observed across the market indicates a definitive transition towards more sustainable and environmentally friendly production methods, coupled with a significant expansion into diversified end-use applications, collectively ensuring the market's long-term expansion, resilience, and transformative potential within the global energy landscape.

Common user questions and profound industry concerns regarding Artificial Intelligence's (AI) transformative impact on the Chemical Merchant Hydrogen Generation Market frequently center on its potential to revolutionize operational efficiency, rigorously enhance safety protocols, accurately predict equipment failures, and fundamentally optimize complex supply chain logistics. Stakeholders are particularly keen to understand precisely how AI technologies can effectively reduce the often-significant operational costs inherent in energy-intensive production processes such as electrolysis or steam methane reforming (SMR). This cost reduction is envisioned through sophisticated real-time process control, advanced predictive maintenance strategies, and intelligent resource allocation. There is also substantial and growing interest in AI's pivotal role in seamlessly integrating intermittent renewable energy sources for large-scale green hydrogen production, encompassing sophisticated management of energy intermittency, real-time optimization of grid interaction, and intelligent energy storage solutions. Concerns frequently articulated include the substantial initial capital investment required for AI infrastructure, ensuring robust data security and privacy, and addressing the critical need for a highly skilled workforce proficient in implementing, managing, and continuously evolving AI solutions within this specialized industrial domain. Despite these challenges, expectations remain exceptionally high for AI to significantly accelerate global decarbonization efforts by rendering hydrogen generation demonstrably more efficient, profoundly reliable, consistently safe, and ultimately more economically viable across the entire value chain, from initial production to complex distribution and varied end-use applications.

The Chemical Merchant Hydrogen Generation Market is profoundly shaped by an intricate interplay of driving forces, significant restraining factors, and burgeoning opportunities, collectively forming a dynamic landscape of impact. Foremost among the key drivers is the escalating and diversified global demand for hydrogen across an ever-widening spectrum of industrial sectors. This demand originates not only from traditional heavy industries such as petroleum refining, petrochemicals, and general chemical manufacturing but also from rapidly emerging clean energy applications. The rigorous and pervasive global push for decarbonization, coupled with the ambitious transition towards a hydrogen economy championed by governments, international organizations, and leading corporations worldwide, is creating an unparalleled surge in the imperative for sustainable hydrogen solutions. This impetus is directly translating into substantial investments in merchant generation capacity, particularly for low-carbon hydrogen. Furthermore, continuous technological advancements across the entire hydrogen value chain, including more efficient production methods, innovative storage solutions, and enhanced distribution networks—especially in advanced electrolysis and carbon capture technologies—are progressively making merchant hydrogen more accessible, cost-effective, and environmentally attractive, thereby significantly expanding its market penetration and utility. The inherent strategic benefits for end-users of outsourcing their hydrogen supply, such as drastically reduced capital expenditure requirements, mitigated operational complexities, and access to specialized expertise, continue to be a foundational element underpinning robust market growth and adoption.

However, the market's trajectory is also tempered by notable restraints that present substantial challenges to its unrestrained expansion. A significant hurdle is the prohibitively high initial capital costs associated with establishing new, large-scale hydrogen generation plants, especially for cutting-edge green hydrogen facilities powered by renewable energy, and the concurrent necessity for developing extensive and complex distribution infrastructure. The inherent volatility in the prices of natural gas, which remains a primary and cost-sensitive feedstock for conventional steam methane reforming (SMR), introduces considerable cost uncertainty and margin pressure for merchant producers. Furthermore, legitimate safety concerns pertaining to the production, storage, and transportation of hydrogen, given its highly flammable nature and specific handling requirements, necessitate the implementation of exceptionally stringent regulatory frameworks and robust, multi-layered safety measures. These requirements invariably add to the operational costs and complexity of hydrogen logistics. Moreover, the absence of a fully developed, integrated, and expansive global hydrogen infrastructure for efficient, large-scale distribution remains a formidable challenge, particularly for nascent yet promising applications in hydrogen mobility and distributed power generation. The substantial energy intensity of certain hydrogen production methods also significantly impacts both the economic viability and the overall environmental sustainability profile of the generated hydrogen, demanding continuous innovation to reduce energy consumption.

Despite these challenges, the opportunities within the Chemical Merchant Hydrogen Generation Market are vast, transformative, and indicative of significant future growth. The accelerating global adoption of green and blue hydrogen production, synergized by rapidly declining costs of renewable energy and highly effective carbon capture technologies, presents immense and unprecedented growth potential for merchant suppliers. This transition allows for the creation of low-carbon hydrogen products that meet increasing environmental standards. The strategic expansion into a multitude of new, high-growth end-use sectors, such as fuel cells for sustainable transportation, hydrogen-powered electricity generation for grid balancing and industrial applications, and innovative green steel production processes, is progressively opening up entirely new and substantial revenue streams for hydrogen providers. Significant government and private sector investments in developing large-scale hydrogen hubs and interconnected pipeline networks are poised to fundamentally revolutionize hydrogen distribution, enabling far more efficient, reliable, and cost-effective supply to concentrated industrial clusters. Furthermore, continuous advancements in small-scale, modular, and on-site hydrogen generation technologies that can be flexibly deployed by merchant providers for specific niche applications offer tailored and localized supply solutions, enhancing market reach. The intensifying global focus on comprehensive energy security, industrial decarbonization, and long-term sustainability is unequivocally cementing hydrogen's pivotal role as a critical future energy carrier and industrial feedstock, thereby positioning the merchant hydrogen generation market at the absolute forefront of the global energy transition, with a strong, unwavering emphasis on delivering highly scalable, sustainable, and economically competitive hydrogen solutions.

The Chemical Merchant Hydrogen Generation Market is meticulously and extensively segmented to provide an extraordinarily comprehensive and nuanced understanding of its intricate dynamics and the diverse operational landscape it encompasses. These granular segmentations are absolutely crucial, as they allow for a highly detailed analysis of the multifaceted market drivers, inherent challenges, and profound opportunities that exist across a multitude of dimensions. These dimensions include the specific method of hydrogen generation employed, the chosen mode of delivery to end-users, the required purity level of the hydrogen, and the vast and expanding array of end-use applications across various industries. This granular breakdown is indispensable for all stakeholders, enabling them to precisely identify specific high-growth areas, formulate highly targeted and effective market strategies, and gain a profound understanding of the complex competitive environment within different, specialized niches of the expansive hydrogen supply chain. The comprehensive segmentation meticulously reflects both well-established, conventional trends and rapidly emerging, transformative developments within the market, ranging from traditional fossil fuel-based production methods to advanced, renewable energy-driven processes, thereby offering a holistic market perspective.

The value chain for the Chemical Merchant Hydrogen Generation Market constitutes a deeply integrated and highly complex network, meticulously organized to ensure the efficient and reliable delivery of hydrogen to industrial consumers. This comprehensive chain initiates with the critical sourcing of primary raw materials or energy inputs, progresses through sophisticated production, rigorous purification, and precise liquefaction processes, and ultimately extends to intricate distribution, secure storage, and the final, timely delivery to the diverse end-user base. The upstream activities are fundamentally concerned with the meticulous procurement of essential feedstocks, which include natural gas for conventional steam methane reforming (SMR), coal for gasification in specific regions, or critically, electricity and water for modern electrolysis. For the burgeoning sustainable hydrogen segment, this explicitly involves securing reliable and cost-effective renewable energy sources, such as wind, solar, and hydropower. The efficiency, cost-effectiveness, and environmental footprint of these upstream processes are paramount determinants of the final hydrogen cost and its overall market competitiveness. Furthermore, a network of specialized suppliers providing catalysts, advanced engineering equipment for reformers and electrolyzers, and cutting-edge carbon capture, utilization, and storage (CCUS) technologies also forms an integral and influential part of the upstream segment, directly impacting production capabilities, cost structures, and environmental sustainability credentials of the hydrogen generated.

Midstream operations embody the core of the merchant hydrogen generation process. This crucial stage involves the actual chemical or electrochemical production of hydrogen, followed by rigorous purification steps designed to meet various stringent industry and application-specific purity standards, and subsequent compression or cryogenic liquefaction for efficient storage and transportation. This phase necessitates substantial upfront capital investment in state-of-the-art production facilities, often integrating highly sophisticated engineering, automated control systems, and specialized operational expertise to ensure maximum efficiency, optimal yield, and uncompromised safety. Distribution channels then represent an absolutely crucial link connecting production to consumption, encompassing a strategic mix of direct and indirect methodologies. Direct distribution typically involves dedicated hydrogen pipelines, which are ideal for large-volume industrial consumers strategically located in close proximity to major production sites. These pipelines offer a continuous, highly cost-effective, and environmentally preferred supply solution. For smaller volumes, geographically dispersed customers, or temporary demand spikes, indirect distribution channels are employed, utilizing specialized tube trailers for compressed gaseous hydrogen or advanced cryogenic tankers for liquid hydrogen. These logistical operations demand highly specialized equipment, rigorous adherence to international safety regulations, and a robust, resilient, and perfectly coordinated transportation network to ensure safe and reliable delivery under varying conditions.

Downstream activities are exclusively focused on the precise delivery and integration of hydrogen into the diverse processes of end-user industries. These customers include but are not limited to, massive petroleum refineries, complex chemical manufacturing plants, precision metal fabricators, and advanced electronics producers. The final point of the value chain involves the effective and safe application of hydrogen within the client's specific operational processes. Beyond mere delivery, merchant hydrogen suppliers frequently extend their services to include comprehensive technical support, specialized advisory services, and collaborative engineering assistance, helping customers to optimally integrate hydrogen supply, maximize utilization efficiency, and seamlessly incorporate it into their complex production workflows. The broader value chain also encompasses a range of critical ancillary services, such as ongoing maintenance and repair of hydrogen systems, rigorous safety training for client personnel, and the development of highly customized hydrogen supply solutions tailored to unique industrial requirements. The relentless pursuit of efficiency and optimization across every single stage of this value chain is unequivocally paramount for merchant hydrogen providers to not only maintain a strong competitive edge but also to consistently ensure a reliable and uninterrupted supply, and critically, to meet the rapidly evolving and increasingly stringent demands for both conventional and, most importantly, low-carbon and green hydrogen solutions in a dynamic global market.

Rapidly emerging and dynamically growing customer segments are set to drive significant future expansion within the merchant hydrogen market. These include the food processing industry, which increasingly employs hydrogen for the precise hydrogenation of edible oils and fats to produce products such as margarines and shortenings with desired textures and shelf lives. The specialized glass manufacturing sector utilizes hydrogen in furnace atmospheres to prevent oxidation, control flame characteristics, and improve the overall quality and clarity of glass products. Furthermore, the burgeoning fuel cell and power generation markets, encompassing hydrogen-powered vehicles, stationary fuel cells for electricity generation, and grid-scale energy storage solutions, represent profoundly significant new avenues for demand. As the global energy transition accelerates decisively, various other industries are actively exploring hydrogen as a clean fuel source for transportation, industrial heating, and comprehensive industrial decarbonization efforts. This includes sectors such as green steel production, which aims to drastical

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 142.8 Billion |

| Market Forecast in 2032 | USD 254.7 Billion |

| Growth Rate | 8.6% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Key Companies Covered | Linde plc, Air Liquide S.A., Air Products and Chemicals Inc., Messer Group GmbH, Taiyo Nippon Sanso Corporation, Chart Industries Inc., ITM Power plc, Nel ASA, Plug Power Inc., thyssenkrupp AG, Cummins Inc., Siemens Energy AG, McPhy Energy S.A., Bloom Energy, Sumitomo Corporation, Ballard Power Systems Inc., Hyundai Mobis, FuelCell Energy Inc., Enapter AG, John Cockerill, Doosan Fuel Cell, H2scan LLC, Proton OnSite (a subsidiary of Nel ASA), Electrochaea GmbH, C-Zero Inc., Green Hydrogen Systems A/S, Sunfire GmbH, Kawasaki Heavy Industries, Ltd., Honeywell International Inc. (UOP), Shell plc (Hydrogen business), BP plc (Hydrogen projects), TotalEnergies SE (Hydrogen initiatives), ExxonMobil Corporation (Blue Hydrogen), Reliance Industries Limited, Mitsubishi Heavy Industries, Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Chemical Merchant Hydrogen Generation Market is fundamentally underpinned by a highly diverse, rapidly evolving, and technologically dynamic landscape, perpetually driven by the imperative for enhanced efficiency, superior scalability, unwavering reliability, and profound sustainability in all aspects of hydrogen production. Historically, steam methane reforming (SMR) has maintained its position as the singularly dominant and most established hydrogen generation technology. This process efficiently converts natural gas and steam into hydrogen gas while producing carbon dioxide as a by-product. Although SMR remains profoundly cost-effective and operationally mature, its inherent environmental footprint, stemming from greenhouse gas emissions, is an increasingly prominent and critical concern in the current global climate. This has, in turn, spurred the vigorous development and implementation of "blue hydrogen" initiatives, which strategically integrate advanced carbon capture, utilization, and storage (CCUS) technologies to significantly mitigate and reduce associated carbon emissions. Complementary technologies such as Autothermal Reforming (ATR) and Partial Oxidation (POX) also utilize various hydrocarbon feedstocks but offer distinct profiles in terms of energy efficiency, operational flexibility, and feedstock versatility. These conventional and carbon-abated methods, despite the environmental pressures, still account for the majority of merchant hydrogen supply globally due to their well-established infrastructure, proven operational reliability, and compelling economic viability, particularly for meeting large-scale, continuous industrial demand from sectors like refining and chemicals.

However, the technological frontier for hydrogen generation is undergoing a rapid and transformative shift, decisively moving towards water electrolysis as a cleaner and more sustainable alternative. This method precisely utilizes electricity to split water molecules into hydrogen and oxygen. Electrolysis is now central to the rapidly expanding production of "green hydrogen" when it is exclusively powered by renewable energy sources such as solar, wind, and hydropower, offering a zero-emission pathway. Key electrolysis technologies include Alkaline Water Electrolysis (AWE), which is mature, robust, and suitable for large-scale deployments; Proton Exchange Membrane (PEM) Electrolysis, known for its high efficiency, rapid response times, and compact footprint, making it exceptionally well-suited for dynamic integration with intermittent renewable energy sources; and Solid Oxide Electrolysis Cells (SOEC), which operate at higher temperatures and can achieve even greater electrical efficiencies, with potential for co-production of syngas and high-temperature waste heat utilization. Continuous and significant advancements in these electrolytic technologies are absolutely crucial for achieving the necessary large-scale commercialization of green hydrogen production, drastically reducing capital and operational costs, and ultimately enabling the realization of a fully decarbonized and sustainable hydrogen supply chain for the global merchant markets, thereby accelerating the broader energy transition.

The Chemical Merchant Hydrogen Generation Market refers to the specialized industrial sector where hydrogen gas is produced and supplied by independent, third-party companies directly to diverse industrial end-users. These end-users typically require consistent, high-purity hydrogen for their processes but prefer to outsource its generation rather than managing their own on-site production facilities. This model offers operational flexibility, cost efficiencies, and access to advanced technical expertise from dedicated suppliers, spanning sectors like refining, chemicals, electronics, and metallurgy, enabling industries to focus on their core business operations.

Merchant hydrogen is delivered through various sophisticated modes tailored to customer needs and volumes. Gaseous hydrogen is supplied in high-pressure cylinders or larger tube trailers for intermediate volumes, and critically, through dedicated pipelines for continuous, high-volume supply to industrial clusters, offering cost-effective and reliable delivery. Liquid hydrogen, which offers higher density, is transported in specialized cryogenic bulk tankers for large-scale, often remote, demand. Some suppliers also offer on-site generation models (Build-Own-Operate) directly at the customer's premises for dedicated, customized supply.

The market's growth is primarily driven by the escalating global demand for hydrogen across a multitude of industrial sectors, the strong impetus from stringent environmental regulations and ambitious decarbonization mandates worldwide, significant and continuous technological advancements in hydrogen production methods (particularly in electrolysis for green hydrogen), and the compelling operational and capital expenditure benefits that end-users derive from outsourcing their hydrogen supply to specialized providers. The global transition towards a hydrogen economy, coupled with energy security concerns, is a profound overarching driver.

Green hydrogen, produced through the electrolysis of water using exclusively renewable electricity (e.g., solar, wind), plays an increasingly pivotal and transformative role in the merchant market. It is central to global decarbonization efforts, offering a sustainable, zero-emission alternative to traditional fossil-fuel-based hydrogen. Its growing adoption is driven by falling renewable energy costs, supportive government policies, and increasing corporate sustainability commitments, creating vast new opportunities for merchant suppliers to meet escalating environmental mandates and diversified demand for clean energy solutions, fundamentally reshaping the market landscape towards sustainability and energy independence.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.