ID : MRU_ 428453 | Date : Oct, 2025 | Pages : 257 | Region : Global | Publisher : MRU

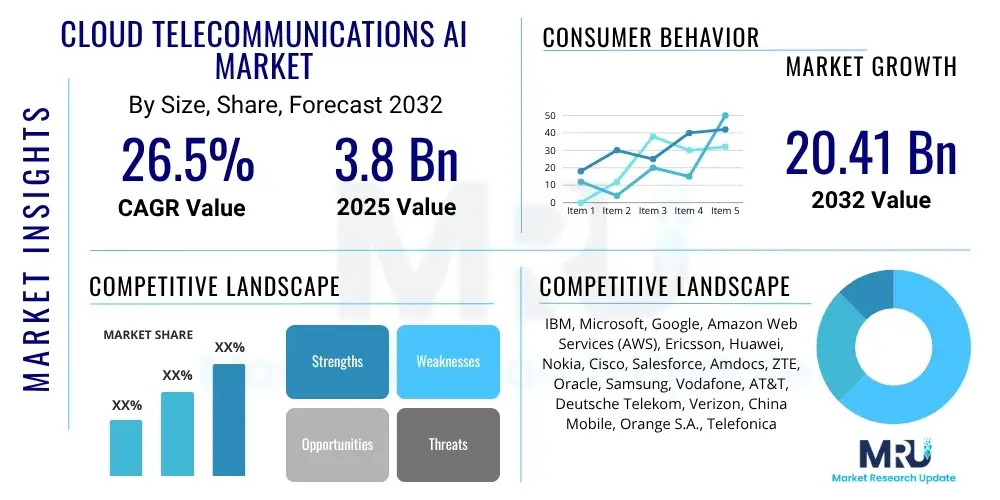

The Cloud Telecommunications AI Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 26.5% between 2025 and 2032. The market is estimated at USD 3.8 Billion in 2025 and is projected to reach USD 20.41 Billion by the end of the forecast period in 2032.

The Cloud Telecommunications AI Market integrates artificial intelligence capabilities with cloud computing infrastructure specifically for the telecommunications sector. This synergy enhances network operations, customer service, and business intelligence, driving innovation and efficiency across various telecom services. The market encompasses a wide array of AI-powered solutions deployed over cloud platforms, ranging from predictive analytics for network maintenance to intelligent virtual assistants for customer engagement, and sophisticated algorithms for fraud detection. These solutions leverage the scalability and flexibility of cloud environments to process vast amounts of data, enabling telecom operators to make data-driven decisions and optimize their service offerings.

Key products within this market include AI-driven network management systems, intelligent contact center solutions, predictive analytics platforms for churn reduction, and AI-enabled security tools. Major applications span across network infrastructure optimization, customer experience management, service provisioning, and operational efficiency improvements. The primary benefits derived from the adoption of Cloud Telecommunications AI include significant cost reductions through automation, enhanced network reliability, personalized customer experiences, and the ability to rapidly deploy new services. These advantages are crucial for telecommunications companies seeking to maintain competitiveness in an increasingly digital and demanding market landscape.

Driving factors for this market's robust growth include the accelerating global adoption of 5G technology, which necessitates more intelligent and adaptive network management; the proliferation of IoT devices generating massive volumes of data requiring real-time analysis; the continuous migration of telecom workloads to cloud environments for agility and scalability; and the rising demand for enhanced customer experience and personalized services. Furthermore, the increasing complexity of network operations and the imperative to reduce operational expenditures are compelling telecom providers to invest in AI and cloud solutions, thereby fueling market expansion.

The Cloud Telecommunications AI market is experiencing significant momentum, driven by a confluence of technological advancements and strategic business imperatives. Key business trends include the strong emphasis on digital transformation initiatives within the telecom sector, leading to increased investment in AI-powered cloud solutions for automation, efficiency, and new service development. Service providers are increasingly leveraging AI to transform their network operations, enhance customer engagement through personalized interactions, and develop new revenue streams from data-driven insights. Partnerships between cloud providers, AI specialists, and telecommunication companies are becoming more prevalent, fostering innovation and accelerating solution deployment. The shift towards a software-defined, virtualized network infrastructure further amplifies the need for AI to manage complex, dynamic environments effectively.

Regionally, North America and Europe currently hold the largest market shares due to early adoption of cloud technologies, advanced telecom infrastructure, and substantial investments in R&D for AI solutions. However, the Asia Pacific (APAC) region is projected to exhibit the highest growth rate during the forecast period, propelled by rapid 5G rollouts, extensive digitalization programs, and a burgeoning base of mobile and internet users. Countries like China, India, and South Korea are at the forefront of this growth, with significant government and private sector investments in AI and cloud infrastructure. Latin America, the Middle East, and Africa are also emerging as promising markets, driven by improving digital infrastructure and increasing demand for advanced telecommunication services.

In terms of segment trends, the solutions segment, particularly network optimization and customer experience management, is expected to dominate the market due to the immediate and measurable benefits offered to telecom operators. Within deployment models, hybrid cloud solutions are gaining traction, allowing operators to balance scalability with control and data security. The growing adoption of predictive maintenance and fraud detection applications is also contributing significantly to market growth, addressing critical operational and financial challenges faced by telecom companies. The continuous evolution of AI algorithms and the increasing availability of robust cloud platforms are enabling more sophisticated and impactful applications across all segments.

Users are keen to understand how AI specifically revolutionizes various facets of cloud telecommunications, ranging from operational efficiency and network reliability to personalized customer experiences and robust security measures. Common inquiries revolve around AI's ability to automate complex network management tasks, predict and prevent service outages, optimize resource allocation for 5G and IoT, and significantly enhance customer interactions through intelligent automation. There is also considerable interest in AI's role in detecting fraudulent activities and improving network security, alongside concerns regarding data privacy, ethical AI deployment, and the potential impact on human employment within the sector. Users expect AI to deliver tangible benefits in cost reduction, service quality improvement, and the enablement of innovative telecom services.

The Cloud Telecommunications AI Market is profoundly shaped by a dynamic interplay of driving forces, restraining factors, and emerging opportunities, all collectively contributing to its overall impact. Drivers such as the global rollout of 5G technology, which demands intelligent network management, and the exponential growth in data traffic from IoT devices are pushing telecom operators to adopt AI in the cloud for enhanced efficiency and scalability. The increasing emphasis on digital transformation, coupled with the need to optimize operational costs and enhance customer satisfaction through personalized services, further propels market expansion. These factors create a compelling case for the integration of AI within cloud-based telecom infrastructure, promising significant improvements in performance and service delivery across the board.

However, the market also faces notable restraints. High initial investment costs for AI implementation and cloud migration can be prohibitive for some smaller operators, while the complexity of integrating diverse AI solutions with legacy telecom systems presents significant technical challenges. Data privacy concerns and stringent regulatory compliance requirements, particularly in regions like Europe with GDPR, pose considerable hurdles for AI deployment and data utilization. Moreover, the scarcity of skilled professionals with expertise in both AI and telecommunications technology can impede adoption and effective management of these advanced systems, limiting the pace of innovation and deployment within the industry.

Despite these challenges, abundant opportunities exist for growth and innovation. The emergence of edge AI, which processes data closer to the source, offers significant potential for reducing latency and enhancing real-time applications, particularly critical for 5G and autonomous systems. Developing highly personalized services and creating new data-driven revenue streams through advanced analytics present lucrative avenues for market players. Furthermore, the continuous advancements in AI algorithms and cloud computing technologies are enabling more sophisticated and efficient solutions, creating a positive feedback loop for market development. The evolving competitive landscape and shifting customer expectations for seamless and intelligent services also act as powerful impact forces, compelling operators to innovate or risk losing market share.

The Cloud Telecommunications AI Market is comprehensively segmented across various dimensions to provide a detailed understanding of its structure, growth trajectories, and areas of innovation. These segmentations allow for a granular analysis of market dynamics, identifying key areas of investment, technological adoption, and end-user demand. The market is typically broken down by components, deployment models, specific applications, and the types of end-users it serves, each category revealing distinct trends and opportunities within the evolving telecommunications landscape. Understanding these segments is crucial for stakeholders to develop targeted strategies and capitalize on the most promising areas of growth.

The value chain for the Cloud Telecommunications AI market is intricate, involving multiple stages from fundamental technology development to end-user service delivery. At the upstream level, the chain begins with hardware manufacturers providing powerful servers and networking equipment, semiconductor companies developing AI chips and processors, and core software developers creating AI algorithms, machine learning frameworks, and cloud operating systems. These foundational elements are critical for building the robust infrastructure necessary to support AI computations and cloud-based telecom applications. Specialized AI research entities and startups also play a vital role in innovating new algorithms and models, contributing to the core intelligence of the solutions.

Moving downstream, cloud service providers (CSPs) like AWS, Microsoft Azure, and Google Cloud offer the scalable infrastructure and platforms where these AI solutions are hosted and executed. Telecom operators then integrate these AI-powered cloud platforms into their networks to enhance various aspects of their operations, from network management and service optimization to customer engagement. System integrators and independent software vendors (ISVs) are crucial intermediaries, providing customization, integration services, and specialized applications tailored to the unique needs of different telecom companies. These downstream players are responsible for the practical implementation and operationalization of AI within telecommunication environments.

Distribution channels for Cloud Telecommunications AI solutions are diverse, encompassing both direct and indirect approaches. Direct sales involve large cloud providers and AI solution vendors engaging directly with major telecom operators and large enterprises through dedicated sales teams and strategic accounts. This approach allows for highly customized solutions and direct technical support. Indirect channels are equally significant, leveraging a network of channel partners, value-added resellers (VARs), and system integrators. These partners often bring industry-specific expertise, local market understanding, and additional services such like consulting and deployment, making complex solutions more accessible to a broader range of telecom service providers and enterprises, including smaller and medium-sized players.

The primary potential customers and end-users for Cloud Telecommunications AI solutions are predominantly telecommunication service providers, encompassing a wide spectrum of operators. This includes major Mobile Network Operators (MNOs) that manage extensive wireless infrastructure, Fixed Network Operators (FNOs) offering broadband and landline services, and Mobile Virtual Network Operators (MVNOs) that leverage existing network infrastructure. These entities are continually seeking ways to optimize their networks, reduce operational costs, enhance customer experiences, and introduce innovative new services, making AI-powered cloud solutions highly attractive for their strategic objectives. The imperative for digital transformation and competitive differentiation drives their adoption of these advanced technologies.

Beyond traditional telecom operators, Cloud Service Providers (CSPs) themselves represent a significant customer segment. As they host and enable these AI solutions, they also integrate AI within their own infrastructure to manage their cloud resources more efficiently, optimize data centers, and offer enhanced services to their telecom clients. Furthermore, large enterprises with substantial in-house communication requirements or those heavily reliant on robust, intelligent telecommunication services for their business operations are also emerging as key buyers. This includes sectors such as finance, healthcare, manufacturing, and logistics, where efficient and intelligent communication infrastructure is paramount for business continuity and innovation.

The increasing complexity of network management, the proliferation of data from 5G and IoT, and the growing demand for personalized and proactive customer service are compelling these diverse customer segments to invest in Cloud Telecommunications AI. Their objective is to leverage AI’s predictive capabilities, automation, and analytical power to gain a competitive edge, improve service quality, and achieve operational excellence. Consequently, solution providers in this market must tailor their offerings to address the specific pain points and strategic goals of these varied customer profiles, ensuring scalability, security, and seamless integration with existing infrastructures.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 3.8 Billion |

| Market Forecast in 2032 | USD 20.41 Billion |

| Growth Rate | 26.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | IBM, Microsoft, Google, Amazon Web Services (AWS), Ericsson, Huawei, Nokia, Cisco, Salesforce, Amdocs, ZTE, Oracle, Samsung, Vodafone, AT&T, Deutsche Telekom, Verizon, China Mobile, Orange S.A., Telefonica |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Cloud Telecommunications AI market is characterized by a sophisticated convergence of artificial intelligence disciplines, advanced cloud computing architectures, and cutting-edge networking protocols. At its core, the market heavily relies on various Machine Learning (ML) techniques, including supervised, unsupervised, and reinforcement learning, to process vast datasets for predictive analytics, pattern recognition, and decision-making. Deep Learning (DL) models, particularly neural networks, are increasingly prevalent for complex tasks such as natural language processing (NLP) for chatbots and virtual assistants, and computer vision for network monitoring and security applications. These AI models are crucial for enabling autonomous network operations and intelligent customer interactions.

The underlying infrastructure is powered by robust cloud computing platforms, primarily public, private, and hybrid cloud environments, which provide the scalability, flexibility, and computational resources necessary for running AI workloads. Technologies such as containerization (e.g., Docker, Kubernetes) and serverless computing are vital for deploying and managing AI applications efficiently in the cloud. Furthermore, the integration of Edge AI is becoming critical, allowing AI processing to occur closer to the data source at the network edge, thereby reducing latency, optimizing bandwidth usage, and enhancing real-time responsiveness, which is essential for 5G and IoT applications in telecommunications. This distributed intelligence paradigm represents a significant technological advancement.

Beyond core AI and cloud components, the market leverages a suite of related technologies. Big data analytics platforms are indispensable for ingesting, processing, and analyzing the enormous volumes of data generated by telecom networks and customer interactions. Natural Language Processing (NLP) is paramount for understanding and generating human language, facilitating intelligent customer service and sentiment analysis. Robotic Process Automation (RPA) plays a role in automating routine back-office tasks, complementing AI's analytical capabilities. Furthermore, advanced cybersecurity frameworks are integrated to protect sensitive data and AI models from threats, ensuring the integrity and reliability of cloud telecommunications AI systems. The continuous evolution of these technologies drives the innovation and expansion of the market.

Cloud Telecommunications AI refers to the integration of artificial intelligence technologies with cloud computing platforms to enhance, automate, and optimize various operations and services within the telecommunications industry. It encompasses AI-powered solutions deployed on cloud infrastructure for network management, customer service, fraud detection, and more.

The main benefits include improved operational efficiency, significant cost reductions through automation, enhanced network reliability and performance, personalized customer experiences, and stronger security measures against fraud and cyber threats. It also enables faster deployment of new services and data-driven decision-making.

Key players driving innovation and market growth include major cloud providers like IBM, Microsoft, Google, and AWS, alongside telecommunications equipment and software vendors such as Ericsson, Huawei, Nokia, Cisco, and Amdocs.

Challenges include high initial implementation costs, complex integration with legacy telecom systems, concerns over data privacy and regulatory compliance (e.g., GDPR), and a shortage of skilled professionals with expertise in both AI and telecommunications.

The market is projected for robust growth, driven by the expansion of 5G, increasing adoption of IoT, and a growing demand for intelligent automation. Future trends include greater integration of edge AI, hyper-personalized services, and the development of new data-driven revenue streams for telecom operators.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.