ID : MRU_ 427998 | Date : Oct, 2025 | Pages : 258 | Region : Global | Publisher : MRU

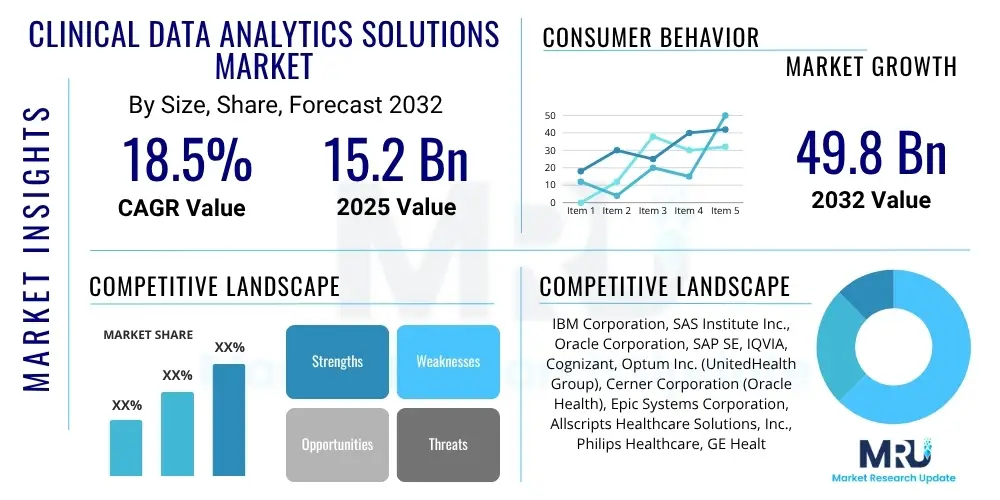

The Clinical Data Analytics Solutions Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2032. The market is estimated at USD 15.2 Billion in 2025 and is projected to reach USD 49.8 Billion by the end of the forecast period in 2032.

The Clinical Data Analytics Solutions Market encompasses a broad spectrum of technologies and services designed to collect, process, analyze, and interpret vast amounts of clinical data generated within healthcare ecosystems. This market addresses the critical need for converting raw, disparate clinical information into actionable insights that can drive improved patient outcomes, optimize operational efficiencies, accelerate drug discovery, and support evidence-based decision-making. These solutions leverage advanced analytical techniques, including machine learning, artificial intelligence, and statistical modeling, to extract valuable patterns, trends, and correlations from complex datasets. The primary objective is to move beyond simple data aggregation to sophisticated predictive and prescriptive analytics, enabling healthcare stakeholders to make informed choices that enhance healthcare delivery and research.

Products within this market range from specialized software platforms for electronic health record (EHR) data analysis, clinical trial management systems with integrated analytics, and population health management tools, to advanced business intelligence solutions tailored for pharmaceutical R&D and healthcare administration. These solutions are characterized by their ability to handle diverse data types, including patient demographics, medical histories, lab results, imaging data, genomic information, and real-world evidence (RWE). Major applications span across critical areas such as personalized medicine, where analytics guide tailored treatment plans; drug discovery and development, by accelerating clinical trials and identifying novel therapeutic targets; and operational efficiency in hospitals, through optimizing resource allocation and patient flow. The inherent complexity of clinical data, coupled with stringent regulatory requirements, necessitates highly specialized and robust analytical tools capable of ensuring data integrity, security, and compliance.

The substantial benefits derived from these solutions are multifaceted, driving their rapid adoption. For patients, these include more accurate diagnoses, personalized treatment strategies, and improved safety. Healthcare providers gain capabilities for predictive analytics to anticipate disease outbreaks, manage chronic conditions more effectively, and reduce readmission rates. For pharmaceutical and biotechnology companies, clinical data analytics significantly streamlines R&D processes, reduces the time and cost associated with drug development, and improves the success rates of clinical trials. Moreover, these solutions play a pivotal role in value-based care models, allowing healthcare systems to demonstrate quality of care and cost-effectiveness. The driving factors behind this market’s expansion are primarily the exponential increase in clinical data volume, the escalating demand for evidence-based medicine, the push for personalized healthcare, and continuous technological advancements in data science and artificial intelligence.

The Clinical Data Analytics Solutions Market is experiencing robust growth driven by the undeniable shift towards data-driven healthcare, presenting significant business opportunities across the value chain. Key business trends include the increasing investment in digital health infrastructure, strategic partnerships between technology providers and healthcare organizations, and a focus on integrating AI and machine learning capabilities into existing analytical platforms. There is a growing demand for cloud-based solutions due to their scalability, flexibility, and cost-effectiveness, enabling broader access to advanced analytics even for smaller healthcare providers. Furthermore, the market is witnessing consolidation through mergers and acquisitions as companies seek to expand their product portfolios, acquire specialized expertise, and gain a larger market share. Value-based care models are compelling providers to adopt analytics to measure outcomes and demonstrate efficiency, further fueling market expansion.

Regionally, North America continues to dominate the market due to its advanced healthcare infrastructure, significant R&D investments, and early adoption of innovative technologies. The presence of major market players, stringent regulatory frameworks encouraging data utilization, and a high volume of chronic diseases contribute to its leading position. Europe follows with substantial growth, particularly in countries like Germany and the UK, driven by government initiatives for digital health transformation and increasing awareness of the benefits of data analytics in improving public health. The Asia Pacific region is emerging as the fastest-growing market, propelled by rapidly expanding healthcare expenditure, a large patient pool, increasing adoption of electronic health records, and government efforts to modernize healthcare systems, especially in countries like China and India. Latin America, the Middle East, and Africa are also showing nascent but promising growth, primarily focusing on addressing health disparities and improving basic healthcare infrastructure through data-driven approaches.

Segment-wise, the market sees significant activity across various components, deployment models, applications, and end-users. The software segment, particularly advanced analytics and business intelligence tools, holds the largest share, constantly evolving with new algorithms and functionalities. Cloud-based deployment models are projected to witness the highest CAGR, reflecting the industry's move towards more agile and scalable solutions. In terms of applications, drug discovery and development remain a critical area, leveraging analytics to accelerate research and reduce time to market. However, precision medicine and population health management are rapidly gaining traction as healthcare systems prioritize individualized care and proactive disease prevention. Among end-users, pharmaceutical and biotechnology companies are primary adopters due to their extensive data generation and the high stakes involved in R&D, while healthcare providers are increasingly investing in analytics to enhance patient care and operational efficiency, driven by complex patient data and rising administrative burdens.

The integration of Artificial Intelligence (AI) and Machine Learning (ML) has fundamentally reshaped the landscape of clinical data analytics, moving it beyond descriptive reporting to sophisticated predictive and prescriptive capabilities. Common user questions often revolve around AI's ability to enhance diagnostic accuracy, personalize treatment protocols, accelerate drug discovery, and streamline clinical operations. Users are keenly interested in how AI can process vast, complex, and heterogeneous clinical datasets—ranging from electronic health records (EHRs) and medical imaging to genomic sequences and real-world evidence—to uncover subtle patterns and insights that human analysis might miss. There's a strong expectation that AI will address critical challenges such as data overload, interoperability issues, and the need for faster, more precise decision-making in high-stakes healthcare environments. Concerns frequently arise regarding data privacy, algorithmic bias, the 'black box' nature of certain AI models, and the ethical implications of autonomous decision-making in patient care, alongside the practicalities of implementation and integration with existing systems.

Summarizing these themes, users primarily seek to understand AI's transformative potential in improving clinical outcomes, operational efficiency, and research velocity, while simultaneously navigating the inherent complexities and risks associated with its deployment. The core expectation is that AI will provide a significant competitive advantage and a paradigm shift in how clinical data is leveraged, moving from retrospective analysis to proactive intervention and personalized health management. Healthcare professionals anticipate AI's role in augmenting their capabilities, reducing diagnostic errors, and enabling more targeted therapies. Researchers foresee AI expediting the identification of biomarkers, optimizing clinical trial designs, and predicting drug efficacy and safety profiles. However, these positive outlooks are tempered by a cautious approach regarding data governance, ethical considerations, and the necessity for robust validation of AI models to ensure patient safety and equitable care. The market's current trajectory is heavily influenced by the ongoing development and deployment of explainable AI (XAI) and privacy-preserving AI techniques to address these user concerns.

AI's influence is seen as pivotal in unlocking the full value of clinical data, particularly in an era characterized by exponential data growth and the imperative for precision medicine. It acts as a force multiplier, enabling analytics solutions to move beyond mere data visualization to truly intelligent systems that can learn, adapt, and make recommendations. This transformative impact spans across early diagnosis, disease progression prediction, treatment optimization, and even resource allocation within healthcare systems. The ability of AI algorithms to identify complex correlations within multi-modal data, such as connecting genetic predispositions with environmental factors and treatment responses, is driving a new era of insights. This translates into more effective clinical workflows, reduced costs associated with trial failures, and ultimately, a more proactive and patient-centric healthcare model. The market is witnessing a surge in AI-powered tools that offer sophisticated functionalities, making clinical data analytics indispensable for modern healthcare. The continuous evolution of AI techniques, from deep learning to natural language processing, is creating new avenues for extracting value from unstructured clinical notes and scientific literature, further amplifying its impact.

The Clinical Data Analytics Solutions Market is profoundly influenced by a complex interplay of Drivers, Restraints, and Opportunities, collectively forming the Impact Forces that shape its trajectory. A primary driver is the astronomical growth in the volume and complexity of clinical data, encompassing everything from electronic health records and medical imaging to genomic sequences and real-world patient data. This data deluge necessitates advanced analytical tools to extract meaningful insights, moving healthcare towards a more evidence-based and personalized approach. Concurrently, the increasing demand for personalized medicine and precision therapies fuels the need for solutions that can analyze individual patient data to tailor treatments. Technological advancements in AI, machine learning, and big data processing are continually enhancing the capabilities of these solutions, making them more powerful and accessible. Regulatory pressures, particularly from government bodies mandating improved patient outcomes, cost-effectiveness, and data-driven decision-making, also serve as a significant catalyst for adoption. Furthermore, the inherent need for operational efficiency within healthcare systems, facing rising costs and resource constraints, drives the adoption of analytics to optimize workflows, manage patient populations, and reduce administrative burdens. The global health crises have further underscored the urgency of robust data analytics for disease surveillance, response, and vaccine development, adding another layer of impetus.

Despite these powerful drivers, several restraints pose challenges to market growth. Data privacy and security concerns remain paramount, with stringent regulations like HIPAA and GDPR requiring robust safeguards for sensitive patient information, which can complicate data sharing and integration. Interoperability issues between disparate healthcare IT systems are a significant hurdle, making it difficult to consolidate and analyze data from various sources effectively. The high upfront implementation costs associated with advanced analytics platforms, including software, hardware, and integration services, can deter smaller healthcare organizations and those with limited budgets. Moreover, a persistent shortage of skilled professionals—data scientists, clinical informaticians, and AI experts—capable of developing, deploying, and managing these complex solutions limits widespread adoption. Resistance to change within traditional healthcare settings, coupled with a lack of understanding regarding the full potential of data analytics, also impedes market penetration. Addressing these restraints requires concerted efforts in standardization, talent development, and demonstrating clear return on investment (ROI).

Opportunities within the Clinical Data Analytics Solutions Market are abundant and diverse, promising continued expansion and innovation. The growing emphasis on real-world evidence (RWE) and real-world data (RWD) for regulatory decision-making, drug development, and post-market surveillance presents a massive opportunity for advanced analytics to synthesize insights from routine clinical practice. The rapid expansion of telehealth and remote patient monitoring services, especially catalyzed by recent global events, generates new streams of data that require sophisticated analytics for effective management and personalized care delivery. The continuous evolution and increasing sophistication of predictive and prescriptive analytics offer new avenues for proactive healthcare interventions, disease prevention, and resource optimization. Furthermore, the market has significant potential for expansion into new therapeutic areas and emerging markets, where healthcare infrastructure is developing, and there is a high demand for efficient, data-driven solutions. Integration with other transformative technologies like the Internet of Medical Things (IoMT) and wearable devices will unlock even richer datasets and more granular insights, creating a highly interconnected and intelligent healthcare ecosystem. These opportunities, when strategically pursued, can overcome existing restraints and propel the market into new frontiers of innovation and value creation.

The Clinical Data Analytics Solutions Market is comprehensively segmented across various dimensions to provide a detailed understanding of its dynamics, adoption patterns, and growth opportunities. These segmentations allow for a granular analysis of how different components, deployment models, applications, and end-users contribute to the overall market landscape, highlighting areas of high growth and innovation. The market's complexity necessitates a multi-faceted approach to segmentation, reflecting the diverse needs and operational structures of healthcare stakeholders. This structured view enables market players to tailor their offerings more effectively, identify niche markets, and develop targeted strategies for growth and competitive differentiation. Each segment represents distinct technological preferences, functional requirements, and investment capacities, collectively painting a holistic picture of the market's current state and future potential.

The value chain for the Clinical Data Analytics Solutions Market is intricate and involves several critical stages, spanning from data generation and aggregation to the delivery of actionable insights and their application in clinical practice. The upstream segment of the value chain primarily focuses on the creation and initial collection of raw clinical data. This includes data generated from electronic health records (EHRs) in hospitals and clinics, laboratory information systems (LIS), imaging modalities (PACS), genomic sequencing platforms, clinical trial management systems (CTMS), remote monitoring devices, and various other healthcare IT systems. Key players in this upstream segment are healthcare providers, diagnostic centers, pharmaceutical companies conducting trials, and technology vendors specializing in data capture hardware and software. The efficiency and accuracy of data collection at this stage are paramount, as they directly impact the quality of downstream analytics. Challenges often revolve around data fragmentation, varying data standards, and the sheer volume of unstructured data that needs to be digitized and organized for subsequent analysis.

Moving downstream, the value chain encompasses data integration, processing, storage, and the core analytics activities. This segment is dominated by specialized clinical data analytics solution providers, big data technology companies, and cloud service providers. Data from diverse sources is first aggregated, cleaned, and standardized to ensure consistency and usability. This often involves significant data engineering efforts, including ETL (Extract, Transform, Load) processes, to prepare data for analytical models. The actual analytical phase involves applying advanced algorithms, including AI and machine learning techniques, to identify patterns, correlations, and predictive insights. Companies in this segment develop and offer sophisticated software platforms, analytical tools, and consulting services that transform raw data into intelligence. The output of this stage includes predictive models for disease progression, patient risk stratification, treatment efficacy analysis, and operational efficiency metrics. The ability to integrate these insights seamlessly back into clinical workflows is a key differentiator, influencing the overall value proposition of these solutions.

The distribution channel for clinical data analytics solutions is primarily direct, with solution providers engaging directly with end-user organizations such as pharmaceutical companies, hospitals, and research institutions. This direct approach allows for tailored solutions, extensive customization, and dedicated support, crucial for complex enterprise-level deployments. Sales teams, clinical specialists, and implementation consultants work closely with clients to understand their specific needs and integrate the solutions into their existing IT infrastructure and clinical workflows. However, an increasing number of indirect channels are emerging, including partnerships with system integrators, value-added resellers (VARs), and cloud marketplace providers. These indirect channels help extend market reach, particularly to smaller healthcare organizations or those seeking bundled IT solutions. Strategic alliances with electronic health record (EHR) vendors are also becoming increasingly common, embedding analytics capabilities directly within widely used clinical systems. Both direct and indirect channels play vital roles in facilitating market access and ensuring the successful adoption and utilization of clinical data analytics solutions across the diverse healthcare ecosystem.

The Clinical Data Analytics Solutions Market serves a broad and diverse range of potential customers, all driven by the common imperative to leverage data for improved decision-making, efficiency, and patient outcomes within the healthcare sector. At the forefront are pharmaceutical and biotechnology companies, which represent a significant segment of end-users. These organizations rely heavily on clinical data analytics throughout the entire drug discovery and development lifecycle, from identifying novel drug targets and optimizing preclinical research to designing and managing complex clinical trials, conducting pharmacovigilance, and performing post-market surveillance. For them, analytics solutions are critical for reducing R&D costs, accelerating time to market for new therapies, enhancing drug safety profiles, and demonstrating clinical effectiveness to regulatory bodies. The ability to analyze vast genomic, proteomic, and patient trial data enables them to pursue precision medicine initiatives and develop highly targeted therapies, positioning data analytics as an indispensable tool for innovation and competitive advantage.

Another major segment of potential customers comprises healthcare providers, including hospitals, integrated delivery networks (IDNs), clinics, and large health systems. These entities are increasingly adopting clinical data analytics to address multifaceted challenges related to patient care, operational efficiency, and financial sustainability. For healthcare providers, analytics solutions are instrumental in improving diagnostic accuracy, developing personalized treatment plans, managing chronic diseases more effectively, and reducing readmission rates. They also utilize these solutions for population health management, identifying at-risk patient cohorts, and implementing proactive interventions. Operationally, analytics aids in optimizing resource allocation, such as bed management, staff scheduling, and supply chain logistics, leading to reduced costs and improved patient flow. Furthermore, financial departments leverage these tools for revenue cycle management, claims processing, and identifying billing anomalies, making analytics a cornerstone of modern hospital administration and patient-centric care delivery.

Beyond pharmaceutical companies and healthcare providers, the market extends to other crucial stakeholders in the healthcare ecosystem. Contract Research Organizations (CROs) are significant adopters, using clinical data analytics to support their clients in pharmaceutical and biotech industries by optimizing clinical trial design, managing trial data, and expediting regulatory submissions. Academic and research institutions utilize these solutions for groundbreaking medical research, public health studies, epidemiological analysis, and training the next generation of healthcare professionals and data scientists. Medical device companies leverage analytics for product development, performance monitoring of devices, post-market surveillance, and ensuring regulatory compliance. Furthermore, government and payer organizations (e.g., health insurance companies, national health services) are increasingly adopting clinical data analytics for policy formulation, public health initiatives, fraud detection, and managing healthcare expenditures. Each of these customer segments seeks robust, scalable, and secure analytical solutions tailored to their specific data types, operational contexts, and strategic objectives, highlighting the broad applicability and growing demand across the entire healthcare spectrum.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 15.2 Billion |

| Market Forecast in 2032 | USD 49.8 Billion |

| Growth Rate | 18.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | IBM Corporation, SAS Institute Inc., Oracle Corporation, SAP SE, IQVIA, Cognizant, Optum Inc. (UnitedHealth Group), Cerner Corporation (Oracle Health), Epic Systems Corporation, Allscripts Healthcare Solutions, Inc., Philips Healthcare, GE Healthcare, Siemens Healthineers, Verily Life Sciences, Medidata Solutions (Dassault Systèmes), Explorys (IBM), Health Catalyst, Tableau Software (Salesforce), Cloudera, Inc., Databricks |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Clinical Data Analytics Solutions Market is underpinned by a dynamic and continuously evolving technology landscape, leveraging a convergence of advanced computing paradigms to process, analyze, and interpret complex healthcare data. At its core, the ecosystem relies heavily on Big Data technologies, which are essential for handling the immense volume, velocity, and variety of clinical information generated daily. This includes distributed file systems like Hadoop and NoSQL databases, providing scalable storage and processing capabilities for diverse data types such as structured EHR data, unstructured clinical notes, medical images, and genomic sequences. These foundational technologies enable the efficient ingestion and management of data from disparate sources, laying the groundwork for more sophisticated analytical operations. Furthermore, data warehousing and data lake solutions are crucial for consolidating and organizing this information into accessible formats, facilitating comprehensive analysis across an entire patient population or research cohort. The ability to manage and query petabytes of clinical data efficiently is a non-negotiable requirement for modern clinical analytics platforms, driving continuous innovation in data infrastructure.

Artificial Intelligence (AI) and Machine Learning (ML) algorithms constitute the intelligence layer of the clinical data analytics landscape, empowering solutions to move beyond descriptive analysis to predictive and prescriptive insights. This includes a wide array of techniques such as deep learning for image and natural language processing (NLP) to extract insights from clinical notes, supervised learning for disease prediction and risk stratification, and unsupervised learning for identifying hidden patterns in patient cohorts. NLP is particularly critical for processing the vast amounts of unstructured text data found in clinical documentation, converting it into machine-readable formats for analysis. Computer vision techniques are extensively applied to medical imaging (e.g., X-rays, MRIs, CT scans) to assist in diagnosis, disease progression monitoring, and treatment planning. The integration of advanced statistical modeling further enhances the rigor and reliability of these analytical outputs, enabling robust evidence generation. The continuous advancements in AI/ML, coupled with increased computational power, are pushing the boundaries of what is possible in areas like personalized medicine, drug discovery, and population health management, transforming raw data into actionable intelligence at an unprecedented scale.

Beyond core Big Data and AI/ML, several other crucial technologies shape the clinical data analytics market. Cloud computing platforms (e.g., AWS, Azure, Google Cloud) are becoming the preferred deployment model, offering unparalleled scalability, flexibility, and cost-effectiveness for managing and processing large datasets. This shift to the cloud facilitates collaboration, enables remote access to analytical tools, and accelerates the development and deployment of new solutions. Data visualization tools and interactive dashboards are also vital components, translating complex analytical results into intuitive, easily understandable formats for clinicians, researchers, and administrators. Technologies focused on data governance, security, and privacy, such as encryption, anonymization, tokenization, and blockchain for secure data sharing, are non-negotiable given the sensitive nature of clinical data and stringent regulatory requirements. Furthermore, interoperability standards and APIs (Application Programming Interfaces) are critical for seamless integration of analytics solutions with existing EHRs, laboratory systems, and other healthcare IT infrastructure, ensuring a unified data ecosystem. The convergence and continuous evolution of these technologies define the advanced capabilities and future direction of the Clinical Data Analytics Solutions Market, fostering innovation for better healthcare outcomes.

The Clinical Data Analytics Solutions Market exhibits significant regional variations in terms of adoption rates, market size, and growth drivers, reflecting disparities in healthcare infrastructure, regulatory environments, technological readiness, and economic development. North America, particularly the United States, stands as the dominant market, driven by its highly advanced healthcare system, substantial investments in R&D, and the early adoption of cutting-edge technologies. The presence of a large number of key market players, coupled with stringent regulatory frameworks that encourage the use of data for quality improvement and patient safety, further propels market growth in this region. High healthcare expenditures, a growing prevalence of chronic diseases, and a strong emphasis on personalized medicine and value-based care models also contribute to the robust demand for clinical data analytics solutions across North America. The region benefits from a mature IT infrastructure and a highly skilled workforce, facilitating the seamless integration and utilization of complex analytical platforms.

Europe represents the second largest market for clinical data analytics solutions, demonstrating steady growth fueled by increasing awareness of the benefits of data-driven healthcare, significant government initiatives for digital health transformation, and a rising focus on population health management. Countries such as Germany, the United Kingdom, France, and the Nordics are leading the adoption curve, driven by national health strategies aimed at improving efficiency, reducing costs, and enhancing patient outcomes through data insights. The implementation of strict data protection regulations like GDPR has also prompted organizations to invest in robust data governance and analytics solutions to ensure compliance while leveraging data for research and care. The region is also characterized by a strong academic and research base, fostering innovation in clinical data science. However, challenges related to data interoperability across different national health systems and varying levels of digital maturity across member states can sometimes impede faster market expansion.

The Asia Pacific (APAC) region is emerging as the fastest-growing market for clinical data analytics solutions, projected to witness substantial expansion throughout the forecast period. This rapid growth is attributable to several factors, including burgeoning healthcare expenditures, the increasing prevalence of lifestyle diseases, a massive patient population, and the accelerating adoption of electronic health records (EHRs) and other digital health technologies. Countries like China, India, Japan, and South Korea are making significant investments in modernizing their healthcare infrastructure and promoting data-driven initiatives. Government support for healthcare IT, coupled with the rising demand for affordable and quality healthcare, is creating fertile ground for market expansion. While challenges related to data privacy regulations and a nascent IT infrastructure in some parts of the region persist, the sheer scale of opportunity and the rapid pace of technological absorption make APAC a critical growth engine. Latin America, the Middle East, and Africa (MEA) are also experiencing nascent but promising growth, driven by efforts to improve basic healthcare access, manage infectious diseases, and leverage technology to address health disparities, with increasing investment in digital health solutions.

Clinical data analytics solutions are advanced software and service platforms that collect, process, analyze, and interpret vast amounts of clinical data from various sources. These solutions transform raw healthcare information into actionable insights, enabling healthcare providers, pharmaceutical companies, and researchers to make informed decisions, improve patient outcomes, optimize operations, and accelerate medical advancements through predictive and prescriptive analytics.

AI revolutionizes clinical data analytics by enabling more accurate diagnoses, personalized treatment plans, accelerated drug discovery, and enhanced operational efficiencies. AI algorithms, including machine learning and deep learning, process complex data like medical images, genomics, and EHRs to uncover hidden patterns, predict disease progression, identify at-risk populations, and automate data extraction from unstructured clinical notes, significantly augmenting human capabilities.

Key challenges in adopting clinical data analytics include stringent data privacy and security concerns, significant interoperability issues between disparate healthcare IT systems, high upfront implementation costs, and a persistent shortage of skilled data scientists and clinical informaticians. Additionally, resistance to change within traditional healthcare settings and the complexity of integrating new solutions with existing workflows often hinder widespread adoption.

The primary beneficiaries are pharmaceutical and biotechnology companies, who use analytics for drug discovery, clinical trials, and pharmacovigilance; healthcare providers (hospitals, clinics) for improving patient care, operational efficiency, and population health management; and academic/research institutions for medical research and public health studies. Patients ultimately benefit from more accurate diagnoses, personalized treatments, and enhanced overall healthcare delivery.

Future trends include the increasing integration of AI and machine learning for predictive and prescriptive analytics, a growing emphasis on real-world evidence (RWE) for drug development and regulatory decisions, expansion of cloud-based deployment models for scalability, and enhanced interoperability across healthcare systems. Additionally, the market will see greater adoption of analytics for personalized medicine, remote patient monitoring, and leveraging data from wearables and IoMT devices.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.